Table of Contents

Overview

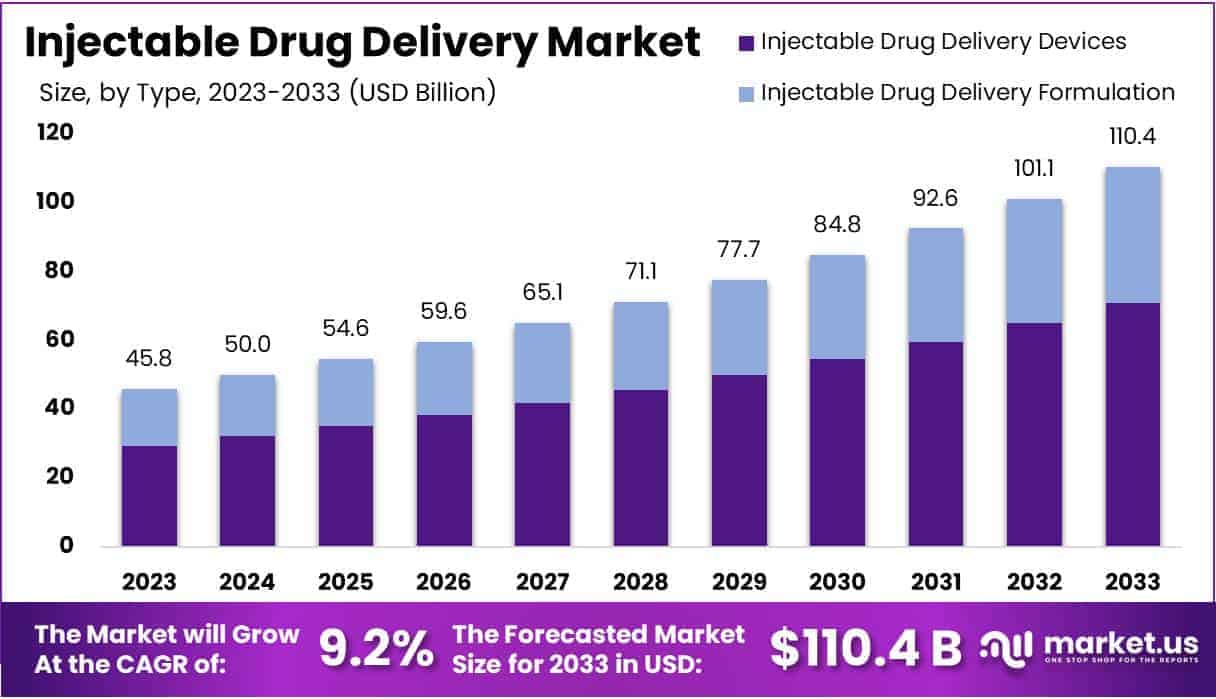

New York, NY – July 16, 2025 – The Global Injectable Drug Delivery Market size is expected to be worth around USD 110.4 Billion by 2033, from USD 45.8 Billion in 2023, growing at a CAGR of 9.2% during the forecast period from 2024 to 2033.

The global Injectable Drug Delivery Market is witnessing significant expansion, driven by the increasing prevalence of chronic diseases, growing biologics demand, and technological innovations in drug delivery systems. Injectable drug delivery involves the administration of therapeutic agents directly into the body through intramuscular, subcutaneous, or intravenous routes. This method ensures rapid onset of action, improved bioavailability, and targeted delivery, making it particularly effective for treating conditions such as cancer, diabetes, and autoimmune disorders.

North America holds the largest market share, attributed to advanced healthcare infrastructure, high biologics consumption, and favorable reimbursement policies. Meanwhile, the Asia-Pacific region is anticipated to witness the fastest growth due to rising healthcare expenditure and increased awareness of injectable therapies.

Technological advancements, such as microneedle systems and long-acting injectables, are transforming the market landscape by enhancing patient compliance and drug efficacy. As pharmaceutical companies continue to invest in R&D and innovative delivery formats, the injectable drug delivery market is poised for sustained growth.

Key Takeaways

- Market Growth: The global injectable drug delivery market is projected to grow from USD 45.8 billion in 2023 to USD 110.4 billion by 2033, registering a compound annual growth rate (CAGR) of 9.2% over the forecast period.

- Device Segment Performance: Injectable drug delivery devices accounted for 64.3% of the market share in 2023, primarily due to their extensive use in administering vaccines, insulin, and biologic therapies.

- Formulation Packaging Trends: Vials led the formulation packaging segment in 2023, holding a 51.2% market share, supported by their advantages in maintaining sterility and drug stability.

