Table of Contents

- Introduction

- Editor’s Choice

- Functional and Natural Health Food Market Value Worldwide

- Healthy Snacks Market Value Worldwide

- Global Dietary Supplements Market Size

- Global Wellness Market Statistics

- Global Digital Health Market Size

- Vitamins & Minerals Market Statistics

- Global Sports and Active Nutrition Market Value

- Protein Intake Worldwide

- Consumers’ Definitions of Healthy Food

- Consumers Who Actively Try to Eat Healthily – By Country

- Demographics of Consumers That Actively Try to Eat Healthy

- Attitudes Towards Food in Various Countries

- Healthy Eating at Restaurants

- Fast Food Preferences

- Worldwide Sales of Organic Food

- Healthy Food Purchase Preferences

- Adoption of Dieting

- Interest in Healthy Eating and Lifestyle

- Consumer Views on Health and Sustainability – By Level of Usage

- Cost of a Healthy Diet in Various Nations and Regions

- Key Spending Statistics

- Regulations for Different Health and Functional Foods

- Recent Developments

- Conclusion

- FAQs

Introduction

Health Conscious Consumer Statistics: A health-conscious consumer prioritizes physical, mental, and environmental well-being in their purchasing decisions.

They favor organic, natural, and plant-based foods, along with functional products like supplements and performance enhancers.

Fitness and active lifestyles are key, with many using technology to track their health. Mental health awareness is also a significant factor, driving interest in stress-reducing and mindfulness products. This group prefers eco-friendly, sustainable options and is heavily influenced by social media trends.

Retailers are responding by offering health-focused products and services, creating growth opportunities in sectors like food, wellness, fitness, and technology.

Editor’s Choice

- From 2021 to 2026, protein intake is expected to grow at varying rates globally, with China and Hong Kong leading at a 10.2% increase.

- In 2024, U.S. consumers defined healthy food primarily as fresh (39%) or rich in protein and low in sugar (37%).

- As of February 2024, the highest proportions of consumers trying to eat healthily were in Nigeria (82%) and Kenya (81%).

- As of September 2024, 67% of respondents in India reported actively trying to eat healthy, reflecting a growing focus on health and sustainability.

- As of April 2023, the Philippines had the highest share of consumers (85%) ordering fast food through delivery apps in Asia.

- In the United States, 45% of respondents in 2024 followed a diet to feel better and have more energy, the most common motivation.

- The National Institutes for Health (NIH) allocated nutritional funding to reach 2.231 billion dollars in 2023.

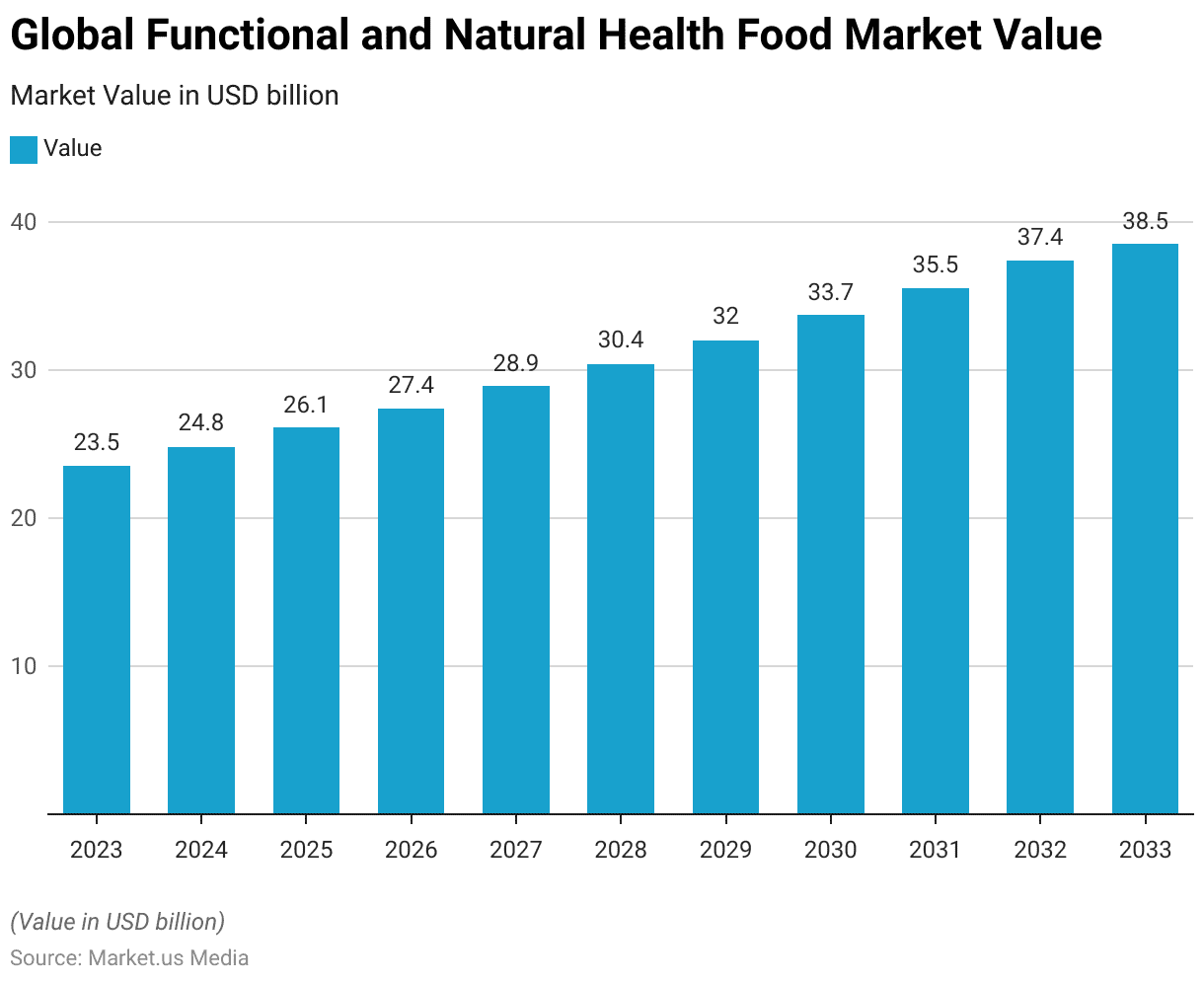

Functional and Natural Health Food Market Value Worldwide

- The global functional and natural health food market is projected to experience steady growth from 2023 to 2033.

- In 2023, the market value is estimated at USD 23.5 billion and is expected to increase to USD 24.8 billion in 2024.

- By 2025, the market is anticipated to reach USD 26.1 billion, followed by further growth to USD 27.4 billion in 2026.

- The upward trend continues, with the market value advancing to USD 28.9 billion in 2027 and USD 30.4 billion in 2028.

- The market is forecasted to expand to USD 32.0 billion by 2029, reaching USD 33.7 billion in 2030.

- By 2031, the market value is projected to grow to USD 35.5 billion, and it is expected to reach USD 37.4 billion in 2032.

- Finally, the global functional and natural health food market is estimated to achieve a value of USD 38.5 billion by 2033.

- This consistent growth highlights the increasing consumer demand for health-conscious and natural food products.

(Source: Statista)

Healthy Snacks Market Value Worldwide

- The global healthy snacks market has shown a consistent upward trajectory from 2021 to 2030.

- In 2021, the market was valued at USD 85.6 billion and increased to USD 90.6 billion in 2022.

- By 2023, the market reached USD 96.58 billion, and it is expected to grow further to USD 102.95 billion in 2024.

- The market value is projected to rise to USD 109.75 billion in 2025 and USD 116.99 billion in 2026.

- This growth continues, with the market reaching USD 124.71 billion in 2027 and USD 132.94 billion in 2028.

- By 2029, the market is forecasted to achieve USD 141.72 billion, and it is expected to reach USD 152.5 billion by 2030.

- This steady expansion reflects the increasing consumer demand for healthier snack options across the globe.

(Source: Statista)

Global Dietary Supplements Market Size

- The global dietary supplements market has demonstrated significant growth from 2016 to 2028.

- In 2016, the market size was valued at USD 135 billion and grew to USD 147 billion in 2017.

- By 2018, the market reached USD 160 billion, continuing its upward trend to USD 175 billion in 2019.

- In 2020, the market expanded further to USD 191 billion, followed by a rise to USD 205 billion in 2021.

- The growth continued in 2022, with the market size reaching USD 220 billion, and it further increased to USD 235 billion in 2023.

- In 2024, the market is expected to reach USD 250 billion, followed by a projected increase to USD 265 billion in 2025.

- By 2026, the market size is forecasted to reach USD 280 billion, continuing its expansion to USD 295 billion in 2027.

- Finally, the global dietary supplements market is expected to reach USD 308 billion by 2028, underscoring the increasing demand for health and wellness products.

(Source: Statista)

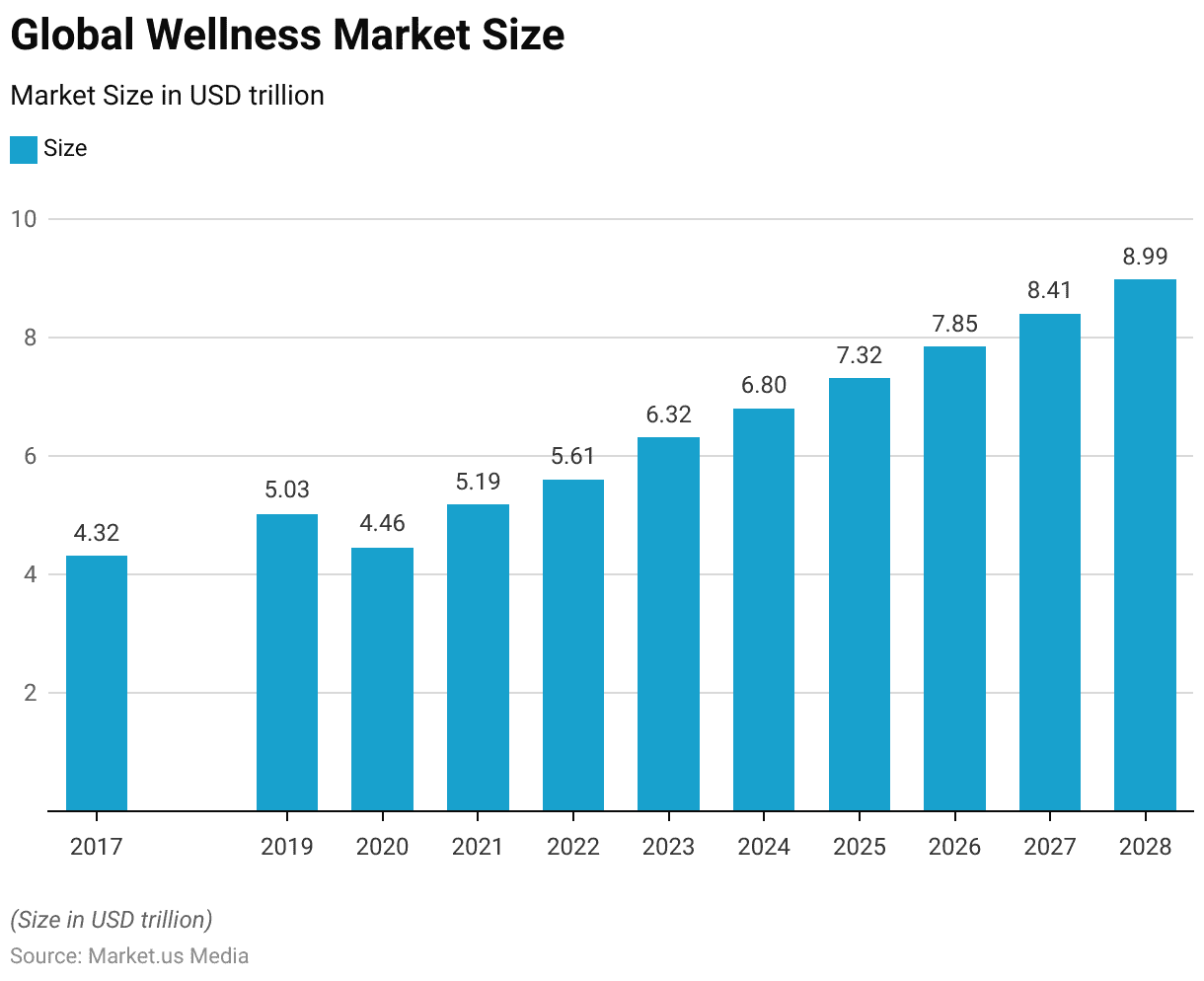

Global Wellness Market Statistics

Size of the Wellness Market Worldwide

- The global wellness market has experienced significant growth from 2017 to 2028.

