Table of Contents

Overview

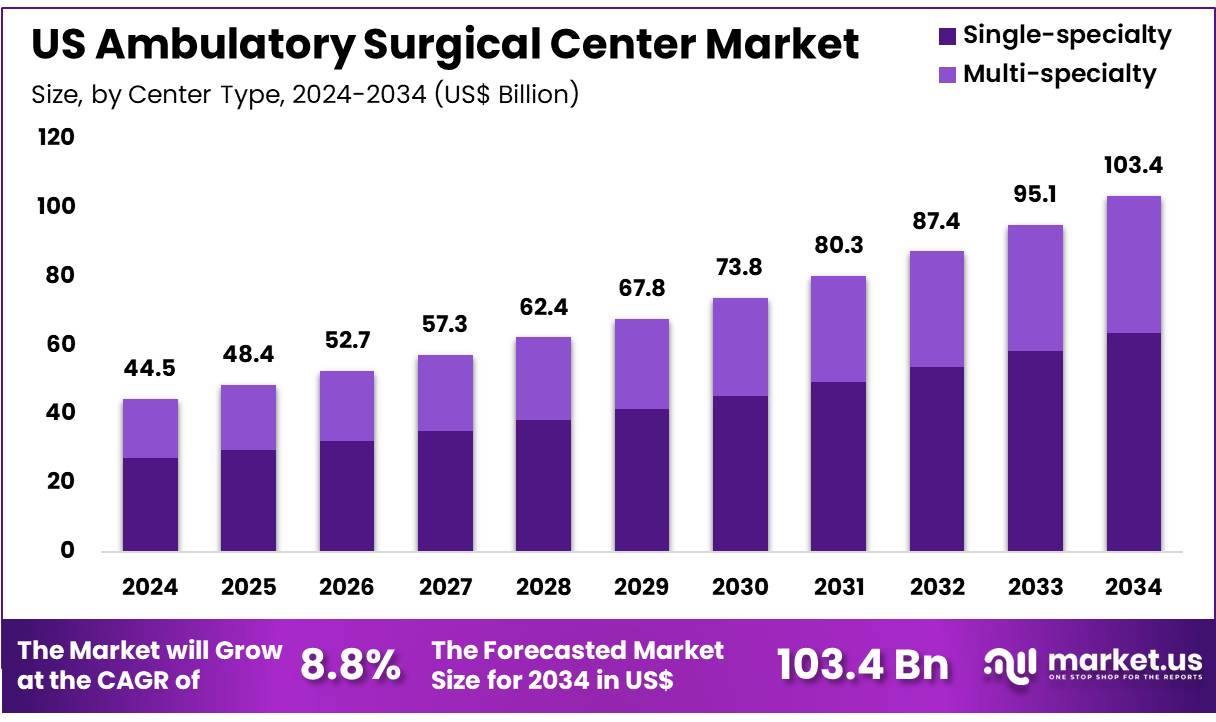

New York, NY – Dec 08, 2025 – The US Ambulatory Surgical Center Market size is expected to be worth around US$ 103.4 Billion by 2034 from US$ 44.5 Billion in 2024, growing at a CAGR of 8.8% during the forecast period 2025 to 2034.

The U.S. Ambulatory Surgical Center (ASC) market has been characterized by consistent expansion, driven by the increasing shift of surgical procedures from inpatient hospitals to cost-efficient outpatient settings. Growth has been supported by rising demand for minimally invasive surgeries, favorable reimbursement structures, and continuous advancements in surgical technologies. The market value has been strengthened by the need for reduced hospital stays and lower overall healthcare spending.

A significant rise in chronic conditions, including orthopedic, cardiovascular, and gastrointestinal disorders, has contributed to the growing procedure volume in ASCs. The adoption of advanced diagnostic and surgical equipment has enhanced precision and reduced recovery time, further supporting patient preference for outpatient care. Regulatory encouragement toward value-based healthcare has also accelerated ASC utilization across the country.

Independent and physician-owned centers continue to represent a major share of the market, although joint ventures with hospitals and private equity groups have increased steadily. These partnerships have been undertaken to expand service capacity, improve infrastructure, and enhance financial sustainability. The market landscape has also been influenced by the growing consolidation trend, which has been undertaken to strengthen operational efficiency and negotiate favorable payer contracts.

