Table of Contents

Overview

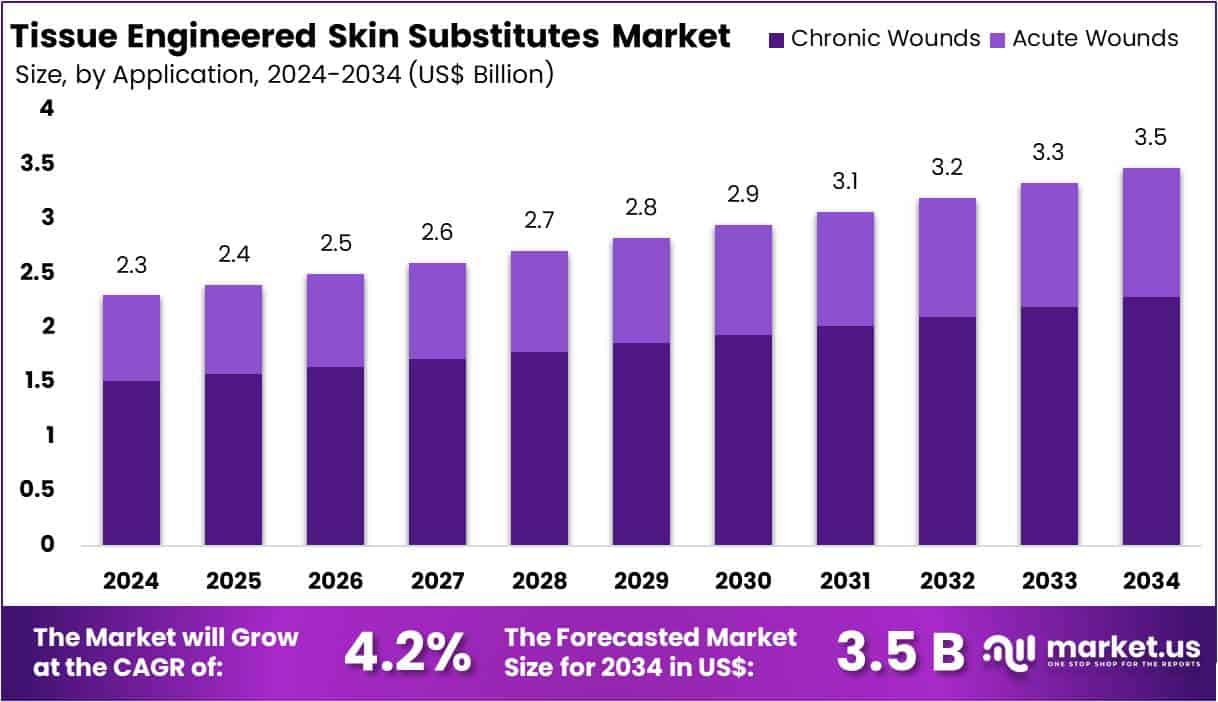

New York, NY – July 28, 2025 – The Global Tissue Engineered Skin Substitutes Market size is expected to be worth around US$ 3.5 Billion by 2034, from US$ 2.3 Billion in 2024, growing at a CAGR of 4.2% during the forecast period from 2025 to 2034.

Tissue engineered skin substitutes represent a major advancement in regenerative medicine, offering promising solutions for patients suffering from severe burns, chronic wounds, diabetic ulcers, and other skin defects. These substitutes are biologically constructed layers of skin cells or bioengineered scaffolds designed to replace or support damaged skin. They are developed using autologous or allogeneic cells, synthetic polymers, natural biomaterials, or a combination of these components.

The basic formation of tissue engineered skin substitutes involves the cultivation of keratinocytes and fibroblasts key cells found in human skin on a biodegradable scaffold that mimics the extracellular matrix. This structure supports cell attachment, proliferation, and differentiation, promoting the regeneration of epidermal and dermal layers. Advanced substitutes may also integrate growth factors or vascularization techniques to improve integration and healing outcomes.

These substitutes are classified as epidermal, dermal, or composite skin substitutes depending on the layer of skin they aim to restore. Composite substitutes, which contain both dermal and epidermal elements, closely replicate the structure and function of natural skin.

