Table of Contents

Overview

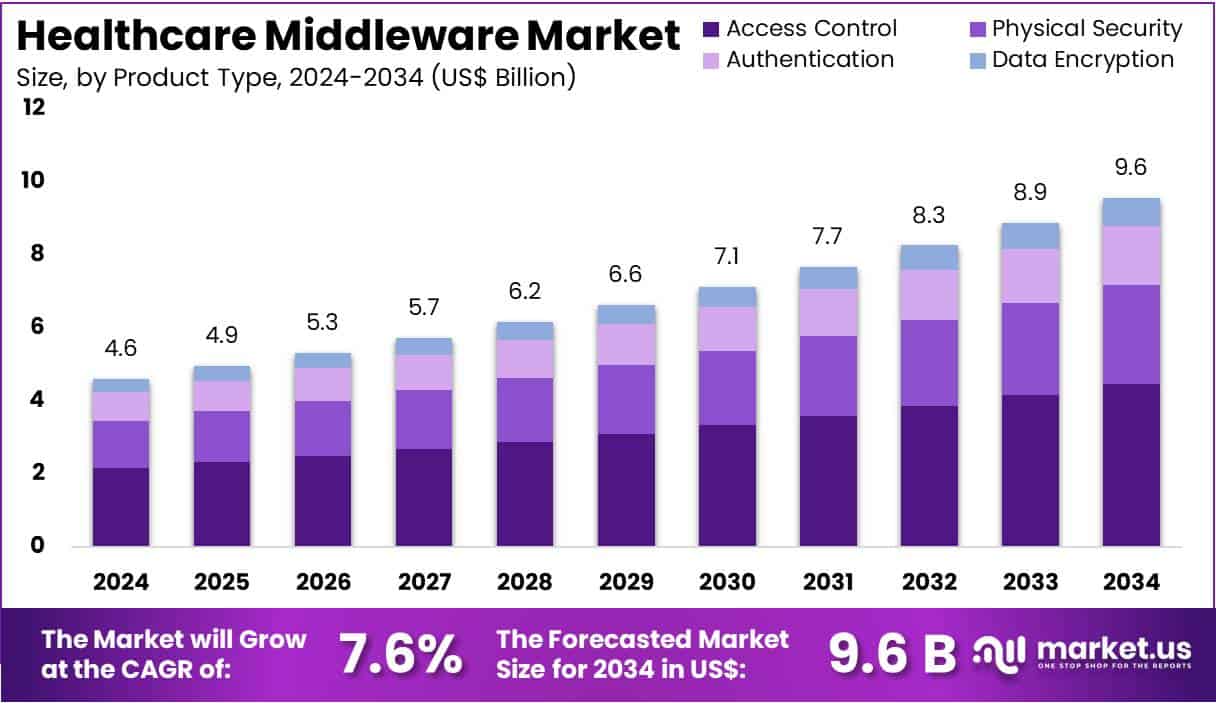

New York, NY – July 28, 2025 – The Healthcare Middleware Market Size is expected to be worth around US$ 9.6 Billion by 2034 from US$ 4.6 Billion in 2024, growing at a CAGR of 7.6% during the forecast period 2025 to 2034.

Healthcare middleware plays a critical role in modernizing healthcare IT systems by enabling seamless communication between diverse applications, devices, and databases across clinical and administrative workflows. As healthcare organizations increasingly rely on digital platforms for electronic health records (EHR), telemedicine, patient engagement, and analytics, middleware serves as the integration backbone that ensures interoperability and real-time data exchange.

This technology acts as a software bridge, allowing disparate systems such as radiology information systems (RIS), laboratory information systems (LIS), and billing platforms to function cohesively. Core functionalities of healthcare middleware include data normalization, secure message routing, device connectivity, application programming interfaces (APIs), and HL7/DICOM standards compliance. These capabilities are essential for achieving a unified healthcare ecosystem that supports value-based care, population health management, and regulatory compliance.

The demand for healthcare middleware is driven by the rapid digital transformation of the healthcare sector, coupled with government mandates for health information exchange (HIE) and data privacy under regulations such as HIPAA and GDPR. Additionally, middleware solutions enhance operational efficiency, reduce IT complexity, and support real-time clinical decision-making by enabling data-driven workflows.

As healthcare providers continue to adopt cloud-based systems, AI applications, and remote patient monitoring tools, healthcare middleware is expected to remain a foundational technology for future-ready, patient-centric digital health infrastructure.

Key Takeaways

- By Product Type: The market is segmented into physical security, access control, authentication, and data encryption. Among these, access control emerged as the leading segment in 2024, accounting for 46.7% of the total market share.

