Introduction

Pet Food Statistics: The pet food sector is a lively industry committed to manufacturing and delivering food for domesticated animals, especially dogs and cats.

It’s presently witnessing expansion, driven by factors like higher pet ownership. An emphasis on pet well-being and a growing desire for top-quality and specialized pet food choices.

Leading companies in this field encompass Nestlé Purina PetCare, Mars Petcare Inc., Hill’s Pet Nutrition, and Blue Buffalo.

To sum up, the pet industry is adapting to meet evolving consumer preferences and the rising significance of pets in our daily lives.

Editor’s Choice

- The global pet food market revenue is anticipated to reach 186.10 billion in 2028.

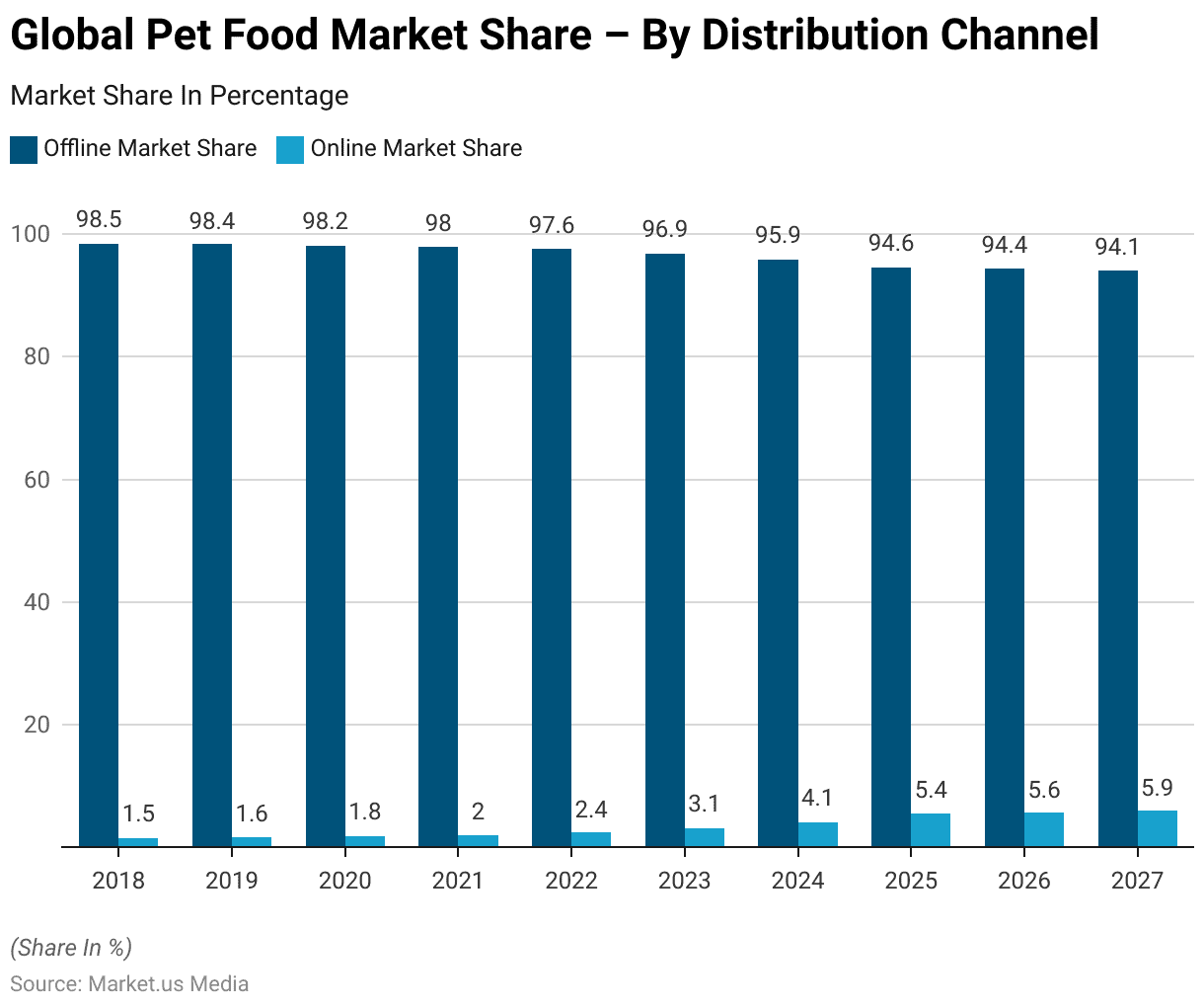

- By 2025, offline channels are projected to hold 94.6% of the market share. While online channels are anticipated to capture 5.4%.

