Introduction

Glucose Biosensors Statistics: Glucose biosensors play a vital role in the healthcare sector, particularly in the monitoring and regulation of diabetes.

Utilizing advanced biotechnological principles, these tools identify and measure glucose levels in biological samples.

Typically including a bioreceptor, transducer, and electronic system for signal processing, glucose biosensors find varied uses in home glucose monitoring devices, continuous glucose monitoring systems, and clinical environments.

Their versatility extends to different sectors like healthcare, food and beverages, and research laboratories.

While the market for glucose biosensors is flourishing, challenges such as accuracy concerns and the need for continuous innovation persist.

Editor’s Choice

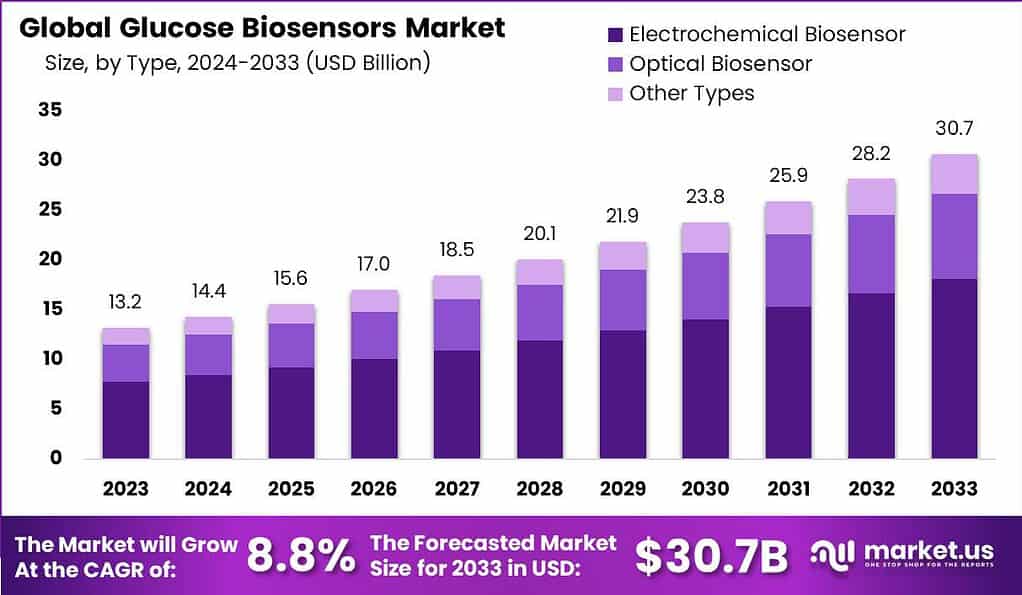

- The glucose biosensors market has exhibited robust growth over the past decade at a CAGR of 7.6 %.

- In 2023, the glucose biosensors market revenue stood at USD 24.64 billion.

