Table of Contents

Overview

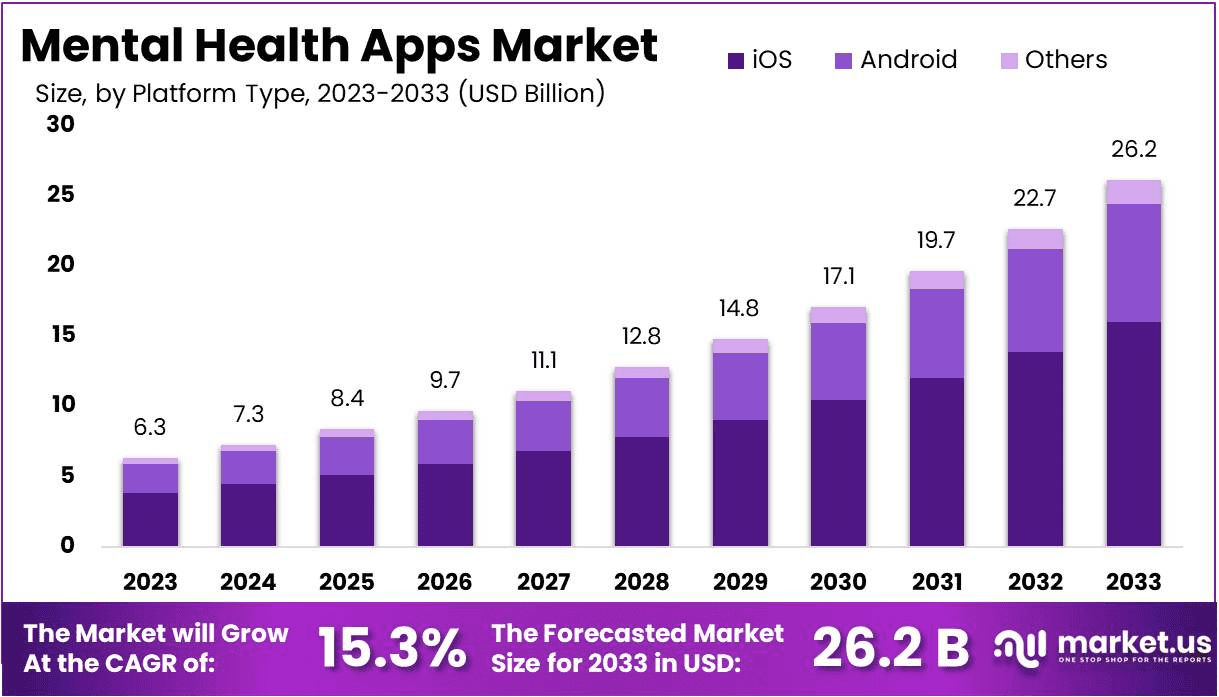

The Global Mental Health Apps Market is projected to reach US$ 26.2 billion by 2033, rising from US$ 6.3 billion in 2023, at a CAGR of 15.3%. This growth is strongly driven by the rising prevalence of mental health disorders. According to the WHO, one in eight people globally suffer from conditions such as anxiety, depression, or stress. The high burden of disease has accelerated demand for accessible and affordable solutions, and mobile applications have become a scalable and reliable response to this challenge.

Growing awareness and reduced stigma are also reshaping the market landscape. Public campaigns, workplace wellness programs, and government-led initiatives are reducing barriers to seeking help. This cultural shift is making individuals more comfortable with non-traditional treatment methods, particularly digital applications. Apps provide privacy, flexibility, and anonymity, which are increasingly valued by users hesitant to seek in-person support.

Smartphone penetration and internet availability are critical enablers of market expansion. Affordable mobile data and widespread connectivity have extended access even in emerging markets. Millions of users in low-income regions now have the opportunity to adopt mental health applications. This accessibility not only expands user bases but also drives long-term adoption as smartphones continue to integrate into daily life.

Another significant factor is the cost-effectiveness of digital tools. Compared with traditional therapy, mental health apps provide affordable alternatives offering meditation, CBT exercises, mood tracking, and online consultations. These on-demand solutions are particularly appealing to younger generations and cost-sensitive populations. The democratization of mental health support is positioning apps as essential tools in preventive care and self-management strategies.

Technology, Policy, and Industry Momentum

The integration of advanced technologies is further accelerating adoption. AI, machine learning, and natural language processing are transforming app capabilities. Chatbots, personalized therapy recommendations, and predictive mood pattern analysis are enhancing user engagement and improving therapeutic outcomes. Such innovations are enabling continuous support and aligning digital care with professional standards.