- Therapeutic Application Insights: The cancer segment emerged as the leading therapeutic area, capturing 36.2% of the market share in 2023, driven by the rising demand for targeted and immuno-oncology therapies.

- Care Type Distribution: Curative care represented 70% of the market in 2023, reflecting the growing need for chronic disease management through sustained injectable treatments.

- Site of Administration Analysis: Treatments targeting the circulatory and musculoskeletal systems dominated the administration site segment, accounting for 49% of the total market share in 2023.

Segmentation Analysis

- Type Analysis: In 2023, Injectable Drug Delivery Devices accounted for over 64.3% of the market share, owing to their extensive use in administering vaccines, insulin, and biologics. Rising chronic disease prevalence has driven demand for efficient delivery tools. Advancements like auto-injectors and pen injectors further enhanced market penetration by improving patient convenience. A strong pipeline of injectable formulations continues to support the dominance of this segment through sustained innovation and application across diverse therapeutic areas.

- Formulation Packaging Analysis: Vials held the leading position in the Formulation Packaging segment in 2023, capturing more than 51.2% of the market. This dominance is linked to their reliability, sterility, and suitability for storing biologics. Strong adoption in clinical and commercial settings, combined with innovations in break-resistant materials and sealing technologies, have bolstered their use. With chronic diseases on the rise, vials remain essential in ensuring precise dosing and maintaining drug integrity during injectable administration.

- Therapeutic Application Analysis: The cancer segment led the Therapeutic Application category in 2023, securing over 36.2% market share. Growth was driven by the global increase in cancer cases and the need for targeted therapies that require injectable delivery. Oncology treatments benefit from fast bloodstream absorption and reduced side effects, boosting demand. The segment continues to gain momentum through the development of biologics, biosimilars, and long-acting injectables, supported by government funding and advancements in cancer care technologies.

- Usage Pattern Analysis: Curative Care dominated the Usage Pattern segment in 2023, capturing over 70% of the market. This is due to the widespread use of injectable therapies for managing chronic conditions such as cancer, cardiovascular diseases, and diabetes. The growth of biologics and user-friendly formulations has further reinforced this segment. Although immunization and autoimmune treatments are expanding, curative care remains central to injectable drug delivery due to its critical role in long-term disease management.

- Site of Administration Analysis: The Circulatory/Musculoskeletal System segment held over 49% market share in 2023. This dominance is attributed to injectable treatments used in managing systemic and musculoskeletal disorders like diabetes, arthritis, and cardiovascular diseases. The segment is supported by increased use of biologics and biosimilars that require systemic administration. Technological innovations in formulations and delivery mechanisms continue to improve treatment outcomes, reinforcing the importance of this segment in chronic disease care and therapeutic precision.

- Distribution Channel Analysis: Hospital pharmacies led the distribution channel segment in 2023 due to their vital role in acute care, emergency treatment, and chronic disease management. Their proximity to patients and robust supply chains support efficient drug administration. Meanwhile, retail pharmacies and online stores are gaining importance, offering improved accessibility and convenience. Growth in online platforms is propelled by better e-prescription systems and logistics, positioning them as reliable sources for injectable medications, especially in non-critical use cases.

- End User Analysis: Hospitals and clinics were the largest end-user segment in 2023, driven by the urgent need for timely drug administration in acute care. The rise in chronic disease incidence and expansion of hospital infrastructure further solidified this position. Simultaneously, home care usage is expanding rapidly due to the preference for self-administration and reduced treatment costs. Patient-friendly injectables like auto-injectors support this shift, enhancing comfort and enabling long-term care outside traditional healthcare settings.

Market Segments

Type

- Injectable Drug Delivery Devices

- Injectable Drug Delivery Formulation

Formulation Packaging

- Ampoules

- Vials

- Cartridges

- Bottles

Therapeutic Application

- Autoimmune Diseases

- Hormonal Disorders

- Orphan Diseases

- Cancer

- Others

Usage Pattern

- Curative Care

- Immunization

- Others

Site of Administration

- Skin

- Circulatory/Musculoskeletal System

- Organs

- Central Nervous System

Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy Online Stores

End User

- Hospitals and Clinics

- Home Care Settings

- Others

Regional Analysis

- North America: In 2023, North America dominated the global injectable drug delivery market, accounting for over 42.3% of the total share, with a market value of USD 19.37 billion. This leadership is driven by a high burden of chronic diseases, well-established healthcare infrastructure, and the strong presence of key industry players. The region also benefits from widespread adoption of advanced injectable devices and supportive reimbursement frameworks, which further propel market expansion.