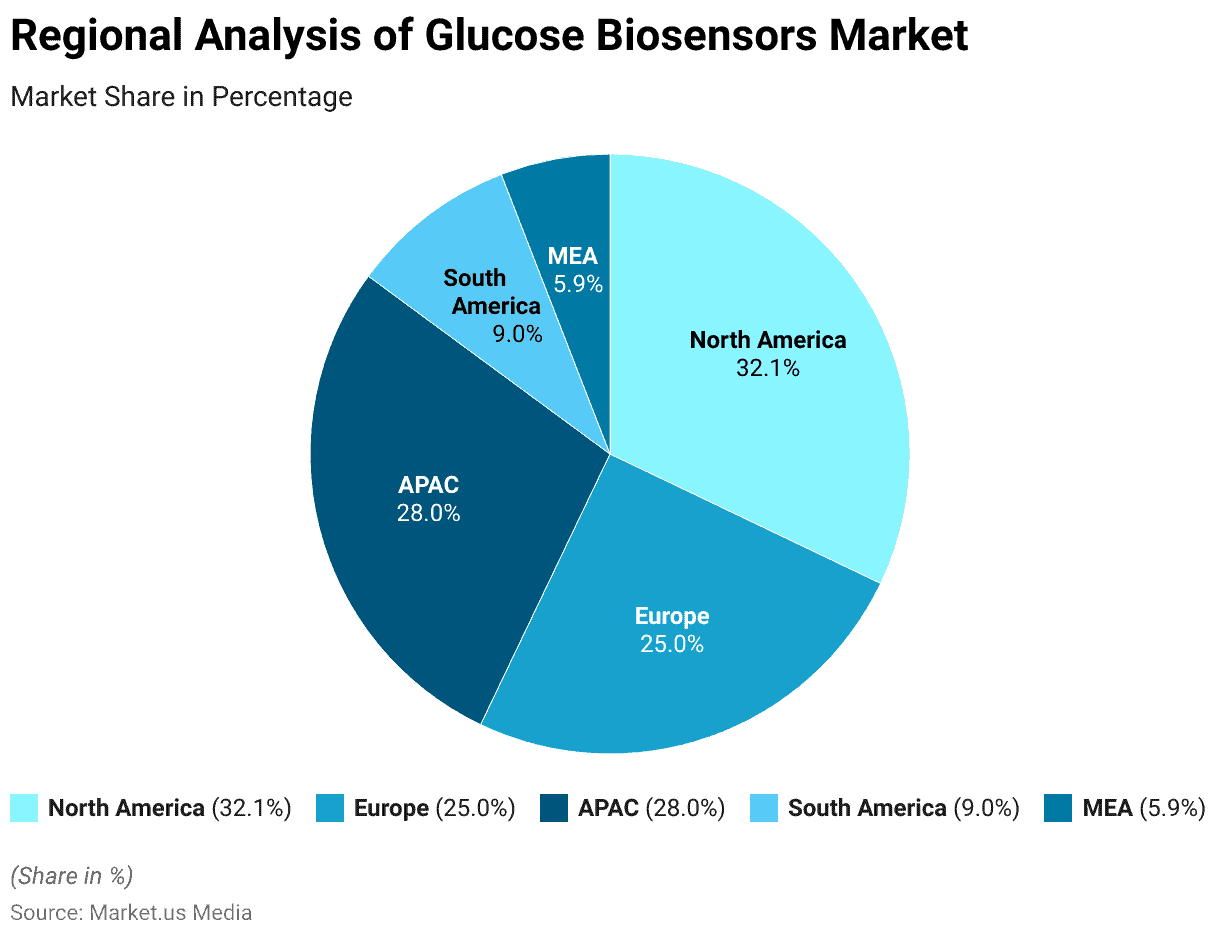

- North America stands out as a major player, commanding a substantial 32.1% share.

