Table of Contents

Overview

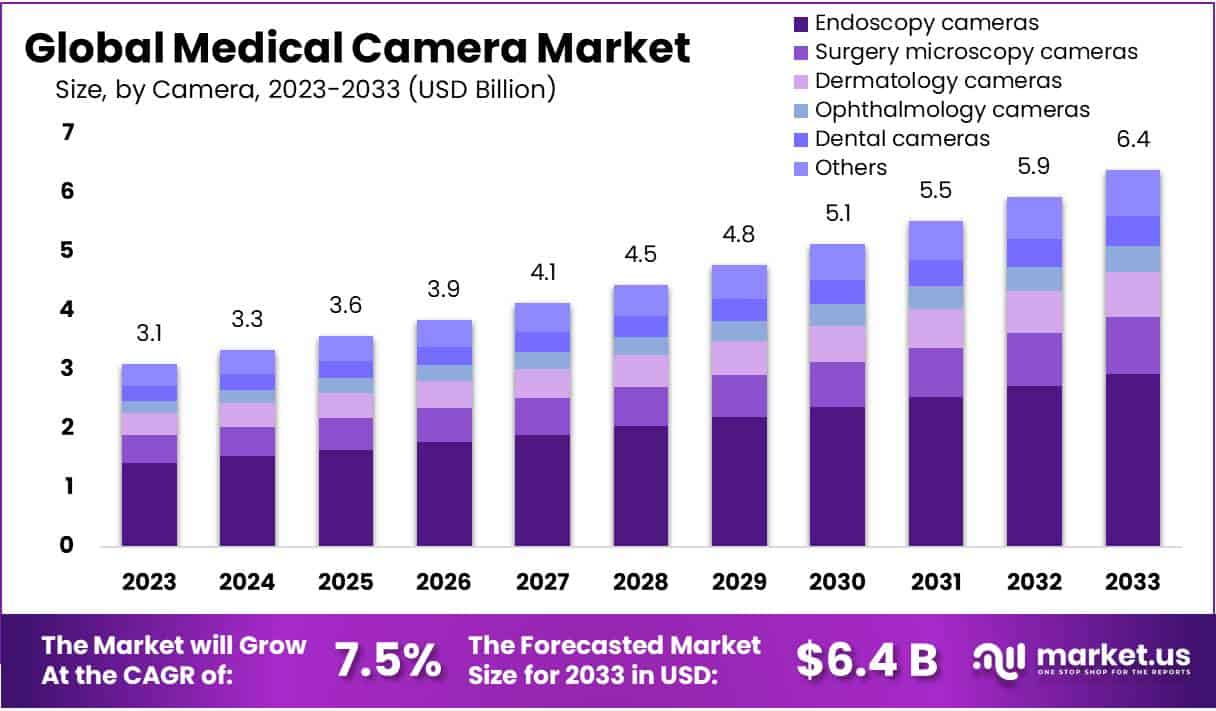

The Global Medical Camera Market is projected to reach USD 6.4 billion by 2033, up from USD 3.1 billion in 2023, registering a CAGR of 7.5% during 2024–2033. Market growth is driven by ageing populations, rising disease burden, and increased surgical activity. The UN projects that by 2050, one in six people will be over 65 years, creating sustained demand for diagnostic and surgical visualization equipment. Age-related conditions such as cardiovascular disease and cancer are fueling the adoption of endoscopic, ophthalmic, and surgical video systems across healthcare facilities.

Rising prevalence of noncommunicable diseases (NCDs) significantly supports market expansion. Cancer and cardiovascular diseases accounted for around three-quarters of non-pandemic deaths in 2021. In 2022, an estimated 20 million new cancer cases and 9.7 million deaths were recorded globally. These trends underscore the growing reliance on endoscopic imaging for screening and treatment. National screening programs across OECD countries are expanding, driving the adoption of flexible endoscopes, capsule endoscopy devices, and high-definition (HD) or 4K camera systems for early detection.

Surgical procedure volumes further strengthen market demand. The Lancet Commission estimates about 313 million surgeries are performed annually. According to the World Health Organization, surgery contributes to nearly 13% of global disease burden. As countries invest in surgical capacity and reporting, procurement of visualization equipment rises correspondingly. Between 2016 and 2023, the number of countries reporting surgical volumes grew by more than 70%, signaling infrastructure development and modernization of imaging systems in hospitals and clinics.