- In 2017, the market was valued at USD 4.32 trillion, and it increased to USD 5.03 trillion in 2019.

- However, in 2020, the market size slightly decreased to USD 4.46 trillion due to the global impact of the pandemic.

- The market rebounded in 2021, reaching USD 5.19 trillion, and continued its upward trajectory in 2022 with a value of USD 5.61 trillion.

- By 2023, the market had grown to USD 6.32 trillion, with further expansion expected in the coming years.

- In 2024, the market is forecasted to reach USD 6.8 trillion, followed by USD 7.32 trillion in 2025.

- The growth continues with projections of USD 7.85 trillion in 2026, USD 8.41 trillion in 2027, and a forecasted value of USD 8.99 trillion by 2028.

- This consistent expansion reflects the increasing global focus on health, well-being, and wellness-related products and services.

(Source: Statista)

Market Size of the Wellness Industry Worldwide – By Segment

- In 2023, the global wellness industry was valued across several key segments.

- The largest segment was personal care and beauty, with a market size of USD 1,213 billion, followed by health eating, nutrition, and weight loss at USD 1,096 billion.

- The physical activity sector reached USD 1,060 billion, while wellness tourism was valued at USD 830 billion.

- Public health prevention and personalized medicine contributed USD 781 billion to the market, and traditional and complementary medicine accounted for USD 553 billion.

- Wellness real estate had a market size of USD 438 billion, with mental wellness at USD 233 billion.

- The spa industry was valued at USD 137 billion, while springs contributed USD 63 billion.

- Workplace wellness was the smallest segment, valued at USD 52 billion.

- This distribution highlights the broad scope and diverse range of services driving the global wellness market in 2023.

(Source: Statista)

Global Digital Health Market Size

- The global digital health market has experienced significant growth from 2019 to 2025.

- In 2019, the market size was valued at USD 175 billion and grew to USD 216 billion in 2020.

- By 2021, the market reached USD 268 billion, followed by a further increase to USD 334 billion in 2022.

- The market continued its rapid expansion, reaching USD 417 billion in 2023.

- It is projected to grow to USD 523 billion in 2024, with the market size expected to reach USD 657 billion by 2025.

- This remarkable growth reflects the increasing integration of digital technologies in healthcare, driven by innovations in telemedicine, wearable devices, and health data management.

(Source: Statista)

Vitamins & Minerals Market Statistics

Revenue of the Vitamins & Minerals Market Worldwide

- The global vitamins and minerals market has shown steady growth from 2020 to 2029.

- In 2020, the market revenue was USD 23.56 billion and increased to USD 25.89 billion in 2021.

- By 2022, the market reached USD 27.5 billion, followed by a rise to USD 29.7 billion in 2023.

- The market continued to expand, with revenues projected to reach USD 31.93 billion in 2024 and USD 35.24 billion in 2025.

- Growth persists through the following years, with the market expected to reach USD 36.7 billion in 2026 and USD 39.2 billion in 2027.

- By 2028, the market is forecasted to grow to USD 41.69 billion, and it is projected to reach USD 44.18 billion by 2029.

- This consistent increase underscores the rising demand for vitamins and minerals, driven by growing health awareness and a focus on preventive care.

(Source: Statista)

Revenue of the Vitamins & Minerals Market Worldwide – By Country

- In 2023, the revenue from the vitamins and minerals market varied significantly across different countries.

- China led with a revenue of USD 4,820.57 million, followed by the United States at USD 4,369.39 million.

- India ranked third with USD 2,402.96 million, while Australia generated USD 1,302.10 million.

- Brazil’s revenue stood at USD 1,175.49 million, and Japan’s market reached USD 1,024.59 million.

- Canada earned USD 937.19 million, with Poland contributing USD 804.08 million.

- The United Kingdom had a revenue of USD 723.66 million, and Indonesia followed with USD 677.32 million.

- South Korea and the Philippines recorded revenues of USD 665.95 million and USD 515.86 million, respectively.

- Russia’s market reached USD 512.94 million, while Germany earned USD 392.19 million.

- Other countries such as Israel, Iran, and Mexico generated USD 360.52 million, USD 335.69 million, and USD 302.97 million, respectively.

- Spain’s revenue was USD 295.16 million, with the Netherlands, France, Switzerland, Belgium, and Turkey earning between USD 191.68 million and USD 97.81 million.

- Saudi Arabia and Sweden recorded much smaller revenues, at USD 49.08 million and USD 5.36 million, respectively.

- This distribution reflects the varying levels of demand and consumption for vitamins and minerals across the globe.

(Source: Statista)

Global Sports and Active Nutrition Market Value

- The global sports and active nutrition market has demonstrated steady growth from 2022 to 2027.

- In 2022, the market was valued at USD 27.7 billion and increased to USD 29.4 billion in 2023.

- By 2024, the market is projected to reach USD 31.1 billion, followed by further growth to USD 33 billion in 2025.

- The expansion continues, with the market expected to reach USD 35 billion in 2026, and it is projected to reach USD 37.1 billion by 2027.

- This growth reflects the rising consumer demand for products that support active lifestyles and athletic performance, driven by increasing health consciousness and fitness trends.

(Source: Statista)

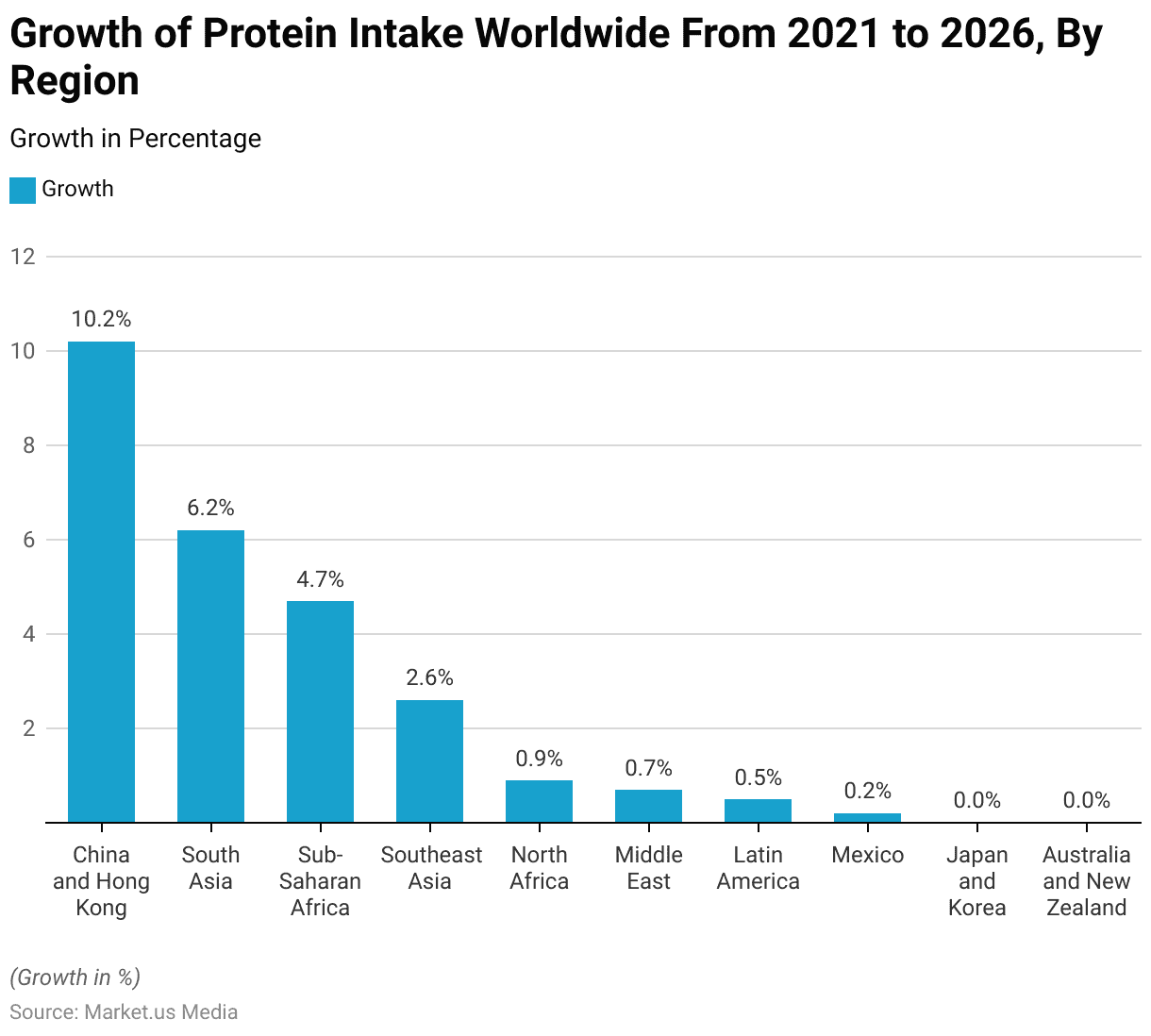

Protein Intake Worldwide

- From 2021 to 2026, protein intake is expected to grow at varying rates across different regions worldwide.

- China and Hong Kong are projected to experience the highest growth, with an increase of 10.2%.

- South Asia follows with a growth rate of 6.2%, while Sub-Saharan Africa is expected to see a 4.7% rise in protein intake.

- Southeast Asia is projected to experience a more moderate growth of 2.6%, followed by North Africa at 0.9%.

- The Middle East is expected to grow at a rate of 0.7%, and Latin America at 0.5%.

- Mexico is forecasted to have a minimal growth of 0.2%. At the same time, Japan and Korea, along with Australia and New Zealand, are expected to see no growth in protein intake during this period.

- These regional variations reflect diverse dietary habits, economic factors, and health trends driving protein consumption worldwide.

