Table of Contents

Overview

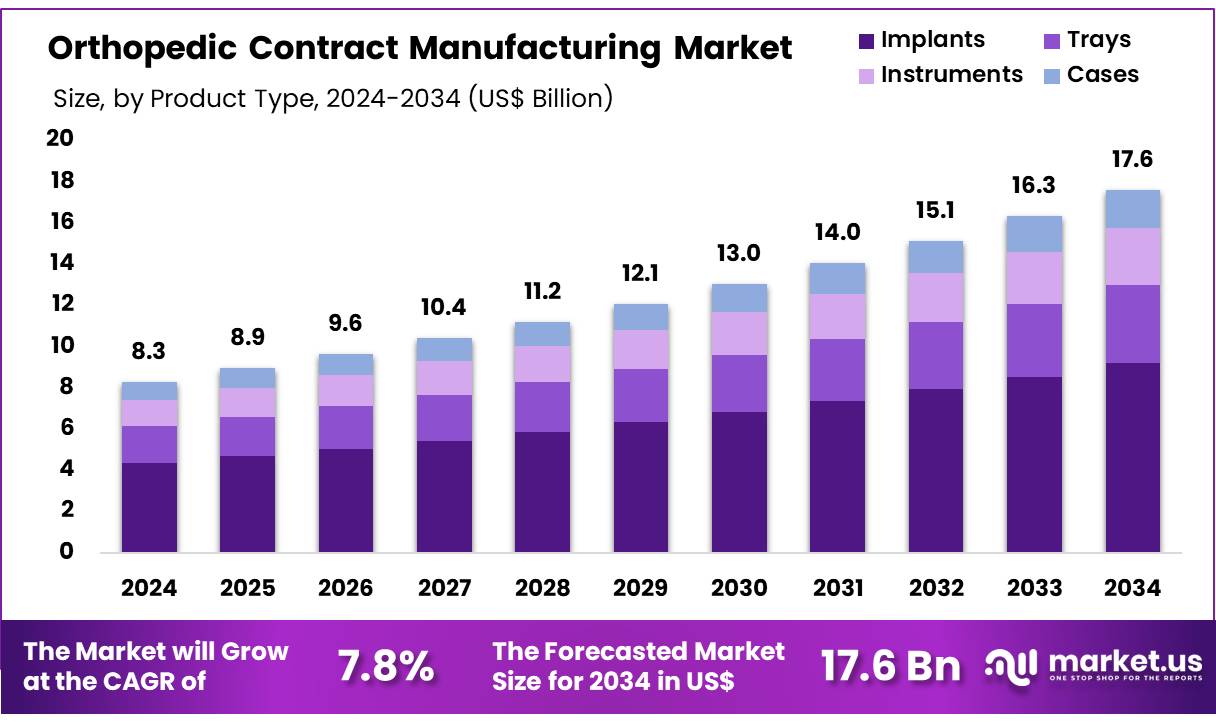

New York, NY – Nov 21, 2025 – Global Orthopedic Contract Manufacturing Market size is expected to be worth around US$ 17.6 billion by 2034 from US$ 8.3 billion in 2024, growing at a CAGR of 7.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.4% share with a revenue of US$ 3.2 Billion.

The global orthopedic contract manufacturing market is experiencing steady expansion as increasing demand for advanced medical implants and instruments continues to influence production activities across the sector. Strong growth has been attributed to the rising prevalence of orthopedic disorders, expanding geriatric populations, and the widespread adoption of minimally invasive surgical procedures. The market has also been strengthened by the growing preference of medical device companies to outsource complex manufacturing functions in order to reduce operational costs and accelerate product commercialization.

Significant investments in precision engineering, additive manufacturing, and high-performance biomaterials have contributed to enhanced product quality and improved performance outcomes. Surge in customization requirements for orthopedic implants has further supported the role of contract manufacturers, as advanced capabilities in design support, prototyping, and regulatory compliance have become essential.

