Table of Contents

Overview

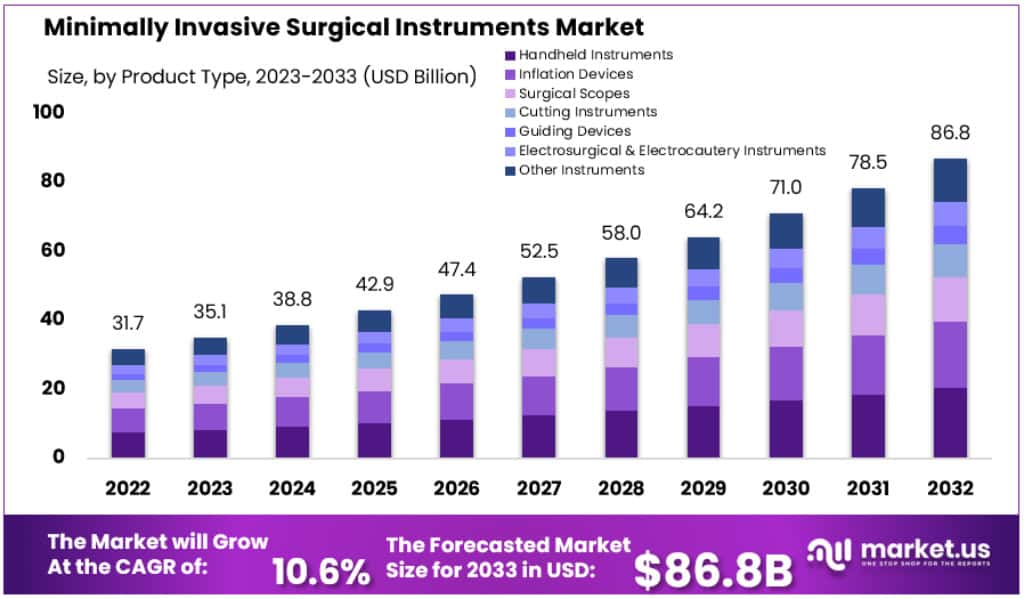

New York, NY – Jan 13, 2026 – The Global Minimally Invasive Surgical Instruments Market size is expected to be worth around USD 86.8 Billion by 2032, from USD 35.1 Billion in 2023, growing at a CAGR of 10.6% during the forecast period from 2024 to 2033.

The global healthcare sector is witnessing steady advancement in minimally invasive surgical instruments, driven by the growing demand for safer, faster, and more efficient surgical procedures. These instruments are designed to support minimally invasive surgeries (MIS), which use small incisions, advanced visualization, and precise tools to reduce tissue damage compared to conventional open surgeries.

Minimally invasive surgical instruments include endoscopic devices, laparoscopic tools, energy-based instruments, and robotic-assisted systems. Their basic formation typically consists of elongated, slim-profile designs, ergonomic handles, high-grade stainless steel or medical polymers, and compatibility with imaging systems. These features enable surgeons to perform complex procedures with enhanced accuracy and control.

The adoption of these instruments has been supported by clear clinical benefits. Reduced postoperative pain, shorter hospital stays, lower risk of infection, and faster patient recovery have been consistently observed. As a result, minimally invasive techniques are increasingly preferred across multiple specialties, including general surgery, orthopedics, gynecology, urology, and cardiovascular procedures.

Technological innovation remains a key growth driver. Continuous improvements in instrument durability, flexibility, and integration with digital and robotic platforms are strengthening surgical outcomes. In addition, rising healthcare expenditure, expanding surgical volumes, and growing awareness among patients and providers are contributing to market expansion.

Looking ahead, the market for minimally invasive surgical instruments is expected to experience sustained growth. Ongoing research and development, combined with the global shift toward value-based healthcare and patient-centric treatment models, are anticipated to further support adoption. These trends position minimally invasive surgical instruments as a critical component of modern surgical practice and future healthcare delivery.

Key Takeaways

- Market Value (2023): The market was valued at USD 35.1 billion in 2023.

- Projected Market Size (2033): The market is forecast to reach approximately USD 86.8 billion by 2033.

- Compound Annual Growth Rate (2023–2033): Growth is expected to be recorded at a CAGR of 10.6% over the forecast period.

- Handheld Instruments Segment: Handheld instruments account for a substantial market share of 23.6%.

- Orthopedic Applications: The orthopedic segment represents more than 24.2% of the overall market.

- Hospital End Users: Hospitals remain the dominant end-user group, contributing over 71.8% of total market revenue.

- North America Market Position: North America leads the global market with a 32.49% share, equivalent to a valuation of USD 10.3 billion.

- Asia Pacific Outlook: The Asia Pacific region is expected to register the fastest growth during the forecast period.

- US Healthcare Expenditure: The United States reports the highest per capita healthcare spending, as highlighted by OECD data.

- Ambulatory Surgical Centers: Adoption of minimally invasive surgical instruments is increasing significantly across ambulatory surgical centers.

- Recent Industry Development: In August 2023, VISEON Inc. introduced an AI-enabled surgical navigation system.

- Key Market Participants: Major companies operating in the market include Medtronic, Siemens Healthineers AG, Johnson & Johnson Services, and Abbott.

- Regulatory Challenges: Market growth is constrained by stringent regulatory frameworks and the requirement for extensive clinical validation.

- Technological Progress: Ongoing advancements in surgical technologies are creating notable growth opportunities.

- Chronic Disease Prevalence: The rising incidence of chronic diseases is accelerating demand for minimally invasive surgical procedures.

Regional Analysis

In 2023, North America maintained a leading position in the minimally invasive surgical instruments market, capturing a 32.49% share and reaching a market value of USD 10.3 billion. This strong market presence is supported by well-established healthcare infrastructure, early adoption of advanced surgical technologies, and a high burden of chronic diseases across the region.

