Table of Contents

Overview

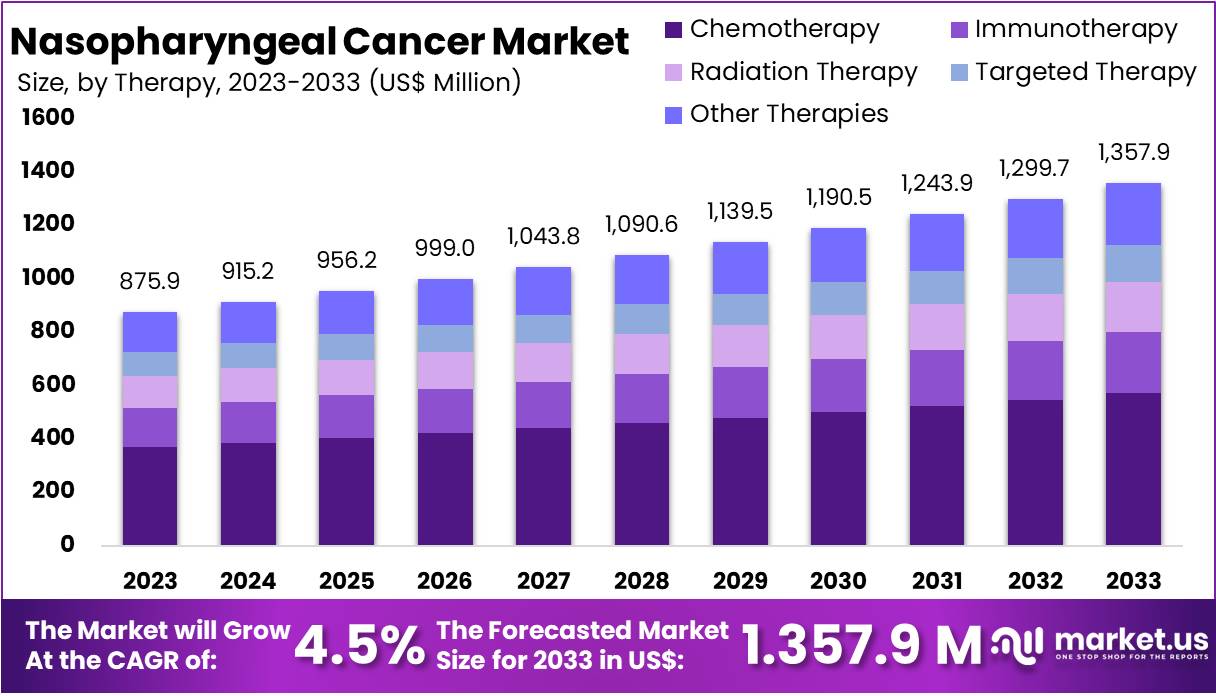

New York, NY – Feb 11, 2026 – The Global Nasopharyngeal Cancer Market size is expected to be worth around US$ 1357.9 Million by 2033, from US$ 875.9 Million in 2023, growing at a CAGR of 4.5% during the forecast period from 2024 to 2033. North America dominated the market, securing a 46.1% share with a market value of US$ 403.8 million.

Nasopharyngeal cancer is a malignant tumor that originates in the epithelial cells lining the nasopharynx, the upper part of the throat located behind the nose and above the back of the throat. The development of this cancer is primarily associated with a combination of genetic susceptibility, environmental exposure, and viral infection. Infection with the Epstein–Barr virus (EBV) has been identified as a significant contributing factor, particularly in endemic regions across East and Southeast Asia.

The formation of nasopharyngeal cancer typically begins with abnormal cellular changes in the mucosal lining of the nasopharynx. Persistent viral infection, along with exposure to risk factors such as consumption of salt-preserved foods, tobacco use, and occupational inhalants, can result in genetic mutations. These mutations disrupt normal cell growth regulation, leading to uncontrolled proliferation and tumor development. Over time, malignant cells may invade nearby tissues and spread to regional lymph nodes.

Early-stage disease may remain asymptomatic or present with non-specific symptoms, including nasal obstruction, epistaxis, hearing disturbances, or neck masses due to lymph node involvement. Early detection through clinical evaluation and imaging plays a critical role in improving patient outcomes. Ongoing research efforts are focused on advancing diagnostic techniques and targeted therapies to enhance survival rates and reduce disease burden globally.

Key Takeaways

- The global nasopharyngeal cancer market is expected to increase from US$ 875.9 million in 2023 to approximately US$ 1,357.9 million by 2033, registering a compound annual growth rate (CAGR) of 4.5% during the forecast period.

- North America accounted for the largest regional share of 46.1% in 2023, with a market valuation of US$ 403.8 million, supported by well-established healthcare infrastructure and strong research capabilities.

- Chemotherapy emerged as the leading therapy segment, representing more than 42.1% of the total market share in 2023, primarily driven by its widespread application in advanced-stage treatment.

- Hospitals and clinics constituted the dominant end-user category, contributing over 41.7% of the market share in 2023, owing to the availability of specialized facilities and comprehensive treatment services.

Regional Analysis

In 2023, North America accounted for over 46.1% of the global nasopharyngeal cancer market, reaching a valuation of US$ 403.8 million. Market leadership has been supported by a highly developed healthcare infrastructure that enables early diagnosis and access to advanced treatment options. Increased public awareness regarding disease symptoms has contributed to timely detection and improved clinical outcomes.

Substantial investments in research and development by academic institutions and oncology centers have accelerated the introduction of innovative therapies and advanced treatment technologies. The strong presence of specialized cancer research facilities has further facilitated the rapid adoption of novel therapeutic approaches across the region.