(Source: Statista)

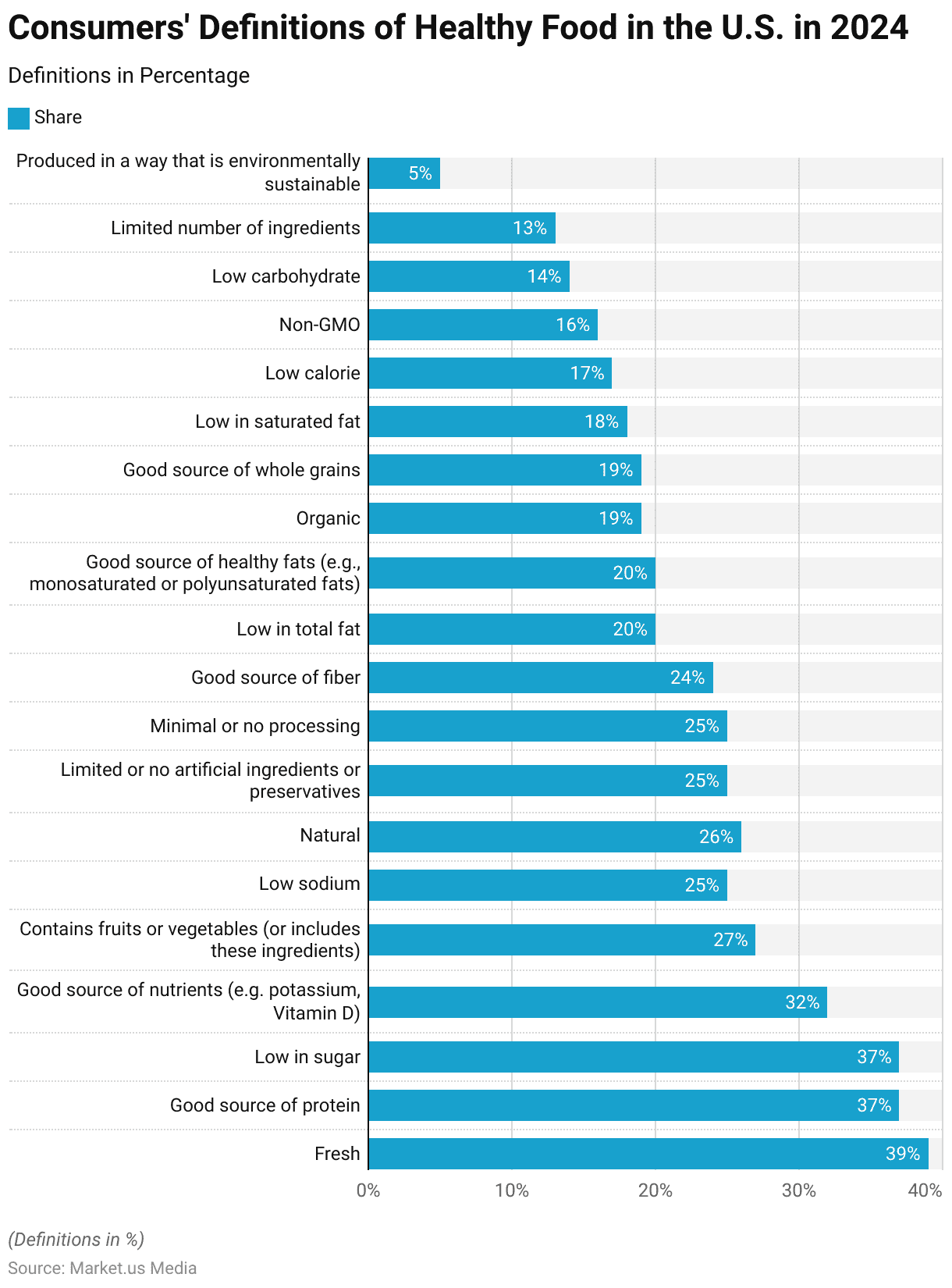

Consumers’ Definitions of Healthy Food

- In 2024, consumers in the United States defined healthy food in various ways, with the most common responses reflecting a preference for fresh and nutritious options.

- A significant 39% of respondents considered fresh food to be healthy, while 37% identified foods that are a good source of protein and low in sugar as key characteristics of healthy eating.

- Additionally, 32% considered foods that are rich in nutrients like potassium and Vitamin D as healthy.

- Other notable responses included foods containing fruits or vegetables (27%) and those that are low in sodium (25%).

- Around 26% viewed natural foods as healthy, and 25% emphasized the importance of foods with minimal artificial ingredients or preservatives.

- Foods that are minimally processed (25%) and high in fiber (24%) were also important to many consumers.

- Lower total fat content (20%) and the presence of healthy fats (20%) were cited by a similar proportion of respondents.

- Organic foods (19%) and those with whole grains (19%) were considered healthy by many, while 18% highlighted the importance of foods that are low in saturated fat.

- Other factors like low-calorie content (17%), non-GMO (16%), low carbohydrate (14%), and a limited number of ingredients (13%) also contributed to the definition of healthy food.

- Lastly, only 5% of respondents emphasized environmental sustainability in food production as a key factor in defining healthy food.

(Source: Statista)

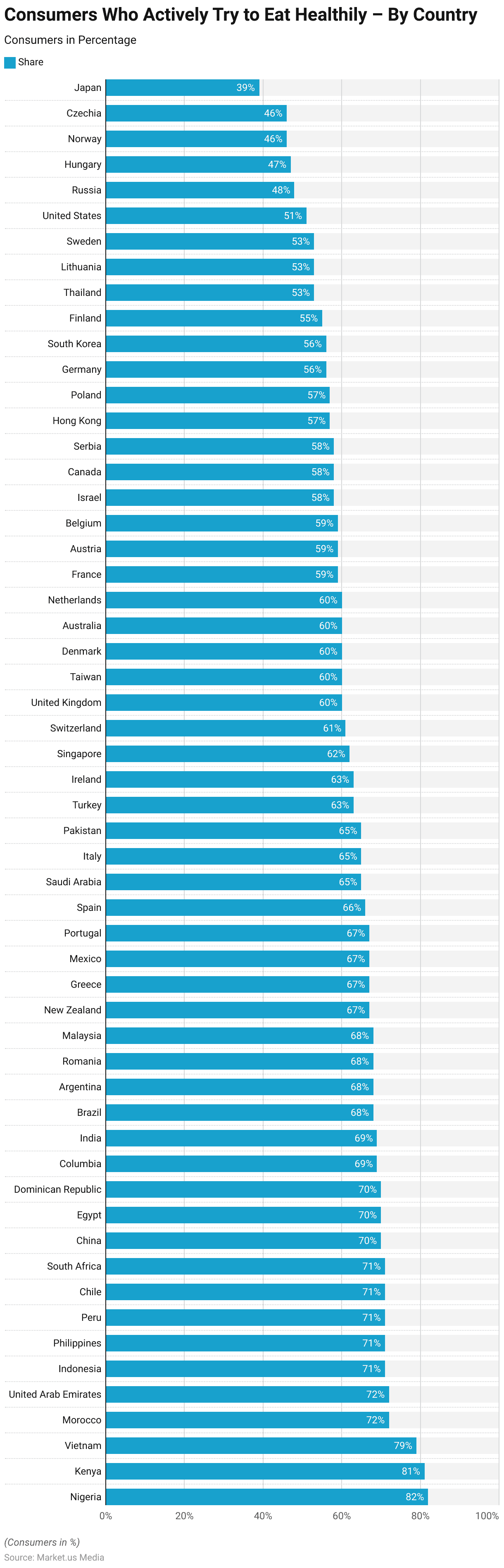

Consumers Who Actively Try to Eat Healthily – By Country

- As of February 2024, the share of consumers who actively try to eat healthily varies significantly across countries and territories worldwide.

- The highest proportions were seen in Nigeria (82%) and Kenya (81%), followed closely by Vietnam at 79%.

- Several countries, such as Morocco, the United Arab Emirates, Indonesia, the Philippines, Peru, and Chile, each reported 71%, while South Africa was at 71%.

- Other notable countries include China and Egypt, both at 70%, with the Dominican Republic also at 70%.

- In South America, Colombia, India, Brazil, and Argentina, around 69% of consumers are trying to eat healthily. Similarly, Romania, Malaysia, and New Zealand recorded 68%.

- In European countries such as Greece, Mexico, Portugal, Spain, Saudi Arabia, and Italy, around 67% of consumers focused on healthy eating.

- Other countries with strong healthy eating trends include Pakistan (65%), Turkey (63%), Ireland (63%), and Singapore (62%).

- In developed markets, Switzerland, the United Kingdom, Taiwan, Denmark, Australia, and the Netherlands all reported 60%, with France, Austria, and Belgium at 59%.

- Israel and Canada showed 58%, while Serbia and Hong Kong were at 58% as well.

- Other countries like Poland and Germany reported around 57%, with South Korea at 56%. In the Nordic and Baltic regions, Finland, Thailand, Lithuania, and Sweden reported 53%.

- The lowest shares of consumers trying to eat healthily were observed in the United States (51%), Russia (48%), Hungary (47%), Norway (46%), and Czechia (46%), with Japan showing the lowest at 39%.

- This data reflects varying levels of health-conscious eating habits across different regions and cultures globally.

(Source: Statista)

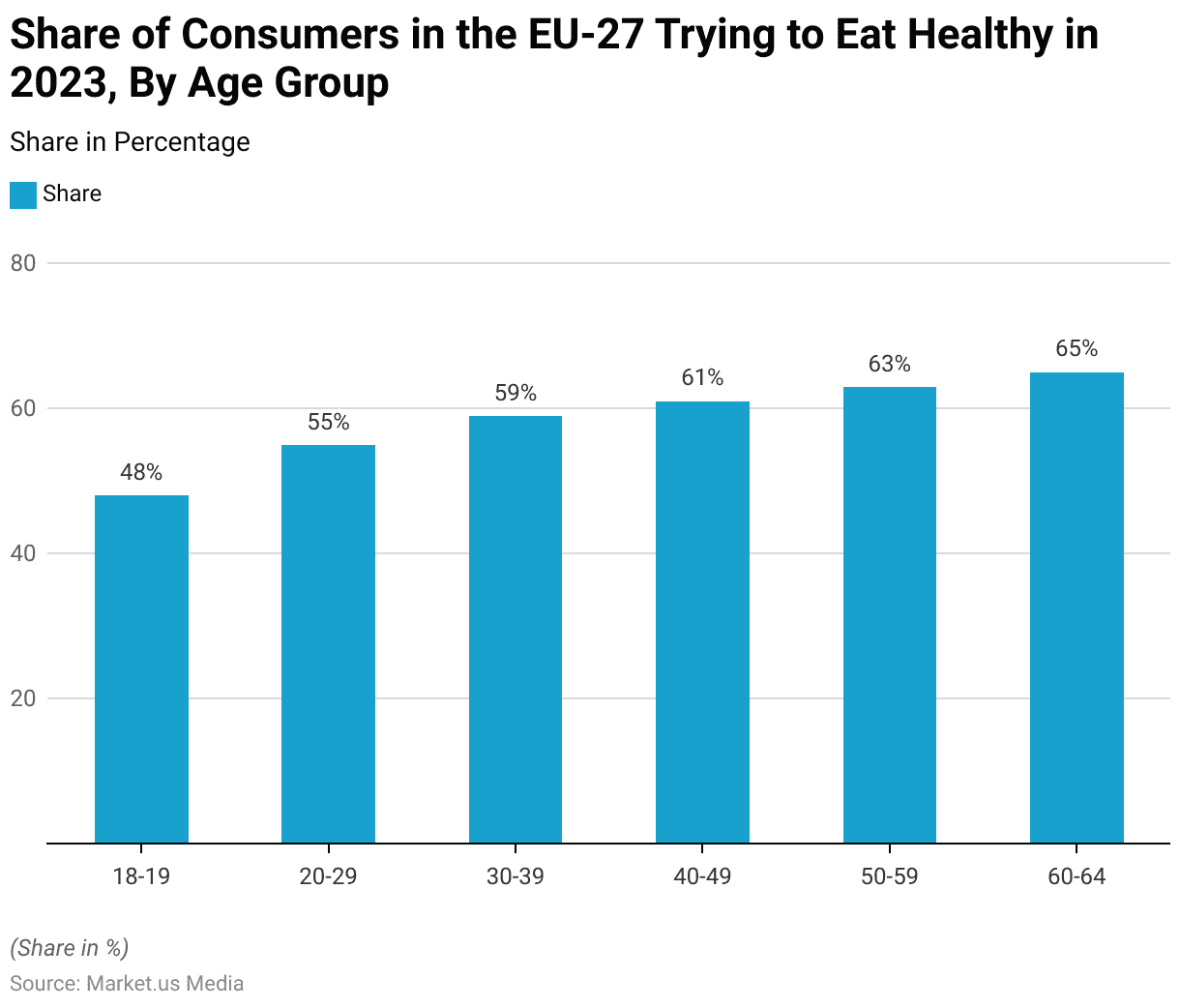

Demographics of Consumers That Actively Try to Eat Healthy

Health Conscious Consumer Statistics By Age Group

- In 2023, the share of consumers in the European Union (EU-27) who actively try to eat healthily varied across different age groups.

