Table of Contents

Overview

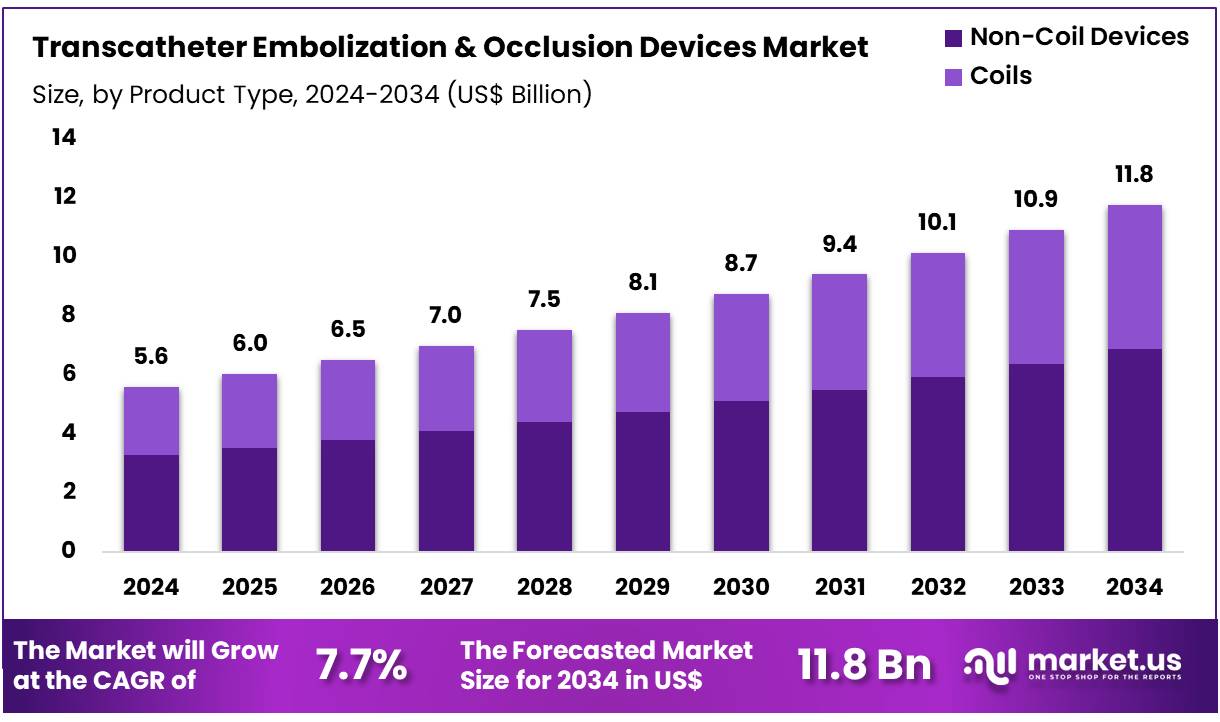

New York, NY – Dec 18, 2025 – Global Transcatheter Embolization & Occlusion Devices Market size is expected to be worth around US$ 11.8 Billion by 2034 from US$ 5.6 Billion in 2024, growing at a CAGR of 7.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.5% share with a revenue of US$ 2.2 Billion.

Transcatheter embolization and occlusion devices play a critical role in modern interventional radiology and cardiology by enabling minimally invasive treatment of a wide range of vascular and non‑vascular conditions. These devices are designed to intentionally block blood flow within targeted vessels, supporting the management of hemorrhage, aneurysms, arteriovenous malformations, tumors, and structural heart defects.

The technology is commonly delivered through catheter based procedures, which allow precise placement under image guidance. Key device categories include embolic coils, vascular plugs, particles, liquid embolics, and occlusion balloons. The use of these devices has increased steadily due to their ability to reduce procedural risks, shorten hospital stays, and improve patient recovery outcomes compared to traditional surgical interventions.

Clinical adoption is being supported by continuous innovation in device materials, enhanced radiopacity, improved deliverability, and greater procedural control. The integration of advanced imaging techniques has further strengthened the accuracy and safety of embolization and occlusion procedures. As a result, these devices are increasingly utilized across applications such as oncology, trauma care, peripheral vascular disease, and congenital heart defect management.

The growth of transcatheter embolization and occlusion devices can be attributed to rising demand for minimally invasive treatments, expanding indications, and increasing prevalence of chronic vascular disorders. Ongoing clinical research and regulatory approvals are expected to support broader adoption across healthcare systems globally.

Overall, transcatheter embolization and occlusion devices represent a vital component of modern interventional therapies, contributing to improved clinical efficiency and patient centered care.

Key Takeaways

- In 2024, the transcatheter embolization & occlusion devices market generated revenue of US$ 5.6 billion and is projected to expand at a CAGR of 7.7%, reaching US$ 11.8 billion by 2034.

- By product type, the market is categorized into non-coil devices and coils, with non-coil devices leading in 2024 by accounting for 58.5% of the total market share.

- Based on application, the market is segmented into oncology, peripheral vascular disease, neurology, urology, and others. Among these, oncology emerged as the largest segment, capturing a 47.2% share.

- In terms of end users, the market includes hospitals, ambulatory surgical centers, and others, with hospitals dominating the landscape and contributing 60.7% of overall revenue.

- North America remained the leading regional market in 2024, holding a 38.5% market share.

Regional Analysis

The transcatheter embolization and occlusion devices market in North America accounted for a substantial 38.5% revenue share in 2024, reflecting strong market expansion during the year. This growth was largely driven by the rising prevalence of conditions requiring minimally invasive treatment, including aneurysms, peripheral artery disease (PAD), and oncology-related interventions.

