Table of Contents

Overview

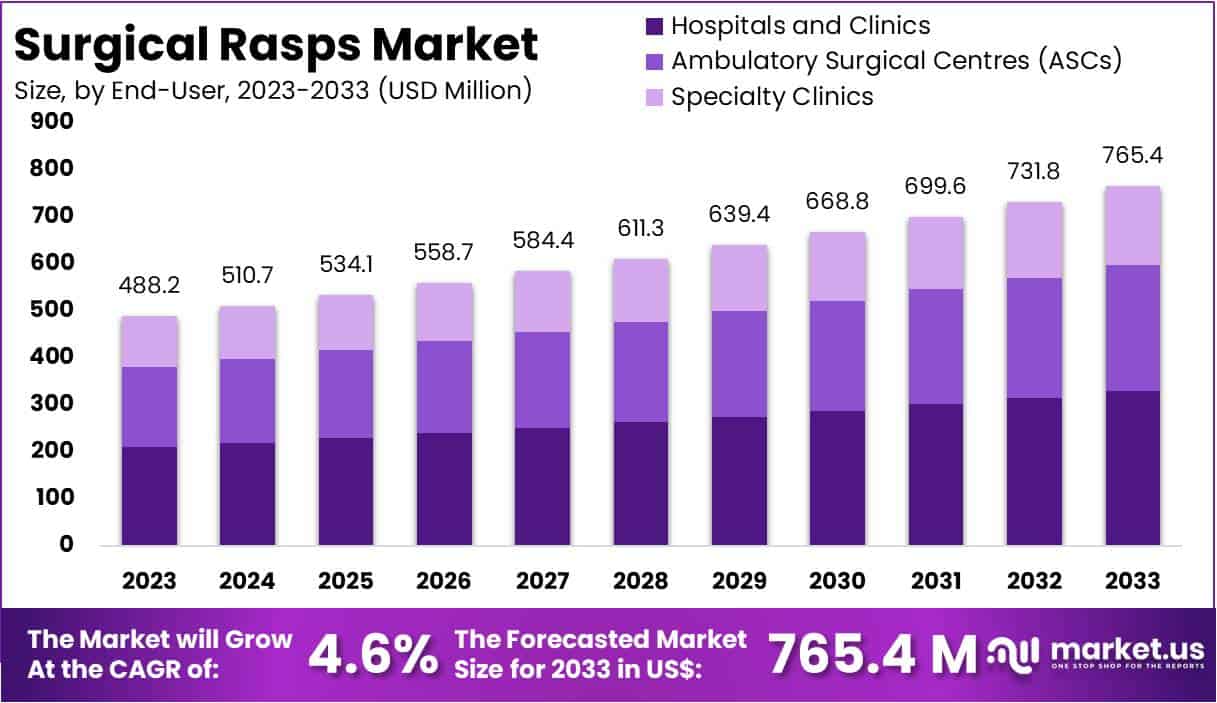

New York, NY – July 25, 2025 – The Global Surgical Rasps Market size is expected to be worth around US$ 765.4 Million by 2033, from US$ 488.2 Million in 2023, growing at a CAGR of 4.6% during the forecast period from 2024 to 2033. North America led the Market, capturing a 39% market share with a valuation of US$ 190.3 Million.

The medical device industry marks another milestone with the advancement of surgical rasps, essential instruments widely used in orthopedic, dental, and reconstructive surgeries. Designed to shape and smooth bone surfaces, these tools are critical in achieving optimal anatomical alignment and ensuring better surgical outcomes.

Modern surgical rasps are now manufactured using high-grade stainless steel and advanced ergonomic designs, enhancing both durability and surgical control. These innovations support greater accuracy in procedures such as joint replacement, maxillofacial reconstruction, and spinal correction.

The integration of customized cutting surfaces, anti-slip handles, and precision-engineered tooth configurations allows surgeons to remove bone tissue more efficiently while minimizing trauma to surrounding structures. As a result, surgical efficiency and patient recovery times have significantly improved.

The global demand for surgical rasps continues to grow, fueled by the increasing number of orthopedic procedures, sports-related injuries, and age-related bone conditions. Surgeons and hospitals are increasingly selecting specialized rasps tailored to specific anatomical applications. With rising investments in surgical innovation and a focus on minimally invasive techniques, the surgical rasp market is expected to witness sustained growth over the coming years.

Key Takeaways

- The global Surgical Rasps Market was valued at approximately USD 488.2 million in 2023 and is expected to reach around USD 765.4 million by 2033, expanding at a compound annual growth rate (CAGR) of 4.6% over the forecast period.

- In terms of product type, the double-ended rasps segment held the dominant position in 2023, accounting for over 73% of the global market share, driven by their versatility and efficiency in various orthopedic procedures.

- By end-user, the hospitals and clinics segment led the market in 2023, capturing more than 43% of the total share, supported by the high volume of surgical interventions and widespread use of specialized instruments in institutional healthcare settings.

- North America emerged as the leading regional market in 2023, holding a 39% share, equivalent to a market value of approximately USD 190.3 million, attributed to advanced surgical infrastructure, high procedural volumes, and early adoption of precision surgical tools.

Segmentation Analysis

- Type Analysis: In 2023, double-ended rasps dominated the surgical rasps market with over 73% share, driven by their versatility and efficiency in surgical workflows. These tools enable rapid switching between functions during procedures, reducing instrument changes and operating time. Conversely, single-ended rasps cater to niche applications that demand high precision, such as dental or reconstructive surgeries. While their share is smaller, their importance remains critical. Together, both types fulfill varied clinical needs and are expected to remain integral to surgical toolkits.

