Introduction

Ready Meals Statistics: Ready meals, also known as convenience food, are pre-packaged meals requiring minimal preparation before consumption.

They’ve surged in popularity due to their convenience, catering to busy lifestyles. Types include frozen, chilled, and canned options.

Market trends indicate a growing demand, particularly for healthier and ethnically diverse choices, alongside a rise in premium offerings.

Key players range from multinational corporations like Nestlé to local and private-label brands. Consumers prioritize convenience, nutrition, flavor variety, and eco-friendly packaging.

In summary, ready meals offer quick, easy solutions for modern life, with a market evolving to meet diverse preferences.

Editor’s Choice

- By 2033, the ready meals market revenue is projected to reach USD 297 billion.

- North America holds the largest share, commanding 41.0% of the market. Which underscores its dominant position in the ready meals sector.

- In the competitive landscape of the global ready meals market, Nestle leads with a 12% share.

- China leads the ready-to-eat meals market with a substantial revenue of USD 149 billion.

- In 2024, the average per capita volume of ready-to-eat meals is expected to rise to 11.1 kilograms.

- The price per unit of ready-to-eat meals is expected to reach USD 7.74 by 2028.

- Presently, one in every five ready meals available is either plant-based or vegetarian, indicating a significant shift in consumer preferences.

Ready Meals Market Statistics

Global Ready Meals Market Size Statistics

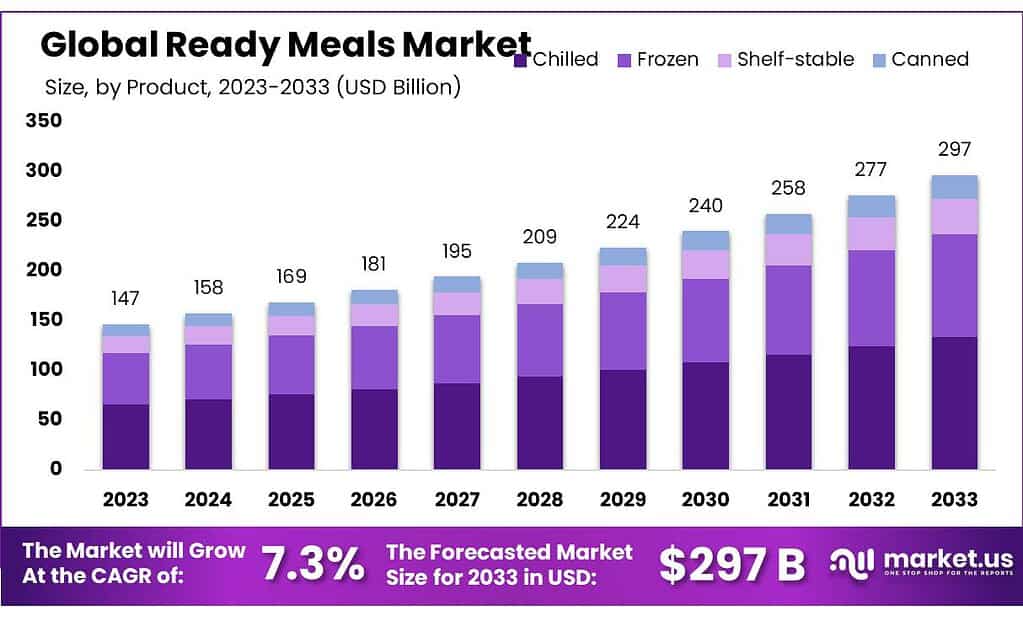

- The global market revenue for ready meals has been forecasted to demonstrate significant growth over the decade from 2023 to 2033 at a CAGR of 7.3%.

- In 2023, the market was valued at approximately USD 147 billion.

- It is projected to increase steadily each year, reaching USD 158 billion in 2024 and continuing to rise to USD 169 billion by 2025.

- The growth trend is expected to persist, with the market size expanding to USD 181 billion in 2026 and further to USD 195 billion in 2027.

- By the end of the decade, the revenue is anticipated to accelerate. Achieving USD 209 billion in 2028, USD 224 billion in 2029, and USD 240 billion in 2030.

- The upward trajectory is set to continue in the subsequent years. The market is expected to grow to USD 258 billion in 2031 and ultimately reach around USD 277 billion in 2032.

- By 2033, the market for ready meals is projected to approach approximately USD 297 billion. Marking a substantial increase over the decade and reflecting a growing consumer preference for convenience foods.

(Source: Market.us)

