Table of Contents

Overview

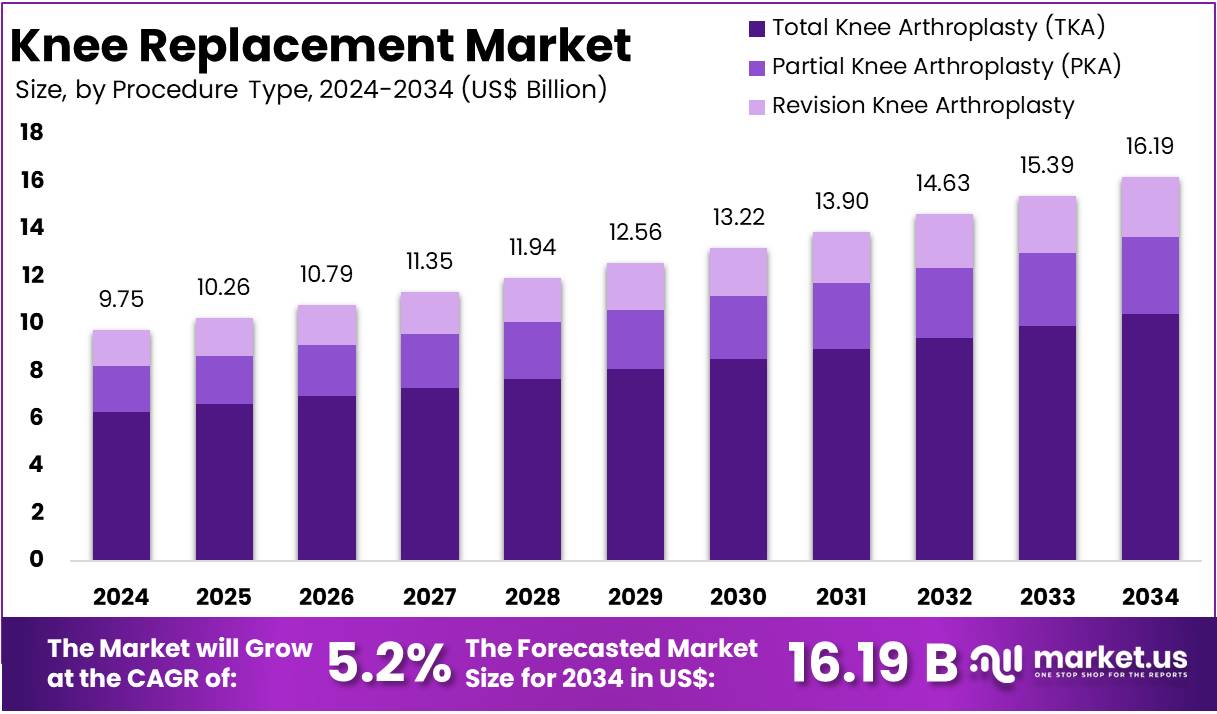

New York, NY – Feb 04, 2026 – The Global Knee Replacement Market size is expected to be worth around US$ 16.19 billion by 2034 from US$ 9.75 billion in 2024, growing at a CAGR of 5.2% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 43.7% share and holds US$ 4.26 Billion market value for the year.

Knee replacement surgery has become a widely adopted and clinically validated procedure for patients suffering from severe knee pain and reduced mobility caused by osteoarthritis, rheumatoid arthritis, or joint injury. The procedure involves replacing damaged or worn knee joint surfaces with artificial implants designed to restore function, relieve pain, and improve overall quality of life.

With advancements in medical technology, modern knee replacement procedures are characterized by high success rates, improved implant durability, and shorter recovery timelines. The use of advanced imaging, precision surgical techniques, and biocompatible materials has significantly enhanced surgical outcomes. As a result, patients are experiencing improved joint stability, increased range of motion, and long-term pain relief.

The growing prevalence of knee-related disorders, particularly among the aging population, has contributed to the rising demand for knee replacement surgeries worldwide. In addition, increasing awareness of treatment options and improved access to orthopedic care are supporting broader adoption of the procedure. Minimally invasive techniques and enhanced rehabilitation protocols are further improving patient satisfaction and post-surgical recovery.

Healthcare providers continue to emphasize patient evaluation, personalized treatment planning, and post-operative physiotherapy as critical factors for successful outcomes. Knee replacement surgery is generally recommended when non-surgical treatments such as medication, physical therapy, and lifestyle modification no longer provide adequate relief.

Key Takeaways

- In 2024, the knee replacement market generated revenue of US$ 9.75 billion and is projected to expand at a CAGR of 5.2%, reaching US$ 16.19 billion by 2034.

- Based on procedure type, the market is segmented into Total Knee Arthroplasty (TKA), Partial Knee Arthroplasty (PKA), and Revision Knee Arthroplasty. Total Knee Arthroplasty (TKA) dominated the segment in 2024, accounting for 64.5% of the total market share.

- By implant type, the market is categorized into Fixed-Bearing Implants, Mobile-Bearing Implants, Medial Pivot Implants, and Customized Implants. Fixed-Bearing Implants held the leading position in 2024 with a 57.1% market share.

- In terms of components, the market is divided into Femoral, Tibial, and Patellar components, with the Tibial component emerging as the leading segment, capturing 55.5% of the market share in 2024.

- Based on material, the market includes Metal-on-Plastic, Ceramic-on-Ceramic, Metal-on-Metal, and Ceramic-on-Plastic. The Metal-on-Plastic segment dominated the market in 2024 with a 49.1% share.

- By surgery type, the market is classified into Traditional Surgery and Technology-Assisted Surgery. Traditional Surgery led the market, representing 83.2% of total procedures in 2024.