According to the Organization for Economic Cooperation and Development (OECD), the United States records the highest per capita healthcare expenditure globally. In addition, patients in the U.S. benefit from greater flexibility in selecting treatment options and healthcare providers, which is expected to further support the adoption of minimally invasive surgical procedures.

Conversely, the Asia Pacific region is projected to witness the fastest growth rate during the 2023–2032 forecast period, driven by expanding healthcare access, rising medical tourism, and increasing investment in modern surgical technologies.

Emerging Trends

- Technological Advancements: The Minimally Invasive Surgical Instrument Market is experiencing sustained growth, largely driven by continuous technological advancements across surgical disciplines, including cardiac, orthopedic, and neurological procedures. Improvements in device design, ergonomics, and functionality have enhanced surgical precision and operational safety. As a result, improved clinical outcomes and reduced procedural risks are being achieved, supporting wider adoption of minimally invasive techniques.

- Rising Adoption of Surgical Robotics: The adoption of surgical robotic systems is increasing steadily within minimally invasive procedures. These systems provide enhanced accuracy, superior dexterity, and improved surgeon control, enabling the execution of complex procedures through smaller incisions. The growing clinical success of robotic-assisted surgeries is expected to accelerate their integration, supported by their ability to improve surgical efficiency, consistency, and patient safety.

- Expansion of Application Areas: Initially concentrated in procedures such as gallbladder removal and gynecological surgeries, minimally invasive surgical instruments are now being increasingly utilized in gastroenterology, cosmetic surgery, and other specialized fields. This expansion is primarily driven by rising patient and clinician preference for procedures that minimize recovery time, reduce post-operative complications, and shorten hospital stays.

- Increasing Penetration in Developing Regions: Developing regions, particularly Asia-Pacific, are witnessing rapid growth in the adoption of minimally invasive surgical instruments. This trend is supported by rising healthcare expenditures, expanding hospital infrastructure, increased medical tourism, and growing awareness of the clinical and economic benefits associated with minimally invasive procedures.

Use Cases

- Orthopedic Surgeries: Minimally invasive techniques are widely applied in orthopedic procedures such as hip and knee replacements. These approaches involve smaller incisions, resulting in reduced tissue trauma, lower post-operative pain, and faster rehabilitation when compared to conventional open surgeries.

- Cardiac Procedures: In cardiac care, minimally invasive surgical instruments are playing an increasingly critical role, particularly in valve repair and replacement procedures. Technologies such as transcatheter-based systems enable interventions without open-heart surgery, significantly lowering procedural risks and improving patient recovery outcomes.

- Gastrointestinal Surgeries: The growing prevalence of gastrointestinal disorders, including obesity and gastric cancer, has increased the adoption of minimally invasive approaches in this segment. These procedures contribute to shorter hospital stays, reduced complication rates, and improved post-operative recovery.

- Cosmetic and Bariatric Surgeries: Minimally invasive instruments are being increasingly utilized in cosmetic and bariatric surgeries to achieve minimal scarring and faster recovery. High precision and reduced tissue disruption are key advantages, supporting both aesthetic outcomes and clinical effectiveness.

Frequently Asked Questions on Minimally Invasive Surgical Instruments

- What are minimally invasive surgical instruments?

Minimally invasive surgical instruments are specialized tools designed to perform procedures through small incisions, enabling surgeons to reduce tissue damage, limit blood loss, shorten hospital stays, and improve overall patient recovery outcomes. - What types of minimally invasive surgical instruments are commonly used?

Common categories include laparoscopic instruments, endoscopic devices, electrosurgical tools, handheld cutting instruments, and robotic-assisted accessories, each engineered to enhance precision, visualization, and control during complex surgical interventions across multiple clinical specialties. - In which medical procedures are these instruments most widely applied?

These instruments are widely used in general surgery, gynecology, urology, orthopedics, and cardiovascular procedures, as they support faster healing, lower infection risks, and improved cosmetic results compared with traditional open surgical approaches. - What are the main challenges associated with minimally invasive surgical instruments?

High initial costs, the need for skilled surgeons, limited tactile feedback, and strict regulatory requirements are key challenges, although continuous technological innovation and training programs are gradually improving adoption rates and clinical effectiveness worldwide. - What does the minimally invasive surgical instruments market represent?

The minimally invasive surgical instruments market represents the global demand for devices supporting less invasive procedures, driven by rising surgical volumes, aging populations, and growing preference for treatments that reduce recovery time and healthcare costs. - What factors are driving the growth of this market?

Market growth is primarily attributed to technological advancements, increasing adoption of robotic-assisted surgery, expanding hospital infrastructure in emerging economies, and higher awareness among patients and clinicians regarding the benefits of minimally invasive techniques. - Which regions dominate and lead growth in the market?

North America dominates the market due to advanced healthcare systems and high procedure volumes, while Asia-Pacific is expected to witness the fastest growth, supported by medical tourism, improving reimbursement, and rising investments in surgical technologies.

Conclusion

The global minimally invasive surgical instruments market is positioned for sustained and robust growth, supported by strong clinical advantages, continuous technological innovation, and expanding adoption across multiple medical specialties. The preference for procedures that reduce recovery time, postoperative complications, and overall healthcare costs has accelerated demand worldwide.

Market expansion is further reinforced by rising healthcare expenditure, increasing surgical volumes, and the integration of digital and robotic technologies. While regulatory challenges and high initial costs remain, ongoing research, training, and infrastructure development are expected to mitigate these barriers, strengthening the role of minimally invasive surgical instruments in modern and future healthcare delivery.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)