Regional Analysis of the Global Ready Meals Market Statistics

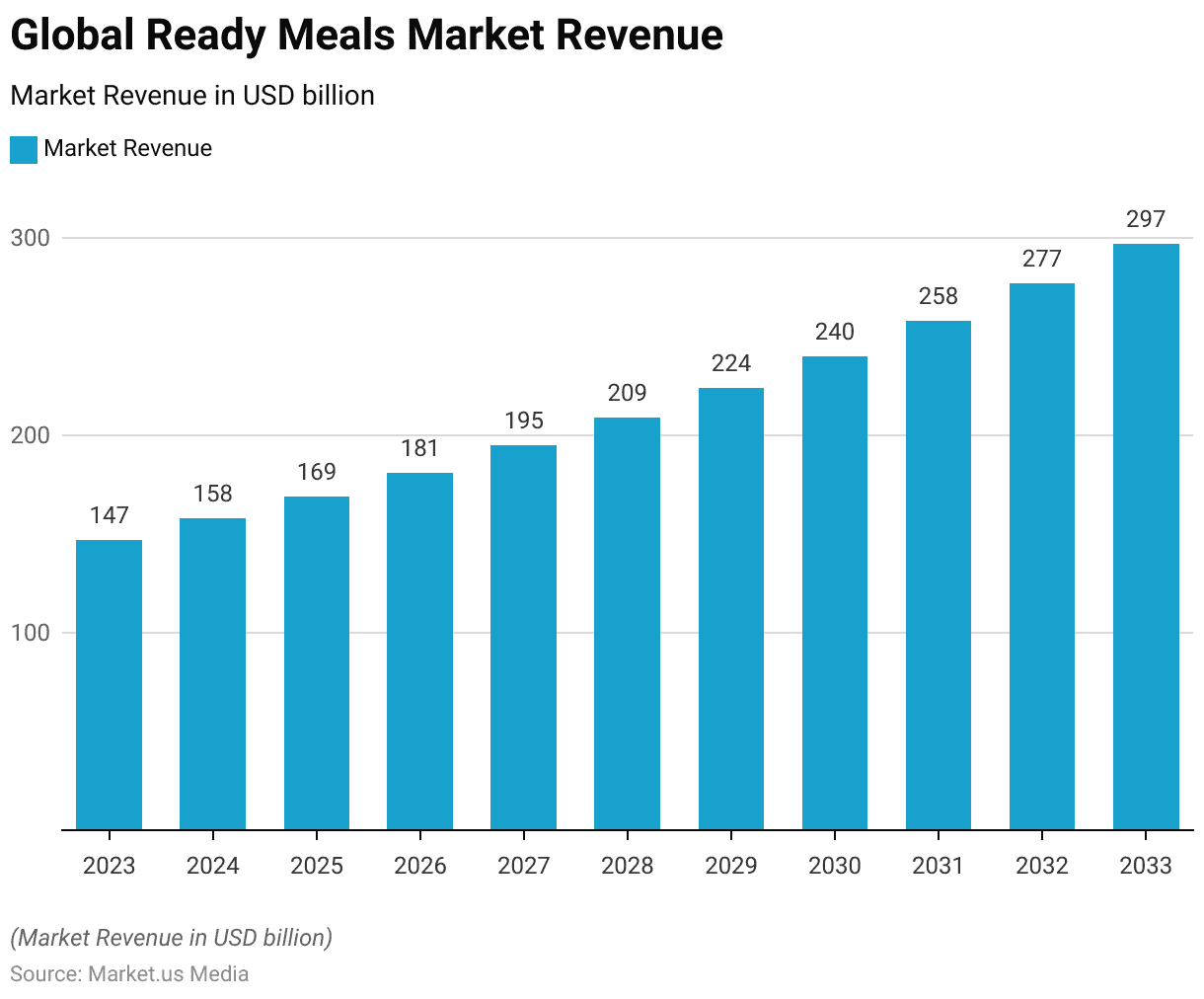

- The distribution of market shares for the global ready meals industry is segmented across different regions. Illustrating varied levels of market penetration and consumer preference.

- North America holds the largest share, commanding 41.0% of the market. Which underscores its dominant position in the ready meals sector.

- Europe follows with a significant 24.0% share, reflecting robust demand in this region.

- The Asia-Pacific (APAC) region, with its growing consumer base and increasing urbanization, accounts for 20.0% of the market.

- Latin America, while smaller in comparison, still maintains a notable share of 11.0%, indicating a rising preference for convenience foods.

- The Middle East and Africa (MEA), with emerging markets and evolving consumer habits, hold the smallest share at 4.0%.

- These figures highlight the geographic diversity in the consumption patterns and market dynamics within the global ready meals industry.

(Source: Market.us)

Competitive Landscape of the Global Ready Meals Market Statistics

- In the competitive landscape of the global ready meals market, several key players have established substantial market shares.

- Nestle leads with a 12% share, reflecting its strong global presence and diverse product portfolio.

- Close behind are General Mills Inc. and Tyson Foods Inc., each holding 10% of the market.

- Kellogg Company and Conagra Brands Inc. are also prominent competitors. Each with an 11% market share, underscoring their significant impact on the industry.

- Dr. Oetker and Green Mill Foods, with a 9% market share each, demonstrate solid performance and consumer trust. Nomad Foods, slightly smaller in scale, commands an 8% share.

- Additionally, a variety of other key players collectively hold 20% of the market. Indicating a vibrant and competitive environment where numerous smaller companies contribute to the industry dynamics and innovation in the ready meals sector.

(Source: Market.us)

Global Ready-To-Eat Meals Market Overview

Global Ready Meals Market Share – By Distribution Channel Statistics

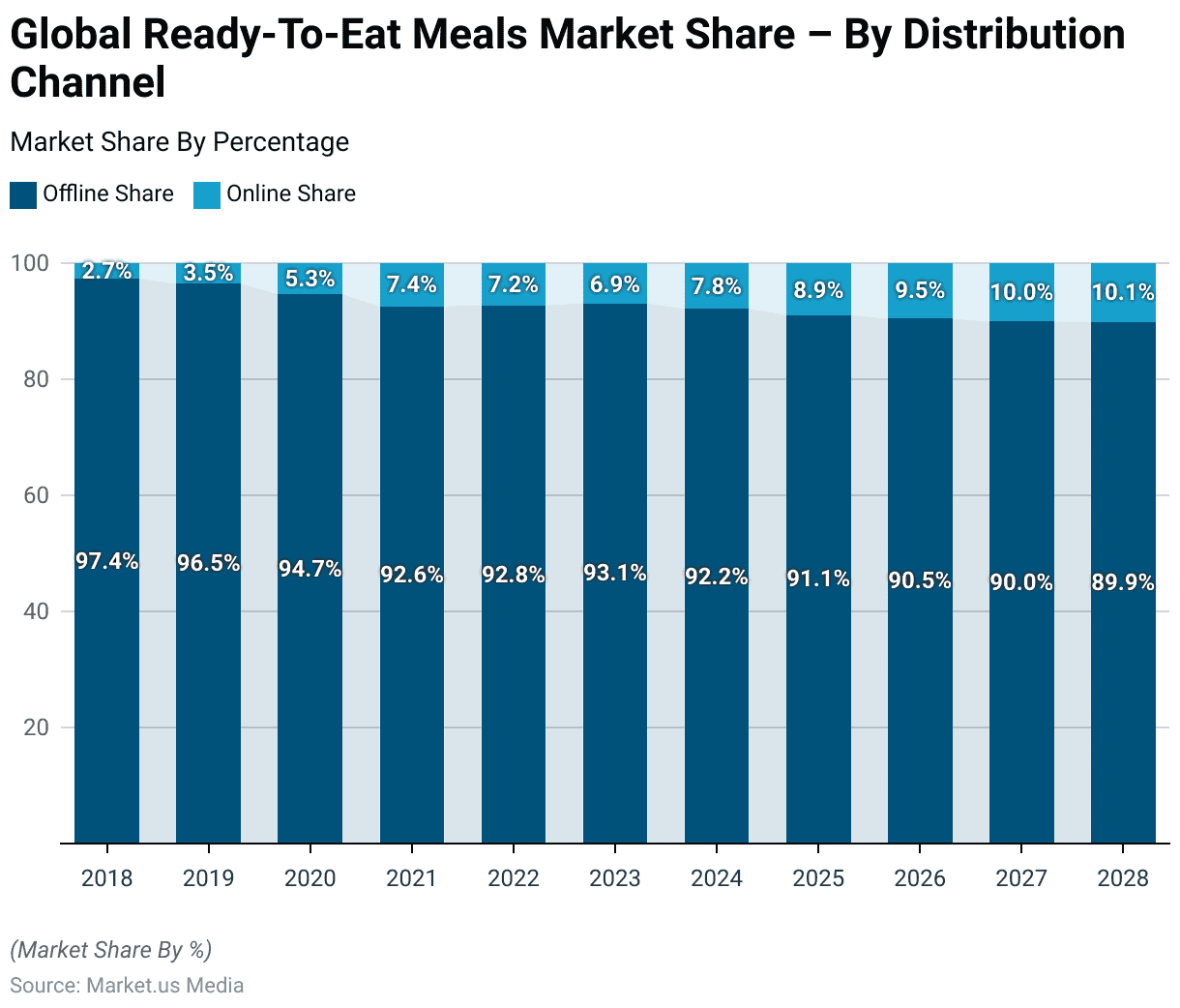

- The distribution dynamics in the global ready-to-eat meals market have significantly evolved from 2018 to 2028, with a marked shift from offline to online channels.

- Initially, in 2018, offline sales dominated the market, accounting for 97.4% of distribution, while online sales comprised only 2.7%.