- By Technology: Healthcare middleware solutions are categorized into cloud-based, on-premise, and hybrid models. Cloud-based solutions dominated the segment, capturing a notable 53.2% share in 2024, driven by scalability and remote accessibility.

- By Application: The application scope includes clinical integration, patient management, enterprise resource planning, and data analytics. The patient management segment held the largest revenue share of 44.3%, reflecting the growing emphasis on coordinated care and operational efficiency.

- By Format: Middleware formats are divided into Health Level 7 (HL7), Fast Healthcare Interoperability Resources (FHIR), and Digital Imaging and Communications in Medicine (DICOM). The HL7 format led the market with a revenue share of 49.1%, owing to its widespread adoption for health data exchange.

- By End-User: The market is further classified into hospitals & clinics, pharmaceutical companies, insurance companies, and healthcare providers. Hospitals & clinics dominated with a 57.8% market share in 2024 due to high demand for integrated IT infrastructure.

- By Region: North America emerged as the leading regional market, holding a commanding 53.2% share in 2024, supported by advanced healthcare IT systems and strong regulatory compliance frameworks.

Segmentation Analysis

- Product Type Analysis: The access control segment accounted for 46.7% of the market in 2024, driven by heightened concerns over data security and patient privacy. Rising cyber threats and stringent healthcare regulations necessitate secure access management solutions. Integration with biometric and multi-factor authentication enhances system security and audit capabilities. As healthcare providers prioritize compliance and operational transparency, access control systems will remain essential for securing physical and digital environments in healthcare facilities.

- Technology Analysis: Cloud-based solutions dominated with a 53.2% share due to their scalability, flexibility, and reduced infrastructure costs. These platforms support seamless data integration across telehealth and mobile health applications while enabling real-time access to healthcare systems. Additionally, centralized security updates and automated compliance support make cloud middleware highly efficient. As healthcare digitization advances, cloud-based technology is expected to remain the preferred deployment model due to its adaptability and support for dynamic healthcare workloads.

- Application Analysis: Patient management held the largest revenue share at 44.3% in 2024, fueled by the shift toward coordinated, patient-centric care. Middleware enhances integration across scheduling, billing, and EHR systems, improving efficiency and minimizing errors. Demand for chronic disease management and personalized treatment plans also drives this segment. Additionally, embedded analytics within middleware supports care quality monitoring, aligning with value-based care initiatives and making patient management a vital application in healthcare middleware platforms.

- Format Analysis: The HL7 format led with a 49.1% revenue share, supported by its widespread adoption as a standard for clinical data exchange. HL7 enables seamless interoperability between EHRs, lab systems, and other healthcare platforms. Its integration with FHIR enhances future compatibility and flexibility. As regulatory bodies emphasize standardized, secure data exchange, HL7-based middleware remains critical for supporting interoperability and compliance, ensuring its continued dominance in the healthcare middleware format segment.

- End-user Analysis: Hospitals and clinics accounted for 57.8% of the market, reflecting their need to manage large volumes of clinical and administrative data. These facilities require middleware to integrate systems across departments for better care coordination, data security, and reporting accuracy. With increasing adoption of cloud and mobile platforms, hospitals are investing in middleware that ensures interoperability and real-time data access. Regulatory pressures and the need for efficient resource utilization further drive this segment’s growth.

Market Segments

By Product Type

- Physical Security

- Access Control

- Authentication

- Data Encryption

By Technology

- Cloud-based

- On-premise

- Hybrid

By Application

- Clinical Integration

- Patient Management

- Enterprise Resource Planning

- Data Analytics

By Format

- Health Level 7 (HL7)

- Fast Healthcare Interoperability Resources (FHIR)

- Digital Imaging and Communications in Medicine (DICOM)

By End-user

- Hospitals & Clinics

- Pharmaceutical Companies

- Insurance Companies

- Healthcare Providers

Regional Analysis

North America Leads the Healthcare Middleware Market

In 2024, North America accounted for the largest revenue share of 39.2% in the global healthcare middleware market. This dominance is primarily driven by the growing need for seamless interoperability and real-time data exchange across complex healthcare IT infrastructures. The U.S. Department of Health & Human Services (HHS) and the Office of the National Coordinator for Health Information Technology (ONC) continue to advocate for standardized health information exchange, reinforcing the importance of middleware technologies.

The widespread implementation of Electronic Health Records (EHRs) in U.S. hospitals supported by ONC-reported high adoption rates further underscores the need for middleware to integrate disparate systems. These technologies enable efficient communication between EHRs, diagnostic platforms, and administrative tools, enhancing clinical workflow efficiency and data accuracy. The regulatory push for improved care coordination and data standardization is expected to sustain regional market growth.

