Table of Contents

Overview

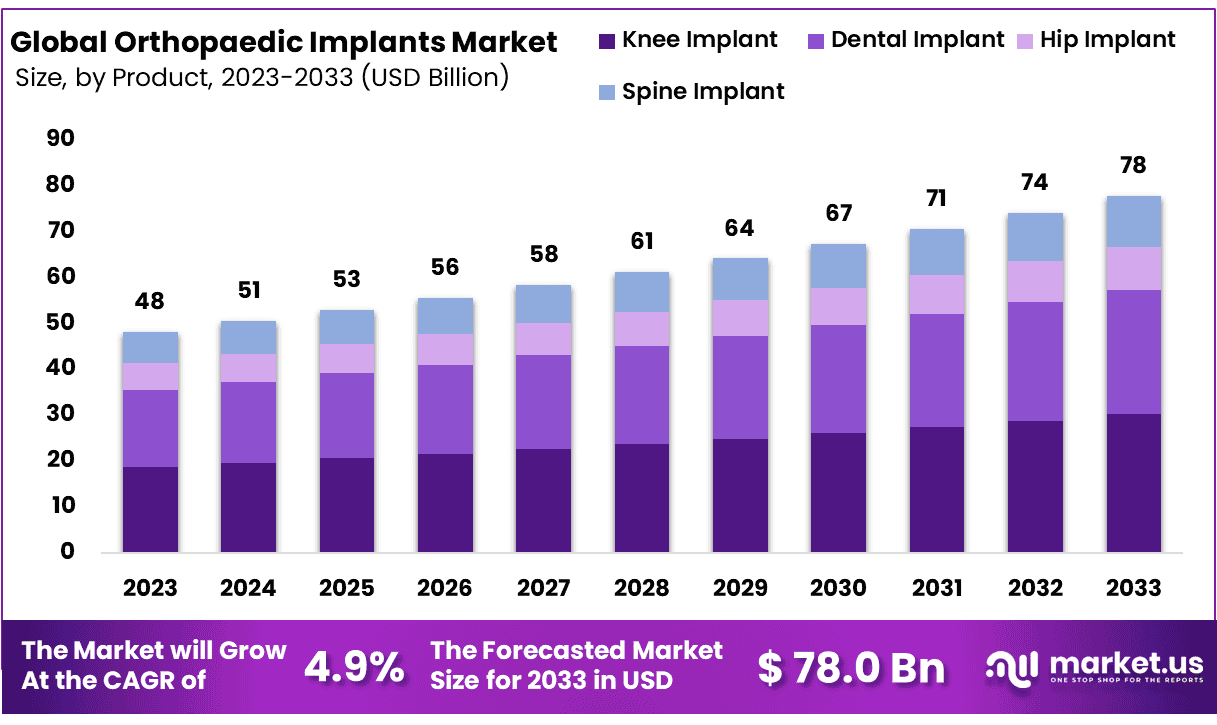

New York, NY – Jan 09, 2026 – The global Orthopedic Implants Market size was worth USD 48 Billion in 2023, and it will grow by USD 78 Billion by 2033. It is anticipated to grow a CAGR of 4.9% between 2024-2033.

The orthopedic implants market is experiencing consistent growth, supported by an increasing number of orthopedic procedures worldwide. This growth is primarily attributed to the rising prevalence of musculoskeletal disorders, age-related bone degeneration, and sports-related injuries. Orthopedic implants are widely used in procedures involving joint replacement, trauma fixation, spinal correction, and reconstructive surgeries, making them a critical component of modern healthcare systems.

The demand for orthopedic implants is further strengthened by the expanding geriatric population, as older individuals are more susceptible to conditions such as osteoarthritis, osteoporosis, and fractures. In addition, improved access to healthcare services and higher awareness of advanced surgical treatments are contributing to greater adoption of implant-based procedures across both developed and emerging economies.

Technological progress has played a significant role in shaping the market landscape. Innovations such as 3D-printed implants, minimally invasive surgical techniques, and advanced biomaterials are improving implant durability, biocompatibility, and patient outcomes. These developments are enabling faster recovery times and reducing the risk of post-operative complications, which supports wider clinical acceptance.

Hospitals and specialty orthopedic centers remain the primary end users of orthopedic implants, supported by rising investments in healthcare infrastructure. From a regional perspective, strong demand is observed in North America and Europe, while Asia-Pacific is emerging as a high-growth region due to increasing healthcare expenditure and a growing patient base.

Overall, the orthopedic implants market is expected to maintain stable expansion, supported by demographic trends, technological innovation, and continuous improvements in orthopedic care delivery.

Key Takeaways

- In 2023, the global Orthopedic Implants Market was valued at approximately USD 48 billion.

- The market is expected to expand by nearly USD 78 billion by 2033.

- The market is projected to register a Compound Annual Growth Rate (CAGR) of 4.9% during the period 2023–2032.

- By 2050, nearly one-sixth of the global population is expected to be aged 65 years and above.

- In North America and Europe, individuals aged over 65 years could account for around 40% of the total population by 2050.

- Globally, an estimated 1.71 billion people were affected by musculoskeletal disorders in 2022.

