Table of Contents

Overview

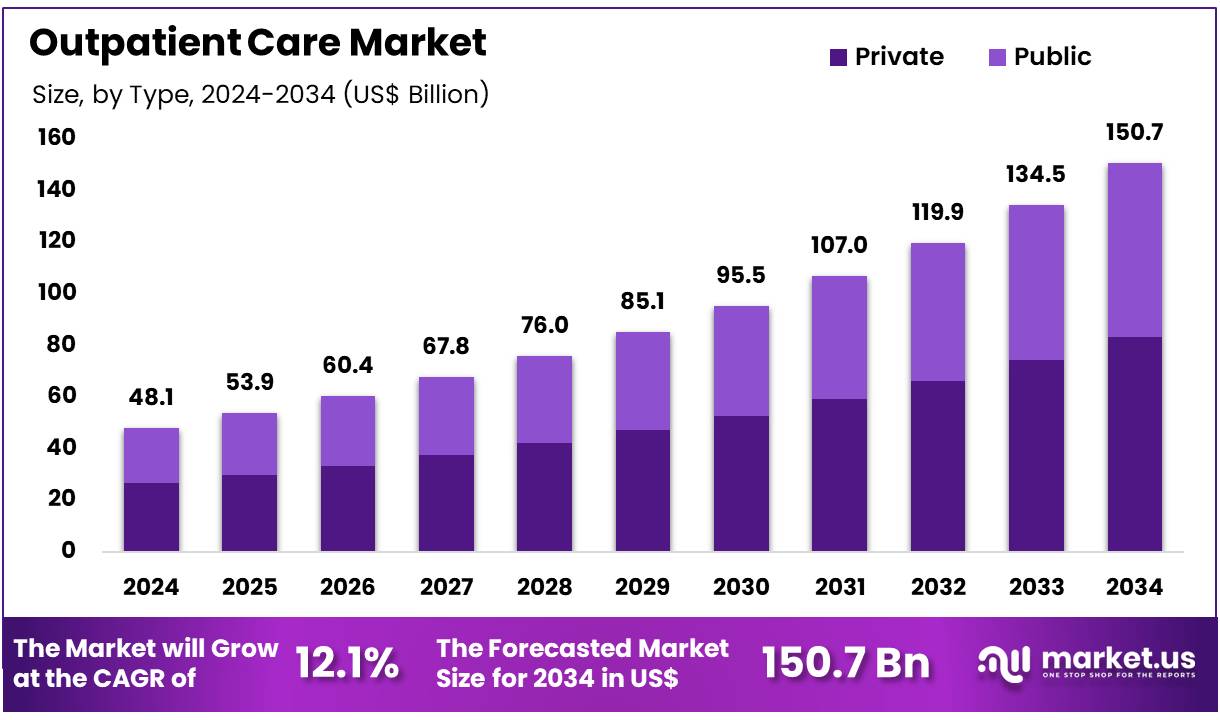

New York, NY – Dec 10, 2025 – Global Outpatient Care Market size is expected to be worth around US$ 150.7 Billion by 2034 from US$ 48.1 Billion in 2024, growing at a CAGR of 12.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 37.4% share with a revenue of US$ 18.0 Billion.

The global outpatient care market has been experiencing steady expansion as healthcare systems continue to shift toward cost-efficient and patient-centric service models. Growth has been supported by rising demand for preventive care, increasing chronic disease prevalence, and the widespread adoption of minimally invasive procedures. A preference for convenient medical services has been observed among patients, and this trend has contributed to the increasing utilization of outpatient facilities.

Technological advancements have played a central role in strengthening outpatient operations. The integration of digital health records, remote monitoring tools, and advanced diagnostic technologies has enhanced care delivery and improved clinical outcomes. These innovations have also increased operational efficiency for healthcare providers, thereby supporting broader market adoption.

Cost advantages have been recognized as another key driver. Outpatient services typically require fewer resources than inpatient treatments, and this factor has been instrumental in supporting their growing acceptance among insurers and patients. The expansion of ambulatory surgical centers, specialty clinics, and diagnostic centers has further widened access to outpatient care across both developed and emerging markets.

Regulatory initiatives promoting value-based healthcare have provided additional momentum to outpatient service providers. Quality-of-care standards are being strengthened and patient safety protocols have been improved, reinforcing confidence in outpatient treatment pathways. The outlook remains positive, as continued investments in healthcare infrastructure and digital technologies are expected to support sustained market growth. The outpatient care model is anticipated to remain a critical component of modern healthcare delivery.

Key Takeaways

- The outpatient care market generated a revenue of US$ 48.1 Billion in 2024, and it has been expanding at a CAGR of 12.1%, with projections indicating an increase to US$ 150.7 Billion by 2034.

- The type segment, which includes public and private facilities, was dominated by the private segment, accounting for 55.3% of the market share in 2024.

- Based on application, the market is categorized into hospitals, ambulatory surgical centres, and others, with hospitals representing a significant share of 38.5%.

- In terms of service types, the market is segmented into ambulatory surgical centers, urgent care centers, diagnostic imaging centers, primary care clinics, and others. Ambulatory surgical centers emerged as the leading segment, contributing 31.2% of the total revenue.

- From a regional perspective, North America dominated the global market, capturing 37.4% of the total market share in 2024.

Regional Analysis

North America accounted for the largest share of the Outpatient Care Market at 37.4%, supported by strong demand for convenient and accessible medical services. The expansion of outpatient capabilities has been enabled by technological advances that allow complex procedures to be performed outside hospital settings. Growth in U.S. national health expenditures, estimated at 8.2% in 2024, and supportive reimbursement policies have reinforced this shift.