- Among respondents aged 18-19, 48% reported actively trying to eat healthy.

- This share increased with age, with 55% of consumers in the 20-29 age group and 59% in the 30-39 group.

- The trend continued upward, with 61% of those aged 40-49, 63% of individuals aged 50-59, and 65% of those in the 60-64 age group actively making efforts to eat healthily.

- This data indicates that older consumers are more likely to focus on healthy eating compared to younger age groups within the EU.

(Source: Statista)

Health Conscious Consumer Statistics By Generation

- In 2023/24, the share of consumers in the United Kingdom who actively try to eat healthy varied across different generations.

- Among Generation Z, 58% of respondents reported actively making efforts to eat healthily, while 59% of Millennials shared the same intention.

- Generation X showed a slightly higher proportion, with 60% trying to eat healthy.

- Baby boomers had the highest percentage, with 63% of respondents actively focusing on healthy eating.

- This data reveals that the inclination to maintain a healthy diet increases with age in the UK, with older generations being more likely to prioritize healthy eating.

(Source: Statista)

Attitudes Towards Food in Various Countries

Health Conscious Consumer Statistics in India

- As of September 2024, attitudes towards food in India reflect a growing focus on health and sustainability.

- A significant 67% of respondents reported actively trying to eat healthy, while 48% expressed a preference for avoiding plastic packaging when purchasing food.

- Additionally, 46% of consumers stated they avoid artificial flavors and preservatives, and 44% emphasized the importance of convenience and fast food options.

- There was also a notable inclination towards reducing meat consumption, with 29% of respondents indicating they try to eat less meat.

- Cultured meat, or lab-grown meat, had a smaller but still significant appeal, with 20% of consumers expressing openness to it.

- Food intolerances were reported by 18% of respondents, and 16% mentioned that they do not enjoy cooking.

- Financial concerns related to healthy eating were acknowledged by 12% of consumers, stating they couldn’t afford to eat healthily.

- Only 3% of respondents indicated they did not relate to any of the listed food-related attitudes.

- These responses highlight the evolving food culture in India, with increasing attention to health, sustainability, and convenience.

(Source: Statista)

Health Conscious Consumer Statistics in United States

- As of September 2024, attitudes towards food in the United States reveal a mix of health-consciousness and convenience.

- Half of the respondents (50%) reported actively trying to eat healthy, while 30% emphasized the importance of food being convenient and fast.

- A significant 24% of consumers stated they avoid artificial flavors and preservatives, and 21% try to eat less meat.

- Financial concerns were noted by 19% of respondents, who said they can’t afford to eat healthily, while 17% expressed a lack of interest in cooking.

- Another 17% reported food intolerances, and 15% indicated they try to avoid plastic packaging when buying food.

- Lab-grown or cultured meat was met with a degree of openness, with 13% of respondents willing to consider it.

- Finally, 12% of participants identified with none of the listed attitudes towards food.

- These findings reflect the ongoing shift in U.S. food attitudes, balancing health, convenience, and environmental considerations.

(Source: Statista)

Health Conscious Consumer Statistics in Australia

- As of September 2024, attitudes towards food in Australia reflect a strong emphasis on health and sustainability.

- A majority of respondents (59%) reported actively trying to eat healthily, while 32% expressed a preference for avoiding artificial flavors and preservatives.

- Additionally, 29% of Australians stated they try to avoid plastic packaging when purchasing food, and 28% emphasized the need for food to be convenient and fast.

- There was also a significant proportion (21%) who try to eat less meat, while 19% indicated that they do not enjoy cooking.

- Food intolerances were reported by 17% of respondents, and 14% mentioned financial barriers, stating they cannot afford to eat healthily.

- The idea of lab-grown or cultured meat was met with some openness, as 14% of consumers expressed interest in it.

- Lastly, 7% of respondents identified with none of the listed attitudes towards food.

- These findings highlight Australia’s growing concern for healthy eating, sustainability, and the convenience of food choices.

(Source: Statista)

Health Conscious Consumer Statistics in France

- As of September 2024, attitudes towards food in France reveal a growing focus on health and sustainability.

- A majority of respondents (58%) reported actively trying to eat healthy, while 36% stated they try to eat less meat, and 35% avoided artificial flavors and preservatives.

- Additionally, 30% emphasized the need for food to be convenient and fast, with the same proportion (30%) also trying to avoid plastic packaging when purchasing food.

- Financial constraints were mentioned by 16% of respondents, who indicated they could not afford to eat healthily, and 16% expressed a lack of interest in cooking.

- Openness to lab-grown or cultured meat was relatively low, with only 10% of consumers willing to consider it.

- Food intolerances were also reported by 10% of respondents and 7% of participants identified with none of the listed attitudes.

- These insights illustrate the evolving food culture in France, balancing health-conscious choices with concerns about sustainability and convenience.

(Source: Statista)

Health Conscious Consumer Statistics in Canada

- As of September 2024, attitudes towards food in Canada highlight a strong focus on health and convenience.

- A majority of respondents (60%) reported actively trying to eat healthily, while 32% avoided artificial flavors and preservatives.

- Additionally, 31% emphasized the importance of food being convenient and fast, and 24% expressed a preference for avoiding plastic packaging when purchasing food.

- There is also a desire to reduce meat consumption, with 24% of respondents trying to eat less meat.

- Financial concerns were noted by 17% of participants, who said they could not afford to eat healthily, while 19% admitted to not enjoying cooking.

- Food intolerances were reported by 16% of respondents, and 13% expressed openness to eating lab-grown or cultured meat.

- Finally, 7% of respondents identified with none of the listed attitudes.

- These findings reflect a growing commitment to healthy eating in Canada, alongside concerns about convenience, sustainability, and affordability.

(Source: Statista)

Health Conscious Consumer Statistics in Spain

- As of September 2024, attitudes towards food in Spain reveal a significant commitment to health and sustainability.

- A majority of respondents (61%) reported actively trying to eat healthily, while 38% avoided artificial flavors and preservatives.

- Additionally, 31% expressed a preference for avoiding plastic packaging when purchasing food, and 28% stated they try to eat less meat.

- The desire for convenience in food was mentioned by 21% of participants, while 16% admitted to not enjoying cooking.

- Food intolerances were reported by 13% of respondents, and 12% expressed openness to eating lab-grown or cultured meat.

- Financial constraints were less of an issue, with only 7% indicating they could not afford to eat healthily, and 7% of respondents identified with none of the listed attitudes.

- These findings highlight a strong focus on health-conscious eating and sustainability, with a growing awareness of food choices in Spain.

(Source: Statista)

Health Conscious Consumer Statistics in the Netherlands

- As of September 2024, consumer attitudes towards food in the Netherlands reflect a strong focus on health and convenience.

- A majority of respondents (59%) actively try to eat healthy, while 37% prioritize food that is convenient and fast.

- Additionally, 33% aim to eat less meat and 25% make an effort to avoid plastic packaging when purchasing food.

- A smaller proportion, 22%, avoid artificial flavors and preservatives, while 17% do not enjoy cooking.

- Lab-grown or cultured meat is a possibility for 16% of respondents, and 11% report having one or more food intolerances.

- Financial constraints seem to be less of a concern, as only 10% indicate they can’t afford to eat healthily.

- These findings suggest that while health-conscious eating and sustainability are important to many Dutch consumers, convenience remains a key factor in their food choices.

(Source: Statista)

Healthy Eating at Restaurants

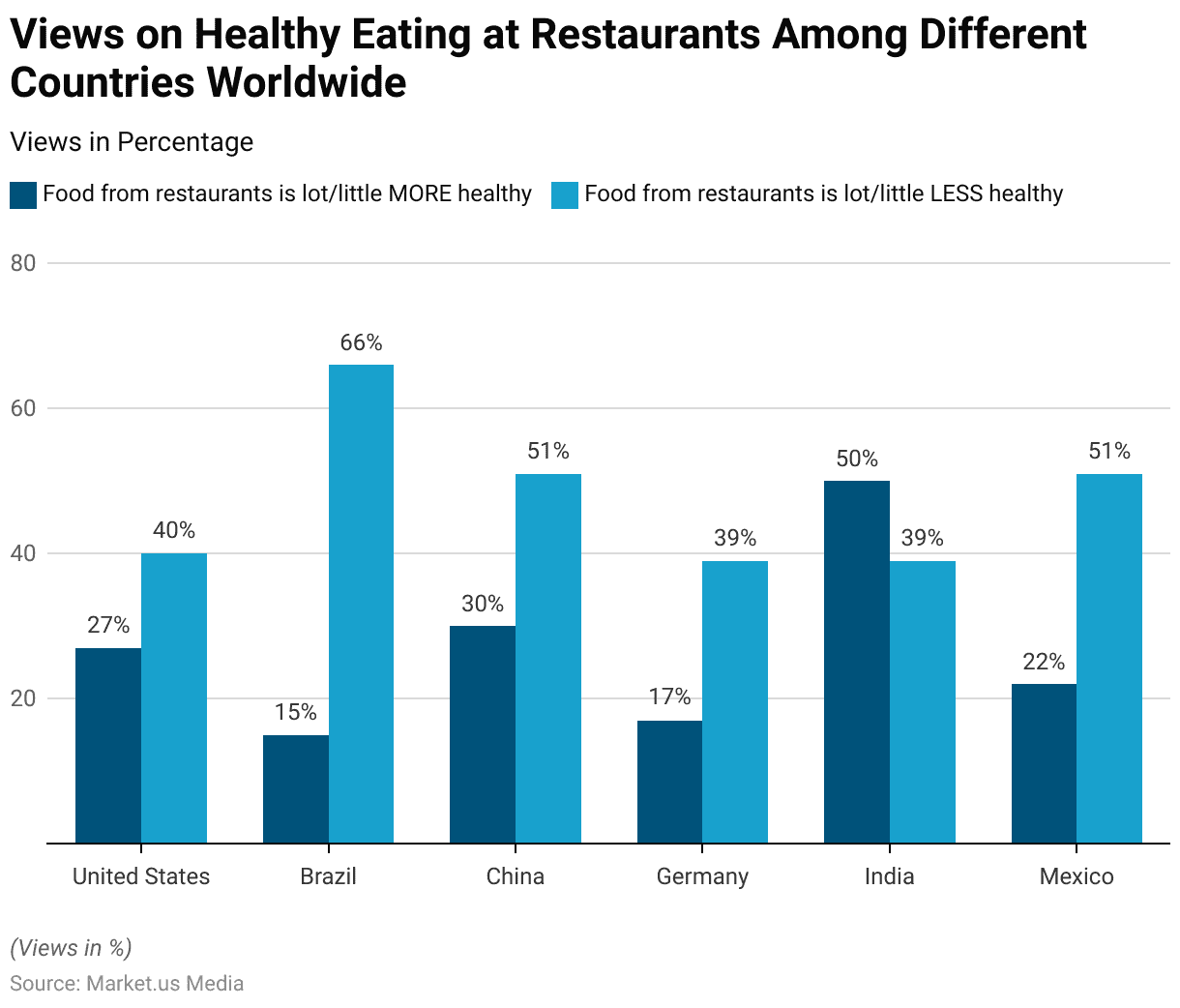

Views on Healthy Eating at Restaurants in Different Countries Worldwide

- In 2021, consumer views on the healthiness of food from restaurants varied across selected countries.