- By 2019, this began to change as offline sales decreased to 96.5%, and online sales rose to 3.5%. This shift gained momentum by 2020, with offline sales reducing further to 94.7% and online sales increasing to 5.3%.

- The trend continued into 2021, with offline sales at 92.6% and online climbing to 7.4%. Although 2022 saw a slight stabilization—92.8% offline and 7.2% online—the general shift persisted into 2023, with 93.1% offline and 6.9% online.

- Projections indicate a steady decline in offline shares; by 2024. Offline distribution is expected to fall to 92.2%, with online increasing to 7.8%.

- This pattern is projected to continue, with offline shares dropping to 91.1% and online rising to 8.9% by 2025, reaching 90.5% offline and 9.5% online by 2026, and by 2028. Approaching a more balanced distribution with 89.9% offline and 10.1% online.

- This ongoing trend reflects a growing consumer preference for the convenience and broader selection offered by online shopping for ready-to-eat meals.

(Source: Statista)

Global Ready Meals Market Revenue – By Country Statistics

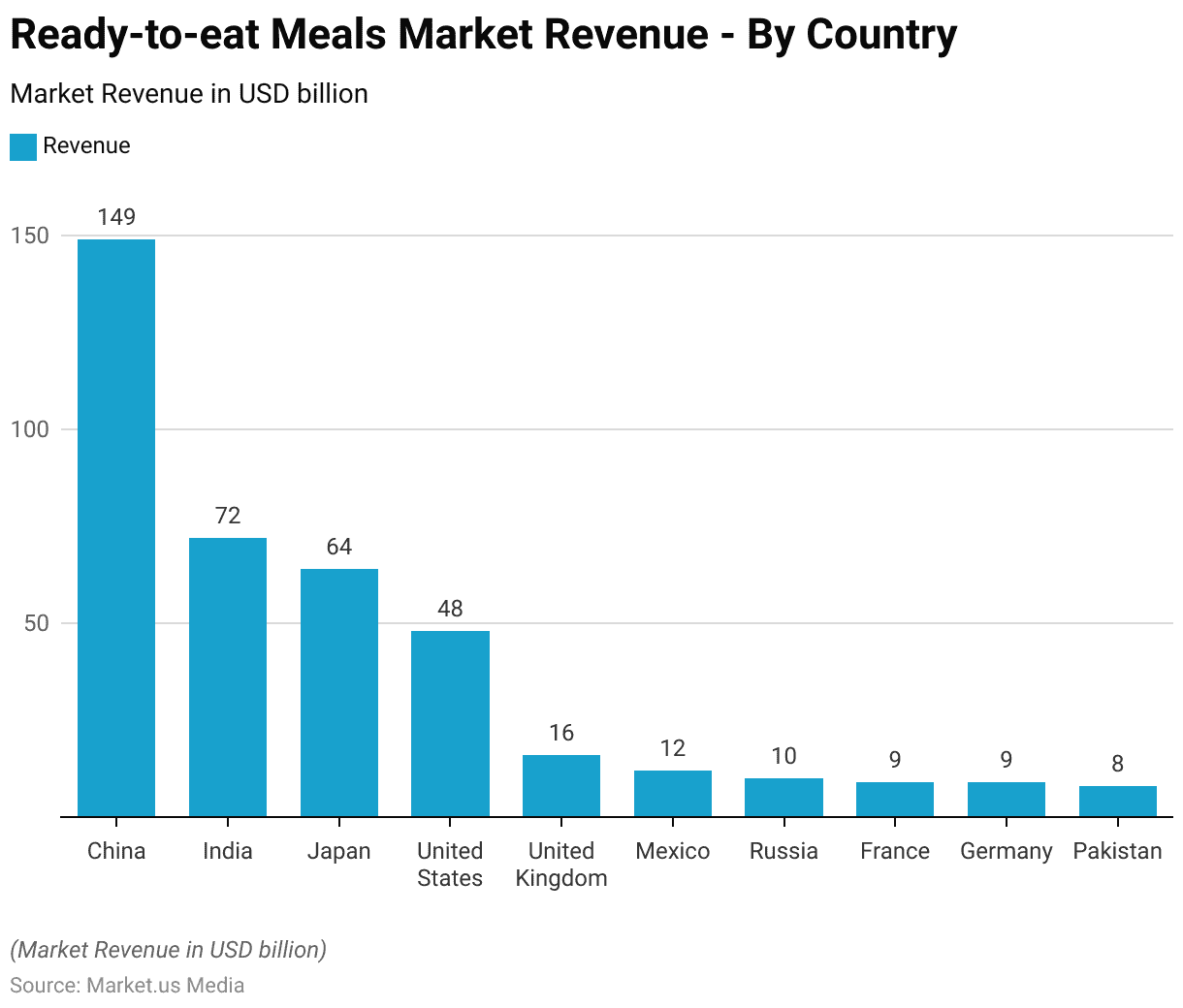

- The ready-to-eat meals market exhibits varied revenue figures across different countries, highlighting distinctive consumption patterns and market sizes.

- China leads with a substantial market revenue of USD 149 billion. Reflecting its large population and increasing consumer demand for convenience foods.

- India follows with a significant revenue of USD 72 billion due to its growing urbanization and changing lifestyle trends.

- Japan also holds a considerable portion of the market, generating USD 64 billion, supported by its high consumer spending on convenience foods.

- In the United States, the market revenue stands at USD 48 billion, indicative of a robust demand for ready-to-eat options.

- The United Kingdom contributes USD 16 billion, while Mexico’s market is slightly smaller at USD 12 billion.

- Russia and France each have market revenues close to USD 10 billion and USD 9 billion, respectively, demonstrating moderate market engagement.

- Germany matches France with a revenue of USD 9 billion. Pakistan, with a developing consumer market, shows a market revenue of USD 8 billion.

- These figures illustrate the global diversity in the readiness and scale of adoption of ready-to-eat meals across various economies.

(Source: Statista)