- In the United Kingdom, more than 20 million individuals are reported to suffer from musculoskeletal diseases.

- During the first wave of the COVID-19 pandemic, orthopedic surgical procedures in the United States declined by 68.4%.

- In 2023, knee implants accounted for a revenue share of 38.8% within the Orthopedic Implants Market.

- Metallic implants represented 57.6% of total market revenue in 2023.

- Hospitals and clinics remained the dominant end users, capturing a revenue share of 62.9%.

- North America accounted for approximately 52% of the global Orthopedic Implants Market.

- Knee implants continue to represent the highest-demand segment within the market.

- The Orthopedic Implants Market is moderately competitive, with the presence of a limited number of major players.

- Strategic partnerships, technological investments, and new product launches are expected to support market growth in the coming years.

Orthopedic Implants Statistics by Segment

Knee Implants

- Annual Knee Replacement Volume (U.S.): More than 600,000 knee replacement surgeries are performed each year in the United States. This volume reflects strong and sustained demand driven by population aging, rising obesity prevalence, and increasing incidence of osteoarthritis.

- Implant Longevity and Durability: Approximately 90–95% of knee implants remain functional for at least 10 years, while 80–85% last up to 20 years, demonstrating the long-term reliability of modern implant designs and materials.

- Gender-Based Procedure Distribution: Nearly 60% of knee replacement procedures are performed on women, indicating a higher burden of knee-related disorders among female patients. This trend is commonly associated with anatomical differences, hormonal factors, and higher osteoporosis prevalence.

- Prevalence of Knee Osteoarthritis (U.S.): It is estimated that almost 50% of U.S. adults will develop knee osteoarthritis during their lifetime, making it one of the most significant drivers of knee replacement surgeries.

- Functional Limitations Among Osteoarthritis Patients: Around 80% of individuals diagnosed with osteoarthritis experience substantial movement limitations, negatively affecting daily functioning and overall quality of life.

- Clinical Success Rate: More than 90% of patients report significant pain relief following knee replacement surgery, highlighting the effectiveness of the procedure in improving clinical outcomes.

- Revision Surgery Incidence: The knee implant revision rate in the United States is approximately 3.6%, reflecting a relatively low need for secondary procedures and indicating strong initial surgical success.

- Research and Innovation Funding: A USD 2.3 million research grant has been awarded by the National Institutes of Health (NIH) to support advancements in knee replacement technologies, with a focus on improving implant performance and patient outcomes.

Hip Implants

- Global Osteoarthritis Prevalence (Aged 60+): Osteoarthritis affects approximately 10% of men and 18% of women aged 60 years and older worldwide, with higher prevalence among women attributed to hormonal factors and longer life expectancy.

- Long-Term Success of Hip Arthroplasty: An estimated 90–95% of hip replacement procedures remain successful at 10 years, demonstrating strong durability and long-term pain relief benefits.

- Growth in Total Hip Arthroplasty in Japan (2007–2014): The annual number of total hip arthroplasty procedures in Japan increased significantly from 9,434 in 2007 to 33,625 in 2014, driven by demographic aging and rising osteoarthritis prevalence.

- Aging Population in Japan: In 2018, 28.1% of Japan’s population was aged 65 years or older, with projections indicating this share will exceed 30% by 2025, further accelerating demand for hip replacement procedures.

- Healthcare System Impact in Australia: The expected rise in hip arthroplasty volumes is projected to place increasing pressure on Australia’s healthcare infrastructure, requiring expanded capacity and resource allocation.

- Radiographic Knee Osteoarthritis in Japan: Radiographic assessments indicate that 54.6% of the Japanese population shows evidence of knee osteoarthritis, contributing to strong demand for both knee and hip implant procedures.

- Procedure Volume Growth Outlook: Hip and knee replacement surgeries are projected to grow steadily on an annual basis, supported by demographic aging trends and the rising global burden of osteoarthritis.

- Japanese Data Source: These insights are supported by data from the National Database of Health Insurance Claims and Specific Health Checkups, which informs healthcare planning and policy development in Japan.

Dental Implants

- Adoption Rate in the U.S.: By 2016, dental implant procedures accounted for 5.7% of annual dental treatments, reflecting growing acceptance of implants as a preferred tooth replacement solution.

- Implant Penetration Among Older Adults: Approximately 13% of individuals aged 65–74 have received dental implants, highlighting strong uptake among the aging population seeking functional and aesthetic oral restoration.

- Revenue Contribution to Dental Practices (2022): Average annual revenue per dental practice reached USD 1.2 million in 2022, underscoring the financial importance of implant procedures within the dental care market.

- Clinical Success Rate: Dental implants demonstrate a high success rate of approximately 97%, reinforcing their reliability and long-term effectiveness.

- Workforce Training Gap: Fewer than 30% of the 150,000 general dental practitioners in the United States are trained to place dental implants, indicating a supply-side constraint amid rising demand.

- Mini Dental Implants: Mini dental implants, typically measuring 1.8 mm to 3 mm in diameter, provide a minimally invasive alternative, expanding treatment options for patients with limited bone volume.

