Table of Contents

Overview

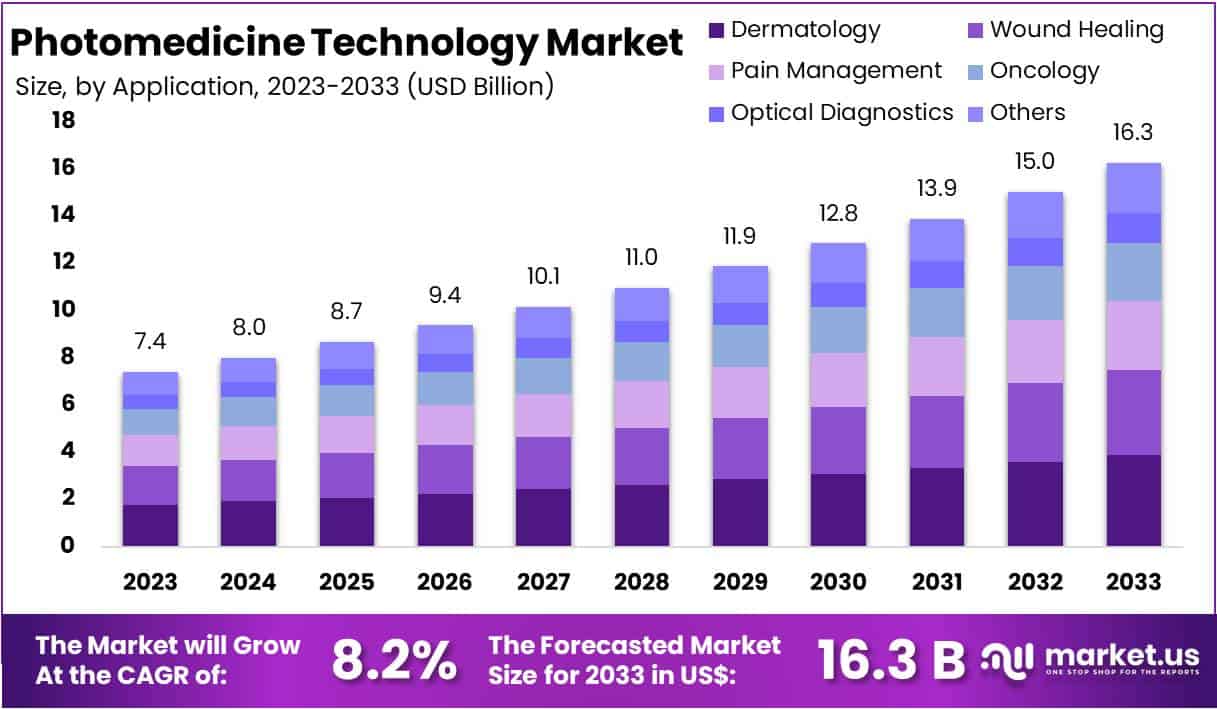

New York, NY – July 25, 2025 – The Global Photomedicine Technology Market size is expected to be worth around US$ 16.3 Billion by 2033, from US$ 7.4 Billion in 2023, growing at a CAGR of 8.2% during the forecast period from 2024 to 2033.

A significant leap forward has been achieved in the field of medical science with the development of advanced Photomedicine Technology, a novel approach that uses light-based therapies to treat a wide range of health conditions with improved precision, safety, and efficacy.

Photomedicine integrates cutting-edge optical engineering with biomedical applications to harness specific wavelengths of light for therapeutic and diagnostic purposes. This technology enables targeted treatment of diseases such as cancer, skin disorders, chronic pain, and wound healing, while minimizing damage to surrounding healthy tissue.

The core innovations include the use of low-level laser therapy (LLLT), photodynamic therapy (PDT), and near-infrared light devices, which stimulate cellular regeneration, reduce inflammation, and improve patient recovery times. These solutions are particularly promising in dermatology, oncology, neurology, and ophthalmology.

Clinical trials are already demonstrating measurable outcomes, with significant reductions in treatment times and patient-reported side effects. The growing interest in non-invasive, drug-free modalities positions photomedicine as a transformative solution in both hospital and outpatient settings. The global photomedicine market is expected to grow steadily over the next decade, driven by increasing demand for personalized and minimally invasive treatments.

Key Takeaways

- The Photomedicine Technology Market was valued at approximately USD 7.4 billion in 2023 and is projected to reach around USD 16.3 billion by 2033, expanding at a compound annual growth rate (CAGR) of 8.2% over the forecast period.

- In terms of technology type, the laser segment held the leading position in 2023, capturing more than 52% of the global market share, owing to its widespread adoption in medical and cosmetic procedures.

- By application, the dermatology segment accounted for the largest share in 2023, representing over 24% of the total market, driven by rising demand for non-invasive skin treatments and aesthetic procedures.

- North America emerged as the dominant regional market in 2023, holding a 49% market share, equivalent to approximately USD 3.6 billion, supported by advanced healthcare infrastructure, strong research investments, and high adoption of photomedical technologies.

Segmentation Analysis

- Industrial Advantages: Photomedicine technology offers notable industrial benefits, including high profit margins driven by increasing demand for non-invasive treatments in dermatology, oncology, and pain management. Companies leading in innovation can secure market leadership and build strong brand trust. Advancements in light-based devices enhance treatment efficacy, reduce recovery times, and lower healthcare costs, offering a competitive edge. The broad application range spanning skin care, wound healing, and diagnostics enables diversification. Emerging markets and consumer wellness trends also present expansion opportunities for key industry players.

