Table of Contents

Overview

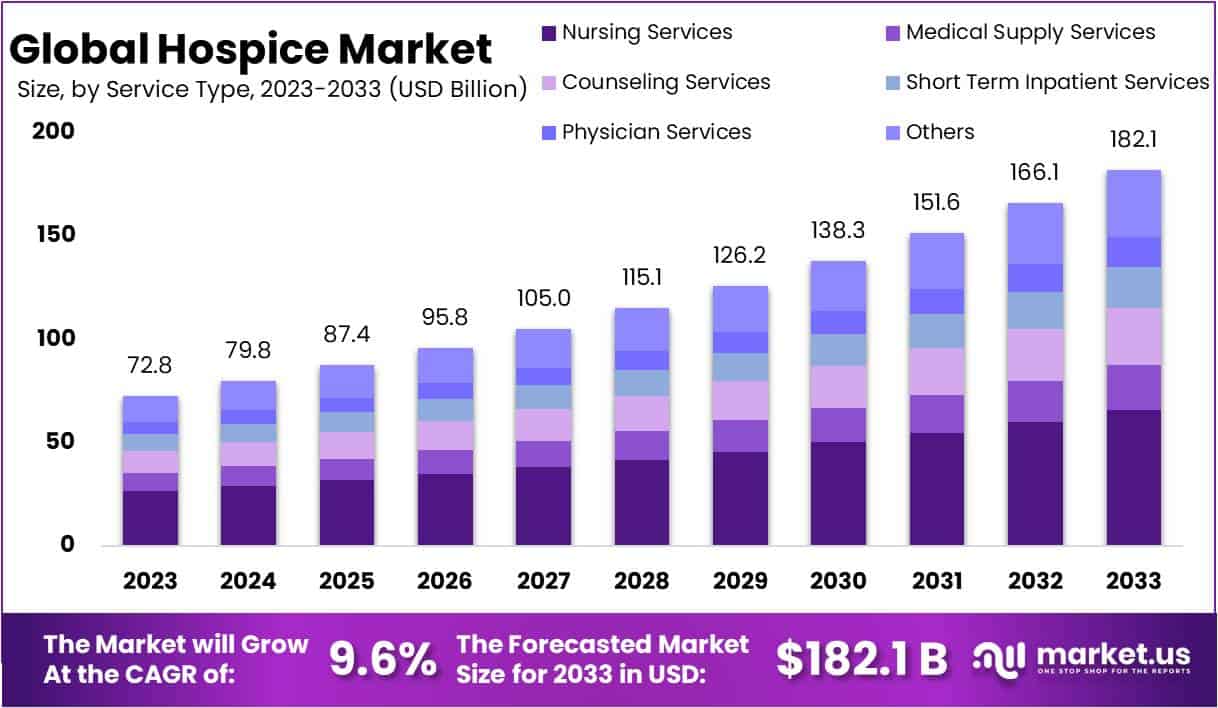

The Global Hospice Market is projected to reach USD 182.1 billion by 2033, growing from USD 72.8 billion in 2023 at a CAGR of 9.6%. Market expansion is driven by the rising ageing population and longer life expectancy worldwide. As more individuals face age-related illnesses, the need for specialized end-of-life care has increased. The focus has shifted from curative treatments to comfort-oriented approaches that improve life quality during advanced stages of illness. This demographic shift continues to strengthen the demand for hospice facilities and home-based care services globally.

The increasing burden of chronic and degenerative diseases, including cancer, cardiovascular disorders, dementia, and respiratory illnesses, is fueling the hospice sector’s growth. Patients with such long-term conditions require continuous symptom management and emotional support, which hospice programs are designed to provide. Growing awareness among healthcare professionals and families about the advantages of early palliative care has further supported this trend. The rising global incidence of lifestyle-related diseases continues to reinforce the importance of accessible and compassionate end-of-life care.

An important trend in the hospice market is the preference for home-based and personalized care. Patients and families are choosing care settings that ensure comfort, dignity, and emotional well-being. The adoption of telehealth, mobile healthcare, and remote monitoring has enhanced the feasibility of home-based hospice programs. These innovations have made care delivery more flexible and responsive to individual needs. The transition to patient-centred care aligns with the broader healthcare focus on personalization and improved patient experience.

Supportive government policies and structured reimbursement frameworks have accelerated market growth. Recognition of hospice care as part of national healthcare systems has increased its accessibility and affordability. In addition, technological advancements such as telemedicine, electronic records, and digital communication tools have improved efficiency and coordination among caregivers. These developments ensure timely interventions, better clinical oversight, and reduced hospital admissions. The combination of policy initiatives and digital transformation continues to strengthen the hospice ecosystem.