Healthcare spending remains elevated post-pandemic, supporting capital investments in imaging technology. Data from WHO and the World Bank show that per-capita health expenditure rose by approximately 25% from 2019 to 2021. This increase enables hospitals to replace outdated camera systems and manage surgical backlogs efficiently. Regulatory and infection-control initiatives also drive technology upgrades. Guidelines from the U.S. FDA and public health authorities promote the use of single-use scopes and advanced reprocessing designs, enhancing safety and sustaining demand for next-generation camera platforms.

Digital health transformation further accelerates market growth. The WHO’s Global Strategy on Digital Health promotes connectivity and data integration in care delivery. Applications such as surgical video capture, tele-mentoring, and AI-based imaging analytics require high-resolution, digitally compatible camera systems. Continuous product innovation is evident through recent FDA 510(k) clearances for upgraded video systems, reflecting ongoing advancements in resolution and performance. Overall, demographic shifts, rising disease burden, healthcare digitization, and regulatory advancements collectively ensure sustained growth in the global medical camera market through 2033.

Key Takeaways

- The medical camera market is projected to expand from USD 3.1 billion in 2023 to USD 6.4 billion by 2033, registering a 7.5% CAGR.

- Endoscopy dominates the camera segment, securing over 46% market share due to its critical role in surgical accuracy and diagnostic precision.

- High-definition (HD) cameras lead the resolution segment, accounting for more than 62% market share, enhancing clarity and diagnostic reliability.

- Technological advancements such as AI integration and HD imaging are driving market growth by improving diagnostic and surgical performance.

- The high cost of advanced medical cameras remains a significant barrier, restricting adoption across low- and middle-income healthcare systems.

- Rising demand for minimally invasive surgeries is propelling market expansion, attributed to shorter recovery times and enhanced procedural safety.

- Artificial intelligence integration in medical cameras is transforming diagnostics through improved accuracy, automation, and operational efficiency.

- North America maintains market dominance, supported by advanced healthcare infrastructure and strong adoption of cutting-edge imaging technologies.

- CMOS sensors account for over 77% of the market, favored for their superior imaging performance, power efficiency, and cost-effectiveness.

- Hospitals represent the largest end-user segment, holding more than 38% market share, reflecting extensive use of medical cameras in multiple applications.

Regional Analysis

In 2023, North America dominated the medical camera market, securing over a 32.5% share valued at USD 1 billion. This dominance was driven by advanced healthcare infrastructure, high healthcare expenditure, and the presence of leading medical device manufacturers. The United States led the region, supported by strong R&D investments and the growing adoption of innovative medical technologies. A consistent focus on improving patient care quality and technological innovation further strengthened North America’s position in the global market, making it a key hub for medical camera development.

Europe ranked second in the global medical camera market, supported by its advanced healthcare systems and strict regulatory standards. These regulations ensure the production and use of high-quality medical devices. The region has seen increasing demand for minimally invasive surgeries that rely heavily on medical cameras. Key markets such as Germany, France, and the UK continue to drive technological progress and innovation. Their healthcare sectors emphasize patient safety, efficiency, and the use of modern medical imaging solutions.

The Asia-Pacific region is projected to experience rapid growth in the coming years. This expansion is supported by improving healthcare infrastructure, rising awareness about medical advancements, and growing investments in healthcare facilities. Countries like China, Japan, and India are major contributors to this growth. Their increasing healthcare spending and large patient populations are fueling market demand. Furthermore, supportive government initiatives aimed at modernizing healthcare systems and adopting advanced medical technologies are strengthening the region’s overall market potential.

Latin America, the Middle East, and Africa are witnessing steady but slower growth in the medical camera market. The expansion is influenced by developing healthcare sectors, increasing public and private healthcare investments, and rising awareness of modern medical procedures. Although these regions currently hold smaller market shares, their growth potential remains strong. Continuous efforts to upgrade healthcare infrastructure and promote advanced medical technologies are expected to accelerate adoption rates, positioning these regions as emerging contributors to global market expansion.