Average Volume Per Capita of Ready-to-eat Meals

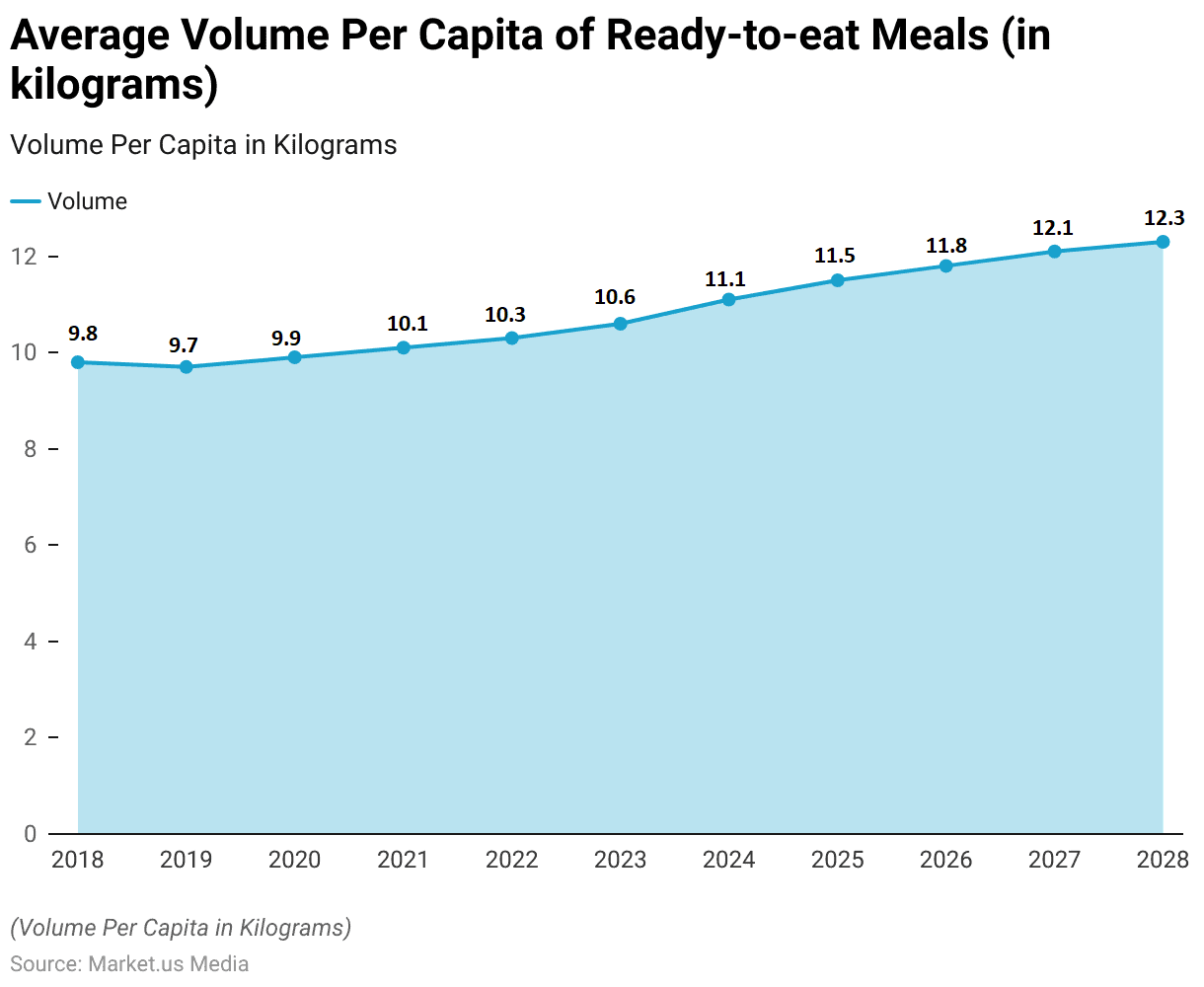

- The average volume per capita of ready-to-eat meals has shown a progressive increase from 2018 through 2028.

- In 2018, the consumption per capita was measured at 9.8 kilograms.

- This figure slightly decreased to 9.7 kilograms in 2019 but rebounded to 9.9 kilograms in 2020, possibly influenced by changing consumption patterns due to global events.

- The upward trend continued steadily, with volumes reaching 10.1 kilograms in 2021 and further increasing to 10.3 kilograms in 2022.

- By 2023, the per capita volume had grown to 10.6 kilograms, and projections show accelerated growth in the subsequent years.

- In 2024, the average volume is expected to rise to 11.1 kilograms, reaching 11.5 kilograms in 2025.

- The trend is anticipated to continue, with volumes growing to 11.8 kilograms in 2026, 12.1 kilograms in 2027, and eventually stabilizing at 12.3 kilograms by 2028.

- This consistent increase underscores a growing consumer reliance on and preference for ready-to-eat meals over the decade.

(Source: Statista)

Price of Ready-to-eat Meals Statistics

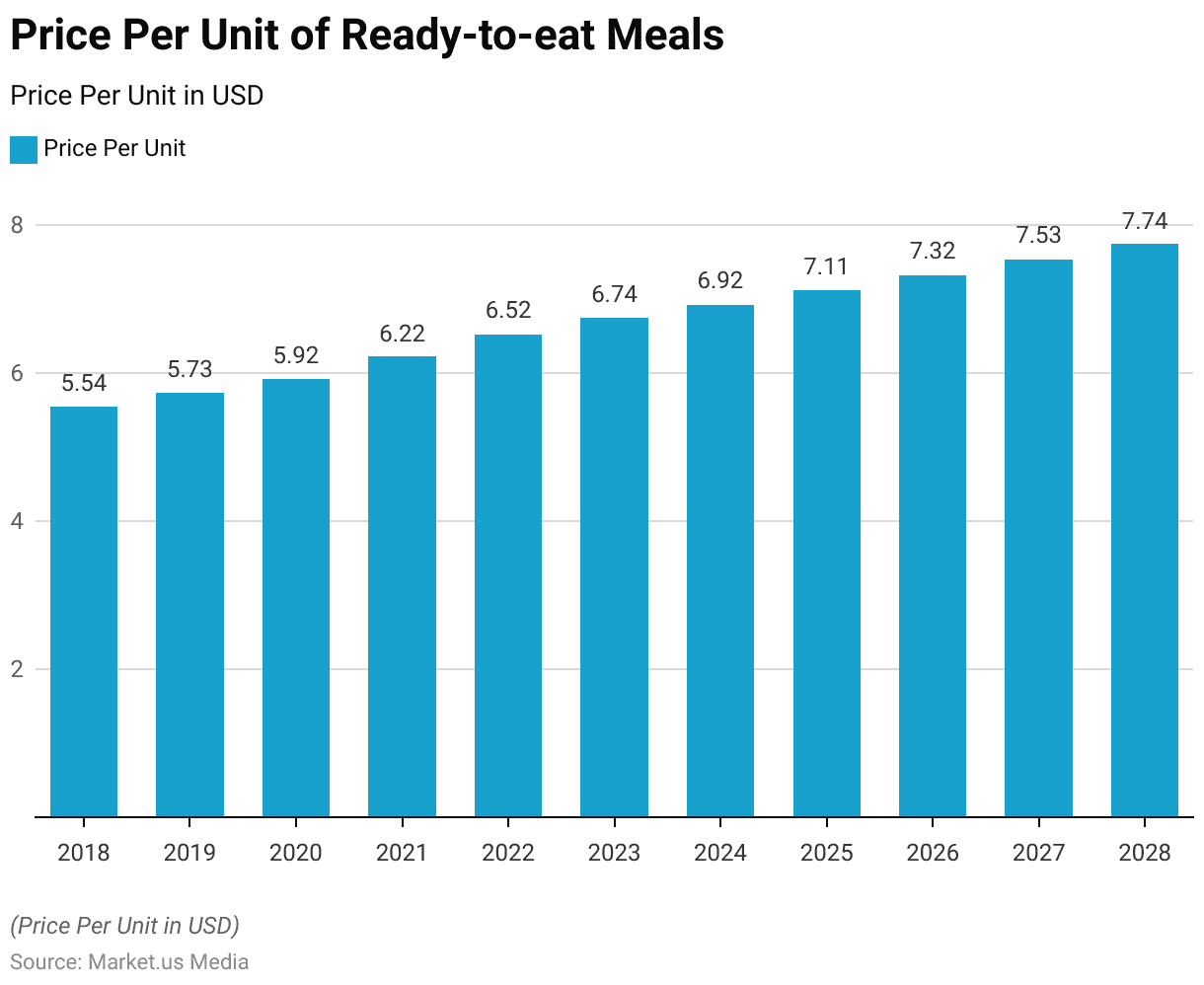

- The price per unit of ready-to-eat meals has shown a consistent upward trend from 2018 through 2028.