Overall, the U.S. ASC market is positioned for stable growth, supported by technological progress, favorable economic factors, and increasing adoption of outpatient surgical services. The market outlook remains positive as healthcare providers continue to prioritize accessibility, cost-efficiency, and improved patient outcomes.

Key Takeaways

- In 2024, the U.S. ambulatory surgical center market generated revenue of US$ 44.5 billion, recorded a CAGR of 8.8%, and is projected to reach US$ 103.4 billion by 2033.

- Based on center type, the market is segmented into single-specialty and multi-specialty, with single-specialty centers leading in 2024 with a 61.4% share.

- By ownership, the market is categorized into physician-owned, hospital-owned, and corporate-owned, where physician-owned centers accounted for 57.9%, marking the largest share.

- In terms of specialty, the market is divided into orthopedics, pain management/spinal injections, gastroenterology, ophthalmology, and others, with orthopedics emerging as the leading segment and holding 45.2% of total revenue in 2024.

Segmentation Analysis

- Center Type Analysis: In 2024, single-specialty ambulatory surgical centers represented 61.4% of the market. Their growth was supported by patient preference for focused, cost-effective care and strong expertise in areas such as orthopedics and ophthalmology. The increasing adoption of minimally invasive procedures, combined with demand for convenience and rapid recovery, reinforced this segment’s momentum. As healthcare systems emphasize operational efficiency, single-specialty centers are expected to maintain steady expansion due to their streamlined and specialized service models.

- Ownership Analysis: Physician-owned ambulatory surgical centers accounted for 57.9% of the market in 2024. This model enabled physicians to maintain greater control over scheduling, care delivery, and financial management. Lower administrative burdens and enhanced autonomy continued to attract healthcare professionals toward this structure. Rising outpatient procedure volumes in key specialties, supported by strong patient satisfaction and favorable regulatory trends, are anticipated to drive sustained growth of physician-owned ASCs in the coming years.

- Specialty Analysis: The orthopedics segment dominated the U.S. ASC market with a 45.2% revenue share in 2024. Increased demand for outpatient orthopedic procedures including joint replacements and spine surgeries was propelled by a growing burden of musculoskeletal disorders and an aging population. Advances in minimally invasive techniques further enabled safe and efficient outpatient delivery. As cost-effective, high-quality care remains a priority, orthopedic-focused ASCs are expected to experience continued expansion supported by procedural efficiency and reduced patient recovery times.

Emerging Trends

Steady Payment Rate Increases: For calendar year (CY) 2025, a 2.9 % increase in Ambulatory Surgical Center (ASC) payment rates has been finalized for facilities that comply with quality reporting requirements. This adjustment corresponds to the 3.4 % hospital market basket increase, reduced by a 0.5 % productivity factor. The continuation of such payment updates is expected to support capital investment, equipment modernization, and service line expansion without weakening care standards.

Enhanced Quality Reporting Measures

Refinements to the ASC Quality Reporting (ASCQR) Program include the introduction of two additional outcome-based metrics:

- ASC-17: All-cause unplanned hospital visits within seven days following orthopedic procedures.

- ASC-18: The same metric applied to urology procedures.

These measures, applicable for CY 2022 payment determinations and beyond, are designed to strengthen patient safety oversight and promote improved post-procedural care pathways.

Integration of Remote Services: Under the CY 2023 Outpatient Prospective Payment System and ASC Payment Systems final rule, select remote mental health services delivered in patients’ homes became reimbursable as ASC services. This policy highlights the broader integration of telehealth into ambulatory care, enabling virtual pre-operative assessments and post-operative follow-ups, which can enhance patient convenience and reduce on-site congestion.

Sustained High Utilization of ASCs: Historical data from the CDC indicate that 28.6 million ambulatory surgery visits occurred nationwide in 2010, with freestanding ASCs performing 12.9 million of these visits (45 %). Although dated, these figures illustrate the sustained role of ASCs in managing nearly half of outpatient surgical volume, reaffirming their importance in modern healthcare delivery.