CMS initiatives continue to incentivize lower-cost care environments, while Medicare Advantage plans recorded nearly 50 million prior authorization determinations in 2023, reflecting substantial activity in managed outpatient services. In Canada, total healthcare spending is projected to rise by 5.7% in 2024. CIHI data indicate sustained growth in emergency department visits and day surgeries, underscoring strong reliance on ambulatory care. Major providers such as HCA Healthcare reported rising revenues and increased outpatient-related admissions, demonstrating expanding demand for non-inpatient services.

Asia Pacific is projected to witness the fastest CAGR, driven by rising chronic disease prevalence, growing incomes, and improved healthcare infrastructure. Government programs in India, Japan, and China continue to strengthen primary and community-based care. Additionally, private providers such as IHH Healthcare are expanding outpatient networks to meet the increasing need for accessible and affordable services.

Use Cases

- Telemedicine for Routine Follow-Ups: The adoption of virtual care has expanded steadily, as reflected by the fact that 30.1% of adults reported at least one telemedicine appointment in 2022. Telehealth platforms are being utilized for chronic disease management, medication adjustments, and mental health follow-up consultations.

- Specialty-Based Utilization of Telehealth: In 2022, telemedicine was incorporated into specialist workflows at varying levels. It was observed that 41.5% of specialists used telehealth for fewer than 25% of their total visits, while 27.4% conducted at least half of their consultations virtually. This pattern illustrates its dual role in both initial assessments and ongoing specialist care.

- Telehealth Integration in Adult Day Services: Telemedicine tools were adopted by approximately 46% of U.S. adult day services centers in 2022. Their utilization supported remote patient monitoring and virtual therapy sessions, particularly for older adults requiring routine oversight.

- Ambulatory Surgery Centers and High-Volume Procedures: Ambulatory surgery centers (ASCs) have broadened their procedural scope to more than 3,600 procedure types. A focused set of 57 procedures accounted for 75% of Medicare revenue, with common high-volume services including cataract surgeries, gastrointestinal endoscopies, and minor orthopedic interventions.

- Home-Based Acute Care Delivery: Under the Hospital-at-Home model, inpatient-level care was extended to patient residences. By October 2024, a total of 366 hospitals had delivered services such as IV antibiotic therapy, cardiac monitoring, and post-operative care to more than 31,000 patients, demonstrating a significant shift from traditional inpatient settings to home-based acute care.

- Physician Office Visit Volumes in Outpatient Care: Outpatient settings continued to form the backbone of U.S. healthcare utilization. In 2023, physician offices recorded approximately 1.0 billion visits, equal to 320.7 visits per 100 persons. These encounters included preventive screenings, acute illness consultations, and routine follow-up appointments.

Frequently Asked Questions on Outpatient Care

- What types of services are included in outpatient care?

Outpatient care includes diagnostic imaging, laboratory tests, physician consultations, rehabilitation, minor surgeries, and chronic disease management. These services are delivered in clinics or ambulatory centers and are designed to support efficient treatment while minimizing inpatient admissions. - Why is outpatient care important?

Outpatient care is important because it lowers treatment costs, improves access, and reduces the burden on hospitals. It supports early intervention and continuous monitoring, enabling better outcomes and helping healthcare systems manage rising patient volumes more effectively. - How does outpatient care benefit patients?

Patients benefit from shorter visits, reduced costs, quicker recoveries, and greater flexibility. Outpatient settings facilitate faster appointments and minimal disruption to daily routines, improving satisfaction and enabling consistent management of both acute and chronic health conditions. - What technologies support outpatient care?

Key technologies include telehealth platforms, electronic health records, remote monitoring tools, and advanced diagnostic systems. These solutions enhance care coordination, reduce waiting times, and increase the efficiency of outpatient workflows, contributing to improved patient outcomes. - How is outpatient care different from inpatient care?

Outpatient care does not require overnight hospitalization, whereas inpatient care involves longer stays for intensive monitoring. Outpatient settings focus on minor procedures and routine services, offering faster recovery and reduced costs compared to more resource-intensive inpatient environments. - What factors are driving growth in the outpatient care market?

Market growth is driven by aging populations, cost pressures on hospitals, advances in minimally invasive procedures, and wider insurance coverage. Increasing patient preference for convenient, lower-cost treatment settings continues to accelerate the shift toward outpatient models. - Which regions lead the outpatient care market?

North America leads due to strong insurance systems, advanced technology adoption, and extensive ambulatory infrastructure. Europe follows with supportive regulatory frameworks, while Asia-Pacific shows rapid growth driven by rising healthcare spending and expanding private outpatient facilities. - Who are the key players in the outpatient care market?

Key participants include hospital groups, ambulatory surgery centers, specialty clinics, diagnostic chains, and integrated care providers. These organizations invest in technology, expand procedures offered, and strengthen partnerships to increase service delivery capabilities across outpatient settings.

Conclusion

The outpatient care market is positioned for sustained expansion as healthcare systems continue to prioritize cost efficiency, accessibility, and patient-centered delivery models. Growth has been supported by rising chronic disease prevalence, advances in minimally invasive procedures, and increased adoption of digital health technologies.

Strong participation from private facilities, expanding ambulatory surgical capabilities, and supportive regulatory frameworks have reinforced market momentum. Regional performance remains led by North America, while Asia-Pacific demonstrates rapid acceleration. Continued investments in infrastructure, technology integration, and value-based care models are expected to strengthen outpatient care’s role as a core component of modern healthcare delivery.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)