- According to end-user, the market is segmented into Hospitals, Ambulatory Surgical Centers (ASCs), and Orthopedic Clinics. Hospitals accounted for the largest share, contributing 64.8% of the global market in 2024.

- North America remained the leading regional market, securing a 43.7% share in 2024.

Regional Analysis

North America continues to dominate the knee replacement market, supported by a high volume of patients requiring surgical intervention and strong adoption of advanced and robotic-assisted technologies. The availability of sophisticated healthcare infrastructure and relatively high procedure costs further supports regional leadership. In addition, the strong presence of major industry participants contributes to sustained market growth.

In June 2024, Johnson & Johnson MedTech announced that DePuy Synthes received FDA 510(k) clearance for the VELYS Robotic-Assisted Solution for use in Unicompartmental Knee Arthroplasty, expanding beyond its earlier approval for Total Knee Arthroplasty. This advancement is expected to accelerate adoption of robotic-assisted knee procedures.

Europe represents a substantial market due to a large eligible patient base, while the Asia-Pacific region is expected to witness notable growth, driven by rising knee disorders and improving access to orthopedic care.

Emerging trends in knee replacement

Fast shift to outpatient and ambulatory surgery centers (ASCs)

- Knee replacement is being moved from long hospital stays to same-day or short-stay care, supported by better pain control and faster rehab.

- In US Medicare joint replacements, the share done in hospital outpatient settings increased from ~14% to ~72% by 2023 (2018–2023 trend).

Registry data also show average length of stay fell from 2.9 days (2012) to 1.1 days (2023) for TKA.

Rapid growth of robotic-assisted knee replacement

- Robotic use in primary TKA reached 15.9% in 2023, and it increased materially versus 2022 (12.5%).

- A US utilization study reported robotic TKA rising from 0.01% (2008) to 8.5% (2020) and projected robotic TKA could reach ~70.1% by 2030 (model-based projection).

Cementless fixation is gaining share (selected patients)

- Cementless fixation in primary TKA increased to ~21.8% (2023) in AJRR reporting.

Implant design mix is changing (medial-congruent growth)

- Medial congruent primary TKA designs reached 32.1% of cases in 2023 (up from 24.1% in 2022 and 2.3% in 2017).

- Posterior-stabilized designs remained large at 40.8% (2023) but declined vs 2022.

Material upgrades and insert innovation are becoming standard

- Highly cross-linked polyethylene remained the largest insert material at 45.9% in primary TKA (2023).

- Patellar resurfacing is still common (87.0% of primary TKA in 2023), though it has declined over time.

Infection remains the leading driver of revision burden

- The most common reason for revision TKA in 2023 was infection (32.5%), followed by mechanical loosening (24.4%).

- In older patients with cemented constructs, AJRR highlights show overall revision rising from 0.83% at 1 year to 2.60% at 10 years (typical range ~2–3% at 10 years).

Better anesthesia + pain pathways are enabling faster discharge

- General anesthesia (without nerve block) in primary TKA dropped to 22.7% (2023) from 40.6% (2017); use of general anesthesia with peripheral nerve block rose to 13.0% (2023) from 3.5% (2017).

Patient-reported outcomes (PROMs) are becoming more operational

- AJRR highlights show 44% of sites submitted PROMs as of Dec 31, 2023, and this was a 27% increase in sites vs the prior report; “linked” outcome completion is ~24–30%.

Procedure volumes remain large, supporting steady device demand

- A 2024 hip & knee industry review (citing iData estimates) reported US knee replacements grew ~5.1% from 2022 to 2023 to about 1.36 million, with primary knees ~1.13 million and revision knees growing ~8.4%.

Frequently Asked Questions on Knee Replacement

- Who is an ideal candidate for knee replacement?

Patients experiencing chronic knee pain, stiffness, or limited mobility due to osteoarthritis, rheumatoid arthritis, or injury, and who do not respond to conservative treatments, are typically considered suitable candidates for knee replacement surgery. - What types of knee replacement procedures are available?

Knee replacement procedures include total knee arthroplasty, partial knee arthroplasty, and revision knee arthroplasty. The choice of procedure depends on the extent of joint damage, patient condition, and clinical evaluation by orthopedic specialists. - How long does recovery take after knee replacement surgery?

Recovery after knee replacement generally takes several weeks to months. Most patients resume daily activities within six to twelve weeks, while complete recovery and optimal joint function may take up to one year. - What are the benefits of knee replacement surgery?

Knee replacement surgery offers long-term pain relief, improved joint mobility, enhanced quality of life, and the ability to perform routine physical activities, making it a highly effective treatment for severe knee joint degeneration. - Which segment dominates the knee replacement market?

Total Knee Arthroplasty dominates the knee replacement market due to its widespread clinical acceptance, proven long-term outcomes, and suitability for patients with severe or advanced knee joint degeneration. - What role does technology play in the knee replacement market?

Technological advancements, including robotic-assisted surgery and customized implants, improve surgical precision, reduce recovery time, and enhance patient outcomes, thereby supporting the increasing adoption of knee replacement procedures globally. - Which region leads the global knee replacement market?

North America leads the global knee replacement market due to high procedure volumes, advanced healthcare systems, strong adoption of innovative technologies, and the presence of major orthopedic device manufacturers.

Conclusion

The global knee replacement market is positioned for steady and sustained growth, supported by rising prevalence of knee disorders, an expanding aging population, and continuous advancements in surgical technologies and implant design. High clinical success rates, improved patient outcomes, and shorter recovery periods are strengthening procedure adoption worldwide.

The shift toward outpatient settings, growing use of robotic-assisted systems, and innovation in materials and implant configurations are reshaping procedural standards. North America remains the dominant market, while Asia-Pacific presents strong growth potential. Overall, favorable clinical outcomes, large procedure volumes, and technological progress are expected to drive long-term market expansion through 2034.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)