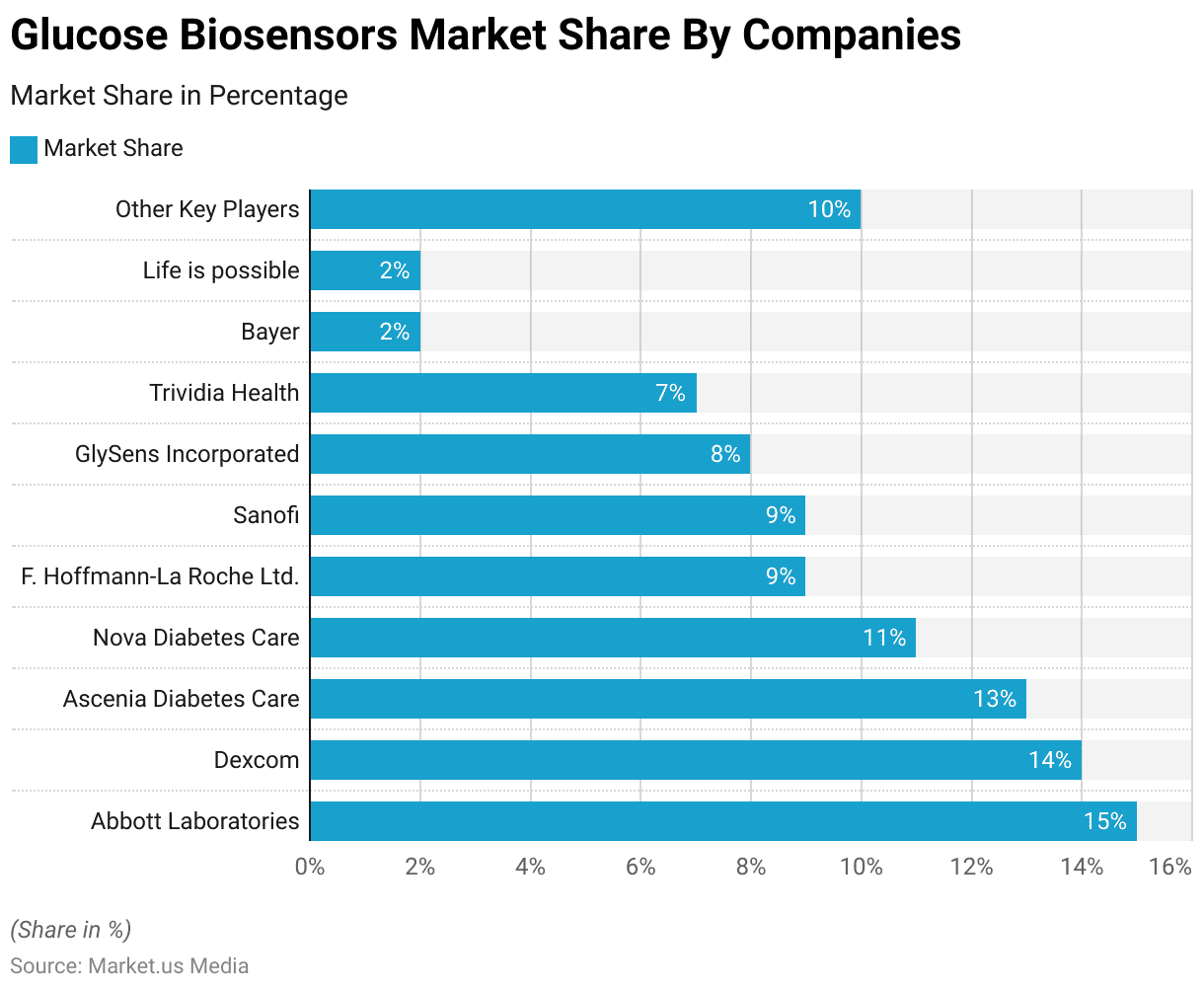

- Abbott Laboratories leads with a notable market share of 15%, showcasing its significant presence and influence in the sector.

