Table of Contents

Overview

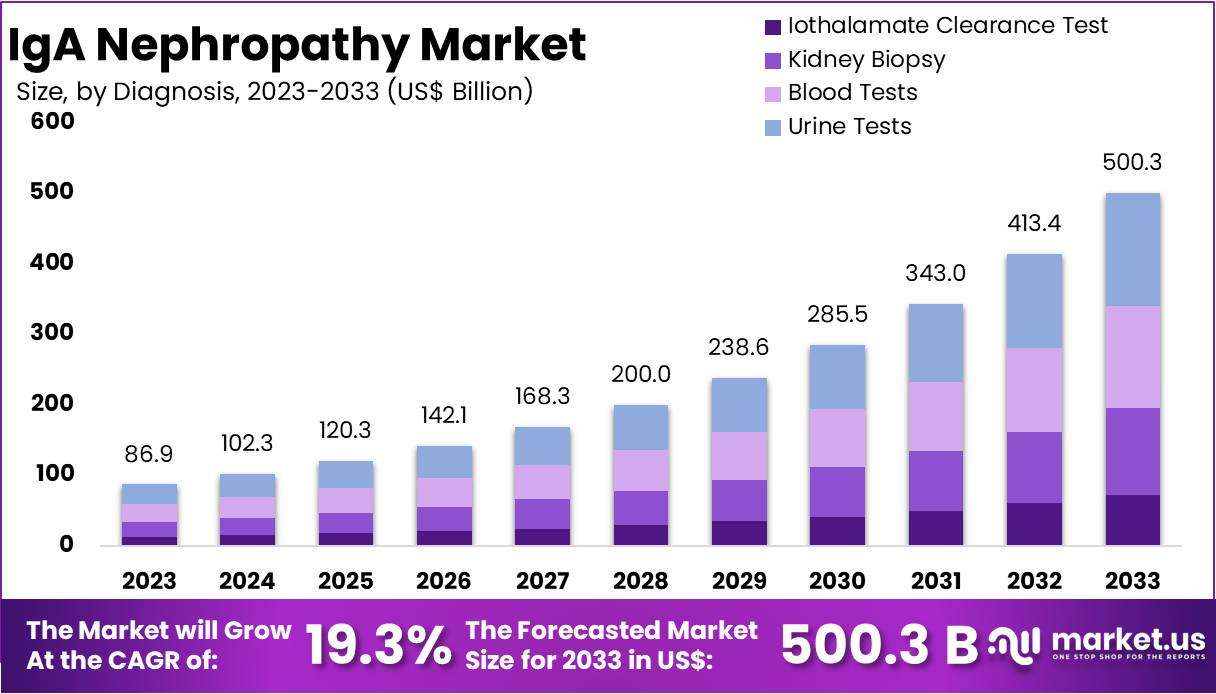

New York, NY – July 22, 2025: The Global IgA Nephropathy Market is projected to grow from US$ 86.9 billion in 2023 to approximately US$ 500.3 billion by 2033. This growth reflects a strong CAGR of 19.3% during the forecast period. IgA Nephropathy, also called Berger’s disease, is a chronic kidney disorder. It results from IgA protein deposits in the kidneys, leading to inflammation and reduced kidney function. While some patients live with mild symptoms, others experience severe outcomes, including end-stage kidney failure. Market growth is driven by unmet needs and the demand for effective treatments.

This market involves the development and distribution of therapies for managing IgA Nephropathy. It includes corticosteroids, immunosuppressants, and biologics. These therapies aim to reduce inflammation, control proteinuria, and slow kidney damage. As there is no cure yet, innovation remains key. Research into targeted immune therapies is expanding. Pharmaceutical companies are investing in novel drugs that modify immune responses. Clinical trials for biologics are gaining momentum. Such advancements make the market highly attractive for investors and stakeholders seeking long-term value.

Globally, IgA Nephropathy is the most common form of glomerulonephritis. According to the National Library of Medicine, the annual incidence is about 2.5 per 100,000 people. Around 30% of patients progress to end-stage renal disease within 20 years of diagnosis. This makes early detection and treatment critical. Regional differences are notable—40% of native kidney biopsies in Japan show IgAN, compared to 25% in Europe and 12% in the U.S. These variations present both challenges and opportunities in market segmentation and tailored treatment approaches.