- In the United States, 27% of respondents believed that restaurant food is a lot or a little healthier than other food options, while 40% felt it is a lot or a little less healthy.

- In Brazil, 66% of respondents considered restaurant food to be less healthy, with only 15% viewing it as healthier.

- In China, 30% saw restaurant food as healthier, but 51% viewed it as less healthy.

- Germany exhibited similar trends, with 39% believing restaurant food is less healthy, while only 17% thought it was healthier.

- In India, half of the respondents (50%) felt that restaurant food was healthier, while 39% considered it less healthy.

- In Mexico, 22% believed restaurant food was healthier, and 51% thought it was less healthy.

- These responses indicate regional variations, with some countries perceiving restaurant food as a less healthy choice, while others view it more favorably in terms of health.

(Source: Statista)

Generations Most Likely to Choose Healthy Restaurants

- As of December 2020, U.S. generations displayed different preferences for choosing restaurants based on healthy menu options. Among those who planned to eat on-premises,

- Baby Boomers (ages 56-74) were the most likely to choose such restaurants, with 45% expressing this preference.

- Gen Z adults (ages 18-23) and Millennials (ages 24-39) followed closely, with 36% each planning to dine at restaurants with healthy menu options.

- Gen X (ages 40-45) had a slightly lower inclination, with 30% choosing restaurants for their healthy offerings.

- Regarding takeout or delivery, Gen Z adults were again the most likely to order from restaurants with healthy menus at 44%, followed by Baby Boomers at 39%.

- Millennials and Gen X showed less interest in takeout from healthy restaurants, at 29% and 31%, respectively.

- Overall, 38% of all customers in the U.S. planned to dine at restaurants offering healthy options on-site, while 33% intended to order takeout or delivery.

(Source: Statista)

Fast Food Preferences

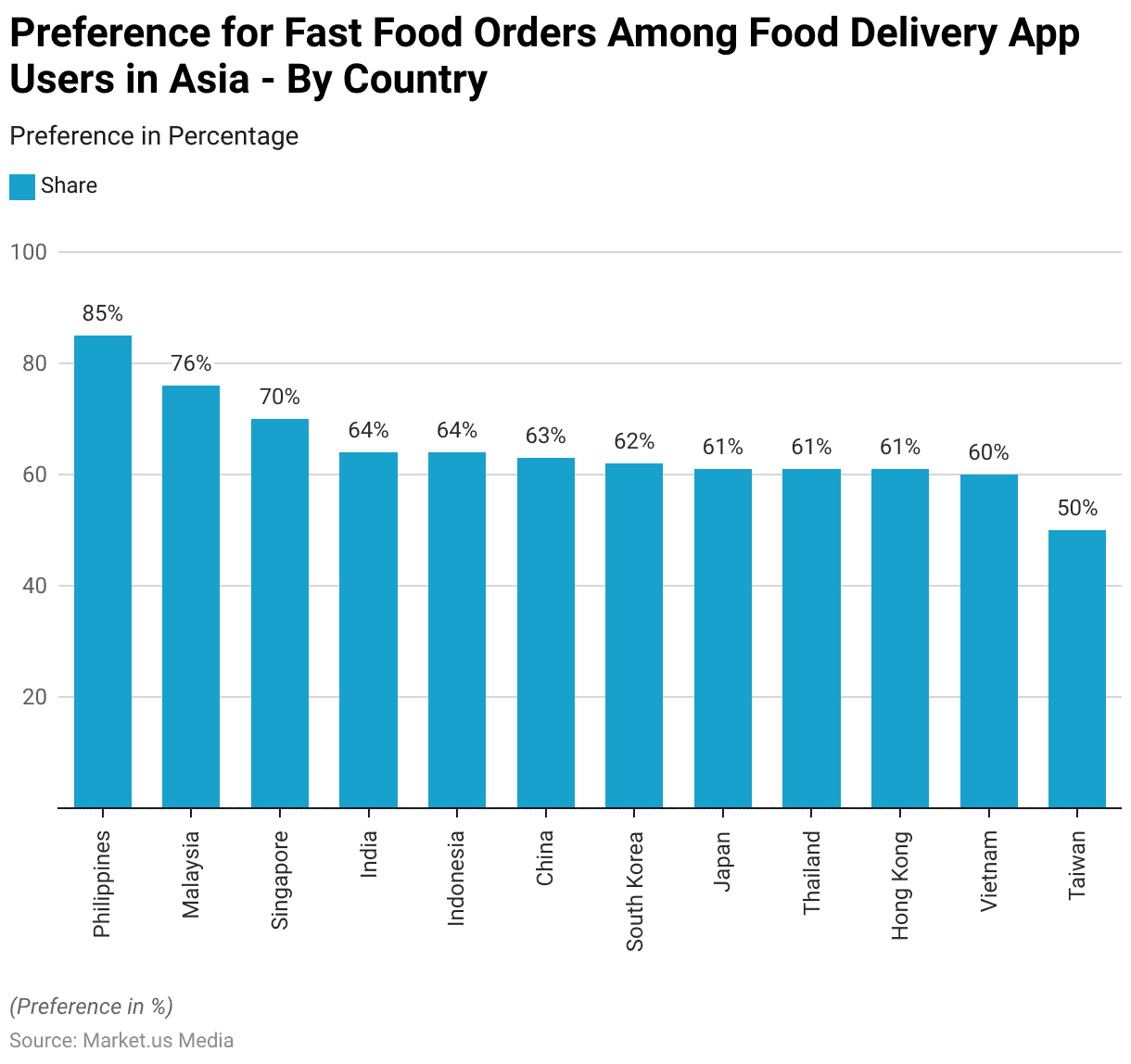

Preference for Fast Food Orders Among Food Delivery App Users

- As of April 2023, the share of consumers in Asia who typically order fast food through food delivery apps varied by country.

- The Philippines had the highest proportion, with 85% of consumers using delivery apps for fast food.

- Malaysia followed with 76%, while Singapore recorded 70%.

- In India and Indonesia, 64% of consumers commonly ordered fast food through such apps.

- China had a similar trend, with 63% of consumers engaging in this behavior, followed closely by South Korea (62%) and Japan (61%).

- Thailand, Hong Kong, and Vietnam also showed notable figures, with 61% of consumers ordering fast food, while Taiwan had the lowest share at 50%.

(Source: Statista)

Frequency of Ordering from Quick Service Restaurants – By Restaurant Type

- As of the first quarter of 2023, the frequency of ordering from quick-service restaurants (QSRs) in the United States varied by restaurant type.

- Coffee and snacks had the highest percentage of consumers ordering more than once a week, at 38%, followed by Tex-Mex (32%) and sandwiches (26%).

- For once-a-week orders, burgers led with 29%, closely followed by chicken (28%) and pizza (28%).

- Orders occurring once every couple of weeks were most common for pizza (31%) and burgers (29%), with chicken (24%) and sandwiches (26%) also showing strong figures.

- For once-a-month orders, chicken (27%) and pizza (31%) were the top choices, while coffee and snacks (15%) and sandwiches (18%) had lower shares in this category.

(Source: Statista)

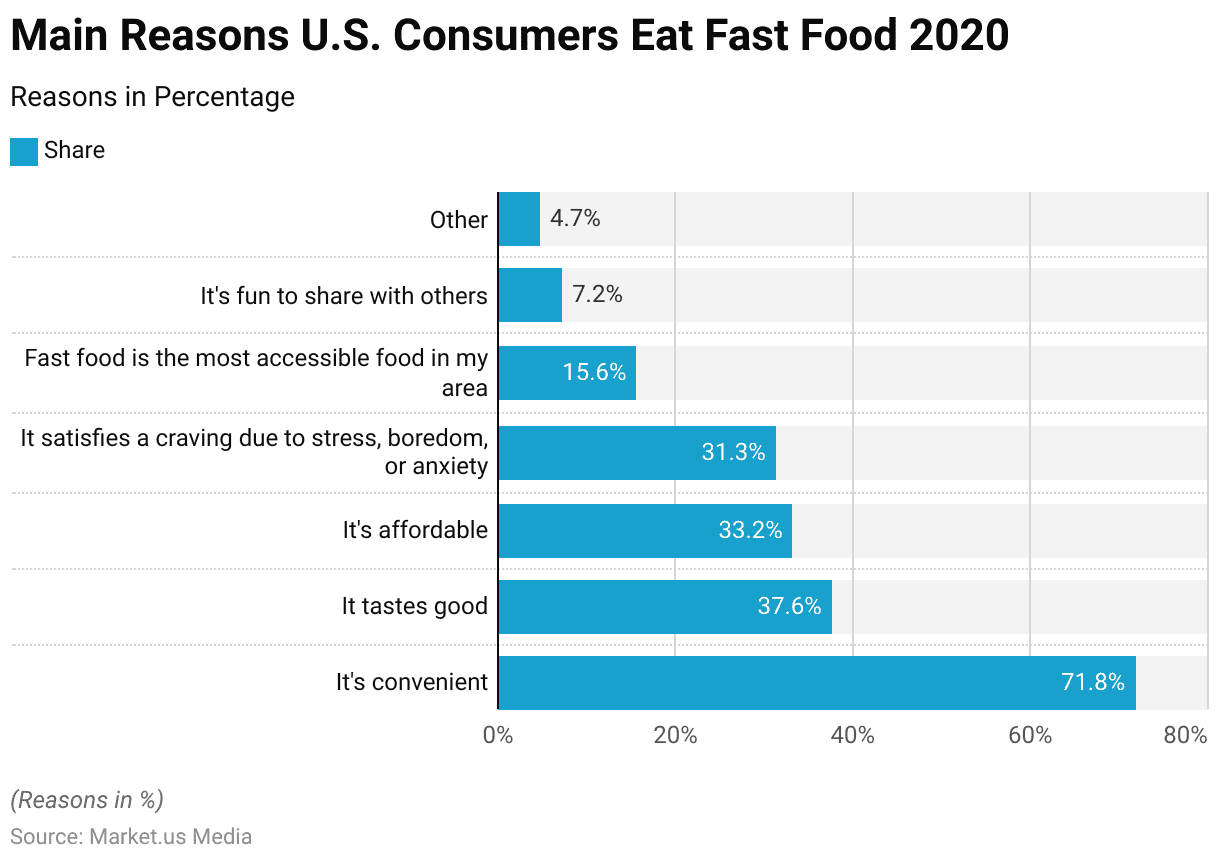

Leading Reasons Consumers Eat Fast Food

- As of November 2020, the leading reasons consumers in the United States eat fast food were primarily driven by convenience, with 71.8% of respondents citing it as a key factor.

- Taste was the second most significant reason, mentioned by 37.6% of consumers, while affordability was important for 33.2%.

- Additionally, 31.3% of respondents indicated that they turn to fast food to satisfy cravings stemming from stress, boredom, or anxiety.

- Access to fast food was a key factor for 15.6% of respondents, as it was considered the most accessible food in their area.