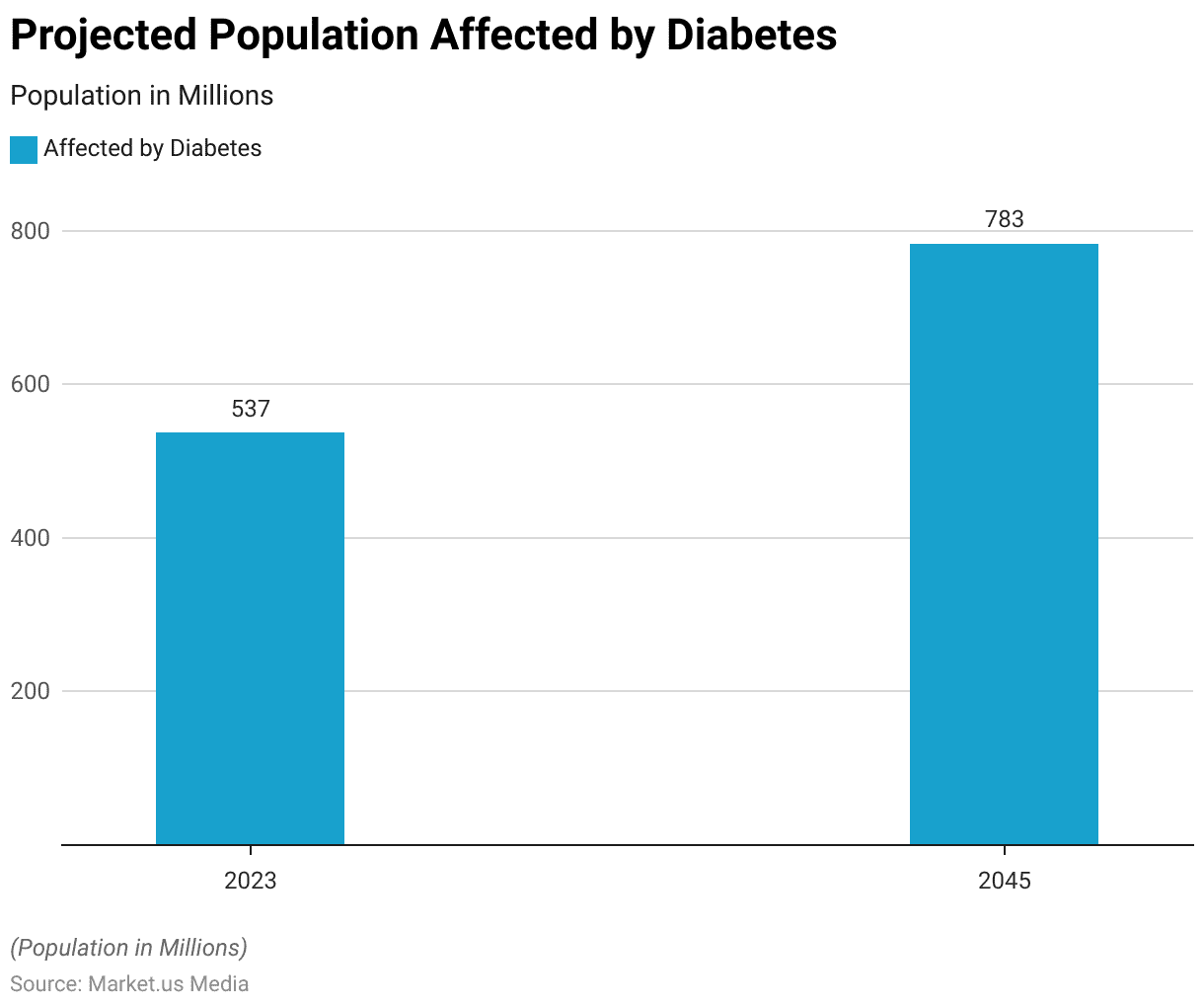

- Presently, an estimated 537 million individuals worldwide are affected by diabetes.

- The commercial market gained momentum with the launch of the MediSense ExacTech blood glucose biosensor in 1987.

- Notable corporate developments include Abbott’s acquisition of MediSense for $867 million in 1996 and LifeScan’s purchase of Inverness Medical’s glucose testing business for $1.3 billion in 2001.

Global Glucose Biosensors Market Statistics

Global Glucose Biosensors Market Size

- The glucose biosensors market has exhibited robust growth over the past decade at a CAGR of 7.6 %, with a significant upward trajectory in revenue.

- In 2022, the market revenue stood at USD 17.94 billion, experiencing a substantial increase to USD 24.64 billion in 2023.

- This positive trend continued, reaching USD 31.34 billion in 2024 and escalating further to USD 38.04 billion in 2025.

- The subsequent years witnessed a consistent climb, with the market revenue reaching USD 44.74 billion in 2026, USD 51.44 billion in 2027, and USD 58.14 billion in 2028.

- The upward momentum persisted, surpassing USD 64.84 billion in 2029. USD 71.54 billion in 2030, and USD 78.24 billion in 2031.

- As we look forward, the projected figures indicate sustained growth, with the market anticipated to reach USD 84.94 billion in 2032.

- This impressive expansion underscores the increasing importance and adoption of glucose biosensors in healthcare and related applications, reflecting a dynamic and flourishing market landscape.

(Source: Market.us)

Regional Analysis of Global Glucose Biosensors Market Statistics

- The global market for glucose biosensors is characterized by a distribution of market share across various regions, each contributing uniquely to the overall industry landscape.