Recent drug approvals mark a turning point for the market. In February 2023, the FDA gave accelerated approval to sparsentan (Filspari). This dual receptor antagonist reduces proteinuria and slows kidney function decline. It offers better outcomes than traditional therapies like irbesartan. Advances in disease pathophysiology have enabled targeted therapies. New drugs now focus on immune pathway modulation. These innovations are expected to boost market confidence. They also improve quality of life for patients, especially those at risk of disease progression.

Scientific research has linked IgAN to immune dysfunction and genetics. Abnormal IgA deposits cause inflammation and fibrosis in the kidneys. Genetic mutations, such as in the C1GALT1 and C1GALT1C1 genes, contribute to disease risk. However, most cases are sporadic, with familial types being rare. No strong infectious or dietary triggers, except for celiac disease, have been confirmed. Increasing awareness and improved diagnostic tools support early intervention. With ongoing investment in R&D, the market is set for continued innovation and clinical advancements in the coming years.

Key Takeaways

- The IgA nephropathy market is forecast to hit US$ 500.3 billion by 2033, rising from US$ 86.9 billion in 2023 at 19.3% CAGR.

- In 2023, urine tests led the diagnostic landscape, capturing 32.1% of the market due to their ease, accessibility, and non-invasive nature.

- Primary IgA nephropathy was the dominant disease type in 2023, accounting for over 65.9% of the total market share globally.

- Hematuria emerged as the top condition associated with IgA nephropathy in 2023, contributing more than 41.6% to the symptoms segment.

- Pediatric patients represented the largest population group in 2023, with over 76.8% market share, reflecting early onset and frequent screening needs.

- Oral administration dominated treatment delivery in 2023, favored in 63.8% of cases for its convenience, adherence, and non-invasive drug delivery method.

- Hospitals were the primary treatment centers in 2023, securing 36.9% market share due to access to specialized nephrology services and advanced diagnostics.

- North America led the regional market in 2023 with a 45.2% share, reaching US$ 39.28 billion, driven by high diagnosis rates and R&D funding.

Regional Analysis

In 2023, North America led the global IgA nephropathy market with a commanding 45.20% share, valued at US$ 39.28 billion. This dominance is primarily attributed to the region’s high disease prevalence and growing demand for innovative treatments. Advanced healthcare infrastructure, easy access to medical facilities, and strong support for research and clinical trials contribute significantly to market growth. The presence of top-tier research institutions and favorable regulatory frameworks has accelerated drug development and approvals, reinforcing North America’s role as a global hub for IgA nephropathy advancements.

The United States plays a key role in maintaining this leadership, hosting numerous pharmaceutical companies and clinical trial centers focused on developing novel therapies. High healthcare expenditure and widespread insurance coverage improve treatment access, while advocacy groups and awareness campaigns promote early diagnosis and intervention. These combined efforts ensure better patient outcomes and sustained market expansion. As the demand for targeted therapies increases and innovation continues, North America is well-positioned to remain at the forefront of the global IgA nephropathy market in the coming years.

Segmentation Analysis

In 2023, urine tests dominated the diagnosis segment of the IgA nephropathy market, securing a 32.1% market share. Their popularity stems from being non-invasive, cost-effective, and easily available in primary care settings. Urine tests play a critical role in detecting early signs of kidney damage, making them essential for initial screening and ongoing monitoring. Their convenience has made them the preferred diagnostic tool among healthcare providers, especially for routine checkups and disease progression assessments in IgA nephropathy patients.

Blood tests followed closely in importance, providing valuable insights into kidney function through markers like creatinine levels. These tests are often used in conjunction with urine tests to confirm diagnoses and assess disease severity. Their reliability, simplicity, and wide availability in clinical settings reinforce their position in the diagnostic toolkit. Kidney biopsies, while more invasive, remain indispensable for complex cases where definitive confirmation is needed. Additionally, iothalamate clearance tests are employed in specialized settings for precise renal function evaluation, enhancing diagnostic accuracy.