Segmentation Analysis

In 2023, endoscopy cameras led the global medical camera market with over 46% share. Their dominance was due to their critical use in diagnostics and surgeries, offering high-resolution imaging for accurate assessments. Surgery microscopy cameras followed, valued for precision in microsurgeries and advanced procedures. Dermatology cameras also held a notable position, driven by rising awareness of skin health and early detection needs. Ophthalmology and dental cameras further contributed, supporting disease management and improved diagnostic accuracy across various healthcare applications.

The HD camera segment secured over 62% market share in 2023 within the resolution category. Its strong position was attributed to the rising demand for high-definition imaging in diagnostics and surgeries. HD cameras deliver detailed visuals crucial for endoscopy, ophthalmology, and other precise medical applications. Although 4K cameras offer superior resolution, adoption remains slower due to high costs and infrastructure needs. Continued healthcare investments, coupled with AI integration in imaging systems, are expected to maintain HD cameras’ market dominance over the coming years.

In the same year, CMOS sensors dominated the medical camera market with over 77% share. Their advantages include cost-efficiency, fast imaging, and low power consumption. These features make CMOS sensors ideal for real-time imaging in compact and portable devices. Technological improvements have enhanced their sensitivity and performance. Despite CCD sensors offering superior low-light performance, their higher cost limits adoption. Continuous innovations, including 4K and AI-enabled imaging, are expected to strengthen CMOS sensors’ dominance and expand their applications in medical diagnostics and surgical imaging.

Hospitals accounted for over 38% of the medical camera market in 2023. Their leadership was driven by increased use of advanced imaging systems for diagnostics and surgical procedures. Hospitals prefer CMOS cameras for endoscopic imaging due to efficiency and speed, while CCD cameras are used where superior image clarity is required. Advancements in HD video and digital interfaces have further supported growth. The rising trend of minimally invasive surgeries and improved healthcare infrastructure continues to boost the adoption of advanced medical camera technologies globally.

Key Market Segments

By Camera

- Endoscopy cameras

- Surgery microscopy cameras

- Dermatology cameras

- Ophthalmology cameras

- Dental cameras

- Others

By Resolution

- HD cameras

- SD cameras

By Sensor

- Complementary Metal-oxide-semiconductor (CMOS)

- Charge Coupled Device (CCD)

By End-use

- Hospitals & clinics

- Ambulatory Surgery Centers

- Others

Key Players Analysis

The medical camera market is shaped by rapid innovation and growing demand for advanced imaging solutions. The focus on precision and clarity has driven manufacturers to enhance diagnostic capabilities across healthcare facilities. Companies are continuously investing in research and development to deliver high-performance imaging systems that support surgical accuracy and improved patient care. This competitive environment fosters technological advancements that are transforming medical diagnostics, visualization, and surgical workflows across hospitals and clinics globally.

Sony Corporation plays a major role in defining imaging excellence within the market. The company’s advanced medical cameras are renowned for their superior resolution and color accuracy. Continuous investment in R&D enables Sony to integrate innovative features that enhance diagnostic precision. Similarly, Olympus Corporation dominates the endoscopic imaging segment. Its advanced camera systems are designed for minimally invasive procedures, ensuring efficiency and reliability in complex examinations. Both companies contribute significantly to improving visualization standards in medical imaging and surgical applications.

Carl Zeiss AG and Stryker Corporation strengthen the market through their specialized offerings. Zeiss provides precision optics that improve image quality and diagnostic accuracy. Its optical systems are widely adopted in surgical and laboratory settings. Stryker, on the other hand, focuses on developing high-definition surgical cameras that enhance visualization during operations. These technologies play an essential role in supporting surgeons with real-time, detailed imagery, ensuring safer and more effective medical interventions. Their innovation drives the continuous evolution of imaging solutions in healthcare.

Other prominent players include Hamamatsu Photonics K.K., Leica Microsystems (a subsidiary of Danaher), Canon Inc., Richard Wolf GmbH, Smith & Nephew plc, and Panasonic Corporation. These companies collectively shape the competitive landscape through diverse product portfolios and continuous innovation. Their technologies address a wide range of clinical needs, from surgical precision to diagnostic imaging. The combined expertise of these firms ensures steady market growth and continuous improvements in imaging standards, ultimately supporting enhanced healthcare outcomes worldwide.