- Sharing fast food with others was noted by 7.2%, while 4.7% gave other reasons for their fast food consumption.

(Source: Statista)

Worldwide Sales of Organic Food

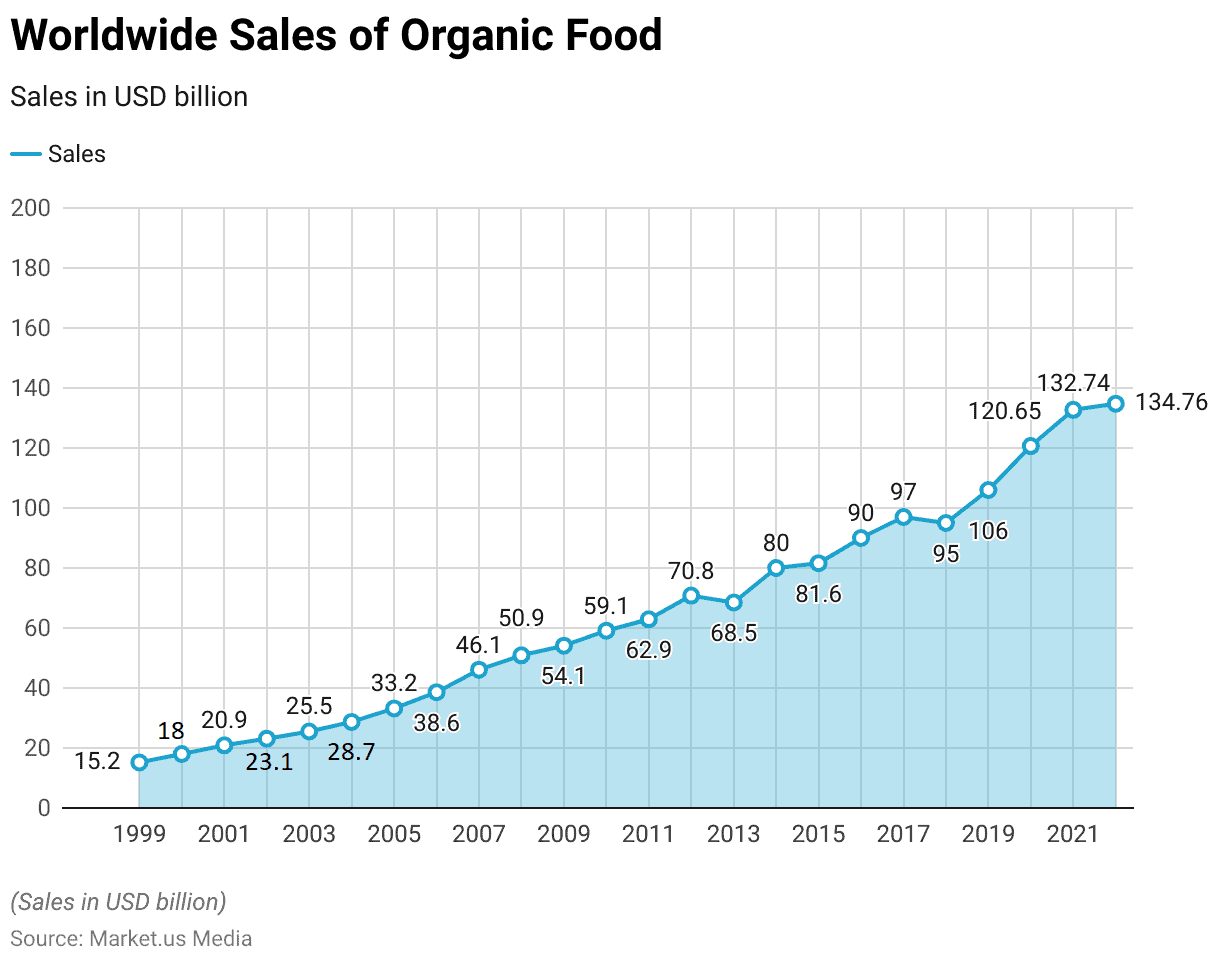

- The global sales of organic food have witnessed substantial growth from 1999 to 2022.

- In 1999, the market was valued at approximately USD 15.2 billion, and this figure steadily increased year on year.

- By 2000, sales had risen to USD 18 billion, and by 2005, it reached USD 33.2 billion.

- The upward trajectory continued, with sales surpassing USD 50 billion in 2008 and USD 60 billion by 2010.

- The market’s growth accelerated further, reaching USD 80 billion in 2014 and USD 90 billion by 2016.

- In 2019, global sales crossed USD 100 billion, reaching USD 106 billion.

- The trend continued into the 2020s, with the market reaching USD 120.65 billion in 2020 and USD 132.74 billion in 2021.

- By 2022, worldwide organic food sales had peaked at USD 134.76 billion.

- This steady increase reflects the growing consumer demand for organic products over the past two decades.

(Source: Statista)

Healthy Food Purchase Preferences

Purchase Location of Healthy Food and Drink Products

- In 2015, the majority of consumers in Europe purchased healthy food and drink products from supermarkets, with 82% of respondents indicating this as their primary purchase location.

- Grocery stores followed with 43%, while 17% reported buying from health food stores.

- Additionally, 16% of consumers made their purchases through online marketplaces, and 15% bought from regional farms or local sources.

- Drug stores accounted for 7% of the purchases.

(Source: Statista)

Reasons for Sustainable and Health Frozen Food Purchases

- In the United States, the reasons for purchasing sustainable and healthy frozen foods remained relatively consistent between October 2022 and October 2023.

- The most common claim driving purchases was “all natural/organic,” which accounted for 11.4% of respondents in October 2022 and slightly decreased to 11% in October 2023.

- The claim of “non-GMO ingredients” was cited by 7.4% of consumers in October 2022, falling to 6.4% the following year.

- “Gluten-free” products saw a decrease from 5.3% in October 2022 to 4.2% in October 2023.

- Consumers also considered the environmental responsibility of brands, with 3.6% of respondents in October 2022 and 3.3% in October 2023 citing this factor.

- Interestingly, the percentage of respondents who valued a “socially responsible brand” increased from 2.3% in October 2022 to 3.3% in October 2023.

(Source: Statista)

Health Functional Food Shopping Frequency Per Year

- In South Korea, the annual frequency of healthy functional food purchases varied among consumers as of July 2022.

- A significant portion of respondents, 42.6%, reported purchasing healthy, functional foods 3 to 4 times a year.

- This was followed by 23.8% who bought them 5 to 6 times annually.

- A smaller group, 16.9%, made such purchases 1 to 2 times per year.

- Additionally, 8.3% of respondents purchased healthy functional foods 7 to 8 times annually, while 5.1% bought them 11 times a year.

- Fewer consumers, 3.4%, reported purchasing them 9 to 10 times per year.

(Source: Statista)

Frequency of Health Functional Food Purchases

- As of February 2023, the frequency of healthy functional food purchases in South Korea varied among consumers.

- Approximately 10% of respondents purchased such products once a month or more.

- A larger share, 24%, bought them once every two months, while 36% made their purchases once every three months.

- Additionally, 23% of respondents bought healthy, functional foods once every six months, and 6% purchased them once a year.

- Only 2% reported purchasing these products less than once a year.

(Source: Statista)

Healthy Food Shopping Frequency Among Consumers – By Education

- In the United States, in 2018, the frequency of looking for healthy food options while shopping varied according to education level.

- Among respondents with less than a college education, 35% reported actively seeking healthy options.

- This number increased to 47% for those with a college degree and further rose to 54% among individuals with a graduate education.

(Source: Statista)

Adoption of Dieting

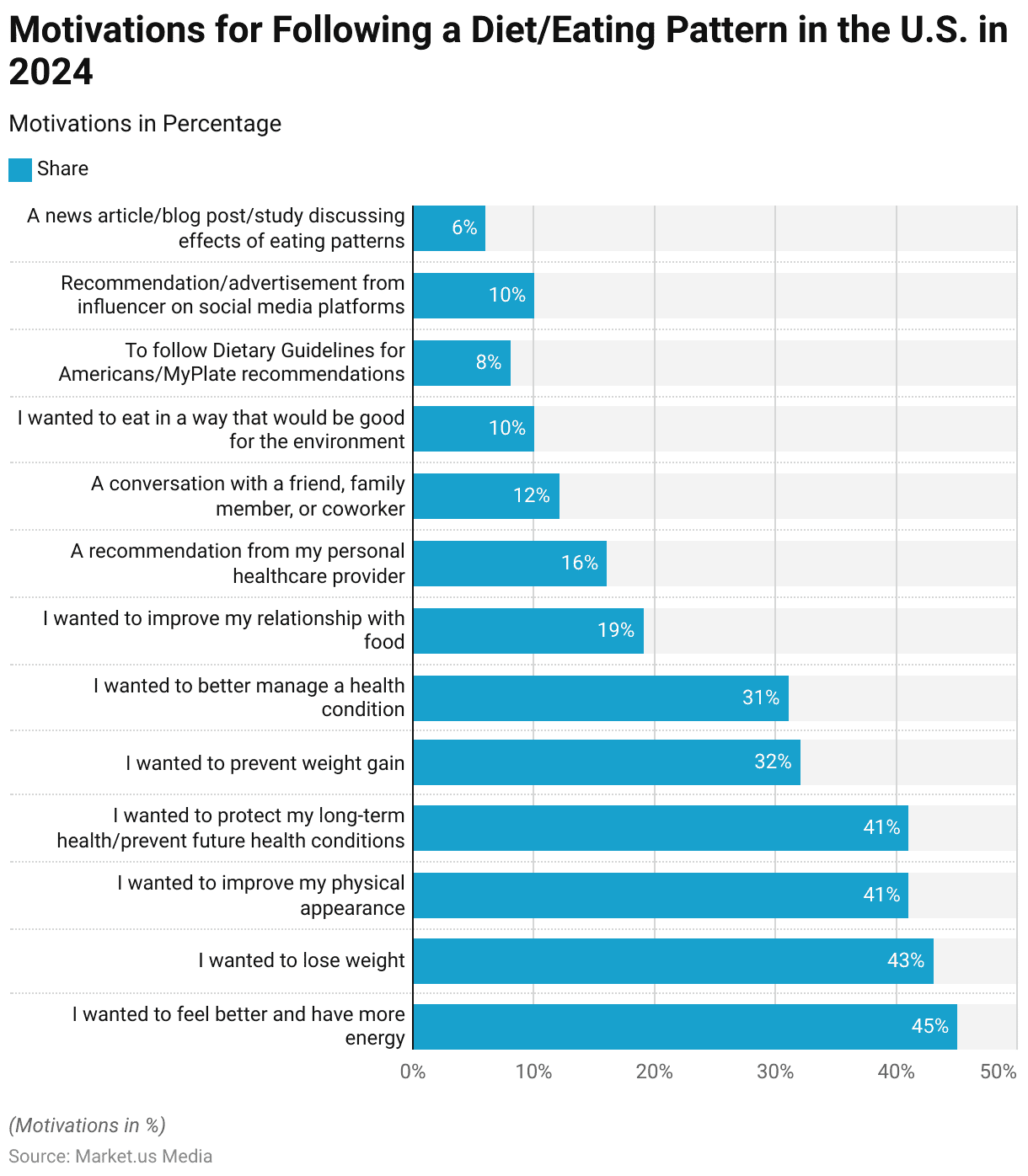

Motivations for Following a Diet or an Eating Pattern

- In the United States, the motivations for following a diet or eating pattern in 2024 were driven by a range of health and personal goals.

- The most common reason, cited by 45% of respondents, was the desire to feel better and have more energy.