Supportive healthcare policies in the United States and Canada, along with significant government funding for cancer research, have strengthened treatment capabilities and innovation. In addition, comprehensive insurance coverage has improved patient access to a wide range of oncology services. Continued research initiatives and policy support are expected to sustain regional market growth over the forecast period.

Emerging Trends

- Integration of Immunotherapy into Standard Care: Immune checkpoint inhibitors targeting PD-1 are increasingly incorporated into first-line chemotherapy for recurrent or metastatic nasopharyngeal carcinoma. Clinical evidence from the JUPITER-02 trial demonstrated improved progression-free survival and overall survival, supporting the regulatory approval of toripalimab and accelerating biologic adoption.

- Liquid Biopsy via EBV DNA Screening: Circulating Epstein-Barr virus DNA assays have demonstrated high diagnostic accuracy for nasopharyngeal carcinoma screening, with sensitivity above 97% and specificity exceeding 98%. Screening programs have enabled earlier stage detection, significantly increasing stage I–II diagnoses compared with historical cohorts and improving intervention opportunities.

- De-escalated Radiation Guided by Treatment Response: Induction chemotherapy–guided intensity-modulated radiation therapy protocols are being evaluated to reduce long-term toxicities in nasopharyngeal carcinoma management. Radiation dose intensity is adjusted based on tumor response, aiming to minimize adverse effects such as xerostomia and dysphagia while maintaining therapeutic efficacy.

- Advances in Precision Imaging and AI Tools: Advanced imaging modalities, including functional MRI and PET, combined with artificial intelligence analytics, are enhancing tumor delineation and treatment response prediction. Early research indicates AI-driven models may forecast immunotherapy benefit, supporting personalized treatment planning and optimized clinical outcomes in nasopharyngeal carcinoma care.

Use Cases

- Community-Based EBV DNA Screening: Large-scale community screening initiatives using EBV antibody and DNA testing have demonstrated measurable detection rates. In a southern China cohort of approximately 52,000 participants, persistent EBV DNA positivity identified confirmed nasopharyngeal carcinoma cases following diagnostic imaging and biopsy evaluation procedures.

- First-Line Treatment of Recurrent or Metastatic NPC: Toripalimab combined with chemotherapy has been implemented as first-line therapy for recurrent or metastatic nasopharyngeal carcinoma. Clinical findings reported objective tumor response rates above 20% with durable responses, reinforcing the therapeutic role of immuno-oncology agents in advanced disease management.

- Maintenance Immunotherapy to Prolong Remission: Maintenance administration of toripalimab following combination therapy has demonstrated extended progression-free survival compared with chemotherapy alone. Long-term analyses indicate improved three-year overall survival rates, highlighting the value of sustained immunotherapy exposure in maintaining remission among advanced nasopharyngeal carcinoma patients.

- Response-Adapted Radiotherapy: Response-adapted intensity-modulated radiation therapy strategies are under clinical evaluation to tailor radiation doses according to chemotherapy response. This adaptive approach aims to reduce grade 3–4 toxicities while preserving tumor control, reflecting a broader transition toward precision-based radiotherapy frameworks in nasopharyngeal carcinoma treatment.

Frequently Asked Questions on Nasopharyngeal Cancer

- What are the common symptoms of nasopharyngeal cancer?

Common symptoms include persistent nasal congestion, nosebleeds, hearing loss, tinnitus, neck lumps due to lymph node enlargement, and headaches. Early symptoms are often mild, leading to delayed diagnosis in many patients. - What are the major risk factors associated with nasopharyngeal cancer?

Key risk factors include Epstein-Barr virus infection, genetic susceptibility, consumption of preserved foods high in nitrosamines, tobacco use, and environmental exposures. Geographic and ethnic predispositions significantly influence disease prevalence rates. - How is nasopharyngeal cancer diagnosed?

Diagnosis typically involves physical examination, nasoendoscopy, imaging techniques such as MRI or CT scans, and biopsy confirmation. Epstein-Barr virus DNA testing in blood is increasingly used for early detection and disease monitoring. - What treatment options are available for nasopharyngeal cancer?

Radiotherapy remains the primary treatment due to tumor location sensitivity. Chemotherapy is often combined for advanced stages, while targeted therapy and immunotherapy are being increasingly integrated into treatment protocols to improve survival outcomes. - What is the survival rate of nasopharyngeal cancer?

Survival rates vary by stage and geographic region. Early-stage detection demonstrates five-year survival rates exceeding 80%, whereas advanced-stage diagnosis significantly reduces survival prospects despite advancements in multimodal treatment approaches. - Which treatment segment dominates the nasopharyngeal cancer market?

Radiotherapy remains the dominant treatment segment due to its established efficacy in localized disease management. However, immunotherapy and targeted therapies are gaining market share due to improved clinical outcomes in recurrent and metastatic cases. - What are the regional trends in the nasopharyngeal cancer market?

Asia-Pacific holds a significant market share due to high disease prevalence, particularly in China and Southeast Asia. North America and Europe are witnessing growth supported by advanced healthcare infrastructure and strong oncology research pipelines.

Conclusion

Nasopharyngeal cancer represents a distinct malignancy characterized by viral association, geographic concentration, and complex treatment requirements. Market growth is being supported by expanding immunotherapy adoption, improved EBV DNA–based screening, and advancements in precision imaging technologies.

North America continues to lead in revenue share, while Asia-Pacific remains epidemiologically significant. Chemotherapy and radiotherapy retain strong clinical relevance, although biologics are reshaping treatment paradigms.

Increasing research investments, supportive healthcare policies, and early detection initiatives are expected to enhance survival outcomes. Overall, steady market expansion is anticipated, driven by innovation, improved diagnostics, and evolving personalized therapeutic strategies globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)