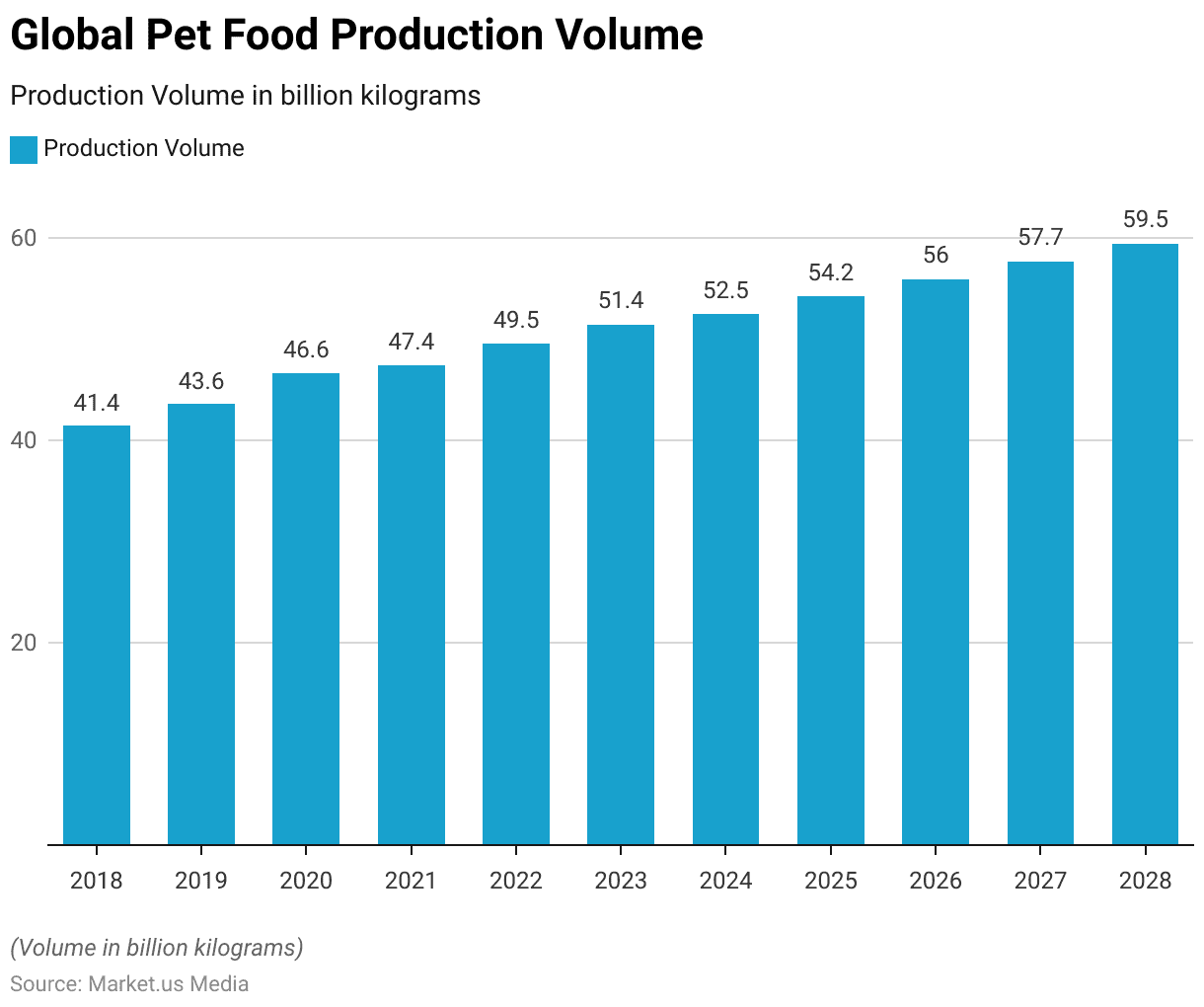

- The trend of increasing production is forecasted to persist, with production volumes of 52.51 billion kilograms in 2024.

- The pet food sales reached a value of USD 133.9 billion in 2023.

- A significant 93% of respondents prioritize a product that they believe their dog or cat will enjoy, emphasizing the importance of palatability.

- Approximately 37% of pet owners are in search of discounts on pet items. While 28% are making use of loyalty programs to accumulate savings.

- A significant portion of pet owners, around 77%, are well aware that cats and dogs have different dietary requirements.