- Type Analysis: In 2023, lasers led the type segment, accounting for over 52% of the market due to their precision in dermatology, dentistry, and ophthalmology. Polychromatic Polarized Light is gaining traction for wound healing and skin treatments, driven by its regenerative and anti-inflammatory effects. Full Spectrum Light is expanding in applications like sleep and mood disorders. Dichroic lamps and LEDs also play a vital role, with LEDs notably rising in skin rejuvenation and photodynamic therapy due to their energy efficiency and therapeutic versatility.

- Application Analysis: Dermatology dominated the application segment in 2023 with over 24% share, owing to rising demand for laser- and LED-based skin treatments. Wound healing applications are expanding rapidly, supported by light therapies that stimulate tissue repair. Pain management is growing, with low-level laser therapies widely used for arthritis and inflammation. Oncology benefits from photodynamic therapies targeting cancer cells, while optical diagnostics support non-invasive imaging. Emerging uses in mental health and sleep regulation continue to broaden the scope of photomedicine applications.

Market Segments

By Type

- Laser

- Polychromatic Polarized Light

- Full Spectrum Light

- Dichroic Lamps

- Light Emitting Diodes

By Application

- Dermatology

- Wound Healing

- Pain Management

- Oncology

- Optical Diagnostics

- Others

Regional Analysis

In 2023, North America dominated the Photomedicine Technology Market, accounting for over 49% of the global share, with a total market value of approximately USD 3.6 billion. This leadership position is supported by the widespread adoption of advanced light-based therapies across the region’s well-established healthcare infrastructure. Strong investment in research and development, along with the presence of major industry players, has further accelerated technological advancements in photomedicine.

The region’s growing demand for non-invasive and clinically effective treatments particularly in dermatology, pain management, and oncology has significantly driven market expansion. Patients increasingly prefer therapies that offer minimal side effects and shorter recovery times, making photomedicine a preferred option. Additionally, North America benefits from favorable regulatory frameworks, which facilitate the approval and integration of novel medical devices and therapies.

The United States remains the leading contributor, with a high concentration of hospitals, specialty clinics, and research institutions actively adopting photodynamic therapy and light-based diagnostic solutions. Continuous innovation and a focus on personalized medicine further strengthen the U.S. market’s growth trajectory.

Canada also contributes meaningfully, particularly through increased utilization of photomedicine in dermatology and wound healing. The country’s emphasis on enhancing healthcare outcomes through technological innovation supports its steady market growth. Overall, North America is expected to retain its leadership in the global photomedicine market throughout the forecast period.

Emerging Trends

- Regulatory Support for Novel Excipients: A voluntary FDA pilot program (PRIME) has been established to review excipients that have never been used in approved drug products and are not common in food. In its first two years, CDER planned to accept approximately four initial proposals (two per year) for in depth review of toxicology and quality data.

- Growth of Co Processed Excipients: The EMA has released harmonized Q&As defining three risk categories for co processed excipients (CoPEs) used in solid oral dosage forms. These combined ingredients are increasingly adopted to achieve multiple functions (e.g., binder+disintegrant) in a single material, reducing tablet size and simplifying manufacturing.

- Enhanced Review Capacity for Excipient Suitability Petitions: Under GDUFA performance goals, the FDA aims to review up to 50 excipient suitability petitions within six months in FY 2024, increasing to 70 petitions in FY 2025 and 80 in FY 2026. This rising capacity is intended to accelerate generic drug development when a novel excipient change is proposed.

- Early Stage Engagement on Excipient Selection: FDA guidance now encourages sponsors to discuss novel excipient use during the IND stage. Early engagement is promoted to address safety and formulation challenges before pivotal clinical studies.

- Replacement of Titanium Dioxide: Following safety evaluations, the EMA issued technical guidance in July 2022 on the removal or replacement of titanium dioxide in oral dosage forms. This has driven research into alternative whitening and opacifying agents compliant with EU food contact regulations.

Use Cases

- Opioid Abuse Deterrent Formulations: Two novel excipient proposals aimed at improving viscosity and gel strength for abuse deterrent opioid tablets were selected in the first two years of FDA’s PRIME program. These excipients are being evaluated for their potential to resist tampering and slow release of active drug.

- Generic Drug Reformulation via Suitability Petitions: In FY 2024, the FDA completed up to 50 excipient suitability petition reviews within the six month goal. This use case involves generic sponsors petitioning to substitute an FDA approved excipient (e.g., microcrystalline cellulose) with a functionally equivalent alternative, enabling product launches without full new drug applications.

- Solid Oral Dosage with Co Processed Excipients: Manufacturers of immediate release tablets are increasingly using CoPEs categorized by EMA into Risk Category I (low risk), Category II (moderate risk), and Category III (high risk) based on composition complexity. This approach streamlines formulations by combining two or more functions (e.g., filler+binder) in 1–3 materials.

- IND Stage Formulation Optimization: During early clinical development, sponsors have leveraged FDA’s recommendation to engage on novel excipients, resulting in improved bioavailability and reduced animal testing. In several IND programs, excipient discussions occurred within 6 weeks of submission to the agency, expediting first in human studies.

- Formulation Without Titanium Dioxide: By July 2022, over 30 marketing authorization holders in the EU had submitted variations to replace titanium dioxide with alternative pigments (e.g., calcium carbonate) in solid oral products, in line with EMA’s technical guidance.

Conclusion

The global Photomedicine Technology Market is experiencing robust growth, driven by rising demand for non-invasive, targeted therapies across dermatology, oncology, and pain management. Advancements in laser and light-based technologies, combined with strong regional performance particularly in North America are enhancing treatment outcomes and expanding market potential.

With the market projected to reach USD 16.3 billion by 2033, key players stand to benefit from high-margin opportunities, regulatory support, and expanding applications. Emerging trends in device innovation and personalized care, alongside increased adoption in both clinical and wellness settings, position photomedicine as a transformative force in modern healthcare delivery.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)