The hospice sector is evolving toward integrated and multidisciplinary care models. Collaboration between hospitals, community organizations, and hospice providers ensures continuity of care. At the same time, awareness campaigns and changing attitudes toward end-of-life care have reduced stigma and increased acceptance of hospice services. Providers are expanding specialized programs for paediatric, dementia, and terminal oncology patients while also offering emotional and spiritual support. This evolution highlights the sector’s commitment to dignity, compassion, and holistic well-being in end-of-life care.

Key Takeaways

- 1. The global hospice market is projected to grow from USD 72.8 billion in 2023 to USD 182.1 billion by 2033, registering a 9.6% CAGR.

- Nearly 50% of hospice patients are aged above 84, highlighting the increasing demand for hospice services among the aging global population.

- Nursing services hold the leading 36.2% market share, driven by growing needs for personalized and high-quality hospice care solutions.

- Acute care dominates with a 63.5% share, underscoring its importance in managing severe and life-limiting conditions within hospice environments.

- Home settings account for over 52% of hospice care, reflecting patient preference for familiar, comfortable, and family-centered care environments.

- The integration of technologies such as telehealth is creating new opportunities to improve hospice care accessibility, efficiency, and overall quality.

- North America leads the hospice market with a 38% share, supported by advanced healthcare systems and a large elderly population base.

- The Asia-Pacific region is witnessing rapid growth due to increasing awareness, healthcare infrastructure improvements, and supportive government initiatives.

- High costs of hospice care remain a major barrier, particularly affecting uninsured individuals and populations in lower-income regions.

- The market shows a clear shift toward personalized, home-based hospice care, aligning with evolving patient expectations and family-centered care preferences.

Regional Analysis

In 2023, North America led the global hospice market with over 38% of the total share, valued at USD 27.7 billion. The dominance of this region is attributed to its strong healthcare infrastructure and the high incidence of chronic illnesses. The growing elderly population also drives the need for end-of-life care services. These factors together support the expansion of hospice facilities and increase the adoption of specialized palliative programs across the region, strengthening its leadership position.

Europe followed as the second-largest regional market. The region’s growth is supported by a rapidly aging population and advanced healthcare systems. Various countries have implemented supportive healthcare policies emphasizing palliative and hospice care. Additionally, growing public awareness of the importance of quality end-of-life care has contributed to steady market expansion. The focus on patient-centered approaches and integrated care models continues to shape Europe’s hospice service landscape, enhancing accessibility and service quality across the region.

The Asia-Pacific region is experiencing rapid growth in hospice services. Rising awareness, healthcare infrastructure development, and changing cultural views on end-of-life care are key factors. Countries such as China and India are major contributors, owing to growing investments in healthcare and supportive government initiatives. Improved training programs for hospice professionals and expanding community-based care models further boost market demand. The region is expected to continue its upward trajectory, reflecting a shift toward compassionate and organized palliative care practices.

Latin America and the Middle East & Africa hold smaller shares but show promising potential. Growth in these regions is driven by better healthcare access and an increasing number of patients with life-limiting conditions. Efforts to raise awareness and expand hospice facilities are underway, though progress remains gradual. Cultural barriers and limited resources still challenge widespread adoption. However, as governments and private providers enhance healthcare standards, these regions are expected to record consistent, long-term market growth.

Segmentation Analysis

In 2023, the Nursing Services segment led the Hospice Market’s Services segment with over a 36.2% share. This growth was driven by the rising demand for personalized patient care and the increasing number of chronic conditions requiring extended nursing support. The growing recognition of quality end-of-life care, emphasizing comfort and dignity, further strengthened the segment. Integration of advanced nursing practices focusing on pain management, symptom control, and emotional support has played a key role in improving patients’ quality of life and reinforcing this segment’s dominance.

The Acute Care segment dominated the Care Type segment in 2023, capturing more than 63.5% of the market share. This strong performance was due to the increasing prevalence of chronic illnesses and an aging population. Acute care focuses on immediate relief for patients with severe symptoms while providing emotional and psychological support. The segment’s growth was also fueled by healthcare policy improvements, integration of palliative services, and higher healthcare expenditures. These factors collectively strengthened acute care’s essential role in the hospice market’s expansion.

In the Application segment, the Home Settings category held a major share of over 52% in 2023. This dominance was due to the rising preference for patient-centered care that allows individuals to remain at home during end-of-life care. The trend was further supported by advancements in telehealth and remote monitoring technologies, which improved home care efficiency. Additionally, cost-effectiveness and insurance reimbursement options enhanced adoption. Home-based hospice care emerged as a practical, compassionate, and affordable alternative to institutional care, driving its continued market growth.