The primary IgA nephropathy type led the disease type segment in 2023, with a share of over 65.9%. This form of the disease is more prevalent and typically develops independently rather than in association with other conditions. It involves immune system dysfunction, specifically IgA antibody buildup in the kidneys, leading to inflammation and scarring. Improved diagnostic capabilities and global awareness have enabled early detection, further increasing the diagnosed cases. Secondary IgA nephropathy, though less common, is gaining clinical attention, especially when linked to liver disease, infections, or autoimmune conditions.

Hematuria emerged as the most reported symptom, representing over 41.6% of the systems segment. Its presence as an early indicator of kidney dysfunction has made it a vital sign in clinical diagnosis. Proteinuria is the second most notable symptom and serves as a key marker for disease progression. It is closely monitored in clinical trials and treatment plans to assess patient outcomes. Symptoms like edema, hypertension, and fatigue, while less prevalent, are being studied more due to their relevance in the advanced stages of the disease.

In terms of population, pediatric patients held a dominant 76.8% market share in 2023. Children often present with more aggressive disease forms, increasing demand for pediatric-focused treatments and care. Early diagnosis and tailored therapies have improved outcomes for this group. The adult segment, while smaller, is steadily growing as awareness and screening improve among older individuals. As the population ages and IgA nephropathy becomes more widely recognized, both segments are expected to see sustained growth, supported by targeted research and personalized treatment plans.

Finally, oral therapies led the route of administration segment, capturing 63.8% of the market. Their convenience and patient compliance make them the preferred choice, especially for long-term management. In contrast, parenteral therapies, such as intravenous or subcutaneous injections, are reserved for severe or unresponsive cases. Hospitals remained the top end-users in 2023, commanding a 36.9% share, owing to their comprehensive care capabilities. These facilities offer specialized diagnostics, expert nephrology care, and structured treatment pathways. As the demand for advanced therapies grows, hospitals will continue to play a central role in IgA nephropathy care delivery.

Key Market Segments

By Diagnosis

- Iothalamate Clearance Test

- Kidney Biopsy

- Blood Tests

- Urine Tests

By Diseases Type

- Primary IgA Nephropathy

- Secondary IgA Nephropathy

By Systems

- Hematuria

- Proteinuria

- Edema

- Others

By Population Type

- Pediatrics

- Adults

By Route of Administration

- Oral

- Parenteral

- Others

By End Users

- Hospitals

- Specialty Clinics

- Homecare

- Others

Key Players Analysis

The IgA nephropathy market is led by major pharmaceutical companies such as Astellas Pharma Inc., Kyowa Kirin Co. Ltd., Merck & Co. Inc., Pfizer Inc., and Johnson & Johnson Services Inc. Astellas emphasizes precision medicine and strategic partnerships to expand its treatment pipeline, while Kyowa Kirin utilizes its immunology and biologics expertise, especially across Asia. Merck capitalizes on its global R&D capabilities to develop therapies for chronic kidney diseases. Meanwhile, Pfizer invests in RNA-based and small-molecule drugs supported by acquisitions, and Johnson & Johnson integrates combination therapies with patient support programs to enhance global access and treatment outcomes.

Emerging players like Omeros Corporation, Calliditas Therapeutics, and Travere Therapeutics are contributing significantly to market innovation. These companies focus on niche treatment strategies, including complement pathway modulation and precision medicine for rare kidney disorders. Collaborations, licensing deals, and region-specific expansion help these players build competitive pipelines. Across the market, increasing awareness, enhanced diagnostics, and rising R&D investments are accelerating growth. Both established and emerging companies are embracing novel therapeutic approaches and patient-centric strategies, creating a competitive and evolving landscape in the IgA nephropathy treatment market.

Market Key Players

- Astellas Pharma Inc.

- Kyowa Kirin Co. Ltd.

- Merck Co. Inc.

- Pfizer Inc.

- Johnson Johnson Services Inc.

- Novartis AG

- Baxter International Inc.

- Fresenius Medical Care AG Co. KGaA

- Otsuka Pharmaceutical Co. Ltd.