- This was closely followed by the aim to lose weight, with 43% of respondents indicating this as a key motivation.

- Additionally, 41% of individuals sought to improve their physical appearance or protect their long-term health and prevent future health conditions.

- A further 32% followed diets to prevent weight gain, while 31% aimed to manage a health condition better.

- Some respondents were motivated by emotional factors, with 19% wanting to improve their relationship with food.

- Recommendations from personal healthcare providers influenced 16% of respondents, and conversations inspired 12% with friends, family, or co-workers.

- Environmental considerations also played a role, with 10% of people seeking diets that they felt were good for the environment.

- Following official guidelines, such as the Dietary Guidelines for Americans or MyPlate recommendations, was a motivation for 8%, while recommendations from social media influencers influenced 10%.

- Finally, 6% of respondents were motivated by news articles, blog posts, or studies discussing the effects of eating patterns.

(Source: Statista)

Factors that Encourage Consumer Adoption of Vegan or Vegetarian Diets

- In the United Kingdom in 2023, various factors encouraged consumers to adopt a vegan or vegetarian diet, with some differences between male and female respondents.

- Among females, 24% were motivated by general health reasons, while environmental concerns drove 19%, and 24% were influenced by concerns over animal welfare.

- Additionally, 19% of female respondents cited worries about health risks related to meat or fish production, such as bacterial infections or food poisoning, as a motivating factor.

- Another 19% wanted to eat more cheaply, while 17% were concerned about the healthiness of processed meat products.

- On the other hand, 8% of female respondents indicated that they were already vegan or vegetarian, and 5% mentioned other reasons for considering the diet.

- Among male respondents, the motivations were somewhat similar, with 19% citing general health reasons and 18% concerned about environmental factors.

- Male respondents were also less likely than females to be motivated by concerns over animal welfare (17% vs. 24%) or health risks related to meat production (16% vs. 19%).

- A similar proportion of males (16%) were motivated by the desire to eat more cheaply, and 14% were concerned about the healthiness of processed meat products.

- Just 7% of male respondents were already vegan or vegetarian, and 7% cited other reasons.

- Lastly, 6% of female respondents and 4% of male respondents were concerned about the accuracy of meat and fish labeling.

(Source: Statista)

Adoption Level of Restrictive Diet

- In Chile, as of August 2017, various restrictive diets were adopted to differing extents.

- The low-sugar diet had the highest adoption rate, with 52% of respondents following it sometimes and 35% adhering to it always.

- A significant proportion of respondents also adopted a low-fat diet, with 60% following it sometimes and 24% always.

- The low sodium diet had a similar adoption pattern, with 49% of respondents sometimes following it and 24% always doing so.

- Less commonly, 25% of individuals followed a lactose-free diet sometimes, and 13% always, while 23% replaced traditional dairy products with vegetable milk (such as soy) sometimes, with only 7% doing so always.

- The gluten-free diet had a lower adoption rate, with 24% following it sometimes and just 3% always, while the vegetarian diet was the least adopted, with 37% occasionally following it and only 3% adhering to it always.

(Source: Statista)

Interest in Healthy Eating and Lifestyle

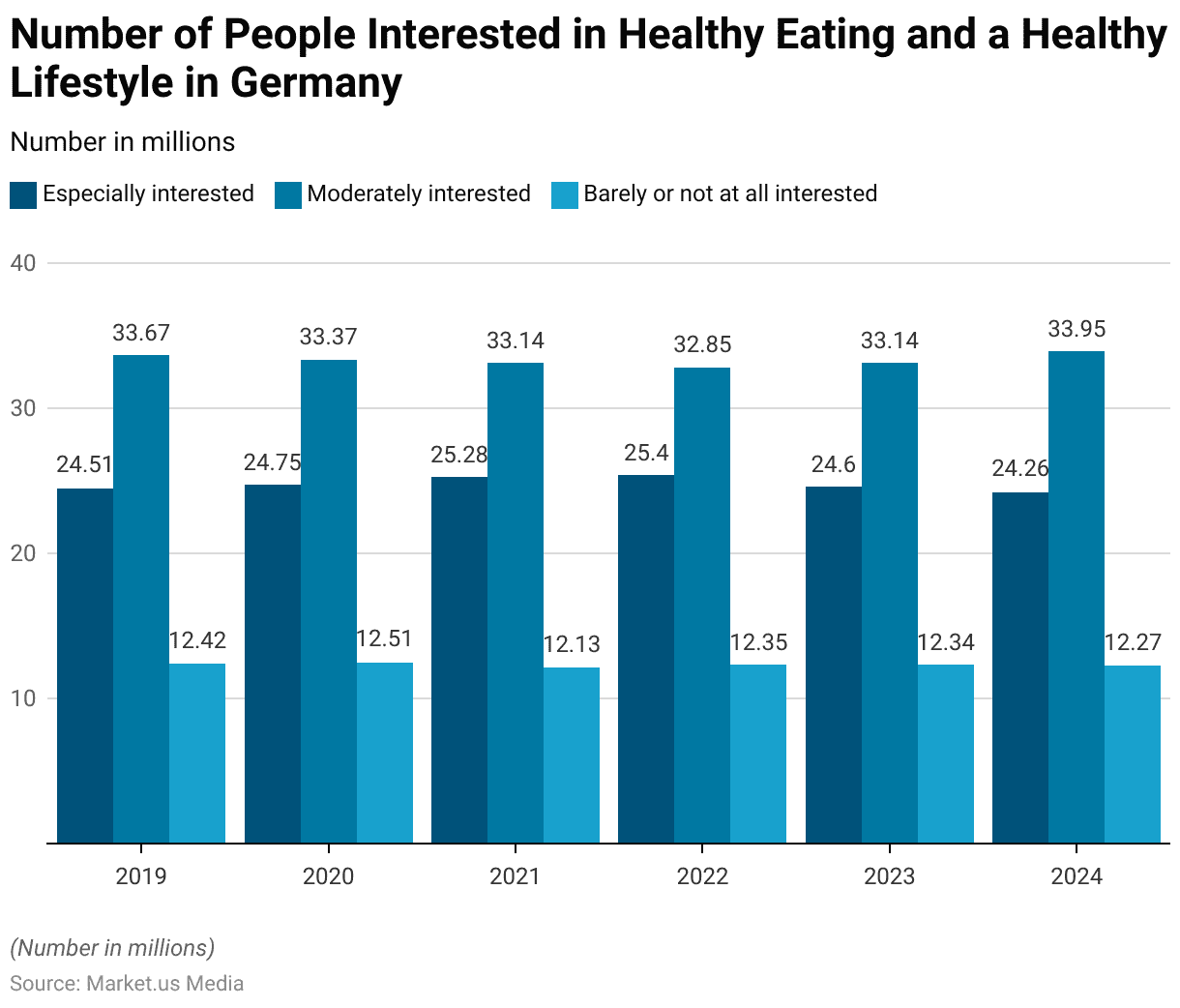

- From 2019 to 2024, the number of people in Germany interested in healthy eating and a healthy lifestyle remained relatively stable.

- In 2019, 24.51 million individuals were especially interested, 33.67 million were moderately interested, and 12.42 million were barely or not at all interested.

- The following year, in 2020, the numbers were similar, with 24.75 million especially interested, 33.37 million moderately interested, and 12.51 million barely or not at all interested.

- By 2021, the number of people especially interested increased slightly to 25.28 million, while the number moderately interested declined to 33.14 million, and those barely or not at all interested decreased to 12.13 million.

- In 2022, the number of those especially interested increased slightly again to 25.4 million, while the number moderately interested dropped to 32.85 million, and the number barely or not at all interested rose to 12.35 million.

- In 2023, the trend continued with 24.6 million especially interested, 33.14 million moderately interested, and 12.34 million barely or not at all interested.

- By 2024, the number of people especially interested declined to 24.26 million, while those moderately interested rose to 33.95 million, and those barely or not at all interested remained at 12.27 million.

(Source: Statista)

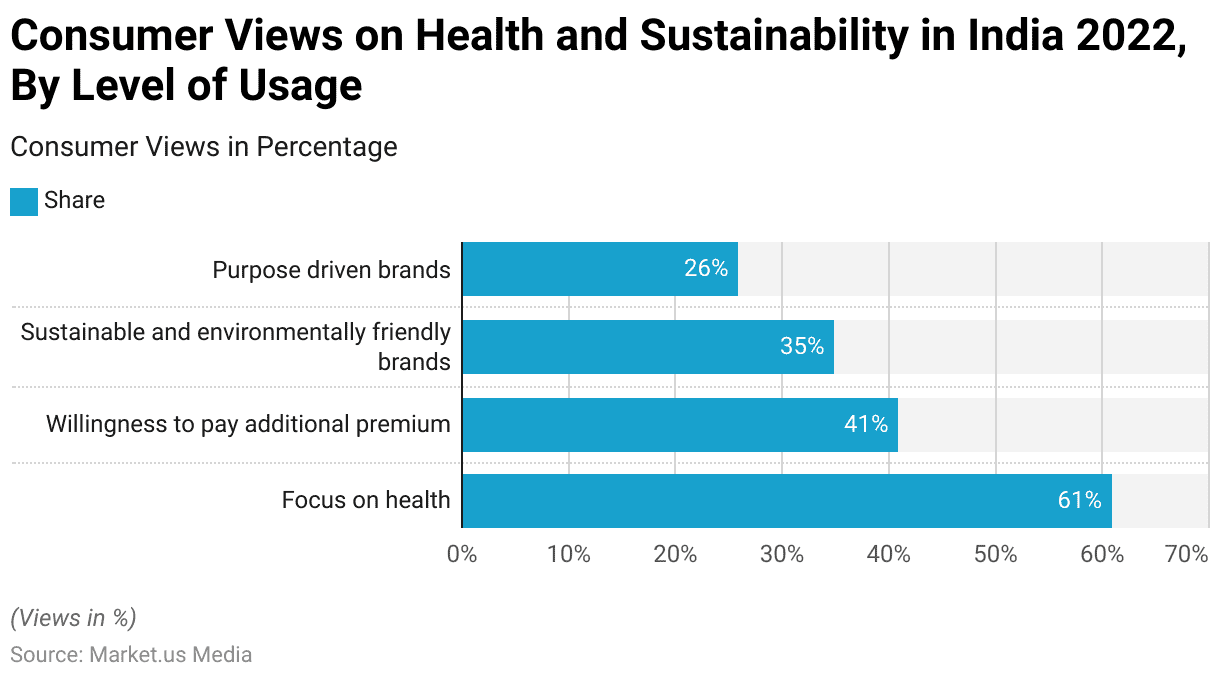

Consumer Views on Health and Sustainability – By Level of Usage

- As of August 2022, consumer views on health and sustainability in India revealed a strong focus on health, with 61% of respondents prioritizing it.

- Additionally, 41% of respondents expressed a willingness to pay a premium for products that align with their health and sustainability values.

- Sustainable and environmentally friendly brands were supported by 35% of consumers, while 26% preferred purpose-driven brands that align with specific social or environmental goals.

(Source: Statista)

Cost of a Healthy Diet in Various Nations and Regions

India

- From 2017 to 2022, the cost of a healthy diet in India gradually increased.

- In 2017, the cost was $2.86 per person per day, and by 2018, it slightly rose to $2.87.

- This upward trend continued in 2019, with the cost reaching $2.92.

- In 2020, it increased further to $3.01, followed by a rise to $3.11 in 2021.

- By 2022, the cost of a healthy diet had risen to $3.36 per person per day.

(Source: Statista)

Japan

- From 2017 to 2021, the cost of a healthy diet per person per day in Japan remained relatively stable.