Market Key Players

- Sony Corporation

- Olympus Corporation

- Carl Zeiss AG

- Stryker Corporation

- Hamamatsu Photonics K.K.

- Leica Microsystems (a subsidiary of Danaher)

- Canon Inc.

- Richard Wolf GmbH

- Smith & Nephew plc

- Panasonic Corporation

Challenges

Regulatory Complexity

The medical camera industry faces rising regulatory challenges. Global standards for safety, performance, and patient data handling are becoming more stringent. Manufacturers must meet these evolving requirements to gain market approval. This includes compliance with regional rules such as FDA, CE, and ISO certifications. Meeting these standards demands extensive documentation, product testing, and audits. The process increases development time and costs. Companies must also monitor ongoing regulatory changes to avoid penalties or recalls. Managing compliance across multiple regions adds further complexity, especially for firms aiming for international market expansion.

Cybersecurity Risk

Medical imaging devices are now more connected than ever. This connectivity raises major cybersecurity risks. Hospitals expect devices to protect patient data from cyber threats and unauthorized access. Manufacturers must integrate strong encryption, software updates, and network protection systems. However, ensuring device security adds cost and design complexity. Regular security patches and compliance with global cybersecurity frameworks are also required. Any weakness can expose hospitals to data breaches, affecting patient trust and safety. The challenge lies in balancing innovation, connectivity, and stringent cybersecurity standards without compromising performance or usability.

Integration Issues

Integrating medical cameras into existing hospital systems remains a significant challenge. These cameras must fit seamlessly within the operating-room infrastructure. Factors such as size, mounting, sterilization, and heat management influence the design. Compatibility with other surgical devices and imaging platforms is also critical. Any mismatch can lead to workflow disruptions and safety risks. Engineers must ensure that the devices function smoothly within constrained spaces while maintaining optical quality and durability. Achieving this balance requires precise design coordination, advanced materials, and thorough testing to meet clinical and operational demands effectively.

Infection Control Concerns

Infection control has become a key focus in hospital environments. Medical cameras must be designed for easy sterilization or single-use application. Regulatory bodies are tightening standards to minimize contamination risks during surgeries. As a result, manufacturers must select materials that withstand cleaning chemicals and high temperatures. The shift toward disposable components also affects cost, design, and procurement strategies. Balancing durability with sterility poses an ongoing challenge. Companies must continuously innovate to meet hygiene requirements without compromising image quality or increasing overall device costs.

Clinical Validation Demand

Hospitals now seek more than just superior image quality. They require clinical validation showing improved patient outcomes and diagnostic accuracy. Manufacturers must conduct extensive clinical trials and real-world studies to prove the value of their products. This involves collaboration with healthcare providers, long-term monitoring, and data analysis. The process is costly and time-consuming but essential for market acceptance. Without clear evidence of outcome improvement, even technologically advanced cameras may face limited adoption. Demonstrating measurable clinical benefits has therefore become a major success factor in the medical camera market.

Supply Chain and Cost Pressures

Medical camera production depends on specialized components like optics, sensors, and cables. Global supply-chain disruptions have created shortages and increased material costs. Manufacturers must find alternative suppliers without compromising on quality. Agile sourcing and strategic inventory management are now essential. Rising prices for semiconductors and precision lenses add further strain. Additionally, healthcare institutions demand cost efficiency, putting pressure on manufacturers’ profit margins. Companies must balance innovation and affordability while ensuring consistent quality and timely delivery. Supply-chain resilience has thus become a key competitive advantage in this sector.

Opportunities

Growing Procedure Demand

The global expansion of healthcare services is increasing the number of surgical and diagnostic procedures. This rise directly drives demand for advanced medical cameras that support precise visualization. Hospitals and clinics are investing in imaging systems to improve surgical accuracy and patient outcomes. The trend is especially strong in minimally invasive and robotic surgeries, where detailed imaging is essential. As patient volumes grow, healthcare providers seek durable, high-resolution cameras that enhance workflow efficiency and reduce diagnostic errors. Manufacturers offering reliable and cost-effective systems are well-positioned to capture this growing demand in both developed and emerging markets.