The COVID-19 pandemic created a structural shift in digital health adoption. Lockdowns, isolation, and heightened stress increased reliance on remote solutions. Mental health apps gained long-term acceptance as viable alternatives to traditional healthcare. Behavioral changes during the pandemic accelerated adoption curves, creating a strong foundation for sustained growth across multiple demographics.

Corporate and institutional adoption is expanding market reach. Organizations are increasingly providing mental health apps in employee wellness programs, while universities and schools integrate them for student support. This institutional endorsement enhances credibility, broadens usage, and creates new revenue opportunities for developers. Such partnerships are expected to remain a stable driver of growth.

Investment flows and regulatory support are shaping a favorable ecosystem. Venture capital funding is directed toward mental health startups, while mergers and acquisitions are fostering innovation and global expansion. At the same time, governments in the U.S., Europe, and Asia-Pacific are establishing supportive digital health frameworks. Validations by regulatory bodies are building user trust and enabling healthcare providers to integrate apps into treatment plans. Together with rising demand for preventive healthcare, these factors position mental health applications as an indispensable component of modern healthcare systems.

Key Takeaways

- In 2023, the Mental Health Apps market generated revenue of US$ 6.3 billion and is projected to reach US$ 26.2 billion by 2033.

- The sector is growing at a CAGR of 15.3%, reflecting rising consumer adoption of digital solutions for mental health and wellness management globally.

- Based on platform type, iOS dominated the market with a 61.2% share in 2023, surpassing Android and other operating systems significantly.

- Within applications, depression and anxiety management apps commanded the largest share of 42.3%, highlighting their critical role in addressing global mental health concerns.

- Stress management, meditation management, and other categories also contributed notably, though their collective shares remained lower compared with depression and anxiety management.

- In terms of end-users, home care settings emerged as the leading segment, securing 54.3% of revenue due to increasing demand for self-managed digital care.

- Mental hospitals and other institutional settings accounted for smaller proportions, emphasizing the shift toward personalized and at-home mental health support tools.

- Regionally, North America led the global market with a 38.7% share, supported by strong adoption, higher awareness, and significant healthcare technology investments.

Regional Analysis

North America accounted for the largest revenue share of 38.7% in the mental health apps market. The growth is driven by rising awareness of mental health issues and declining stigma, encouraging adoption of digital solutions. Investments from public and private sectors have enhanced app accessibility and innovation. Integration of mental health support into healthcare systems and workplaces has expanded the user base. Additionally, the long-term impact of COVID-19 accelerated demand for remote solutions as individuals increasingly sought virtual platforms for emotional and psychological support.

The need for accessible solutions is highlighted by rising mental health concerns in the United States. The National Center for Biotechnology Information reported in November 2022 that 9.2% of Americans experienced severe depressive episodes in 2020. Young adults were most affected, creating strong demand for apps offering personalized care. High smartphone penetration and advanced technological infrastructure further strengthened adoption. These factors positioned digital mental health tools as critical resources in the North American healthcare landscape, supporting robust market growth across various demographic groups.

Key drivers of North American market expansion include the growing prevalence of smartphone usage, advanced network coverage, and rising social media penetration. According to GSMA’s The Mobile Economy Report 2023, smartphone adoption in the region was 84% in 2022 and is forecast to reach 90% by 2030. This expanding user base ensures widespread availability of mental health applications. Strong consumer readiness to adopt technology-driven healthcare solutions continues to support the steady revenue growth of digital mental health services across the United States and Canada.

Asia Pacific is projected to record the highest CAGR during the forecast period. Growth is supported by increasing awareness of mental health, rising smartphone use, and expanding digital health initiatives in key markets. Governments and non-governmental organizations are investing in mental health programs, encouraging adoption of digital interventions. Culturally relevant content and localized features in apps are expected to improve user engagement. Rising mental health prevalence, particularly in China and India, alongside economic growth and higher consumer spending, positions Asia Pacific as a significant growth driver globally.

Segmentation Analysis

In 2023, the iOS platform held the leading position with a 61.2% market share, supported by Apple’s extensive user base and strong security framework. Developers are increasingly adopting iOS due to its reliable ecosystem and user-friendly interface. Frequent and consistent updates improve app performance and security, strengthening user trust. Moreover, Apple’s rigorous app review process ensures quality standards, which attracts users who prioritize reliability. As global demand for iOS devices grows, the platform is expected to see further expansion in mental health app development.