- North America stands out as a major player, commanding a substantial 32.1% share.

- This dominance can be attributed to factors such as advanced healthcare infrastructure. Technological innovations, and a high prevalence of diabetes, driving the demand for glucose monitoring solutions.

- In Europe, the market maintains a robust presence, accounting for 25.0% of the total market share. The region’s contribution reflects a combination of well-established healthcare systems. Research and development initiatives, and a growing awareness of the importance of glucose monitoring in managing chronic conditions.

- The Asia-Pacific (APAC) region emerges as a significant player, holding a considerable 28.0% market share.

- This reflects the region’s rising economic prosperity, increasing healthcare investments, and a large population with a growing focus on health and wellness.

- In South America, the market share is noteworthy at 9.0%, indicative of a growing recognition of the value of glucose biosensors in healthcare management.

- The region’s share, though smaller compared to North America and Europe. Suggests a positive trajectory in the adoption of these devices.

- The Middle East and Africa (MEA) region contributes 5.9% to the global market share.

- While comparatively smaller, this share reflects an emerging market with potential growth opportunities. Driven by an increasing focus on healthcare infrastructure development and rising awareness of the importance of glucose monitoring in chronic disease management.

(Source: Market.us)

Key Players in the Global Glucose Biosensors Market Statistics

- The market for glucose biosensors is characterized by a diverse landscape of key players, each contributing to the industry’s dynamics.

- Abbott Laboratories leads with a notable market share of 15%, showcasing its significant presence and influence in the sector.

- Dexcom follows closely, holding a substantial 14% market share, underscoring its prominence in the continuous glucose monitoring segment.

- Ascenia Diabetes Care and Nova Diabetes Care contribute 13% and 11% respectively. Reflecting their strong market positions and contributions to glucose monitoring solutions.

- F. Hoffmann-La Roche Ltd. and Sanofi share a combined 18% market share. Attesting to their considerable influence in the pharmaceutical and healthcare sectors.

- GlySens Incorporated, Trividia Health, Bayer, and Life possibly collectively account for 29%, with each making distinct contributions to the market.

- Notably, other key players contribute 10%, highlighting the overall diversity and competitiveness within the glucose biosensors market.

- This distribution underscores the collaboration and competition among industry leaders and emerging players, driving innovation and advancements in glucose monitoring technologies.

(Source: Market.us)

Factors Driving the Demand for Glucose Biosensors Statistics

- The World Health Organization reported approximately 1.5 million deaths attributed to diabetes in 2019. Presently, an estimated 537 million individuals worldwide are affected by diabetes.

- Projections indicate a significant increase, reaching around 783 million people living with diabetes globally by the year 2045.

- Interestingly, the nations with the highest occurrence of diabetes are concentrated predominantly on the Pacific islands.

- Take, for instance, the Marshall Islands, where approximately 25% of adults are affected by diabetes. In contrast, the prevalence of diabetes in OECD countries is considerably lower.

- However, the United States stands out with figures significantly surpassing the OECD average, reaching an almost 14% prevalence rate.

- In the United States, over 24 million individuals have received a diabetes diagnosis, although the actual number of people living with diabetes is presumed to be higher.

- Notably, a disproportionately large segment of the population in the Southern states of the United States grapples with diabetes.

- Globally, expenditures on healthcare related to diabetes reached an estimated 966 billion U.S. dollars in the year 2021. Notably, the countries with the highest per-patient spending on diabetes are the United States, Switzerland, and Norway.

- Specifically, in 2021, the United States allocated approximately 11,779 U.S. dollars per individual with diabetes.

- Consequently, the treatment of diabetes constitutes a substantial submarket within the pharmaceutical industry.

- Key players in this sector include Novo Nordisk and Sanofi. In 2022, Sanofi’s Lantus, a long-lasting insulin used for diabetes treatment. Emerged as the company’s second-best-selling pharmaceutical product, generating revenue close to 2.3 billion euros.

(Source: Statista)

Timeline of Commercial Glucose Biosensor Development

- The timeline of commercial biosensor development is marked by significant milestones that have shaped the field. In 1916, the first report on protein immobilization showcased the adsorption of invertase on activated charcoal.