Key Market Segments

Services

- Nursing Services

- Medical Supply Services

- Counseling Services

- Short Term Inpatient Services

- Physician Services

- Others

Care Type

- Acute Care

- Respite Care

Application

- Home Settings

- Hospitals

- Specialty Nursing Homes

- Hospice Care Centers

Key Players Analysis

The hospice market is defined by strong competition and continuous advancements in patient care standards. Key organizations have established a dominant presence by offering compassionate and specialized services. Their efforts focus on improving the quality of life for patients with terminal illnesses. Through strategic programs and care models, these organizations promote comfort, dignity, and support for both patients and families. This approach has positioned them as trusted providers in the broader healthcare continuum, setting benchmarks for professional excellence and emotional care.

Among the leading participants, Covenant Care is notable for its patient-centered philosophy that emphasizes empathy and holistic well-being. Its commitment to personalized care has strengthened its market presence. The National Association for Home Care & Hospice contributes through advocacy and policy leadership, ensuring consistent service standards across the sector. By influencing regulations and best practices, it enhances the overall credibility and sustainability of hospice services in various regions.

Kindred Healthcare LLC plays a crucial role through its integrated care framework. Its model connects hospice services seamlessly with rehabilitation and home health programs, ensuring continuity and efficiency in patient management. This comprehensive approach supports better outcomes and operational scalability. Similarly, PruittHealth has gained recognition for its dedicated care toward elderly and chronically ill populations. The company’s tailored hospice solutions reinforce family engagement and long-term patient comfort, further strengthening its industry reputation.

Other prominent entities, such as the National Hospice and Palliative Care Organization, Alzheimer’s Association, VITAS Healthcare, LHC Group Inc., and Samaritan Health Services, also drive significant advancements. Their combined efforts promote innovation, training, and technological adaptation in hospice care delivery. Collectively, these organizations enhance accessibility, improve service quality, and expand awareness about end-of-life care. Their contributions continue to shape market growth and position the hospice sector as a key component of modern healthcare systems.

Market Key Players

- Covenant Care.

- National Association for Home Care & Hospice.

- Kindred Healthcare LLC

- PruittHealth

- National Hospice and Palliative Care Organization

- Oklahoma Palliative & Hospice Care.

- Alzheimer’s Association

- VITAS Healthcare

- LHC Group Inc.

- Dierksen Hospice

- Samaritan Health Services.

- Other Key Players

Challenges

1) Workforce Shortages and Turnover

Recruiting and retaining skilled staff such as nurses, aides, and social workers remains a major challenge. Staffing shortages and high turnover continue to affect home- and hospice-based care across the U.S. Although some metrics show slight improvement since the pandemic, vacancy rates are still high in critical roles. This ongoing workforce pressure limits capacity and leads to more referral rejections. Providers must balance service demand with staffing gaps, often resulting in operational strain and reduced care availability for patients needing end-of-life support.

2) Payment Updates and Margin Pressure

The U.S. Centers for Medicare & Medicaid Services (CMS) approved a 2.9% payment increase for FY 2025. Providers failing to submit required quality data will face a negative adjustment. Wage index updates and the overall cap also continue to affect local reimbursement rates. As a result, margins remain tight and vary significantly among providers. Financial outcomes are closely linked to care settings, length of stay, and case mix. Sustaining profitability under these conditions requires efficient resource allocation and close monitoring of reimbursement trends.

3) Tightened Oversight and Compliance Risk

Federal oversight of hospice operations is growing stronger. The HHS Office of Inspector General (OIG) continues to audit and investigate Medicare payment practices. Recent findings highlight improper billing and documentation issues in hospice care. These actions increase the compliance and administrative burden for providers. Organizations must strengthen internal controls, update documentation protocols, and train staff to meet federal standards. Failing to comply could result in penalties, repayment demands, and reputational harm. Compliance now requires ongoing vigilance and proactive management across all levels.

4) Quality Reporting Changes

Quality reporting in hospice care is becoming more complex. CMS has updated the Hospice Quality Reporting Program (HQRP) and introduced new public reporting elements. Starting October 1, 2025, some measures will transition to the new HOPE assessment tool for FY 2026 data. Providers must also adapt to revisions in the CAHPS® Hospice Survey, which will soon include a web-based response option. These updates require operational planning, staff training, and system adjustments. Staying compliant with evolving reporting standards is essential for maintaining eligibility and public transparency.