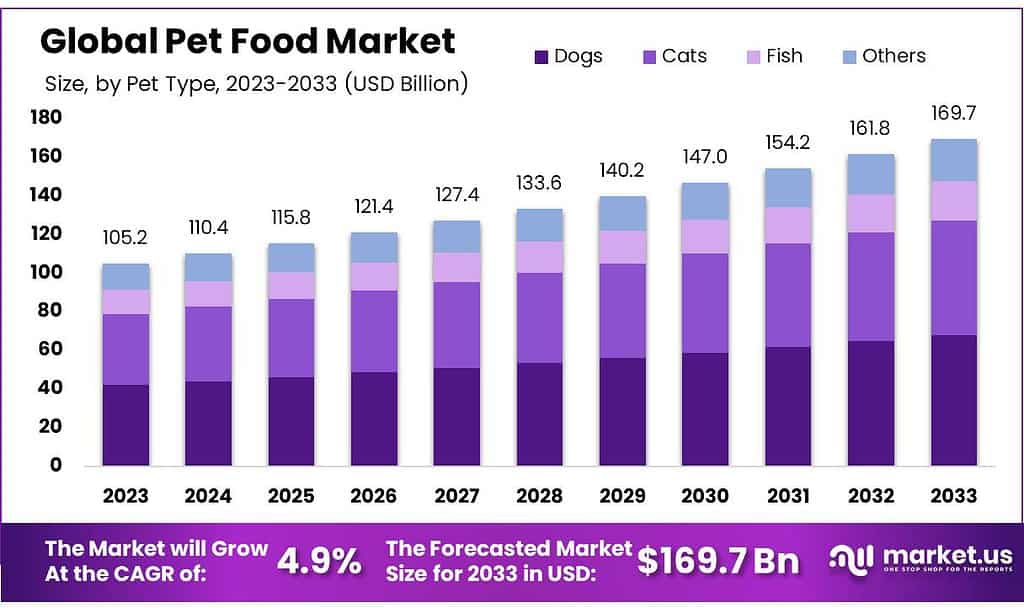

Global Pet Food Market Overview

Global Pet Food Market Size Statistics

- The global pet food market has exhibited a remarkable growth trajectory over the past few years at a CAGR of 5.6%.

- In 2018, the market’s revenue stood at USD 88.91 billion, and by the end of 2019, it had increased to USD 98.57 billion.

- The year 2020 witnessed a further substantial rise, with the market reaching USD 111.90 billion.

- This growth trend continued in 2021, as the market revenue soared to USD 121.00 billion.

- Looking ahead, the market is expected to maintain its upward trajectory. With projected revenues of USD 133.70 billion in 2022 and USD 143.60 billion in 2023.

- The forecast for the coming years remains optimistic, with the pet food market projected to reach USD 149.90 billion in 2024, USD 158.60 billion in 2025, and a promising USD 167.70 billion in 2026.

- This growth is expected to persist, with revenues reaching USD 177.40 billion in 2027 and USD 186.10 billion in 2028.

- These figures reflect the industry’s resilience and the increasing importance placed on pet nutrition and well-being in households worldwide.

(Source: Statista)

Pet Food Market Share – By Distribution Channel Statistics

- The global pet food market’s distribution channel dynamics have witnessed a gradual shift in recent years.

- In 2018, offline distribution channels dominated, accounting for 98.5% of the market share. While online channels held a modest 1.5% share.

- This trend continued in 2019, with offline channels at 98.4% and online at 1.6%. However, a notable transition began in 2020, as offline channels slightly decreased to 98.2%, while online channels saw a gradual increase to 1.8%.

- The momentum continued in 2021, with offline channels at 98.0% and online channels reaching a 2% market share.

- The shift toward online channels accelerated in subsequent years, with offline market shares declining to 97.6% in 2022 and further to 96.9% in 2023. Simultaneously, online channels experienced steady growth, capturing 2.4% in 2022 and a substantial 3.1% market share in 2023.

- This transition intensified in 2024 when offline channels dipped to 95.9%, while online channels gained significant ground, reaching 4.1%.

- Looking ahead, the trend of online market expansion is expected to continue. By 2025, offline channels are projected to hold 94.6% of the market share. While online channels are anticipated to capture 5.4%.

- In 2026, the divide narrows further, with offline channels at 94.4%, and online channels growing to 5.6%. This shift is expected to reach a critical point in 2027, as offline channels are predicted to account for 94.1%, while online channels are projected to secure 5.9% of the market share.

- These developments reflect the changing consumer preferences and the increasing prominence of online shopping for pet food products in the global market landscape.

(Source: Statista)