- AbbVie Inc.

- Bristol-Myers Squibb Company

- Chugai Pharmaceutical Co. Ltd.

- HoffmannLa Roche Ltd.

Emerging Trends

Shift Toward Targeted Therapies

New therapies are now focusing on the root causes of IgA nephropathy. These treatments aim to control the immune system’s abnormal behavior that leads to kidney damage. Unlike older drugs that work broadly, targeted therapies go after specific immune pathways. This helps reduce kidney inflammation more effectively. It also limits side effects, which is a major improvement for patients. Drug developers are exploring biologics and small molecules for better results. Many of these therapies are now in clinical trials. If successful, they may become standard care in the near future. This trend marks a major step forward in personalized kidney disease treatment.

Increased Focus on Pediatric Treatment

More children are being diagnosed with IgA nephropathy. This shift has caught the attention of researchers and drug companies. Pediatric cases often require different treatment approaches than adults. Children’s immune systems respond differently, and side effects must be carefully managed. As a result, there is growing demand for child-specific therapies. Clinical trials are starting to include younger participants. These studies help doctors understand how well new treatments work in children. Pediatric kidney specialists are also collaborating more with pharmaceutical companies. The goal is to make safer, more effective therapies for kids. This focus on pediatric care is expected to grow.

Rise in Genetic Research

Scientists are looking into how genetics affect the risk of developing IgA nephropathy. Studies show that some people carry genes that make them more likely to get the disease. Research teams are now mapping these genes. They are also exploring how these genes impact treatment response. This information can lead to more personalized care. For example, doctors might one day use genetic testing to choose the best medication for each patient. This type of precision medicine is becoming more common in chronic diseases. As genetic research advances, it could lead to earlier diagnosis and better outcomes for IgA nephropathy patients.

Improved Diagnostic Tools

Early detection of IgA nephropathy is key to better treatment. That’s why better diagnostic tools are in high demand. Traditional tests like urine and blood analysis are being improved for greater accuracy. Researchers are also developing new non-invasive methods to catch the disease early. These tools help doctors detect kidney issues before major damage occurs. Faster and more accurate diagnosis can also reduce unnecessary procedures like biopsies. Many hospitals are adopting digital tools for early screenings. These advancements are helping doctors start treatment sooner. In the long run, this can improve patient outcomes and slow disease progression.

Growing Interest in Complement Inhibitors

Complement inhibitors are a new class of drugs attracting attention in IgA nephropathy research. These drugs target a specific part of the immune system known as the complement pathway. This pathway plays a major role in kidney inflammation. By blocking it, complement inhibitors may reduce damage to kidney tissues. This approach is different from traditional treatments, which suppress the entire immune system. Early trial results are promising, showing fewer side effects and better kidney function. Several companies are now investing in this treatment method. If approved, these drugs could offer a safer, more effective option for many patients.

Use Cases

Long-Term Disease Monitoring

Monitoring is essential in managing IgA nephropathy over time. Most patients undergo 4 to 6 lab tests each year. These include urine tests to check protein levels and blood tests to track kidney function. Regular testing helps doctors detect changes early. It also guides decisions about adjusting medications. By spotting signs of worsening disease quickly, treatment plans can be updated. Some patients also use home urine test kits to support this monitoring. Long-term follow-up is critical to prevent complications. Consistent tracking supports stable kidney health and delays the need for more aggressive treatments.

Treatment with Steroids or Immunosuppressants

For patients with mild to moderate IgA nephropathy, steroid treatment is often the first step. These drugs help reduce inflammation in the kidneys. About 60–70% of early-stage patients respond well to steroids. In many cases, treatment is combined with lifestyle changes like reducing salt intake and managing blood pressure. Immunosuppressants are used when steroid treatment isn’t enough. These medications slow disease progression by lowering immune system activity. Both approaches require close monitoring to avoid side effects. For many, these treatments help maintain kidney function and delay more serious interventions.