- The year 1922 witnessed the introduction of the first glass pH electrode, a fundamental component in biosensor technology.

- A pivotal moment occurred in 1956 with the invention of the oxygen electrode by Clark.

- The subsequent decade saw the emergence of the first biosensor in 1962, described as an amperometric enzyme electrode for glucose by Clark and Lyons.

- The years 1973-75 marked a groundbreaking event with the introduction of the first commercial biosensor by Yellow Springs Instruments for glucose detection.

- The medical landscape witnessed a transformative development in 1976 with the creation of the Miles Biostator, the inaugural bedside artificial pancreas.

- Advancements continued with the introduction of the first fiber optic-based biosensor for glucose in 1982 by Schultz.

- The year 1984 brought forth another breakthrough with the first mediated amperometric glucose biosensor, utilizing ferrocene with glucose oxidase for detection.

- The commercial market gained momentum with the launch of the MediSense ExacTech blood glucose biosensor in 1987.

- Notable corporate developments include Abbott’s acquisition of MediSense for $867 million in 1996 and LifeScan’s purchase of Inverness Medical’s glucose testing business for $1.3 billion in 2001.

- Abbott further strengthened its position by acquiring i-STAT for $392 million in 2003 and TheraSense for $1.2 billion in 2004.

- These events collectively underscore the dynamic evolution and growth of commercial biosensor technology over the decades, playing a crucial role in healthcare diagnostics and monitoring.

(Source: CORE- Open University)

Generations of Glucose Biosensor

First-Generation Glucose Biosensor Statistics

- First-generation enzymatic glucose biosensors utilize H2O2 generation or reduction in oxygen (O2) concentration to measure glucose levels in the sample.

- These biosensors are characterized by a simple design and miniaturization, yet they face challenges.

- The amperometric measurement of H2O2 in first-generation biosensors requires a high operational potential, posing limitations. This elevated potential may lead to interference from electroactive molecules (e.g., ascorbic acid, uric acid) and certain drugs (e.g., acetaminophen).

- Additionally, oxygen solubility limitations in biological fluids may cause oxygen deficiency, impacting sensor response and narrowing the linearity of glucose concentration detection ranges.

- Despite their advantages, first-generation glucose biosensors exhibit constraints related to operational potential and oxygen deficiency, influencing their overall performance.

(Source: Scholarly Community Encyclopedia)

Second-Generation Glucose Biosensor Statistics

- The second-generation enzymatic glucose biosensor addresses the limitation of oxygen dependence seen in the first generation by incorporating artificial redox mediators instead of relying on an oxygen-dependent electrode.

- However, these biosensors are not ideal for implantable devices due to the use of free mediators in the solution.

- This design presents a challenge, as the concentration of these free mediators would fluctuate over time if the device were implanted in a patient.

- Despite their advancement in overcoming oxygen dependence, second-generation glucose biosensors face challenges in maintaining consistent mediator concentrations when implanted.

(Source: Maciac Sensors)

Third-Generation Glucose Biosensor Statistics

- Third-generation enzymatic glucose biosensors enable direct electron transfer between the enzyme and electrode, eliminating the need for natural or synthetic mediators.

- This advancement provides advantages like improved selectivity and sensitivity to glucose, faster response times, and a reduced operating potential.

- Challenges in this generation include enzyme leaching and the necessity for nanomaterials with optimal conductivity to facilitate direct electron transfer from the FAD-active redox center of the enzyme to the working electrode.

- Despite these challenges, third-generation enzymatic glucose biosensors demonstrate enhanced performance characteristics.

(Source: Scholarly Community Encyclopedia)

Fourth-Generation Glucose Biosensor Statistics

- Fourth-generation glucose sensors operate by directly oxidizing glucose on the surface of the electrode.

- The fourth-generation glucose biosensor marks a significant leap in biosensing technology, incorporating advanced materials like nanomaterials and biocompatible polymers for heightened sensitivity.

- Notable improvements include innovative transduction mechanisms, such as electrochemical and optical methods, allowing real-time monitoring and versatility in applications.