- Starting at $5.54 per unit in 2018, there has been a gradual increase each year. In 2019, the price rose slightly to $5.73, followed by an increment to $5.92 in 2020.

- The trend of rising prices continued more markedly in the subsequent years, with the price reaching $6.22 in 2021 and further climbing to $6.52 in 2022.

- By 2023, the price per unit had increased to $6.74, reflecting ongoing market adjustments and inflationary pressures.

- The projections for the following years indicate a steady rise in pricing: $6.92 in 2024, $7.11 in 2025, and $7.32 in 2026.

- The price is expected to continue its upward trajectory, reaching $7.53 in 2027 and $7.74 by 2028.

- This consistent rise in prices underscores the growing costs of production and perhaps an increase in consumer demand for the quality and convenience offered by ready-to-eat meals.

(Source: Statista)

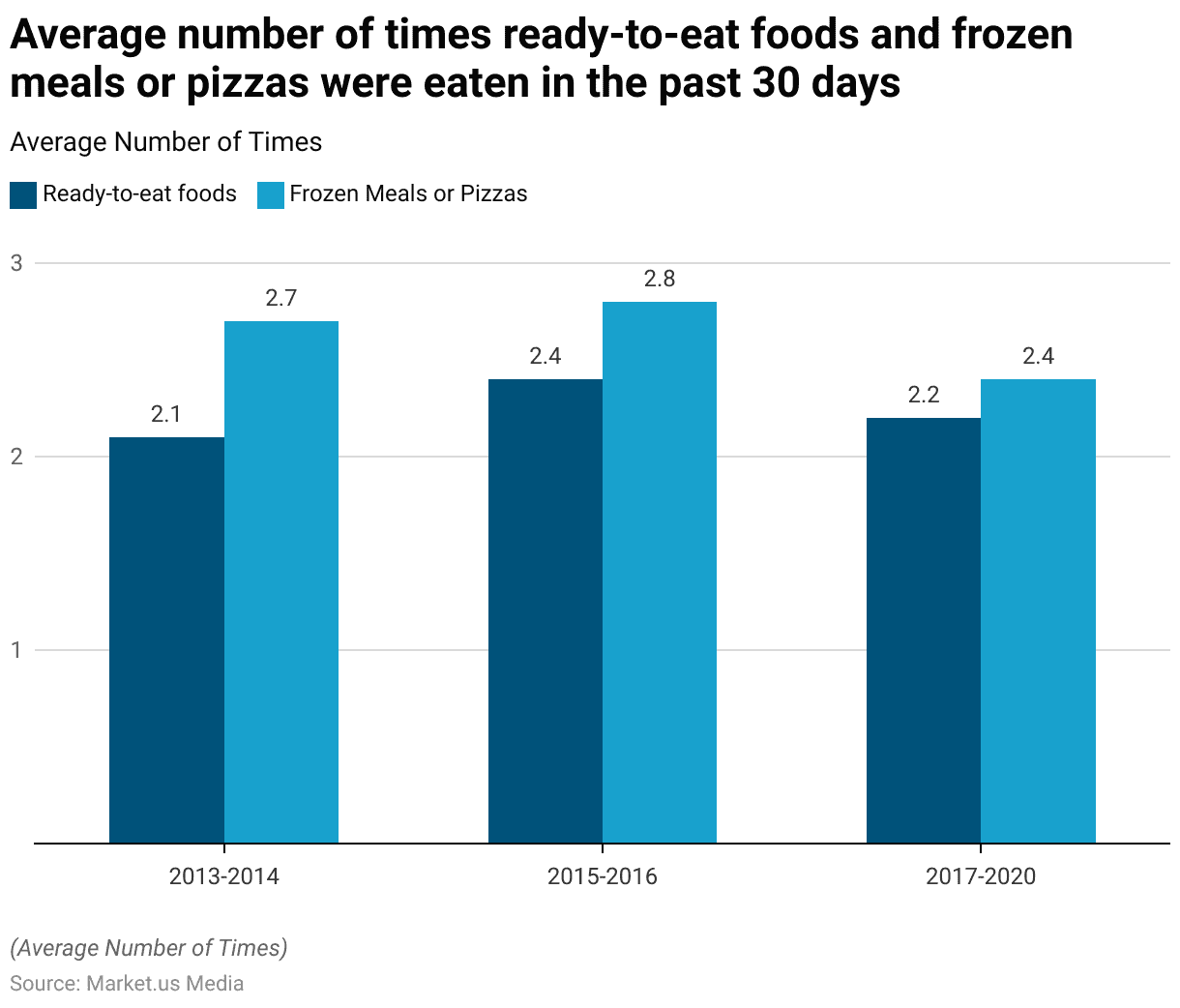

Average Consumption of Ready-To-Eat Foods and Frozen Meals or Pizzas

- Over the period from 2013 to 2020, there has been noticeable variability in the consumption patterns of ready-to-eat foods and frozen meals or pizzas.

- In the years 2013-2014, the average number of times ready-to-eat foods were consumed in the past 30 days stood at 2.1, while frozen meals or pizzas were consumed slightly more frequently at an average of 2.7 times.

- This trend saw a modest increase in the subsequent period of 2015-2016, with ready-to-eat foods being consumed 2.4 times and frozen meals or pizzas slightly higher at 2.8 times.

- However, from 2017 to 2020, there was a slight decline in consumption rates; ready-to-eat foods were consumed 2.2 times, and frozen meals or pizzas dropped to an average of 2.4 times.

- This period reflects a slight fluctuation in consumer habits concerning these convenient food options.