Asia Pacific to Exhibit the Fastest Growth Rate

The Asia Pacific region is projected to witness the highest compound annual growth rate (CAGR) during the forecast period, driven by increased investment in digital health infrastructure and the rapid expansion of interconnected healthcare systems. Several countries in the region are launching national health information exchange (HIE) platforms, which rely on middleware for secure and standardized data sharing.

The growing number of hospitals and healthcare institutions, alongside the accelerating adoption of EHRs, telehealth, and mobile health applications, is creating a strong demand for integration platforms. As governments advance digital health policies and prioritize data-driven healthcare delivery, middleware adoption across Asia Pacific is expected to rise significantly, positioning the region as a key growth frontier.

Emerging Trends

- Interoperability via FHIR-based Middleware: Healthcare middleware now frequently uses HL7 FHIR APIs to enable real-time data exchange between disparate systems. For example, U.S. rules now mandate FHIR-based patient access APIs for Medicare Advantage and Medicaid plans under the 21st Century Cures Act. Germany and Switzerland are adopting FHIR under national initiatives (such as gematik or SWITCH A.1) to deliver device data, lab results, and medication records via middleware layers.

- Shift to Open and Standardized Frameworks: A long-term federal trend in U.S. healthcare has pushed movement from proprietary systems toward open, standards-based platforms supported by middleware layers that enforce security, data validation, and connectivity.

- Service-Oriented, Health 4.0 Middleware Frameworks: The concept of Health 4.0 integrates edge computing, IoT, cloud/fog, big data, and machine learning within sophisticated middleware frameworks. These frameworks deliver services such as real-time patient monitoring, event detection, and integration with cyber-physical systems.

- Middleware as Translation Layer for Legacy Systems: Roughly 60% of U.S. healthcare providers face fragmentation due to incompatible legacy systems. Middleware is increasingly used to connect legacy Electronic Health Records (EHR) with modern applications, handling extract-transform-load (ETL) and translation tasks to enable unified workflows.

- Integration of IoHT and Wearables via Real-Time Middleware: Academic studies demonstrate IoT-based middleware for connecting sensors (e.g. ECG, blood pressure monitors) to diagnostic applications. One case used real-time messaging middleware (FastDDS) to support remote X-ray classification with latency ~65 ms and throughput ~3.2 KB/s, achieving ~88% accuracy in chest imaging.

Use Cases

- Secure Inter-facility Data Exchange: Middleware enables hospitals and clinics to share patient data including lab results, medication history, clinical notes electronically and securely. One example is the Bidirectional Health Information Exchange (BHIE) used by the U.S. Department of Veterans Affairs and Department of Defense. It supports real-time exchange of outpatient pharmacy data, allergies, lab orders, radiology, and clinical notes across facilities.

- Interoperability Between Disparate EHR Systems: Middleware acts as a translator between different Electronic Health Record (EHR) systems. It converts data from legacy formats into standardized structures such as HL7 or FHIR, enabling seamless integration without replacing existing systems.

- Laboratory Workflow Automation: Cloud-based middleware streamlines lab processes by automating result entry, quality control checks, and result delivery. Such tools reduce turnaround time and improve data quality in testing services.

- IoT-based Patient Monitoring: Specialized middleware supports integration of biosensors and wearable devices (IoHT). This enables continuous monitoring of vital signs and transmission to remote caregivers for chronic disease management and home care monitoring.

- Standardized API Access via FHIR: Middleware provides FHIR-compliant APIs that enable structured access to discrete healthcare data (e.g. patient details, admissions, medications), allowing third-party apps and digital platforms to interact securely with healthcare information systems.

- Clinical Alert Routing and Messaging: Middleware routes real time clinical alerts from alarm systems or nurse calls to appropriate staff via mobile devices or central dashboards. This improves patient safety by ensuring timely response to critical events.

Conclusion

In conclusion, healthcare middleware is a vital enabler of digital transformation across the global healthcare ecosystem. By ensuring interoperability, secure data exchange, and seamless integration of diverse health IT systems, middleware supports efficient clinical workflows, regulatory compliance, and patient-centered care. Its applications span EHR interoperability, lab automation, IoT-based monitoring, and real-time analytics.

With rising adoption of cloud platforms, FHIR standards, and connected care technologies, the demand for middleware is poised to grow. North America leads the market, while Asia Pacific presents the fastest growth potential. As healthcare evolves toward data-driven, integrated care models, middleware remains a foundational component of future-ready health infrastructure.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)