As clinical demand rises for effective and rapid wound healing products, the development of tissue engineered skin substitutes continues to expand, driven by innovations in biomaterials, cell culture technology, and 3D bioprinting. These next-generation therapies are expected to significantly improve patient outcomes and quality of life.

Key Takeaways

Tissue engineered skin substitutes have emerged as a transformative advancement in regenerative medicine, addressing complex skin injuries such as burns, chronic ulcers, and surgical wounds. These substitutes are bioengineered constructs developed using autologous or allogeneic cells primarily keratinocytes and fibroblasts cultured on biocompatible scaffolds that mimic the skin’s natural extracellular matrix.

The fundamental design includes three types: epidermal, dermal, and composite substitutes. Composite substitutes, comprising both epidermal and dermal layers, are considered most effective due to their structural and functional resemblance to native skin. The scaffolds used are typically derived from synthetic polymers or natural biomaterials, supporting cell proliferation and tissue integration.

Advancements such as 3D bioprinting, incorporation of growth factors, and vascularization techniques are enhancing the efficacy and adoption of these products. With rising clinical demand for advanced wound healing solutions, tissue engineered skin substitutes are positioned to play a pivotal role in improving patient recovery and outcomes in dermatological and surgical care.

Segmentation Analysis

- By 2034, the global Tissue Engineered Skin Substitutes Market is expected to reach a valuation of US$ 3.5 billion , up from US$ 2.3 billion in 2024.

- The market is projected to grow at a compound annual growth rate (CAGR) of 4.2% between 2025 and 2034.

In 2024, Biologic Skin Substitutes dominated the product segment, accounting for over 51.1% of the global market share. - Chronic Wounds represented the leading application area in 2024, contributing to more than 65.8% of the total market.

- Hospitals emerged as the primary end users in 2024, holding a market share exceeding 53.4% in the tissue engineered skin substitutes segment.

- North America retained its position as the leading regional market in 2024, generating US$ 839.5 million in revenue and accounting for over 36.5% of the global market share.

Market Segments

- Product Analysis: In 2024, Biologic Skin Substitutes led the market with over 51.1% share, driven by the widespread use of allografts and xenografts in chronic and deep wound care. Allografts, sourced from human donors, provide superior compatibility, while xenografts, typically derived from animals, serve as affordable options in emergency care. Biosynthetic substitutes gained moderate traction for their balanced biological activity and durability. Synthetic substitutes, though smaller in share, are growing steadily due to innovations in polymers and nanomaterials.

- Application Analysis: Chronic wounds accounted for more than 65.8% of the market share in 2024, primarily due to rising cases of diabetic foot ulcers, pressure sores, and venous leg ulcers. Diabetic ulcers are a major concern, especially among aging populations in North America and Europe. Acute wounds, including those from burns, trauma, and surgery, represent a smaller but growing segment. Increasing demand for fast healing and infection control has expanded the use of tissue-engineered substitutes in surgical and emergency wound care.

- End-User Analysis: In 2024, hospitals held a dominant position with over 53.4% market share, supported by their access to advanced surgical units, high patient volumes, and favorable reimbursement systems. These institutions treat complex wounds and often lead in clinical adoption of engineered skin products. Ambulatory Surgical Centers held a moderate share, mainly used for outpatient skin procedures. The Others segment including clinics and home care remains smaller but is gradually expanding due to growing interest in decentralized wound care services.

Regional Analysis

In 2024, North America led the global tissue engineered skin substitutes market, accounting for over 36.5% share and generating approximately US$ 839.5 million in revenue. This dominance is largely attributed to the increasing incidence of burn and trauma injuries. According to the American Burn Association, nearly 450,000 burn cases require medical intervention annually in the U.S., significantly driving the demand for advanced wound care solutions, including tissue engineered skin substitutes.

The region’s well-established healthcare infrastructure supports the integration of regenerative technologies across hospitals and specialized trauma centers. Advanced wound care units, particularly in the United States and Canada, facilitate the widespread use of skin substitutes for treating chronic and acute injuries.

Strong governmental and private investment continues to bolster innovation in regenerative medicine. Institutions like the National Institutes of Health (NIH) provide extensive research funding, while active clinical trials by academic and biotech entities accelerate product development. Regulatory support from the U.S. Food and Drug Administration (FDA) through recent approvals of bioengineered skin products has improved market accessibility and treatment options.