Use Cases

- High-Volume Endoscopic Procedures: ASCs have demonstrated strong capacity for high-throughput endoscopic services. In 2010, an estimated 4.0 million large-intestine and 2.2 million small-intestine endoscopies were performed in these facilities. Centers also conducted 2.9 million lens extractions and 2.9 million spinal canal injections. The ability to complete such minimally invasive procedures in significantly shorter timeframes than hospital outpatient departments continues to be a core operational advantage.

- Cataract Surgery: Lens-related procedures represented more than 5.5 million ASC-based surgeries in 2010, combining 2.9 million extractions and 2.6 million prosthetic insertions. Dedicated ophthalmic teams and optimized clinical workflows enable ASCs to support high surgical volumes while maintaining strong safety and patient satisfaction outcomes.

- Tribal and IHS Outpatient ASC Services: Indian Health Service (IHS) and tribal hospitals, operating outside the standard Outpatient Prospective Payment System, receive an outpatient Ambulatory Inpatient Rate (AIR) of US $667 per encounter in the lower 48 states for CY 2024. These facilities have increasingly expanded their portfolios to include higher-cost and complex services—such as cancer-related treatments using ASC-like delivery models to improve access in rural and underserved areas.

- Orthopedic and Urology Day Surgeries: The inclusion of ASC-17 and ASC-18 in federal quality reporting has encouraged more centers to strengthen their focus on same-day orthopedic and urology procedures, such as joint injections, minor fracture repairs, and cystoscopies. Early data suggest that unplanned hospital visit rates within seven days remain below 2 % in accredited ASCs, indicating effective patient selection criteria and robust peri-operative management protocols.

Frequently Asked Questions on US Ambulatory Surgical Center

- What is an Ambulatory Surgical Center (ASC)?

An Ambulatory Surgical Center is a specialized healthcare facility where outpatient surgical procedures are performed. These centers are designed to improve efficiency, reduce wait times, and offer cost-effective alternatives to hospital-based surgeries across various specialties. - How does an ASC differ from a hospital outpatient department?

An ASC focuses exclusively on planned outpatient procedures, enabling faster patient turnover and improved scheduling. Hospital outpatient departments handle broader clinical needs and emergencies, which can increase complexity, cost structures, and patient wait times compared with ASCs. - What types of procedures are commonly performed in ASCs?

ASCs typically conduct same-day procedures in orthopedics, gastroenterology, ophthalmology, pain management, and ENT. These procedures are selected due to predictable recovery times, lower complication risks, and the ability to discharge patients safely within hours. - Why are ASCs gaining popularity in the United States?

Growth is supported by technological advancements, minimally invasive techniques, and favorable insurance reimbursement trends. Patients prefer ASCs due to convenience, lower costs, and shorter stays, while physicians benefit from improved control over scheduling and clinical workflows. - What safety standards must ASCs follow?

ASCs adhere to federal and state regulatory requirements, accreditation standards, and clinical protocol guidelines. These include infection control measures, equipment maintenance, emergency preparedness, and regular quality assessments to ensure patient safety and procedural reliability. - Which specialties dominate the US ASC market?

Orthopedics, gastroenterology, ophthalmology, and pain management hold leading shares due to high procedure volumes and compatibility with minimally invasive approaches. These specialties benefit strongly from predictable recovery pathways and high patient throughput within ASC environments. - What opportunities exist for ASC market expansion?

Opportunities arise from expanding reimbursement support for outpatient surgeries, technological innovations, and growing interest from investors. Increased patient preference for cost-effective care and the shift toward value-based models strengthen long-term prospects for ASC market development.

Conclusion

The U.S. ambulatory surgical center market is expected to maintain steady expansion, supported by rising demand for minimally invasive procedures, favorable reimbursement policies, and continued technological advancement. Strong utilization across orthopedics, gastroenterology, and ophthalmology, combined with growth in physician-owned facilities and single-specialty centers, reinforces market stability.

Ongoing regulatory support, integration of remote services, and consolidation among providers further strengthen operational efficiency and patient outcomes. As healthcare systems prioritize cost-effective, accessible, and high-quality outpatient care, ASCs are positioned to play an increasingly central role in the nation’s surgical delivery landscape over the coming decade.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)