North America continues to lead market activity due to the presence of established medical device manufacturers and a robust regulatory ecosystem. Asia-Pacific is expected to witness faster growth, driven by the availability of cost-efficient production facilities and increasing healthcare expenditure in emerging economies.

Manufacturers are focusing on strategic partnerships, capacity expansions, and technology integration to strengthen their competitive positioning. The market outlook remains positive as healthcare providers and device developers seek reliable, scalable, and technologically advanced manufacturing partners to support next-generation orthopedic solutions

Key Takeaways

- In 2024, orthopedic contract manufacturing revenue reached US$ 8.3 billion, supported by a 7.8% CAGR, and the market is projected to attain US$ 17.6 billion by 2033.

- The implants category accounted for the largest share within product types in 2024, representing 52.3% of the market.

- Within services, forging/casting emerged as the dominant segment, contributing 48.7% of total market share.

- North America led the global landscape with a 38.4% market share in 2024.

Regional Analysis

North America is leading the orthopedic contract manufacturing market

North America commanded the largest revenue share of 38.4%, supported by rising demand for joint replacements, trauma implants, and advanced surgical tools. A 12% increase in 510(k) clearances for orthopedic devices reported by the US Food and Drug Administration (FDA) in 2023 indicated stronger production requirements. Procedure volumes also expanded, as noted by the Centers for Medicare & Medicaid Services (CMS), which recorded an 8% rise in orthopedic interventions during the same year, reinforcing the need for outsourced manufacturing.

Major industry participants increased their reliance on external manufacturers. Stryker reported a 15% rise in contract manufacturing expenditures, and Zimmer Biomet followed similar sourcing patterns. The American Academy of Orthopaedic Surgeons (AAOS) registered a 20% increase in robotic-assisted surgeries in 2023, which heightened the need for precision-engineered orthopedic components. Alongside robust US medical device export activity, these developments strengthened North America’s role as a central hub for orthopedic manufacturing.

Asia Pacific is expected to experience the highest CAGR during the forecast period

The Asia Pacific region is projected to expand at the fastest CAGR due to improving healthcare systems, cost advantages, and supportive government policies. India’s Department of Pharmaceuticals reported a 22% increase in medical device production in 2023, influenced by initiatives such as the Production Linked Incentive (PLI) scheme. China’s National Medical Products Administration (NMPA) recorded an 18% rise in approvals for orthopedic implants in 2023, reflecting stronger manufacturing momentum.

Japan’s Ministry of Health, Labour and Welfare documented a 10% increase in orthopedic surgeries in 2023, which contributed to additional production requirements. Countries such as Thailand and Vietnam experienced a 13% increase in medical exports in 2023, according to World Bank trade data, thereby attracting more outsourcing from international medical device companies. Australia’s Therapeutic Goods Administration (TGA) also accelerated regulatory processes, with orthopedic device clearances rising by 25% in 2023. These indicators suggest continued regional expansion supported by growing investment in medical technology and streamlined regulatory frameworks.

Emerging Trends

The adoption of additive manufacturing has strengthened the production of patient-specific implants and surgical tools. Three-dimensional printing supports intricate geometries and porous structures that enhance bone ingrowth while reducing lead times and material waste. Regulatory oversight under the FDA Quality System Regulation (21 CFR Part 820) has intensified, with the Center for Devices and Radiological Health accepting 3,276 510(k) submissions in FY 2023, reinforcing the need for stringent design control and validated processes that many OEMs now outsource to specialized contract manufacturers.

Supply chain resilience has gained significant priority in response to earlier disruptions. Domestic and near-shore production strategies are being reassessed to ensure the continuity of essential device manufacturing. Long-term partnership agreements between OEMs and CMOs have become more common, supported by programs such as the Medicare Comprehensive Care for Joint Replacement Model, which rewards cost efficiency and quality, encouraging providers to engage manufacturing partners capable of ensuring compliance and scalable capacity.