(Source: University of Manchester)

Issues Concerning Glucose Biosensors Statistics

- Many challenges associated with glucose biosensors stem from factors other than the device itself.

- In almost every instance, the fundamental design of commercially successful biosensors has remained largely unchanged for an extended period.

- The prevalent approach continues to be mediated amperometric designs akin to the original MediSense ExacTech device, introduced 15 years ago.

- Companies producing glucose meters have been slow in adopting new technologies, often opting for a strategy of repackaging existing technology in a new casing.

- This, coupled with targeted marketing campaigns, allows for the short-term retention of market share but does little to expand the market beyond the existing user base.

(Source: CORE- Open University)

Recent Developments

Technological Innovations:

- Recent advances have been made in electrochemical glucose biosensors, focusing on enhancing the precision and efficiency of glucose oxidase-based (GOx) amperometric sensors.

- These innovations aim to address challenges like the variability of background oxygen affecting sensor accuracy and improving the enzymatic reaction cycles for consistent glucose monitoring.

Funding Rounds:

- Series B funding round for a glucose biosensor developer in February 2024, raising $40 million to advance research and development efforts and expand commercialization efforts.

- Seed funding for a biosensor manufacturing company in April 2024, securing $15 million to scale up production capacity and meet growing demand for glucose monitoring devices.

Market Dynamics:

- The glucose biosensors market continues to expand with the integration of non-invasive monitoring technologies.

- These advancements aim at enhancing patient comfort by eliminating the need for blood samples and instead using alternative physiological fluids like sweat or ocular fluid for glucose monitoring.

Commercial Developments:

- On the business front, there have been several strategic initiatives, such as mergers and acquisitions, aimed at expanding product portfolios and entering new markets.

- For instance, significant collaborations and product launches are anticipated to propel the market growth. Driven by increasing demand for innovative and reliable glucose monitoring solutions.

Investment Landscape:

- Venture capital investments in glucose biosensor startups totaled $2.9 billion in 2023, with a focus on companies developing innovative glucose monitoring technologies.

- Strategic partnerships and collaborations between medical device manufacturers, pharmaceutical companies, and digital health startups accounted for 55% of total investment activity in the glucose biosensors market in 2023, reflecting industry efforts to advance diabetes management and improve patient outcomes.

Conclusion

Glucose Biosensors Statistics – In summary, glucose biosensors are essential tools in healthcare and diagnostics, evolving through generations to address challenges and improve performance.

While first-generation biosensors relied on mediators and had limitations, third-generation biosensors achieved direct electron transfer, enhancing selectivity and sensitivity.

However, commercial innovation has been slow, with companies often repackaging existing technology. Future developments, such as fourth-generation glucose biosensors, hold promise in overcoming limitations and expanding applications, benefiting diabetes management and personalized medicine.

As technology advances, these biosensors will play a pivotal role in monitoring and enhancing the lives of individuals with diabetes and related conditions.

FAQs

A glucose biosensor is a device that measures the concentration of glucose in a biological sample, such as blood or saliva. It typically consists of an enzyme that reacts with glucose, a transducer to convert the reaction into an electrical signal, and a display or readout for the user.

Glucose biosensors work by utilizing enzymes like glucose oxidase to catalyze the reaction of glucose with oxygen or other substances. This reaction generates an electrical signal that is proportional to the glucose concentration in the sample.

Glucose biosensors are often categorized into first, second, and third generations based on their technology and design. First-generation biosensors rely on mediators, second-generation biosensors use artificial mediators, and third-generation biosensors enable direct electron transfer between the enzyme and electrode.

The primary application of glucose biosensors is in diabetes management. They allow individuals with diabetes to monitor their blood glucose levels regularly. Additionally, glucose biosensors find applications in medical diagnostics, research, and various industries, including food and beverage.

Yes, glucose biosensors may have limitations, including the need for calibration, susceptibility to interference from other substances in the sample, and the requirement for frequent enzyme replacement. Additionally, the accuracy of glucose biosensors can be affected by factors like temperature and humidity.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)