Screening and Early Intervention

Preventive healthcare is becoming a major focus across global health systems. Governments and private organizations are promoting early screening programs for cancer, cardiovascular, and other chronic diseases. This trend boosts demand for imaging devices that provide accurate, non-invasive diagnostics. Medical cameras play a vital role in early disease detection, supporting visual examinations in endoscopy, dermatology, and ophthalmology. The shift toward proactive healthcare creates steady demand for advanced imaging solutions. Manufacturers offering compact, high-quality, and AI-enabled cameras can help healthcare providers achieve faster and more reliable diagnoses, strengthening their position in the preventive healthcare segment.

AI and Image-Enhancement Capabilities

Artificial intelligence is transforming the medical imaging field. By integrating AI and image-enhancement technologies, manufacturers can improve image clarity, automate analysis, and reduce interpretation time. Smart medical cameras assist clinicians by highlighting abnormalities, guiding procedures, and minimizing human error. These advanced systems also enable real-time decision support during surgeries. AI integration not only improves patient outcomes but also adds new revenue opportunities through software-based upgrades and subscriptions. Companies that combine hardware excellence with intelligent software solutions can build strong competitive advantages and long-term customer relationships in the evolving medical imaging landscape.

Advanced Optics and Modalities

Innovations in optics and imaging modalities are reshaping the medical camera market. Technologies such as 3D visualization, chip-on-tip design, and fluorescence imaging are setting new standards in precision and performance. High-definition and ultra-high-resolution cameras enable surgeons to view fine anatomical details with greater clarity. These advancements open premium upgrade paths for hospitals aiming to improve diagnostic accuracy and operational efficiency. As healthcare providers seek systems that deliver real-time, detailed visuals, manufacturers offering advanced optical solutions stand to benefit from higher margins and stronger market differentiation.

Infection Prevention Design

Infection control is a growing priority in healthcare environments. Medical cameras designed for easy cleaning, sterilization, or single-use applications are gaining traction. The integration of antimicrobial materials and disposable components helps minimize cross-contamination risks. Hospitals increasingly prefer devices that support strict hygiene standards without compromising image quality. Manufacturers focusing on infection-resistant designs can align with evolving hospital purchasing policies. This focus on safety and usability enhances trust among healthcare professionals and improves product acceptance in global markets where infection prevention is a top concern.

Upgrade Cycles in Established Markets

In developed healthcare systems, replacement of aging imaging equipment presents a significant opportunity. Hospitals and diagnostic centers regularly upgrade to newer cameras with improved performance, longer lifespan, and better service support. Vendors offering flexible upgrade programs and after-sales services can attract customers seeking cost-effective modernization. The demand for enhanced imaging quality, digital connectivity, and integration with hospital networks further accelerates these replacement cycles. Companies that provide scalable, future-ready solutions can maintain strong relationships with established institutions while positioning themselves for continuous growth in mature markets.

Conclusion

The global medical camera market is set for steady growth, driven by rising surgical needs, aging populations, and the increasing focus on advanced imaging technologies. Continuous innovation in high-definition and AI-powered systems is improving diagnostic accuracy and surgical precision. Hospitals and clinics are investing in modern camera solutions to enhance patient care and workflow efficiency. Growing demand for minimally invasive procedures and infection control designs further supports market expansion. With ongoing upgrades, regulatory support, and integration of smart imaging technologies, the medical camera market is expected to maintain strong momentum and play a crucial role in shaping the future of healthcare imaging worldwide.

View More

Intraoral Cameras Market || Fundus Cameras Market || Live Cell Imaging Market || Diagnostics Imaging Market || Medical Digital Imaging Systems Market || 3D Medical Imaging Devices Market || Medical Imaging Outsourcing Market || Diagnostic Imaging Market || Urology Imaging Systems Market || Medical Imaging Phantoms Market || Retinal Imaging Devices Market || Molecular Imaging Market || Bio-imaging Market || Mass Spectrometry Imaging Market || Hyperspectral Imaging Systems Market || Optical Imaging Market || US Medical Imaging Market || AI in Medical Imaging Market || Clinical Trial Imaging Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)