(Source: U.S. Department of Agriculture – Economic Research Service)

Consumer Behaviour and Trends

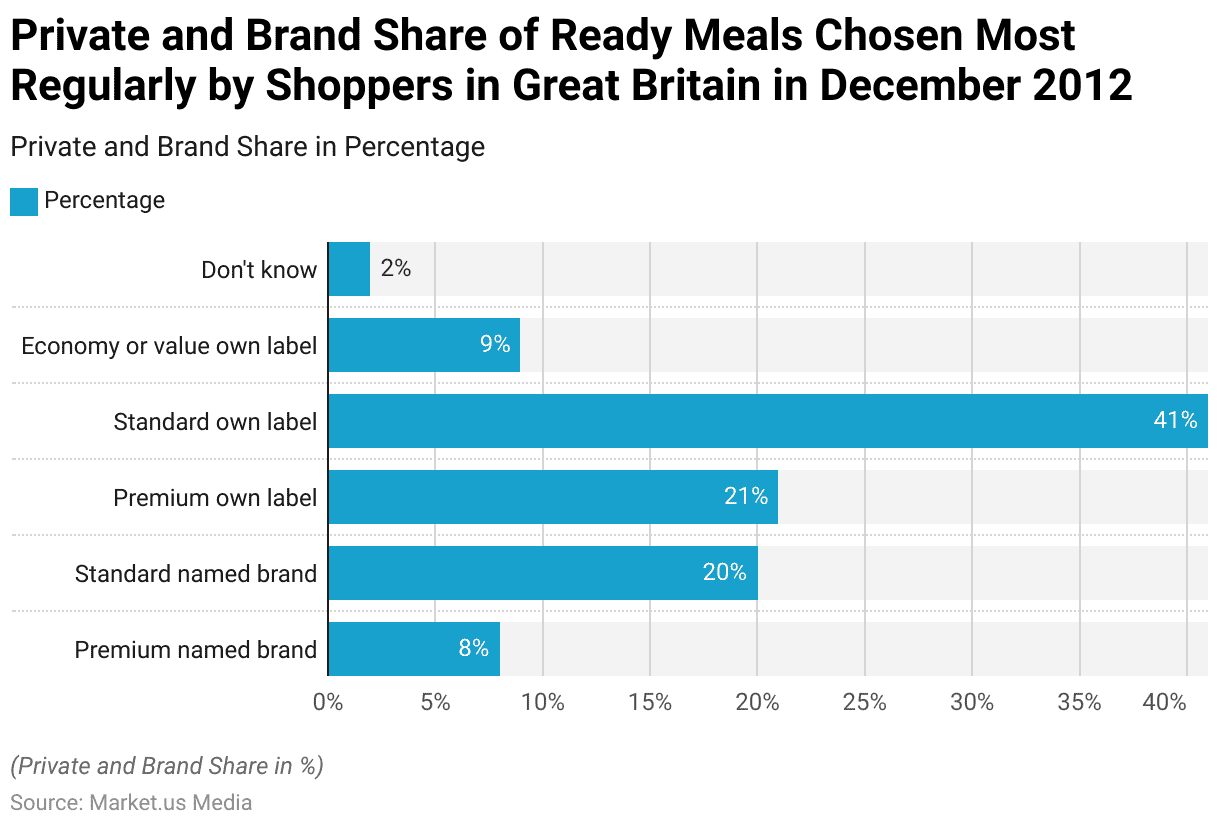

Ready Meals Brand Preferences Among Shoppers Statistics

- In December 2012, the distribution of ready meals chosen most regularly by shoppers in Great Britain revealed distinct consumer preferences.

- Premium-named brands were chosen by 8% of respondents, while standard-named brands were more popular and selected by 20% of shoppers.

- Own-label products, however, dominated the market preferences. Premium own-label ready meals were chosen by 21% of consumers, but it was the standard own-label options that held the largest share, preferred by 41% of the shoppers.

- Additionally, economy or value-own-label products were selected by 9% of respondents.

- A small percentage, 2%, were unsure of their regular choice, indicating a level of indecision or lack of brand loyalty among some consumers.

- These figures highlight a strong inclination towards own-label products over named brands, reflecting possibly both price sensitivity and trust in in-store brands among British shoppers.

(Source: Statista)

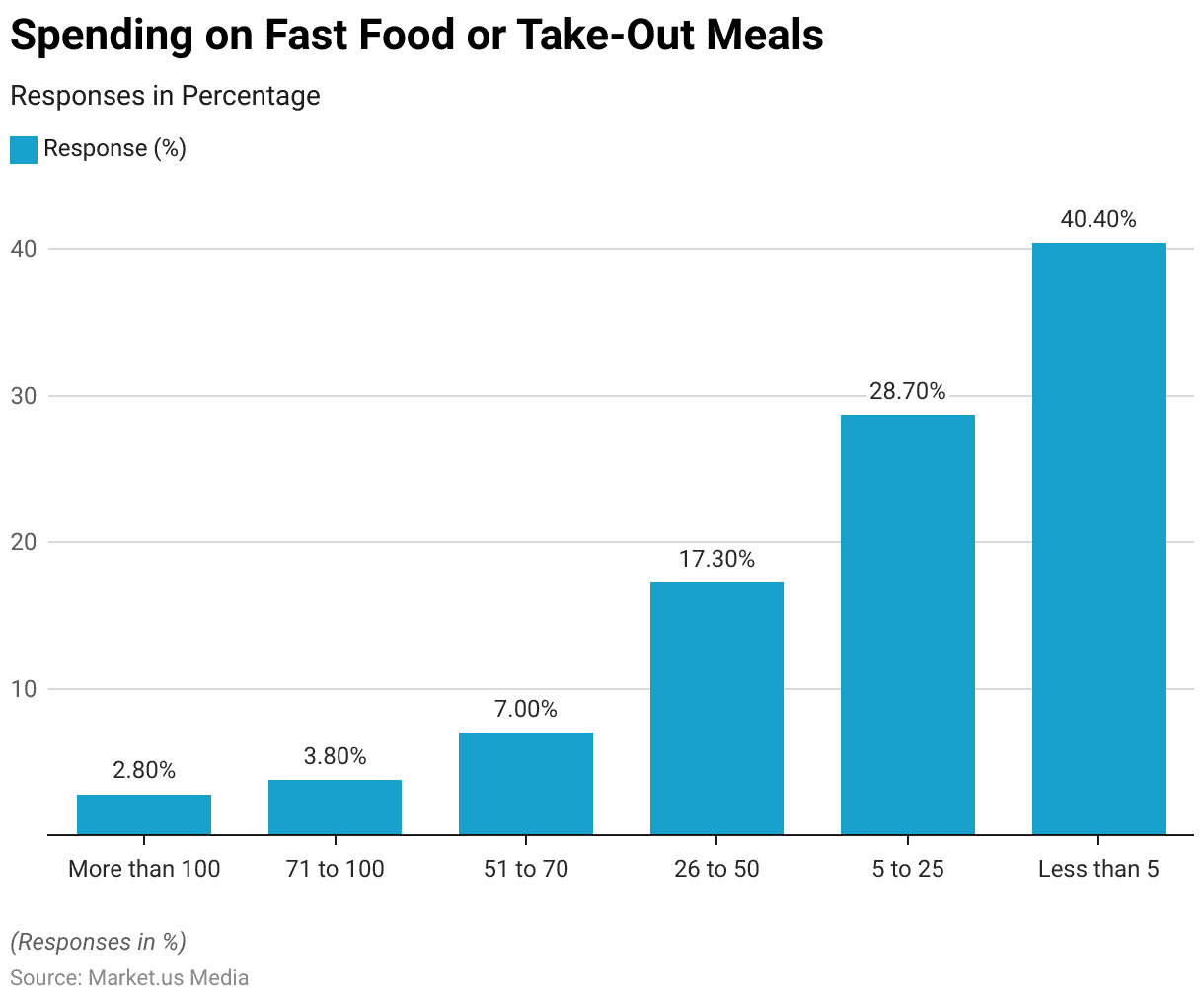

Spending on Fast Food or Take-Out Meals

- A survey on spending patterns for fast food or take-out meals reveals a broad range of consumer behaviors.