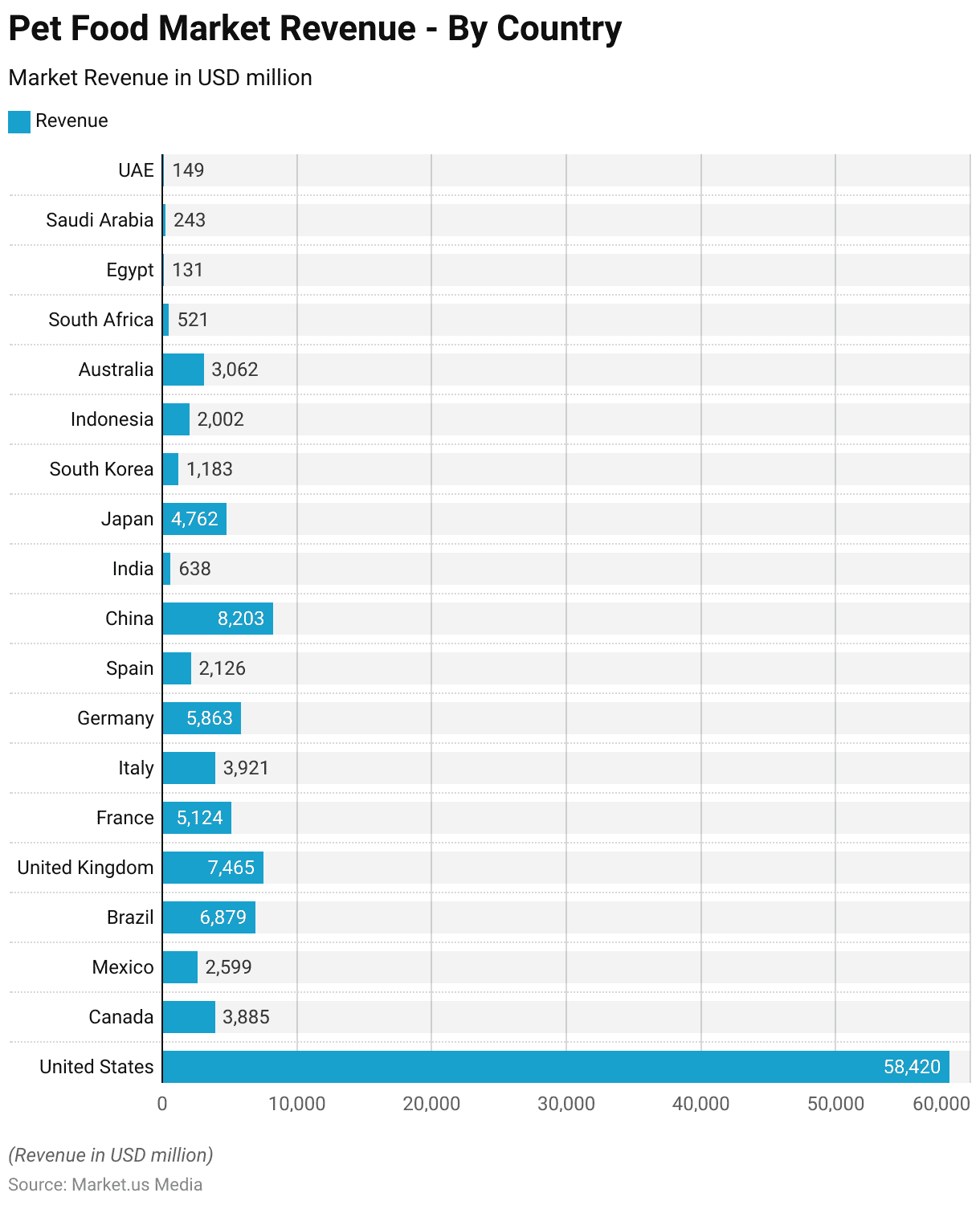

Regional Analysis of the Pet Food Market Statistics

North America

- The regional analysis of the pet food market reveals significant variations in revenue across different countries.

- Leading the pack, the United States stands out with a substantial revenue of USD 58,420 million, reflecting its status as a major pet-loving nation.

- In North America, Canada and Mexico contribute USD 3,885 million and USD 2,599 million, respectively, highlighting their growing pet food markets.

(Source: Statista)

Europe

- Moving across the Atlantic, Europe demonstrates its importance in the industry.

- The United Kingdom, with USD 7,465 million, showcases a strong market presence. Followed by France with USD 5,124 million, Italy with USD 3,921 million, and Germany with USD 5,863 million.

- Spain, while smaller in comparison, still contributes a notable USD 2,126 million to the regional market.

(Source: Statista)

Asia Pacific

- In the Asia-Pacific region, China emerges as a key player with USD 8,203 million in pet food revenue, underscoring the expanding pet ownership trend.

- India, Japan, South Korea, and Indonesia exhibit varying market sizes, with India at USD 638 million. Japan at USD 4,762 million, South Korea at USD 1,183 million, and Indonesia at USD 2,002 million.

- Australia, in the same region, reports a noteworthy USD 3,062 million in pet food revenue, signifying its substantial presence in the market.

(Source: Statista)

Middle East and Africa

- In the context of the pet food market, several countries in the Middle East and Africa region are making their mark, albeit with varying levels of market revenue.

- South Africa stands out with a revenue of USD 521 million, showcasing a growing pet food industry within the country.

- Egypt, with USD 131 million in revenue, reflects a developing market with potential for expansion. Similarly, Saudi Arabia reports a noteworthy USD 243 million, indicating a significant presence in the region’s pet food sector.

- Meanwhile, the United Arab Emirates (UAE) contributes USD 149 million to the market, highlighting its role in the growing pet food industry in the Middle East.

(Source: Statista)

Pet Food Production Statistics

Production Volume

- The global pet food production volume has displayed a consistent upward trajectory in recent years.

- In 2018, the production volume amounted to 41.43 billion kilograms, and this figure steadily increased to 43.61 billion kilograms in 2019.

- The trend continued in 2020, as production rose to 46.62 billion kilograms. In 2021, the industry produced 47.39 billion kilograms of pet food, reflecting continued growth.

- Looking ahead, the production volume is projected to maintain its positive momentum. In 2022, it is expected to reach 49.53 billion kilograms, followed by 51.44 billion kilograms in 2023.

- The trend of increasing production is forecasted to persist, with production volumes of 52.51 billion kilograms in 2024, 54.22 billion kilograms in 2025, and 55.95 billion kilograms in 2026.

- The upward trajectory continues through the forecast period, with production volumes projected to reach 57.69 billion kilograms in 2027 and 59.47 billion kilograms in 2028.

- These figures highlight the industry’s growth, driven by the rising demand for pet food products and the increasing focus on pet nutrition and well-being globally.