Global Orthopedic Implants Market Summary

- Global Geriatric Population (2019): The global population aged 65 and above reached 703 million, accounting for 9% of the total population, and serving as a primary demand driver for orthopedic implants.

- Burden of Musculoskeletal Disorders: Approximately 1.7 billion older adults worldwide are affected by musculoskeletal conditions, significantly increasing the need for joint replacement interventions.

- U.S. National Health Expenditure (2020): Healthcare spending in the United States totaled USD 4.1 trillion, representing 19.7% of GDP, with a substantial share allocated to chronic and orthopedic care.

- Medicare Expenditure (2020): Medicare spending reached USD 829.5 billion, accounting for 20% of total U.S. healthcare expenditure, with orthopedic procedures forming a major cost component.

- Medicaid Expenditure (2020): Medicaid spending amounted to USD 671.2 billion, or 16% of national healthcare spending, supporting access to orthopedic care among low-income populations.

- Healthcare Spending Growth Rate: U.S. healthcare expenditure is projected to grow at a compound annual rate of 5.4%, driven by demographic shifts and rising chronic disease prevalence.

- Joint Replacement Procedures in Canada (2020–2021): Approximately 110,000 joint replacement surgeries were performed, indicating sustained demand within the Canadian healthcare system.

- Same-Day Joint Replacement Surgeries in Canada: More than 7,300 procedures were conducted on a same-day basis, reflecting advancements in surgical efficiency and post-operative care protocols.

- Hip Implant Procedures in India (2019): India recorded 4,700 hip implant surgeries in 2019, signaling growing adoption of orthopedic interventions in emerging markets.

- Osteoarthritis Prevalence in the U.S.: Osteoarthritis affects approximately 32.5 million adults in the United States, making it one of the leading clinical indications for joint replacement surgery.

Regional Analysis

North America holds a leading position in the Orthopedic Implants Market, accounting for the largest share of global revenue. With a market share of approximately 54.5%, the region is expected to maintain its dominance throughout the forecast period. Market expansion in North America is supported by an increasing geriatric population, a rising incidence of bone and musculoskeletal disorders, and continuous advancements in orthopedic surgical technologies.

The region is further supported by a growing volume of joint replacement procedures and a favorable regulatory framework that encourages innovation and adoption of advanced implants. Meanwhile, the Asia-Pacific region is projected to register notable growth over the forecast period. This growth can be attributed to the increasing prevalence of osteoarthritis, osteoporosis, and trauma-related bone injuries, particularly in countries such as Japan and China. Rising healthcare expenditure and ongoing improvements in medical infrastructure are also contributing to the expansion of the Orthopedic Implants Market across the region.

Frequently Asked Questions on Orthopedic Implants

- What materials are commonly used in orthopedic implants?

Orthopedic implants are primarily manufactured using biocompatible materials such as titanium alloys, stainless steel, cobalt-chromium alloys, ceramics, and medical-grade polymers, ensuring durability, corrosion resistance, and long-term compatibility with human bone and tissue. - What conditions require orthopedic implants?

Orthopedic implants are used to treat conditions including osteoarthritis, osteoporosis-related fractures, spinal deformities, sports injuries, and severe trauma. These devices help maintain alignment, promote bone healing, and improve patient mobility and quality of life. - How long do orthopedic implants typically last?

The lifespan of orthopedic implants generally ranges from 15 to 25 years, depending on implant type, material quality, patient age, activity level, and surgical precision. Advances in materials science have contributed to improved implant longevity.. - What factors are driving the orthopedic implants market growth?

The growth of the orthopedic implants market is driven by rising geriatric populations, increasing prevalence of musculoskeletal disorders, higher sports injury rates, and growing demand for joint replacement procedures across developed and emerging healthcare systems. - What are the major product segments in the orthopedic implants market?

Major market segments include joint reconstruction implants, spinal implants, trauma fixation devices, dental implants, and orthobiologics. Joint reconstruction, particularly hip and knee implants, represents a significant share due to high procedure volumes globally. - How is technology influencing the orthopedic implants market?

Technological advancements such as 3D printing, robotic-assisted surgery, and patient-specific implants are improving surgical accuracy and outcomes. These innovations are enhancing implant customization, reducing revision rates, and supporting overall market expansion. - Which regions dominate the orthopedic implants market?

North America dominates the orthopedic implants market due to advanced healthcare infrastructure, high procedure adoption, and favorable reimbursement policies. Europe follows closely, while Asia-Pacific is witnessing rapid growth driven by expanding medical tourism and aging populations.

Conclusion

The orthopedic implants market is positioned for steady and sustained growth, supported by rising orthopedic procedure volumes, an expanding geriatric population, and the growing burden of musculoskeletal disorders worldwide. Continuous advancements in implant materials, surgical techniques, and personalized solutions are improving clinical outcomes and long-term implant performance.

Strong demand for knee and hip implants, combined with increasing healthcare investments, reinforces market stability. While North America and Europe remain mature markets, Asia-Pacific is emerging as a key growth engine. Overall, demographic trends, technological innovation, and improved access to orthopedic care will continue to drive long-term market expansion.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)