The depression and anxiety management segment accounted for 42.3% of the market share in 2023. This dominance is linked to the growing prevalence of mental health conditions and higher awareness of emotional well-being. Innovative features, including real-time mood monitoring and personalized therapy, are driving adoption. As social stigma around mental health reduces, individuals are engaging more with such applications. These tools provide accessible and tailored support, creating opportunities for stronger market penetration and long-term growth in this critical application segment.

Home care settings captured 54.3% of the revenue share, highlighting their importance in mental health management. The preference for convenient and remote solutions has grown, particularly among elderly and chronically ill patients. The rising acceptance of telehealth and the affordability of home-based care solutions have accelerated this trend. Continuous monitoring through mobile apps provides patients with ongoing support outside traditional facilities. This shift is expected to persist, as home care demonstrates both practicality and cost-effectiveness, making it a vital growth driver for mental health app adoption.

The overall market outlook suggests continued expansion across all segments. iOS will remain dominant due to its quality ecosystem and high consumer trust. Depression and anxiety applications are anticipated to lead application adoption, supported by growing societal acceptance and the demand for personalized tools. Home care settings will keep fueling growth as users seek accessible care outside hospitals. Collectively, these factors reflect a strong trajectory for mental health apps, with increasing integration into both healthcare systems and everyday personal wellness practices.

Key Players Analysis

The mental health apps market is witnessing strong participation from leading players who are actively investing in product innovation. These companies are introducing advanced features and user-friendly platforms that focus on improving mental wellness and accessibility. Strategic moves such as collaborations, acquisitions, and expansions are shaping the competitive environment. The continuous adoption of digital tools for mental health support is reinforcing market growth. As competition intensifies, differentiation through technology and enhanced user experience is becoming a critical factor for sustaining market leadership.

In January 2022, Mayo Clinic partnered with K Health to leverage artificial intelligence in advancing hypertension treatment. This strategic collaboration highlights the increasing role of AI in healthcare innovation. While the partnership is focused on physical health, its broader implications extend to mental health solutions. The integration of AI-based insights into digital health tools demonstrates how leading players are investing in next-generation technologies. Such initiatives not only strengthen competitiveness but also accelerate adoption rates among healthcare providers and end-users.

The integration of artificial intelligence into mental health apps is reshaping the market landscape. AI-driven solutions are being designed to deliver personalized care, predictive analytics, and timely interventions. These advancements are improving the precision and effectiveness of mental health applications in addressing issues such as stress, anxiety, and depression. As leading players adopt AI, the scope of digital therapy solutions is expanding. This trend is expected to fuel further innovation, enhance user trust, and drive sustainable growth in the mental health apps industry.

FAQ

1. What are mental health apps?

Mental health apps are digital tools designed to improve emotional well-being and support users with conditions such as anxiety, stress, and depression. These apps provide features like guided meditation, therapy modules, mood tracking, and access to professionals. They can be used anywhere and anytime, making mental health support more accessible. With the growth of smartphones, these apps are gaining popularity worldwide. Their main purpose is to offer affordable, easy-to-use, and supportive solutions for individuals seeking better mental health.

2. How do mental health apps work?

Mental health apps work by offering evidence-based techniques such as cognitive behavioral therapy (CBT), meditation, or mindfulness exercises. They help users track moods, manage stress, and build healthy habits through daily reminders and interactive activities. Some apps use AI-driven chatbots to provide emotional support, while others connect users to licensed therapists for online consultations. The apps are designed to create consistency in mental health management, encouraging small, manageable steps toward improvement. They are useful tools for regular practice and progress tracking.

3. Are mental health apps effective?

Studies show that mental health apps can be effective in reducing symptoms of stress, anxiety, and depression, especially in mild to moderate cases. Their effectiveness is stronger when the app is based on clinical research and offers structured exercises. Consistent use is essential for lasting results, as users often see improvements with daily practice. However, results vary between individuals. These apps work best when combined with other mental health strategies and should be considered supportive rather than a complete replacement for therapy.

4. Are mental health apps safe to use?

Most mental health apps are safe to use, especially those developed by reliable organizations that follow privacy regulations such as HIPAA or GDPR. They are designed to protect user information, although concerns remain regarding data sharing and the accuracy of self-assessment tools. Users should carefully review app policies before using them. Choosing well-known apps with transparent privacy practices is recommended. While these apps are generally helpful, they should be used responsibly, and sensitive data should always be handled with caution.