(Source: Statista)

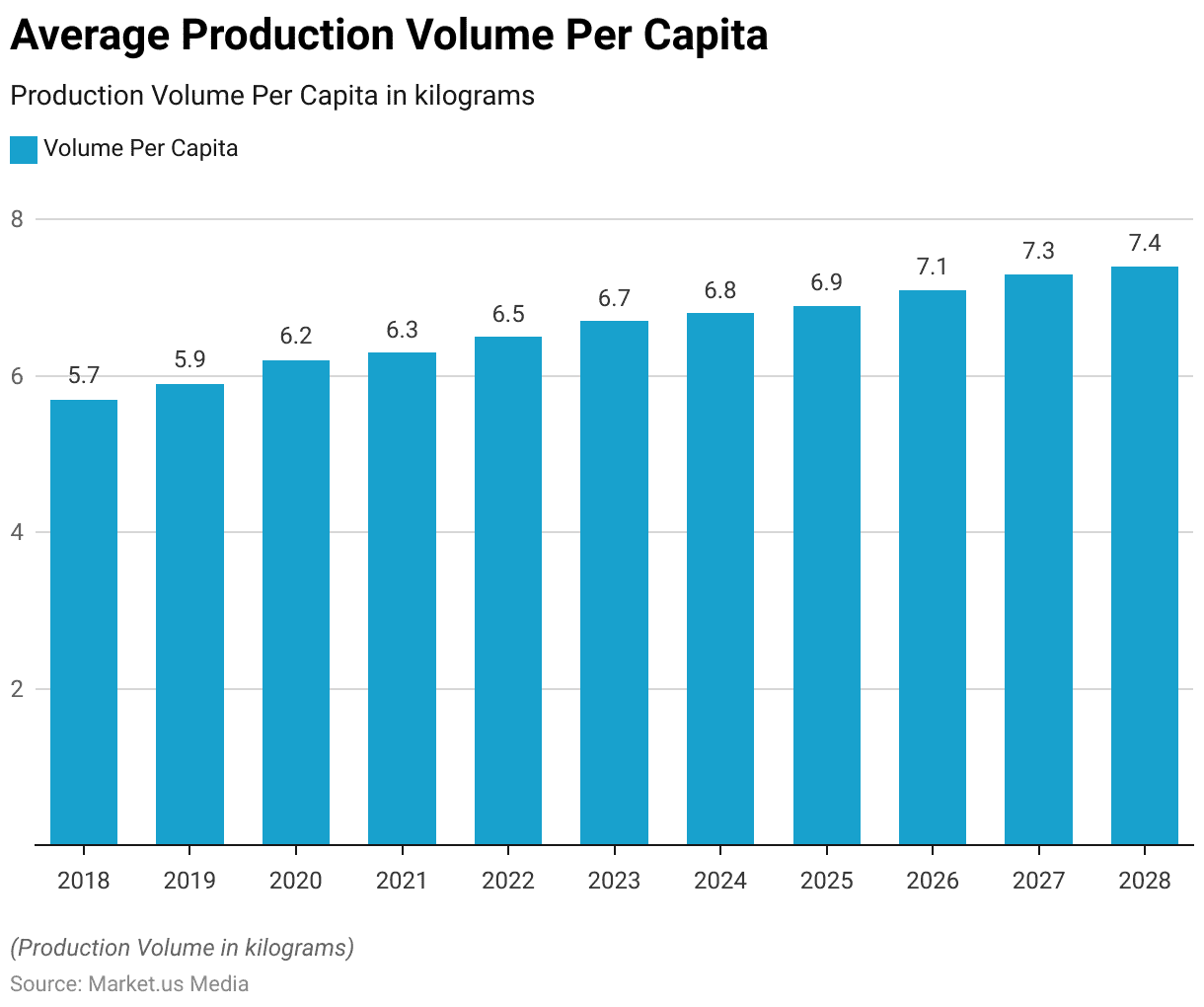

Average Per Capita Production Volume

- The average production volume of pet food per capita has demonstrated a consistent increase over the years. Reflecting the growing demand for pet nutrition and the evolving dietary preferences of pet owners.

- In 2018, the average production volume per capita stood at 5.7 kilograms, and by the end of 2019, it had risen to 5.9 kilograms.

- This upward trend continued in 2020, with per capita production reaching 6.2 kilograms. Emphasizing the industry’s commitment to meeting the dietary needs of pets.

- As we progress through the years, the average production volume per capita is projected to maintain its growth trajectory. In 2021, it reached 6.3 kilograms, and in 2022, it is expected to further increase to 6.5 kilograms.

- The forecast for the coming years remains positive, with per capita production projected to reach 6.7 kilograms in 2023, 6.8 kilograms in 2024, and 6.9 kilograms in 2025.

- The trend of increasing per capita production continues, with projected averages of 7.1 kilograms in 2026, 7.3 kilograms in 2027, and 7.4 kilograms in 2028.

- These figures underscore the industry’s dedication to ensuring a consistent supply of high-quality pet food. To meet the growing demand and the evolving expectations of pet owners worldwide.

(Source: Statista)

Pet Food Price Statistics

- The price per unit of pet food, denominated in USD, has exhibited a gradual but consistent upward trend over the years.

- In 2018, the price per unit was recorded at USD 2.15, and this figure steadily increased to USD 2.26 in 2019, reflecting moderate price growth.

- The trend continued in 2020, as the price per unit reached USD 2.40, and further accelerated in 2021 when it rose to USD 2.55.