5) Telehealth Policy Uncertainty

Medicare’s telehealth flexibilities remain in place until September 30, 2025. However, several provisions will expire after that date, creating uncertainty for hospice providers. Many organizations adopted virtual visits and remote recertifications during the pandemic. As these flexibilities phase out, hospices must modify care workflows and documentation practices. Providers need to balance patient convenience with regulatory requirements while ensuring continuity of care. Clear policy guidance and early adjustments are crucial to minimize disruption and maintain quality under changing telehealth rules.

6) Access and Equity Gaps

Globally, only about 14% of people needing palliative care receive it. In the U.S., hospice use among Medicare beneficiaries remains below pre-pandemic levels. Geographic disparities persist, especially in rural and frontier communities, where access to care is limited. Socioeconomic and cultural factors further widen these gaps. Expanding equitable access requires policy reforms, community outreach, and resource investment. Efforts to address these inequities can improve care quality and ensure that all individuals, regardless of location, receive compassionate end-of-life support.

Opportunities

1. Expand Home-Based and Community Models

The demand for home-based hospice care is increasing rapidly. Patients and families prefer familiar surroundings with easier access to caregivers. Partnerships with community and primary care providers can help expand these services. The experience gained during the pandemic proved that remote monitoring and triage can work effectively. By maintaining these workflows, organizations can enhance responsiveness and after-hours support. Home and community care also reduce hospital dependency and improve patient satisfaction. Expanding these models ensures greater reach, better continuity of care, and cost efficiency while addressing growing patient preferences.

2. Strengthen Quality and Patient Experience

Improving care quality and patient satisfaction remains a key priority. Upcoming HQRP and HOPE transitions provide a roadmap for progress. Standardizing assessments and reducing documentation gaps enhance consistency in care delivery. CAHPS® data help identify communication issues, symptom management needs, and caregiver training opportunities. Public reporting updates also encourage organizations to maintain excellence in quality performance. Focusing on patient experience not only improves outcomes but also strengthens trust. Investing in better communication, staff education, and consistent quality reviews builds a strong reputation and boosts patient and caregiver confidence.

3. Optimize Case Mix and Care Pathways

Effective case management and balanced care pathways can improve both patient outcomes and financial performance. MedPAC analysis highlights that hospice margins depend on the length of stay and care setting mix. Early engagement with palliative care and clear eligibility workflows reduce late referrals. Proactive goals-of-care discussions help match patients to appropriate services sooner. These actions prevent unnecessary hospitalizations and ensure timely support. Optimizing care pathways promotes clinical efficiency and cost stability without extending stays beyond need. It allows hospices to provide compassionate, well-timed care while maintaining operational balance.

4. Workforce Redesign and Retention

Retaining skilled hospice staff is crucial for sustainable growth. Workforce redesign can reduce turnover and improve care quality. Proven strategies include flexible scheduling, cross-training, preceptor programs, and mental health support. Career ladders motivate employees by offering professional advancement opportunities. Partnerships with nursing schools can also strengthen hiring pipelines. Paid preceptorships help new nurses gain real-world experience while building long-term loyalty. These approaches improve workforce stability, maintain visit capacity, and ensure consistent patient care. A supportive work environment enhances engagement and reduces burnout, making organizations more resilient and efficient.

5. Compliance as a Competitive Edge

Strong compliance systems can become a major advantage for hospice providers. Proactive audit preparation and accurate billing help reduce financial risks. Using data-driven tools for benefit coordination and billing review minimizes recoupments and errors. Continuous staff education ensures regulatory updates are followed correctly. As oversight tightens, organizations that maintain audit readiness will perform better. Compliance analytics also enhance transparency and accountability. By viewing compliance as a strategic function rather than a burden, hospices can protect revenue, strengthen reputation, and demonstrate integrity in every aspect of care delivery.

6. Address Unmet Need and Equity

Many communities still lack adequate hospice care access. Expanding services to underserved populations presents a major growth opportunity. Collaboration with rural health centers, faith-based groups, and community clinics can help close care gaps. These partnerships encourage timely referrals and reduce disparities in symptom relief and caregiver support. Equity-focused initiatives also improve trust among diverse populations. Addressing unmet needs supports national goals for inclusive and accessible healthcare. By reaching marginalized patients, hospice organizations can grow responsibly while fulfilling their mission of compassionate, equitable end-of-life care.

Conclusion

The global hospice market is growing steadily due to the rising elderly population and the increasing number of chronic illnesses worldwide. The shift toward patient-centered and home-based care reflects a broader preference for comfort, dignity, and quality of life in end-of-life support. Strong government policies, telehealth adoption, and integrated care models are improving service delivery and accessibility. However, workforce shortages and compliance pressures remain key challenges. Continued investments in staff training, technology, and equitable access will be essential for sustainable growth. The hospice sector is expected to expand further, driven by compassionate care models and the global focus on holistic healthcare.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)