- Europe: Europe held a substantial share of the market in 2023, supported by a growing geriatric population and increased demand for biologics and biosimilars. Government-backed initiatives to adopt innovative drug delivery technologies and consistent investments in research and development continue to drive regional market growth. The emphasis on healthcare modernization across major economies contributes further to sustained demand.

- Asia-Pacific: The Asia-Pacific region is projected to witness the fastest growth during the forecast period. Rising healthcare expenditure, increased awareness among patients, and greater involvement of global pharmaceutical firms are major growth drivers. Rapid urbanization and healthcare facility expansion in countries such as China and India, coupled with a growing prevalence of chronic illnesses, are accelerating the adoption of injectable drug delivery systems.

- Latin America: Latin America is expected to register moderate growth, fueled by improving healthcare infrastructure and increased governmental spending on public health. Efforts to enhance access to modern medical treatments and expand pharmaceutical distribution channels are contributing to the market’s development across the region.

- Middle East & Africa: The Middle East & Africa market is also poised for gradual growth, driven by rising incidences of chronic diseases and a growing focus on healthcare innovation. However, regional progress remains limited by economic disparities and political instability in certain areas, which may constrain market potential in select countries.

Emerging Trends

- Microneedle-Based Systems: The use of micron sized needles mounted on patches is gaining momentum. These microneedles enable painless, minimally invasive delivery with fast drug uptake and high bioavailability. As of mid 2025, at least eight clinical studies investigating microneedle patches for anesthesia, insulin delivery, and dermatologic therapies were active on ClinicalTrials.gov.

- Long Acting Injectable Formulations: Development has shifted toward formulations that release medication over weeks or months. In 2023, six novel injectable biologics including fusion proteins and monoclonal antibodies received FDA approval, reflecting this focus on sustained release therapies.

- Smart, Wearable Injectors: Wearable patches that sense physiology and adjust dosing automatically are under preclinical and early stage development. For example, smart insulin patches using glucose responsive microneedle arrays were first demonstrated in 2015, with advanced prototypes validated in large animal models by 2020.

- Suprachoroidal Ocular Delivery: Microneedle injection into the eye’s suprachoroidal space is emerging for posterior segment therapies. This route can increase local drug levels by up to 60 fold compared to eye drops, improving treatment of macular degeneration, diabetic retinopathy, and uveitis.

- Needle Free Microjet Injectors: Research on highly focused liquid microjets offers a path to true needle free administration. Experimental systems have demonstrated precise penetration with microjets achieving well controlled dispersion and small volume dosing in tissue models.

Use Cases

- Vaccination via Microneedles: Dissolving or coated microneedle patches have been shown to elicit immune responses comparable to standard injections. In a recent pediatric study, measles–rubella vaccine delivered by microneedle patch generated antibody levels equivalent to conventional needles, while eliminating sharps waste and reducing pain.

- Diabetes Management: Phase 1 trials (e.g., NCT00837512) have demonstrated that insulin delivered through microneedle arrays achieves rapid glucose lowering with minimal discomfort, paving the way for self administered, pain free insulin therapy in type 1 diabetes patients.

- Ocular Therapies: Suprachoroidal microneedle injections of triamcinolone acetonide (XIPERE) are now FDA approved for macular edema, enabling up to 60× higher drug concentrations in retinal tissues versus eye drops, and reducing treatment frequency for patients with uveitis..

- Pain Management: Electrospun magnetic fiber platforms have been explored for on‑demand release of pain relievers. In preclinical studies, ketorolac loaded fibers under alternating magnetic fields produced controlled drug release with local heating of up to 8°C within 5 minutes, suggesting a future for remotely triggered analgesia.

- Local Anesthesia: Transdermal microneedle patches delivering lidocaine have been compared to EMLA cream in multiple clinical trials. Microneedle pretreatment was found to reduce onset time by approximately 50%, improving patient comfort and procedural efficiency in minor dermatologic procedures.

Conclusion

The global injectable drug delivery market is poised for robust growth, driven by rising chronic disease prevalence, expanding biologics use, and continuous innovation in delivery technologies. Dominated by North America in 2023, the market is witnessing rapid advances such as microneedle patches, long-acting injectables, and smart wearable systems, enhancing both efficacy and patient compliance.

Asia-Pacific is projected to lead future growth due to increasing healthcare investments. Applications span cancer care, diabetes management, and ocular therapies. As pharmaceutical R&D accelerates and self-administration trends rise, injectable drug delivery is set to remain a vital component of modern therapeutic strategies.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)