- A significant portion of respondents, 40.4%, reported spending less than $5, indicating a conservative approach to expenditure on these types of meals.

- The next largest group, comprising 28.7% of participants, spends between $5 and $25, suggesting a moderate but more frequent indulgence in fast food or take-out.

- Those spending between $26 and $50 represent 17.3% of the survey population, showing a willingness to allocate a reasonable portion of their budget to convenience dining.

- A smaller segment, 7%, spends between $51 and $70, while 3.8% allocate between $71 and $100 to such meals, reflecting a higher but less common spending threshold.

- The smallest group, at 2.8%, spends more than $100, indicating a significant commitment to fast food or take-out meals among a minor subset of consumers.

- These data points illustrate a diverse range of spending habits associated with fast food and take-out meals, from very minimal to substantial investment.

(Source: Real Research Survey)

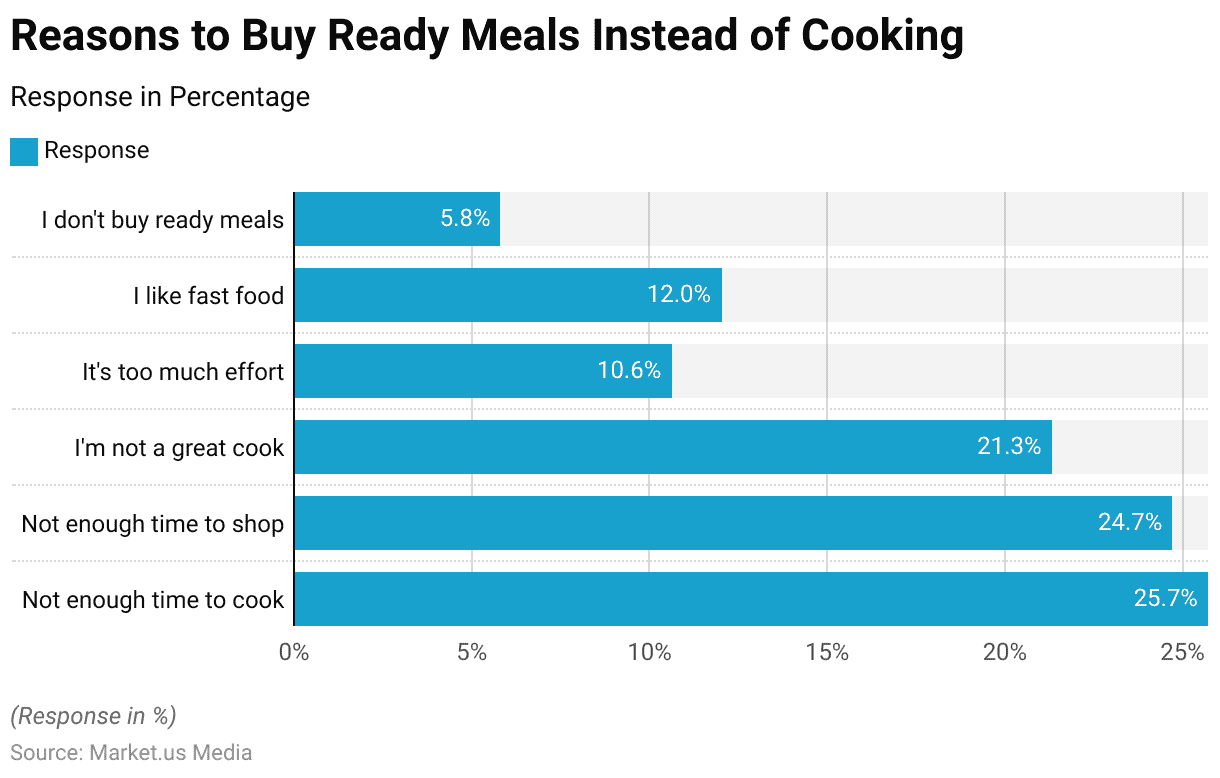

Reasons to Buy Ready Meals Instead of Cooking Statistics

- A survey investigating the reasons consumers choose ready-to-cook meals over cooking at home highlights various motivations tied to lifestyle and personal preferences.

- The leading reason, reported by 25.7% of respondents, is not having enough time to cook, indicating a significant demand for convenience.

- Closely following, 24.7% of individuals cited the lack of time to shop for groceries as their main reason, which further underscores the need for quick and easy meal solutions.

- Additionally, 21.3% of participants admitted to purchasing ready meals because they do not consider themselves great cooks, suggesting that skill level is a notable factor in food choices.

- About 12% of respondents expressed a preference for fast food simply because they like it, while 10.6% described cooking as too much effort.

- Interestingly, a small portion of the surveyed population, 5.8%, stated that they do not buy ready meals at all, highlighting a minority that either prefers to cook or chooses other options.

- These findings reveal a variety of reasons that drive the consumption of ready meals, with time constraints and convenience being the predominant factors.

(Source: Real Research Survey)