Technological advancements have improved procedural precision, safety, and clinical outcomes, further accelerating adoption. PAD remains a major global health concern, particularly among aging populations. According to a study published in BMC Public Health in May 2025, approximately 113 million individuals aged 40 years and above were living with PAD globally in 2019, highlighting a large addressable patient base.

The increasing preference for minimally invasive procedures, due to reduced recovery times and lower complication risks, continues to support market growth. Key manufacturers reported strong performance in 2024, with Boston Scientific’s Cardiovascular segment recording 27.4% organic growth, while Penumbra, Inc. achieved US$1,194.6 million in revenue, up 12.9% year on year.

The Asia Pacific market is projected to register the highest CAGR over the forecast period. Growth is being supported by rising cardiovascular disease incidence, increasing healthcare spending, and expanding adoption of advanced interventional technologies. Government initiatives, infrastructure development, and the expansion of global medtech companies are collectively strengthening market potential across the region.

Key use cases

- Stop severe gastrointestinal (GI) bleeding when endoscopy fails

- Where used: Non-variceal upper GI bleeding (e.g., bleeding ulcers) when endoscopy cannot control bleeding.

- Devices used: Coils, particles, liquid embolics, glue.

- Numeric signals: Severe bleeding despite endoscopy happens in ~5%–10% of patients, creating a direct need for embolization as the next step.

- Control life-threatening bleeding after pelvic trauma

- Where used: Pelvic fracture bleeding in trauma care.

- Devices used: Coils, gelfoam (temporary), particles, plugs.

- Numeric signals: Technical success for pelvic fracture embolization is often reported as ~90%–100% in clinical literature.

- Emergency control of postpartum hemorrhage (PPH) to avoid hysterectomy

- Where used: Severe bleeding after delivery when medical measures fail.

- Devices used: Particles, gelfoam, coils (depending on anatomy and bleeding point).

- Numeric signals: In one clinical series, pelvic arterial embolization success was ~89.6% (with failures leading to surgical options).

- Treat uterine fibroids with a minimally invasive option (Uterine Fibroid Embolization / UFE)

- Where used: Symptomatic fibroids (heavy bleeding, pain, pressure symptoms).

- Devices used: Microspheres/particles (most common), sometimes coils as adjuncts.

- Numeric signals (population driver): Fibroids occur in ~50%–70% of females by menopause, reaching >80% in Black women. This large patient pool sustains procedure volume and device demand.

- Pre-surgical devascularization of brain arteriovenous malformations (AVMs)

- Where used: Neurointerventions before surgery to reduce bleeding risk and simplify resection.

- Devices used: Liquid embolics (e.g., Onyx), glue systems.

- Numeric signals (regulatory): Onyx is FDA-approved for presurgical embolization of brain AVMs. ([FDA Access Data][7])

- Also relevant: N-butyl cyanoacrylate (NBCA) liquid embolic systems have FDA approval for embolization of cerebral AVMs when presurgical devascularization is desired.

- Treat benign kidney tumors (renal angiomyolipoma) and prevent rupture

- Where used: Symptomatic tumors or high-risk lesions; emergency rupture control.

- Devices used: Particles, coils, liquid embolics.

- Numeric signals: A meta-analysis reported a ~43.3% average tumor size reduction after embolization; post-embolization syndrome was reported around 54% (important for hospital protocols and product selection).

Frequently Asked Questions on Transcatheter Embolization & Occlusion Devices

- What types of embolization and occlusion devices are commonly used?

Common device types include coils, vascular plugs, liquid embolics, particles, and occlusion balloons, each selected based on vessel size, flow dynamics, anatomy, and clinical indication to ensure durable occlusion while minimizing non-target embolization risks. - What are the major clinical applications of these devices?

These devices are widely used in oncology, trauma, gastroenterology, neurology, and cardiology to manage tumors, hemorrhage, arteriovenous malformations, aneurysms, and congenital defects, offering effective therapy when surgery is high-risk or contraindicated. - What benefits do transcatheter embolization and occlusion devices offer?

Key benefits include reduced procedural trauma, shorter hospital stays, faster recovery, lower complication rates, and the ability to treat complex vascular conditions through precise, catheter-based approaches under real-time imaging guidance. - What risks are associated with embolization and occlusion procedures?

Potential risks include non-target embolization, vessel perforation, infection, and device migration; however, careful patient selection, advanced imaging, and experienced operators significantly reduce adverse event rates in routine clinical practice settings. - What does the transcatheter embolization and occlusion devices market include?

The transcatheter embolization and occlusion devices market comprises sales of devices used in minimally invasive vascular interventions, with growth driven by rising chronic diseases, expanding interventional radiology adoption, and preference for minimally invasive treatments globally. - Which regions dominate the market, and why?

North America and Europe dominate due to advanced healthcare systems and early technology adoption, while Asia-Pacific shows fastest growth, supported by large patient pools, improving hospitals, and increasing investments in interventional cardiology and radiology services. - How is the competitive landscape characterized?

The market is moderately consolidated, featuring global medical device companies focusing on product innovation, portfolio expansion, clinical evidence generation, and strategic partnerships to strengthen competitive positioning and address diverse procedural requirements across specialties.

Conclusion

Transcatheter embolization and occlusion devices have become integral to modern interventional care, offering effective, minimally invasive solutions across a broad range of vascular and non-vascular conditions. Market expansion is being driven by rising procedural volumes, technological innovation, and growing preference for catheter-based therapies over surgery.

Strong adoption in oncology, trauma, and cardiovascular applications continues to support revenue growth, particularly in North America, while Asia Pacific is emerging as a high-growth region. Overall, continued clinical validation, regulatory approvals, and expanding indications are expected to sustain long-term market momentum and improve patient-centered outcomes globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)