Management of End-Stage Kidney Disease (ESKD)

A significant portion of patients—between 25% and 30%—eventually develop end-stage kidney disease. When this happens, dialysis or a kidney transplant becomes necessary. Most patients reach this stage within 5 to 10 years of diagnosis. Hospitals create specialized care plans for these individuals. This includes preparing for transplant evaluations, coordinating with nephrologists, and scheduling dialysis sessions. Emotional and nutritional support are also important parts of care. Managing ESKD is complex and requires a multi-disciplinary team. Early planning and ongoing support improve both survival and quality of life for these patients.

Use of Oral Therapies at Home

Many IgA nephropathy patients rely on oral medications for long-term management. About 65% of patients prefer pills because they can take them at home. Oral treatments help control blood pressure, reduce protein in the urine, and slow down kidney damage. This method is less disruptive to daily life compared to injections or hospital visits. Most medications are taken once or twice a day. Some patients also take vitamin D or cholesterol-lowering drugs as part of their care plan. The convenience of oral therapy makes it a top choice for early to moderate-stage patients.

Clinical Trials for Advanced Therapies

Clinical trials are opening new doors for patients who don’t respond to standard treatments. Thousands of people worldwide are participating in these studies. The trials often focus on drugs that target the immune system more precisely. These include therapies that block specific pathways involved in kidney inflammation. Participation is highest in the U.S., Japan, and several European countries. Many of these patients have moderate to severe disease. The goal is to offer better outcomes with fewer side effects. Clinical trials are also helping researchers gather data to improve future treatment guidelines.

FAQs on IgA Nephropathy

1. What is IgA Nephropathy?

Ans:- IgA Nephropathy, also known as Berger’s disease, is a kidney disorder caused by the buildup of Immunoglobulin A (IgA) in the kidneys. This leads to inflammation and, over time, can affect kidney function.

2. What causes IgA Nephropathy?

Ans:- The exact cause is unknown, but it is linked to immune system abnormalities. Genetics, infections, and autoimmune responses may play a role in triggering the disease.

3. What are the common symptoms of IgA Nephropathy?

Ans:- Symptoms include blood in the urine (hematuria), protein in the urine (proteinuria), swelling in the hands and feet (edema), high blood pressure, and fatigue.

4. How is IgA Nephropathy diagnosed?

Ans:- It is typically diagnosed through urine and blood tests. In some cases, a kidney biopsy is needed to confirm the presence of IgA deposits in the kidney tissue.

5. Is IgA Nephropathy curable?

Ans:- There is no known cure for IgA nephropathy. However, treatments can slow disease progression, control symptoms, and reduce the risk of kidney failure.

6. What is the IgA Nephropathy Market?

Ans:- The IgA nephropathy market includes the development, approval, production, and sale of diagnostics, drugs, and therapies for treating the disease.

7. What is driving growth in the IgA Nephropathy market?

Ans:-Key growth drivers include rising disease prevalence, better diagnostic tools, increased awareness, new drug approvals, and investment in precision medicine.

8. Who are the major players in this market?

Ans:- Major companies include Astellas Pharma, Kyowa Kirin, Merck & Co., Pfizer, Johnson & Johnson, Calliditas Therapeutics, Omeros Corporation, and Travere Therapeutics.

9. What types of treatments are being developed?

Ans:- Targeted therapies, oral treatments, complement inhibitors, RNA-based drugs, and biologics are currently being researched and developed.

10. Which region holds the largest market share?

Ans:- North America leads the market, driven by high awareness, advanced healthcare systems, and strong R\&D activity, particularly in the United States.

Conclusion

The global IgA nephropathy market is undergoing a rapid transformation, fueled by rising disease awareness, advancements in diagnostics, and the shift toward targeted and personalized therapies. With the market expected to surge from US$ 86.9 billion in 2023 to US$ 500.3 billion by 2033 at a strong CAGR of 19.3%, there is significant opportunity for pharmaceutical innovation and investment. Key drivers include the increasing prevalence of pediatric and chronic cases, regional disparities in disease incidence, and breakthroughs in biologics, oral treatments, and complement inhibitors. As clinical trials and genetic research accelerate, the market is poised to deliver more effective, patient-centric solutions, improving long-term outcomes and redefining care standards for IgA nephropathy globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)