Purchasing Preferences

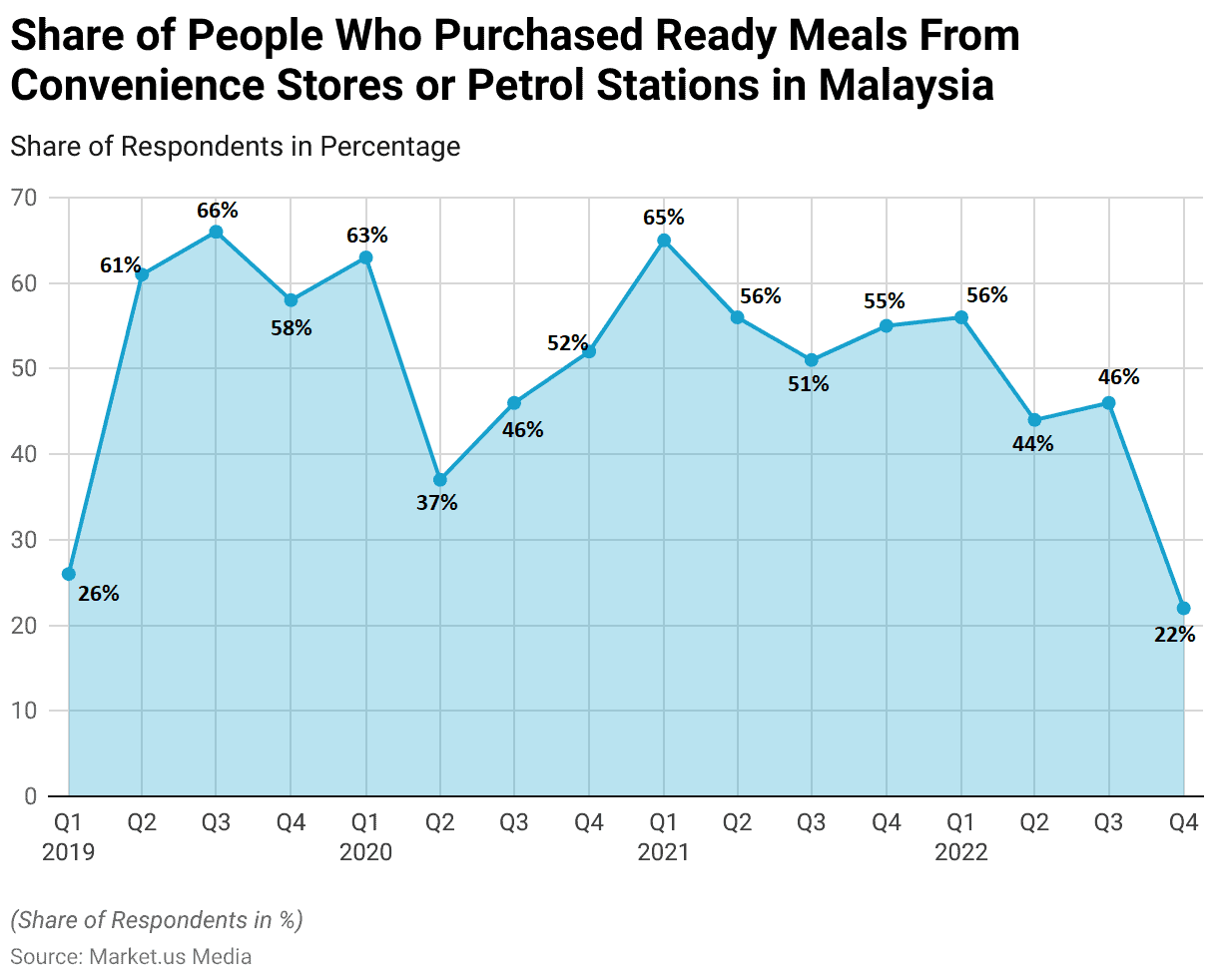

- Between the first quarter of 2019 and the fourth quarter of 2022, the percentage of people in Malaysia purchasing ready meals from convenience stores or petrol stations exhibited notable fluctuations.

- The trend started with 26% of respondents in Q1 2019, which saw a significant increase to 61% by Q2 2019 and peaked at 66% in Q3 2019. By the end of 2019, the share had decreased slightly to 58%.

- In 2020, the percentages continued to fluctuate markedly, starting at 63% in Q1, dropping to 37% in Q2 during the height of global disruptions, recovering to 46% in Q3, and further increasing to 52% by Q4.

- The year 2021 saw relatively high numbers, beginning at 65% in Q1, then declining progressively across subsequent quarters to 56% 51%, and stabilizing at 55% in Q4.

- In 2022, the purchasing rate maintained a level of 56% in Q1, dropped to 44% in Q2, remained stable at 46% in Q3, and then saw a significant drop to 22% by Q4 2022.

- This pattern reflects a dynamic interplay of factors influencing consumer behavior toward ready meals in Malaysia over the years.

(Source: Statista)

New Trends in Preferences for Plant-based Meals

- The plant-based meal category has experienced remarkable growth, soaring by 92% since 2018.

- Over the same period, there has been a notable 50% surge in plant-based and vegetarian meal options.

- Presently, one in every five ready meals available is either plant-based or vegetarian, indicating a significant shift in consumer preferences.

- Moreover, these plant-based and vegetarian options are now priced as the most economical choices across various retailers.

- Notably, major supermarkets such as ALDI and Tesco have substantially expanded their plant-based offerings, with ALDI witnessing a remarkable 175% increase, now constituting a quarter of its ready meals range.

- Similarly, Tesco has expanded by 103%, while the Co-op and Morrisons have both seen growth exceeding 60%. Interestingly, the prevalence of cheese in vegetarian meals has declined by 62% over three years.

- Additionally, although meat-based meals still dominate the market, the proportion of meals featuring meat as the primary ingredient has decreased by 9% since 2018, with 70% of ready meals surveyed still containing meat.

(Source: Eating Better Survey)

Recent Developments

Acquisitions and Mergers:

- Nestlé’s Acquisition of Freshly: Nestlé, a global food and beverage company, acquired Freshly. A U.S.-based subscription-based meal delivery service, for approximately $1.5 billion in October 2020.

- Nomad Foods’ Acquisition of Findus Switzerland: Nomad Foods, a leading frozen foods company, completed the acquisition of Findus Switzerland in December 2021. Expanding its presence in the European ready meals market.

New Product Launches:

- HelloFresh’s Expansion into Ready Meals: HelloFresh, is known for its meal kit delivery services. Launched a range of ready meals in March 2022, catering to consumers seeking convenient and nutritious meal options.

- Conagra Brands’ Launch of Healthy Choice Power Bowls: Conagra Brands introduced new varieties of Healthy Choice Power Bowls. Including plant-based options, in response to growing demand for healthy and convenient meal solutions.

Funding and Investments:

- MealPal’s Series C Funding Round: MealPal, is a subscription-based meal service offering ready-to-eat meals from local restaurants. Raised $50 million in a Series C funding round led by Bain Capital Ventures in September 2021, enabling further expansion and product innovation.

- Gobble’s Investment from Khosla Ventures: Gobble, a meal kit delivery service emphasizing quick and easy preparation. Secured an undisclosed investment from Khosla Ventures in November 2021 to fuel its growth and enhance its product offerings.

Market Growth and Trends:

- Convenience, health-consciousness, and diverse dietary preferences are driving the demand for ready meals, with consumers seeking quick, nutritious, and customizable meal options.

Expansion Strategies:

- Several companies in the ready meals sector are expanding their distribution channels and geographic reach. Through partnerships with online retailers, grocery stores, and food service providers, aim to reach a wider consumer base.

Conclusion

Ready Meals Statistics – In summary, the ready meals market has shown significant growth. Driven by consumer demands for convenience, urbanization, and evolving lifestyle preferences.

Key regions like North America and Europe have contributed substantially, with emerging markets in Asia-Pacific also displaying rapid expansion.

The shift from offline to online shopping reflects wider retail trends. The competitive landscape sees major players like Nestlé and General Mills alongside innovative smaller brands.

Although the market faces challenges such as health concerns and the need for sustainability. It is poised for continued expansion, highlighting its integral role in the global food industry.

This growth trajectory underscores the sector’s adaptation to changing consumer demands and the increasing importance of convenience in the culinary world.

FAQs

Ready meals are pre-packaged meals that come fully cooked and only require heating before eating. They are designed for convenience, saving time on meal preparation and cooking.

The healthiness of ready meals can vary widely depending on the ingredients and preparation methods. Some ready meals are high in sodium and preservatives, while others are designed to be balanced and nutritious. It’s important to read nutritional labels to make informed choices.

The shelf life of ready meals depends on their packaging and storage conditions. Frozen meals can last several months in the freezer. While refrigerated meals typically have a shelf life of a few days to a week. Always check the expiration date on the package.

Ready meals can be cost-effective compared to dining out but are generally more expensive than cooking from scratch. They offer value in terms of time saved, which might be a priority for many consumers.

Ready meals are available in a wide range of cuisines, from traditional comfort foods to international dishes, catering to diverse tastes and dietary preferences.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)