5. Do mental health apps replace traditional therapy?

Mental health apps do not replace traditional therapy but rather complement it. They offer convenient access to tools and exercises that can support well-being between therapy sessions. For individuals with mild concerns, apps can provide valuable guidance and coping techniques. However, for serious conditions such as major depression or trauma, licensed therapists and medical professionals remain essential. Apps serve as an additional resource for managing mental health but should not be considered a full substitute for professional, in-person care.

6. What features are commonly offered by mental health apps?

Mental health apps often include mood tracking, guided meditation, stress relief exercises, and self-care reminders. Many provide tools based on cognitive behavioral therapy, as well as AI chatbots for instant support. Some apps allow access to licensed therapists through video or chat sessions. Community forums are also common, offering peer interaction and emotional support. Other features include sleep improvement tools, breathing exercises, and habit tracking. These features aim to make mental health management more practical and personalized for daily use.

7. How large is the mental health apps market?

The mental health apps market has experienced rapid growth in recent years. Mental Health Apps Market Size is expected to be worth around US$ 26.2 billion by 2033 from US$ 6.3 billion in 2023, growing at a CAGR of 15.3% during the forecast period 2024 to 2033. The market expansion is supported by the increasing demand for affordable digital health tools. Smartphone penetration and rising awareness of mental health have further boosted adoption. This strong growth outlook reflects the role of technology in making therapy and mental health support widely accessible.

8. What factors are driving market growth?

The growth of the mental health apps market is driven by several factors. Rising cases of stress, anxiety, and depression have created greater demand for accessible support tools. The widespread use of smartphones and wearable devices makes these apps more available to people worldwide. The COVID-19 pandemic accelerated digital health adoption, boosting telehealth and app usage. Increasing awareness about mental well-being, combined with the need for affordable therapy options, is also contributing to market expansion. Together, these factors support steady and sustained growth.

9. Which regions are leading the market?

North America is currently leading the mental health apps market, supported by high healthcare spending, advanced technology, and early adoption of digital solutions. Europe follows closely, as government programs and strong regulatory frameworks encourage mental health innovation. The Asia-Pacific region is experiencing the fastest growth, thanks to rising mental health awareness, large populations, and increased smartphone usage. Countries such as India, China, and Japan are driving significant expansion in the region. These combined regional developments ensure a balanced global market landscape.

10. Who are the major players in the mental health apps market?

The market includes both specialized app providers and larger technology companies. Leading players include Mindscape, Calm, MoodMission Pty Ltd., Sanvello Health, Headspace Inc., Youper, Inc., Happify, Bearable, BetterHelp, Talkspace, and Diago all of which are recognized for delivering trusted mental health solutions. In addition, major technology firms such as Apple and Google are integrating wellness features into their devices and services. These companies invest heavily in innovation and partnerships, making mental health support more advanced and accessible. Together, these players shape competition and expand opportunities across the global market.

11. What challenges does the market face?

The mental health apps market faces challenges despite rapid growth. Data privacy remains one of the top concerns, as users share sensitive health information. Many apps also lack clinical validation, raising questions about effectiveness. Retention and engagement are additional issues, as users often stop using apps after a short period. Regulatory barriers in some regions also slow telehealth integration. Addressing these challenges requires better security measures, transparent clinical backing, and improved user engagement strategies to maintain long-term growth and trust.

12. What trends are shaping the future of the market?

Several key trends are shaping the future of the mental health apps market. Artificial intelligence and chatbots are being integrated to create personalized therapy experiences. Wearable devices are also contributing by monitoring stress levels and moods in real time. Developers are focusing on culturally adapted content to meet global needs. Partnerships between app providers and healthcare organizations are growing, which helps improve credibility. Subscription-based business models and workplace wellness programs are gaining traction, making mental health support more mainstream and accessible.

Conclusion

The global mental health apps market is set for strong growth, driven by rising awareness, digital adoption, and demand for affordable care. These apps are emerging as vital tools for managing conditions like anxiety, stress, and depression while offering privacy and convenience. Advancements in artificial intelligence, smartphone penetration, and institutional support are further shaping their role in preventive and personalized healthcare. Although challenges such as data privacy and clinical validation remain, ongoing innovation and supportive policies are expected to strengthen user trust. With expanding adoption across regions and demographics, mental health apps are positioned to become an essential part of modern healthcare and wellness management.

View More

AI In Mental Health Market || Chatbots for Mental Health and Therapy Market || Environmental Health and Safety Software Market || Mental Health Services Market || mHealth Market || mHealth Services Market || mHealth Apps Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)