- Looking ahead, the price per unit is projected to continue its ascent. In 2022, it is expected to reach USD 2.70, followed by USD 2.79 in 2023.

- The upward trajectory persists in 2024, with a price of USD 2.85 per unit, and in 2025 when it is anticipated to be USD 2.93.

- As we move into 2026 and beyond, the trend remains positive. With prices projected to reach USD 3.00 in 2026, USD 3.08 in 2027, and USD 3.13 in 2028.

- These figures highlight the industry’s response to factors such as inflation, ingredient costs, and consumer demand. For premium and specialized pet food products, resulting in gradual but sustained price increases in the pet food market.

(Source: Statista)

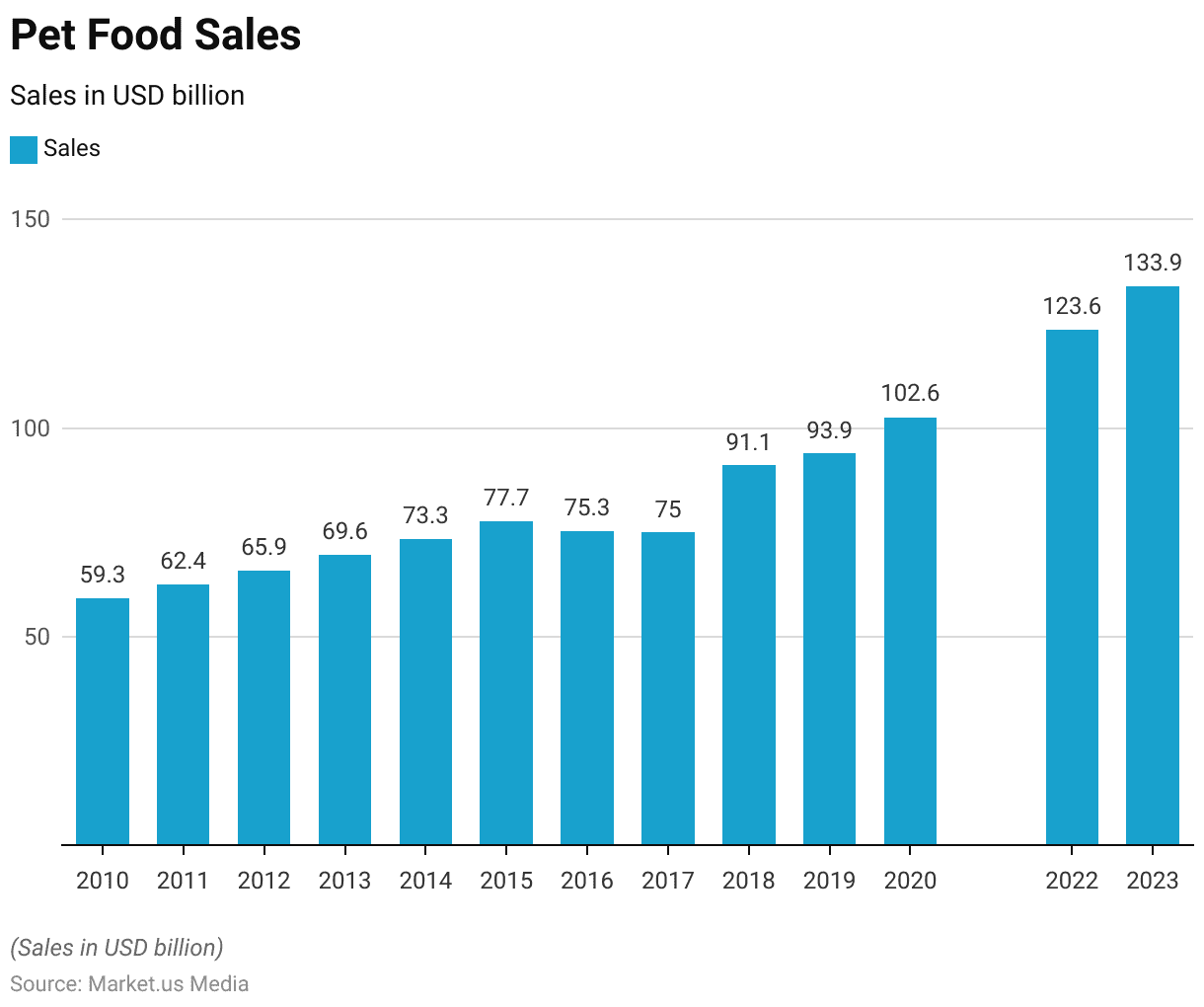

Global Pet Food Sales Statistics

- The pet food industry has witnessed substantial growth in sales over the past decade. Reflecting the evolving preferences and priorities of pet owners.

- In 2010, pet food sales amounted to USD 59.3 billion, and this figure steadily increased in the subsequent years.

- By 2014, sales had reached USD 73.3 billion, indicating a growing market.

- While 2016 saw a slight dip in sales to USD 75.25 billion, the trend reversed, and by 2018. The industry experienced a significant surge with sales reaching USD 91.1 billion.

- This growth continued in 2019, with sales totaling USD 93.9 billion, and further accelerated in 2020, when the industry recorded sales of USD 102.6 billion.

- Looking ahead, the forecast is optimistic, with projected sales of USD 123.6 billion in 2022 and USD 133.9 billion in 2023.