- In 2017, the cost was $5.53 in PPP dollars, and it slightly increased to $5.7 in 2018.

- In 2019, the cost decreased slightly to $5.57 but then rose again to $5.65 in 2020.

- By 2021, the cost was $5.64, indicating a small fluctuation but no significant changes over the five years.

(Source: Statista)

China

- From 2017 to 2021, the cost of a healthy diet per person per day in China showed slight fluctuations but remained relatively stable.

- In 2017, the cost was $5.53 in PPP dollars, which increased to $5.7 in 2018.

- In 2019, it slightly decreased to $5.57, followed by a modest rise to $5.65 in 2020.

- By 2021, the cost remained almost unchanged at $5.64, showing only a minor decline over the five years.

(Source: Statista)

Hong Kong

- From 2017 to 2021, the cost of a healthy diet per person per day in Hong Kong steadily increased.

- In 2017, the cost was $3.66 in PPP dollars, which rose to $3.82 in 2018.

- The upward trend continued in 2019 with a significant increase to $4.15, followed by a further rise to $4.51 in 2020.

- By 2021, the cost reached $4.72, marking a consistent annual increase over the five years.

(Source: Statista)

Latin America and the Caribbean

- From 2017 to 2022, the cost of a healthy diet per person per day in Latin America and the Caribbean showed a consistent upward trend.

- In 2017, the cost was $3.62 in PPP dollars, which slightly increased to $3.69 in 2018.

- The cost continued to rise, reaching $3.78 in 2019 and $3.88 in 2020.

- By 2021, the cost had risen further to $4.08, and in 2022, it reached $4.56, reflecting a steady annual increase over the six years.

(Source: Statista)

Key Spending Statistics

Spending on Health and Functional Foods

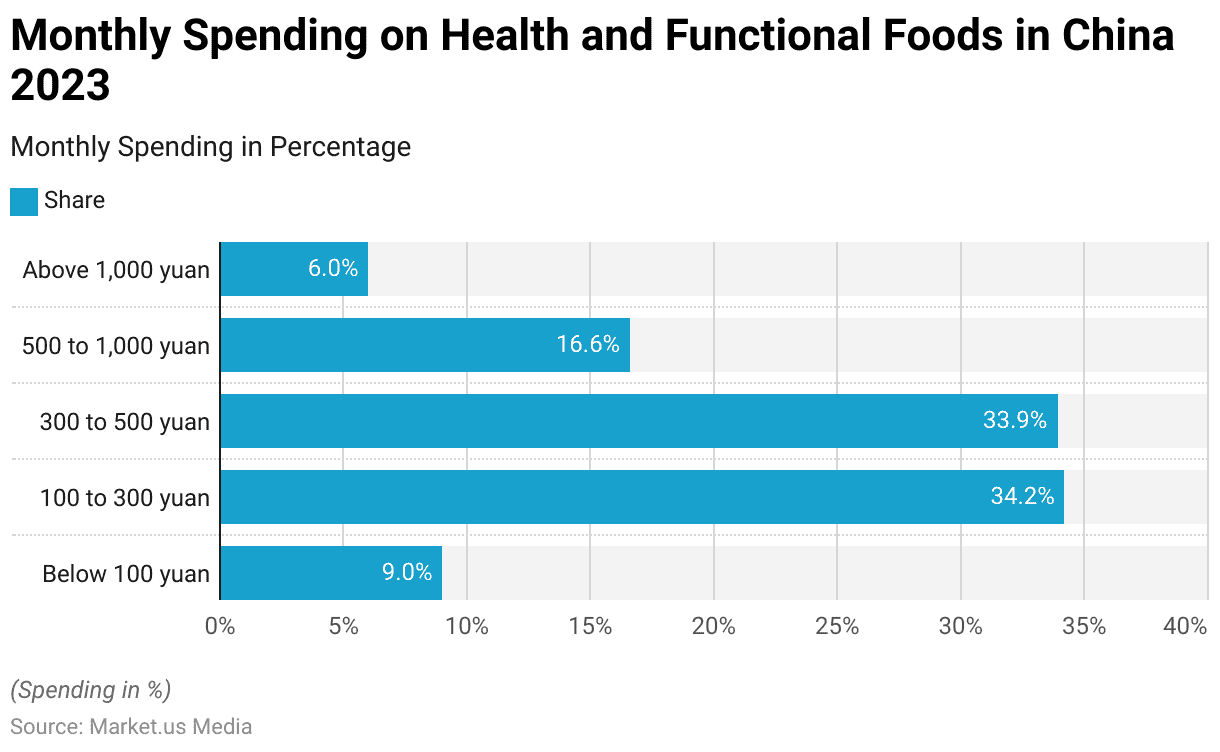

- As of February 2023, the distribution of monthly spending on health and functional food products in China revealed varying spending habits.

- A significant portion of respondents, 34.2%, spent between 100 to 300 yuan, followed closely by 33.9% who spent between 300 to 500 yuan.

- Additionally, 16.6% of respondents allocated between 500 to 1,000 yuan, while 9% spent less than 100 yuan.

- Only a smaller group, 6%, reported spending above 1,000 yuan on these products each month.

(Source: Statista)

Willingness to Spend Money on Good Food

- From 2019 to 2023, the number of people in Germany with a high willingness to spend money on a good diet and quality food showed a gradual decline.

- In 2019, the figure stood at 39.05 million, slightly increasing to 39.15 million in 2020.

- However, this number decreased over the following years, with 38.17 million in 2021, 37.49 million in 2022, and reaching 36.68 million in 2023.

(Source: Statista)

Nutrition Spending Per Household – By Degree of Urbanization

- From 2016 to 2020, the monthly expenditure per household on nutrition products in Vietnam varied between urban and rural areas.

- In urban areas, the expenditure ranged from 467,000 Vietnamese dong in 2016 to 468,000 dong in 2020, showing a steady trend.

- Meanwhile, rural households initially spent 50,000 dong in 2016, which gradually increased over the years, reaching 266,000 dong by 2020.

- The gap between urban and rural expenditure on nutrition products widened as the years progressed, reflecting the increasing consumption of nutrition products in rural areas, though urban areas consistently spent more.

(Source: Statista)

Funding for Nutrition Research

- From FY 2013 to FY 2025, the National Institutes for Health (NIH) allocated increasing funding for nutrition research.

- The funding began at 1.524 billion U.S. dollars in 2013 and steadily rose each year, reaching 2.301 billion U.S. dollars in 2025.

- The most notable growth occurred from 2013 to 2020, with funding surpassing the two billion-dollar mark in 2020.

- In 2023, the funding reached 2.231 billion dollars, a slight increase from the previous year.

- The allocation has remained relatively stable, with a small dip projected in 2024 to 2.224 billion dollars before rising again in 2025.

- This trend highlights a consistent commitment to advancing nutrition research.

(Source: Statista)

Regulations for Different Health and Functional Foods

- Regulations for health and functional foods vary significantly across countries, reflecting diverse approaches to ensuring consumer safety and product efficacy.

- In the United States, the Food and Drug Administration (FDA) oversees dietary supplements under the Dietary Supplement Health and Education Act of 1994, which requires manufacturers to ensure product safety and proper labeling but does not mandate pre-market approval.

- The European Union enforces the Food Supplements Directive 2002/46/EC, mandating that supplements be proven safe in both dosage and purity before market entry.

- Japan‘s system includes Foods for Specified Health Uses (FOSHU), where products must undergo rigorous evaluation and approval by the Consumer Affairs Agency to bear health claims.

- In India, the Food Safety and Standards Authority of India (FSSAI) regulates health supplements and nutraceuticals under the Food Safety and Standards (Health Supplements, Nutraceuticals, Food for Special Dietary Use, Food for Special Medical Purpose, Functional Food, and Novel Food) Regulations, 2016, requiring product approval and adherence to specified standards.

- These regulatory frameworks aim to protect consumers by ensuring that healthy and functional foods are safe, accurately labeled, and their health claims substantiated.

(Sources: U.S. Senate, EU, FOSHU, FSSAI)

Recent Developments

Acquisitions and Mergers:

- Unilever Acquires The Vegetarian Butcher (2023): Unilever acquired The Vegetarian Butcher for an undisclosed amount to expand its plant-based product portfolio. The company aims to strengthen its position in the growing health-conscious consumer segment, where plant-based food demand is rising.

- Nestlé Acquires the AI-Powered Health Tech Firm (2024): In a bid to integrate health-conscious tech solutions into its portfolio, Nestlé acquired a health technology firm, which uses AI to personalize nutrition and wellness plans. This move highlights Nestlé’s focus on integrating technology with food offerings to cater to health-conscious consumers, especially in the wake of the rising trend in personalized nutrition.

Product Launches

- Coca-Cola’s New Line of Health-Oriented Beverages (2023): Coca-Cola launched a new product line called “Coca-Cola with Nutrients” which includes beverages enriched with vitamins, minerals, and electrolytes to appeal to health-conscious consumers. The company invested $100 million in developing these health-conscious beverages, targeting the growing demand for functional drinks.

- PepsiCo’s Launch of Plant-Based Snacks (2024): PepsiCo introduced a line of plant-based snacks under the “Off the Eaten Path” brand. This launch is aligned with consumer preferences for clean-label, healthy, and sustainable snack options, responding to the 18% annual growth of the plant-based food market globally.

Funding and Investments:

- Impossible Foods Raises $200 Million (2024): Impossible Foods, known for its plant-based meat products, raised $200 million in Series G funding in 2024 to expand its offerings and market presence. The company plans to use the funds to scale production and enhance consumer education on plant-based eating, aiming to tap into the growing number of health-conscious individuals seeking sustainable food options.

- MycoTechnology’s $75 Million Investment (2024): MycoTechnology, a company specializing in edible fungi-based products, raised $75 million in a Series D round to boost production of its plant-based protein alternatives. The company plans to use the investment to expand product lines that cater to the health-conscious consumer seeking alternatives to traditional protein sources.

Conclusion

Health Conscious Consumer Statistics – The rise of health-conscious consumers is reshaping global purchasing behaviors, with individuals increasingly prioritizing natural, organic, and sustainable products.

Driven by a growing awareness of the link between diet and well-being, consumers are willing to pay more for healthier food options, as seen in the rising costs of healthy diets and increased nutrition research funding.

This trend is evident across regions, influencing food industries to offer more health-focused and sustainable choices.

As consumers demand better-for-you products, the health-conscious shift is expected to continue driving innovation and influencing market dynamics worldwide.

FAQs

A health-conscious consumer actively seeks out products and services that contribute to physical and mental well-being, with a focus on natural, organic, and sustainable options. They prioritize health benefits and often choose food and lifestyle products based on their nutritional value, environmental impact, and ethical considerations.

Health-conscious consumers are driving the demand for healthier, organic, and sustainable food options. They are prompting companies to innovate by offering products with cleaner ingredients, fewer additives, and environmentally friendly packaging. This trend is also leading to the growth of plant-based, gluten-free, and non-GMO foods.

Yes, studies show that a significant portion of health-conscious consumers are willing to pay a premium for products they perceive as healthier, more natural, or sustainable. This includes organic foods, functional foods, and products with transparent ingredient sourcing.

The main drivers include increased awareness of the connection between diet and long-term health, growing concerns over environmental sustainability, and the rise of chronic diseases linked to poor eating habits. Social media and influencers also play a significant role in shaping consumer preferences.

Sustainability is increasingly important to health-conscious consumers. Many seek products from brands that promote environmental responsibility and ethical sourcing, such as those offering plant-based foods or eco-friendly packaging. This trend also extends to choosing companies that prioritize animal welfare and carbon footprint reduction.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)