Additionally, North America’s aging population contributes to increased demand for wound healing therapies, especially for pressure sores and diabetic foot ulcers. Growing awareness of chronic wound care, along with rising healthcare expenditure, is expected to sustain the region’s leadership in the global tissue engineered skin substitutes market over the forecast period.

Emerging Trends

- Shift toward composite and autologous substitutes: Newer TESSs combine both dermal fibroblasts and epidermal keratinocytes often from the same patient (autologous composite) to more closely mimic real human skin. They have shown better long-term wound healing and reduced rejection risk. MSCs (mesenchymal stem cells) and even gene-corrected patient cells are being integrated in ongoing trials, especially for rare diseases such as epidermolysis bullosa.

- Integration of advanced biomaterials and scaffolds: Biocompatible scaffolds (e.g. collagen-GAG matrices, acellular dermal matrix) are used to support the skin structure. These materials support strength, elasticity, and controlled degradation while delivering cells effectively.

- Development of antimicrobial and sensor-embedded constructs: Research is underway into biomaterials with built-in antimicrobial or biosensing properties such as nanodiamond-silk membranes that detect infection or inflammation and reduce bacterial colonization while promoting healing.

- Use of three dimensional (3D) bioprinting for shaped grafts: Investigators at Columbia University have created anatomically shaped, edgeless skin grafts via 3D printing that fit complex body parts like fingers or limbs. In animal studies they lead to improved functional and cosmetic results compared to flat patches.

- Defining functional wound closure beyond just visible healing: The U.S. Diabetic Foot Consortium (NIDDK) highlighted the importance of measuring barrier restoration not only surface closure to predict wound recurrence. Even visually closed wounds may fail if barrier function is incomplete.

Use Cases

Treatment of burn injuries (acute wounds)

TESSs have been used in clinical trials for full-thickness burns. For example, a phase IIb study enrolling children aged 1–17 is assessing autologous dermo-epidermal substitutes in severe burns, aiming to improve outcomes over traditional grafts.

In Melbourne, lab-grown skin from the patient’s own cells covered up to 60% of body surface area in burns, expanded from a coin-size biopsy into sheets measuring 100×100mm within four weeks. This supports faster healing, less infection, and reduced scarring in initial phase-1 use (trial continues through 2026).

Chronic wounds including diabetic foot ulcers and venous leg ulcers:

Products like Dermagraft and Apligraf (living constructs of human fibroblasts/keratinocytes) have FDA approval and long-term use for diabetic foot ulcers and venous leg ulcers. They promote re-epithelialization and reduce healing time compared to standard care.

Acellular dermal matrices, placental membranes (dHACM), or fish-skin grafts rich in omega-3 are supported by randomized trials. For instance, a multicenter RCT with 110 patients showed superior healing rates in diabetic foot ulcers using acellular dermal matrix versus conventional dressings.

Rare genetic skin disorders (e.g. epidermolysis bullosa, EB)

Autologous gene-corrected composite TESSs are in Phase I/II clinical trials (e.g. for RDEB, ClinicalTrials.gov NCT04186650). These aim to provide long-term closure and correct the genetic defect in patients’ own skin cells. Early clinical results are promising with improved wound healing persistence.

War-wound management and battlefield medicine:

U.S. Department of Defense is funding spray-on, stem-cell enriched delivery systems and topical regenerative therapies to treat burn and blast wounds rapidly in field conditions. The aim is minimal scarring, zero donor-site injury, and immediate application without surgery.

Conclusion

The global tissue engineered skin substitutes market is experiencing steady growth, driven by rising clinical demand for advanced wound care, particularly for chronic wounds and burn injuries. With a projected market value of US$ 3.5 billion by 2034, the sector benefits from strong adoption in hospitals, innovation in biomaterials, and supportive regulatory frameworks.

Advancements such as 3D bioprinting, antimicrobial scaffolds, and autologous composite constructs are improving clinical outcomes. Ongoing trials in rare skin disorders and battlefield medicine further highlight the therapeutic potential of these substitutes. The market is poised to play a transformative role in regenerative medicine and wound management.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)