- These figures underscore the robust nature of the pet food market, driven by an increasing emphasis on pet nutrition, wellness, and the humanization of pets, making it a dynamic and thriving industry.

(Source: Statista)

Pet Food Preferences Statistics

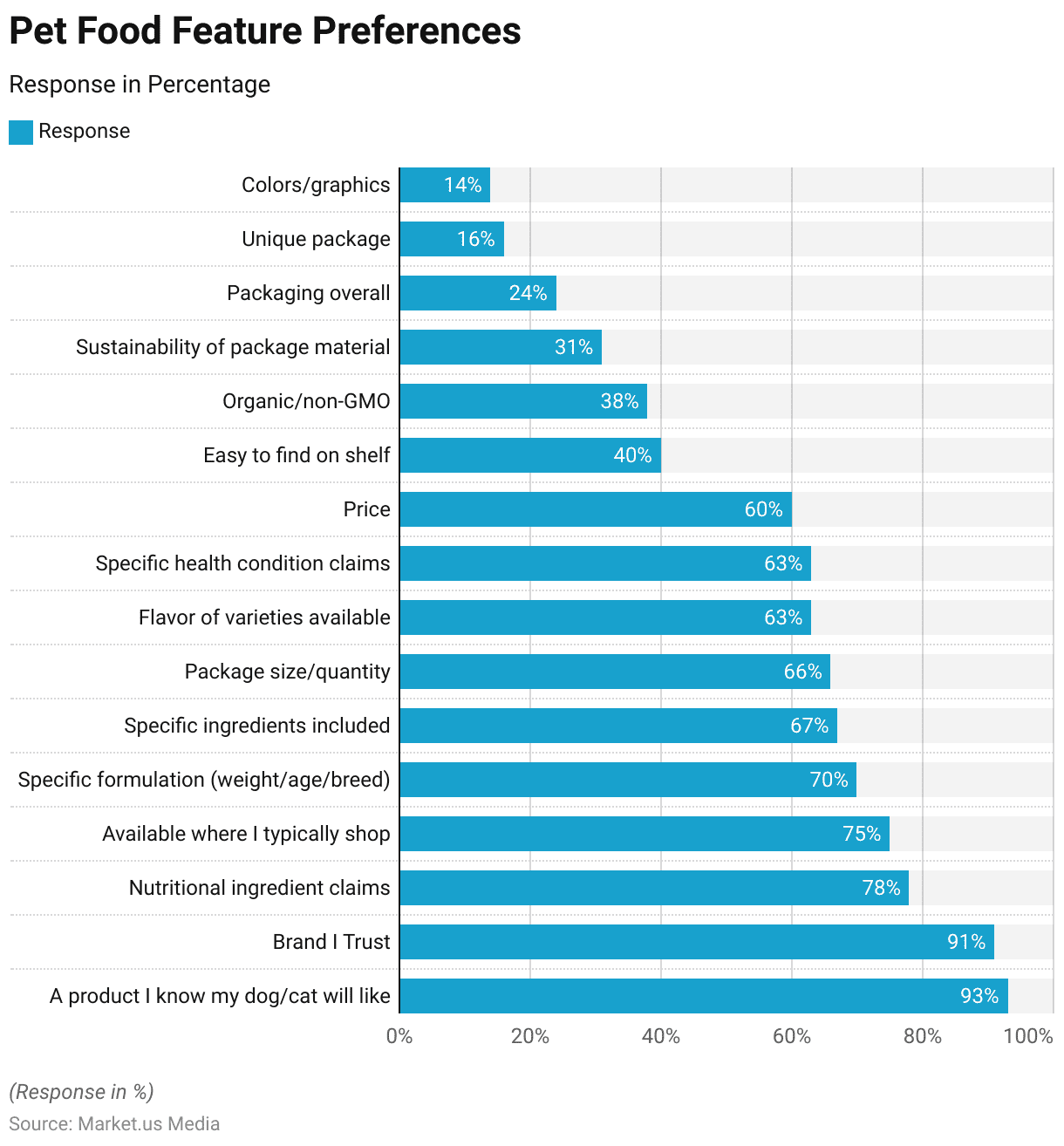

Feature Preferences

- The Mondi and Dow Chemical survey results reveal the preferences of respondents regarding the importance they assign to various features when choosing pet food products.

- Notably, a significant 93% of respondents prioritize a product that they believe their dog or cat will enjoy, emphasizing the importance of palatability.

- Additionally, 91% of respondents value brands they trust, indicating the role of brand reputation in their decision-making process.

- Nutritional ingredient claims hold considerable weight as well, with 78% of respondents deeming them important.

- Furthermore, 75% consider the availability of pet food in their usual shopping locations as a crucial factor, emphasizing convenience.

- Specific formulations tailored to weight, age, or breed are important to 70% of respondents. While 67% value knowing the specific ingredients included in the product.

- Other factors influencing purchasing decisions include package size or quantity (66%), flavor variety availability (63%), and health condition claims (63%).

- Price is a significant consideration for 60% of respondents. In contrast, features such as ease of finding the product on the shelf (40%), and organic or non-GMO status (38%). Sustainability of package materials (31%), and packaging overall (24%) are of moderate importance.