- End-User Analysis: In 2023, hospitals and clinics led the end-user segment with over 43% market share, reflecting their high volume of complex surgical procedures that rely on advanced instruments like rasps. Ambulatory Surgical Centers (ASCs) also contribute significantly, favored for their efficient and cost-effective approach to outpatient surgeries. Specialty clinics, though holding a smaller share, are key users of surgical rasps in targeted treatments like orthopedics and podiatry. Each facility type plays a distinct role in sustaining overall market demand.

Market Segments

By Type

- Double-ended Rasps

- Single-ended Rasps

By End-User

- Hospitals and Clinics

- Ambulatory Surgical Centres (ASCs)

- Specialty Clinics

Regional Analysis

In 2023, North America held a leading position in the global Surgical Rasps Market, accounting for over 39% of the total share and reaching a market value of approximately USD 190.3 million. This strong performance is primarily attributed to the region’s highly developed healthcare infrastructure, which facilitates the adoption of advanced surgical instruments across a wide range of medical specialties.

The United States, in particular, drives regional growth due to its substantial healthcare expenditure and increasing demand for precision surgical tools. The rising volume of orthopedic procedures, fueled by an aging population and a growing incidence of sports-related injuries, further supports the expanding market.

The presence of major surgical instrument manufacturers in the region contributes significantly to innovation and rapid product availability. These companies continuously enhance the performance, ergonomics, and clinical reliability of surgical rasps to meet stringent practitioner standards.

Additionally, favorable regulatory frameworks in the U.S. and Canada, including the FDA’s robust approval process, ensure the circulation of safe and effective medical devices. Ongoing investment in research and development also plays a pivotal role in advancing surgical technologies, enabling North American healthcare providers to remain at the forefront of surgical innovation. This combination of infrastructure, demand, and innovation secures North America’s continued market dominance.

Emerging Trends

- Integration of Computer Assisted Navigation: Patient outcomes can be improved by guiding rasp placement with computer navigation systems. In one review, computer assisted preoperative planning and navigation templates were identified as key innovations that enhance rasp accuracy and reduce placement errors during orthopedic procedures.

- Use of Patient Specific Instrumentation (PSI): Three dimensional (3D) planning and patient specific guides have been adopted to match rasp orientation precisely to each patient’s anatomy. A study of MiniHip short stem hip arthroplasty showed that using a cross laser projection system attached to the rasp handle reduced stem placement deviation to an average of 1.8°±0.2° in anteversion—significantly smaller than conventional methods (p<0.001).

- Development of Curved and Ergonomic Rasps: Rasps with curved shafts have been shown to reduce the rate of femoral stem malalignment. Intraoperative use of a curved rasp was associated with a statistically significant reduction in malalignment incidence compared to straight rasps. This trend reflects a broader focus on ergonomic handle designs that lower surgeon fatigue and improve control.

- Virtual Reality (VR)–Based Skill Training: Surgical education is incorporating VR simulation to train residents in rasp handling before real procedures. A randomized clinical trial on virtual reality training for total hip arthroplasty skills has been initiated (ClinicalTrials.gov Identifier: NCT05807828), illustrating growing adoption of immersive simulation to enhance rasping technique proficiency.

- Focus on Regulatory Compliance and Safety: As manual surgical instruments, rasps classified under FDA Product Code GAC remain ClassI exempt devices; however, manufacturers are increasingly registering their establishments and implementing quality management systems to uphold safety standards. Recent device recalls (e.g., Exeter femoral rasp handle) have underscored the importance of traceability and post market surveillance for reusable rasp assemblies.

Use Cases

- Total Hip Arthroplasty (THA): Rasps are routinely used to prepare the femoral canal before stem insertion. In 2010, 310,800 total hip replacements were performed among U.S. inpatients aged45 and over more than double the 138,700 procedures in 2000 highlighting the critical role of rasps in a market that continues to expand.

- Total Knee Arthroplasty (TKA): In TKA, tibial and femoral rasps shape bone surfaces for implant fit. An estimated 719,000 total knee replacements were conducted in U.S. hospitals in 2010, making it the most common inpatient surgical procedure for adults aged45 and over.

- Unicompartmental Knee Replacement: In partial knee arthroplasty, specialized rasps are used to contour a single compartment of the tibia or femur, supporting quicker recovery and preservation of healthy tissue.

- Spinal Fusion and Graft Bed Preparation: In spine surgery, rasps remove cortical bone to create a graft bed for autograft or allograft placement. The availability of 3D printed graft rasp systems (e.g., for decortication and graft delivery) illustrates the expansion of rasp use beyond joint replacement into spinal procedures.

- Plastic and Reconstructive Surgery: Manual rasps are applied in craniofacial contouring to smooth bone edges after osteotomies. Their ability to deliver controlled bone removal in delicate areas makes them essential in reconstructive workflows.

- Shoulder Arthroplasty: During shoulder joint replacement, humeral rasps shape the proximal humerus to fit prosthetic stems. The trend toward short stem and stemless implants has driven the development of smaller, more precise rasp profiles.

Conclusion

The global surgical rasps market is experiencing significant growth, driven by advancements in surgical technology, an aging population, and the rising demand for orthopedic procedures. Innovations such as ergonomic designs, computer-assisted navigation, and patient-specific instrumentation are enhancing surgical precision and improving patient outcomes.

North America leads the market, supported by advanced healthcare infrastructure and regulatory frameworks. With continued research, development, and integration of minimally invasive techniques, surgical rasps are poised to play a critical role in a wide range of procedures, ensuring improved efficiency, reduced recovery times, and better clinical results in the years ahead.