Use Cases

Total knee replacements remain a major driver of orthopedic manufacturing demand. The CDC National Hospital Discharge Survey reported 719,000 total knee replacement procedures in the United States in 2010, highlighting the sustained requirement for precision-engineered femoral and tibial components. Contract manufacturers support this demand by producing high-volume implants within controlled clean-room environments and adhering to FDA-mandated sterilization standards.

Spinal implant instrumentation serves as another significant application. In December 2024, the FDA cleared a Titanium Niobium Nitride–coated stemmed femoral component for total disc replacement devices under traditional 510(k) number K242869. This approval illustrates the advanced machining and coating capabilities required, which are frequently outsourced to CMOs with strong regulatory and quality management expertise.

Additionally, more than 671,000 fracture reduction procedures were recorded in 2010, sustaining demand for contract-manufactured plates, screws, and fixation systems engineered to precise biomechanical performance requirements.

Frequently Asked Questions on Orthopedic Contract Manufacturing

- Why do orthopedic companies outsource manufacturing?

Outsourcing is adopted to lower operational expenses, access advanced production capabilities, and reduce the burden of regulatory compliance. Partnerships allow companies to focus on innovation and commercialization while leveraging contract manufacturers’ expertise in precision engineering, materials, and quality assurance. - Which products are commonly produced through orthopedic contract manufacturing?

Commonly manufactured products include joint reconstruction implants, trauma fixation devices, spinal implants, arthroscopy instruments, and orthopedic power tools. High-precision metal and polymer components are produced to meet stringent performance, biocompatibility, and regulatory standards required in global orthopedic markets. - Which materials are widely used in orthopedic contract manufacturing?

Materials commonly include titanium alloys, stainless steel, cobalt-chromium, and high-performance polymers like PEEK. These materials are selected for superior biocompatibility, mechanical strength, corrosion resistance, and long-term reliability essential for orthopedic implants and surgical instruments. - What quality standards govern orthopedic contract manufacturing?

Manufacturing activities follow global standards such as ISO 13485, FDA 21 CFR Part 820, and EU MDR requirements. These standards ensure consistent product safety, validated processes, rigorous traceability, and continuous quality management across production and supply chain operations. - Which product segments dominate the market?

Joint reconstruction, trauma fixation, and spinal implants represent major segments due to high procedure volumes and steady innovation. Demand for advanced materials, surface technologies, and personalized implant solutions strengthens production requirements across these leading categories. - What role does technology play in market growth?

Adoption of CNC machining, robotics, automation, and additive manufacturing strengthens efficiency and precision. These technologies lower production errors, improve scalability, and support innovative implant designs that help contract manufacturers meet evolving clinical and regulatory expectations. - Which regions lead the orthopedic contract manufacturing market?

North America dominates due to strong regulatory frameworks, advanced manufacturing infrastructure, and concentration of large orthopedic companies. Europe follows closely, while Asia-Pacific experiences accelerating growth supported by cost advantages, rising healthcare investments, and expanding device production capabilities. - How is demand for customized implants influencing the market?

Growing demand for patient-specific implants encourages investment in digital modeling and 3D printing capabilities. Contract manufacturers benefit from this trend as medical device companies increasingly rely on external partners for customization and precision-engineered orthopedic solutions.

Conclusion

The global orthopedic contract manufacturing market is expected to maintain a positive trajectory as demand for advanced implants, specialized materials, and precision technologies continues to rise. Growth is supported by expanding surgical volumes, increasing customization needs, and strengthened regulatory oversight that encourages OEMs to rely on specialized manufacturing partners.

North America retains a dominant position, while Asia Pacific demonstrates rapid expansion driven by cost advantages and supportive government initiatives. Ongoing investments in automation, additive manufacturing, and quality systems are expected to enhance production efficiency and scalability. Overall, the market outlook remains favorable as manufacturers adapt to evolving clinical and regulatory requirements.