- Unique packaging, colors, and graphics are ranked as less important, with 16%, 14%, and 9% of respondents, respectively, valuing these features.

- These insights provide valuable guidance to pet food manufacturers, highlighting the key factors that influence consumers when making choices for their beloved pets.

(Source: Mondi and Dow Chemical Survey)

Other Preferences

- Some pet owners remain steadfast in their standards when purchasing pet products, while others are actively looking for ways to save money.

- Approximately 37% of pet owners are in search of discounts on pet items. While 28% are making use of loyalty programs to accumulate savings.

- Nevertheless, the majority of consumers are not willing to compromise on the quality of the products they buy for their pets.

- According to a report by Vericast, 78% of survey participants are open to increasing their spending on pet food and treats in the current year compared to 2022.

- Furthermore, 38% of respondents indicated a willingness to pay a higher price for health-related pet products like supplements and vitamins.

- Pet owners are diversifying their shopping habits for pet products, with 32% opting for specialty stores such as Petco or PetSmart. 30% favoring other large retail stores, 20% preferring online shopping, and 13% seeking out local boutique pet shops.

(Source: Pet Food Processing)

Latest Consumer Trends in Pet Food Industry

- A significant portion of pet owners, around 77%, are well aware that cats and dogs have different dietary requirements.

- Specifically, the belief that cats are natural carnivores is widespread, with only 16.4% thinking otherwise.

- However, opinions on dogs’ dietary nature are more varied, with 45.6% considering them carnivores. 42.5% regard them as omnivores, and a small 2.4% classify them as herbivores.

- Interestingly, a majority of survey participants (approximately 79.9%) have not fed their dogs a vegan or plant-based diet.

- Of the minority who have, their motivations vary. Approximately 58% believe it’s beneficial for their dogs’ health, 41.7% view it as an eco-friendly choice, 38% are vegans themselves, and 30.6% do it due to their dogs’ allergies.

- Furthermore, almost half of pet owners (45.9%) express a willingness to transition their dogs to a vegan diet.

- Their primary reasons include the perceived health benefits and the belief that it’s more environmentally friendly.

(Source: Global Pet Food Industry)

Recent Developments

Acquisitions and Mergers:

- Wind Point Partners acquired UK-based Assisi Pet Care Group to expand its presence in the European Union pet food market.

- General Mills entered the pet supplement category with its acquisition of Fera Pets, Inc., aligning with the creation of its growth equity fund.

- Antelope acquired Ark Naturals Company, a pet health and wellness brand known for its functional pet chews.

- United Petfood purchased Gold Line Feeds, a UK-based animal feed manufacturer, bolstering its production capabilities.

- Mars Petcare plans to acquire Champion Petfoods, which includes well-known brands ORIJEN and ACANA.

New Product Launches:

- Mars Petcare’s TEMPTATIONS brand launched a new complete-and-balanced dry cat food line, expanding beyond its traditional treat products.

- Benebone introduced a new dog chew shaped for easy handling and flavored with real beef tripe.

- Blue Buffalo launched the BLUE Wilderness Premier Blend, a high-protein dry dog food line that mixes dry kibble with new tender meaty cuts.

Funding Rounds:

- Series C funding round for a pet food startup focusing on personalized nutrition for pets in February 2024. Raising $50 million to expand product lines and invest in research and development.

- Seed funding for a novel pet food ingredient company in April 2024, securing $10 million to develop innovative ingredients for premium pet food formulations.

Investment Landscape:

- Venture capital investments in pet food startups totaled $3.2 billion in 2023, with a focus on companies offering innovative pet food formulations and sustainable packaging solutions.

- Strategic partnerships and acquisitions between pet food brands, retail chains, and technology companies accounted for 60% of total investment activity in the pet food market in 2023, reflecting industry efforts to capitalize on evolving consumer trends and preferences in the pet food industry.

Conclusion

Pet Food Statistics – The pet food industry is thriving, driven by the evolving preferences of pet owners. Consumers prioritize factors like taste, brand trust, and nutritional value when choosing pet products. Quality remains a top concern, leading many to consider premium options.

Pet owners shop through various channels, from specialty stores to online platforms. Awareness of pets’ dietary needs is high, with recognition that cats and dogs have different requirements.

Some are open to feeding dogs a vegan diet, citing health and eco-friendly reasons. Overall, the industry adapts to meet changing demands, promising growth as pets become cherished family members.

FAQs

The growth of the pet food market can be attributed to factors such as increasing pet ownership, humanization of pets, rising disposable incomes, and a growing awareness of pet health and nutrition.

Some notable trends in the pet food industry include a shift towards natural and organic ingredients, grain-free and limited-ingredient diets, as well as a focus on sustainability and eco-friendly packaging.

Regulatory agencies like the FDA (Food and Drug Administration) in the United States set standards for pet food safety and labeling. They monitor pet food manufacturers to ensure compliance with these standards.

Challenges include concerns over product recalls, the need for transparency in labeling, and addressing specific dietary requirements for pets with allergies or sensitivities.

E-commerce has significantly influenced the distribution of pet food, making it convenient for consumers to purchase online. Many pet food brands now offer direct-to-consumer options.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)