Table of Contents

Overview

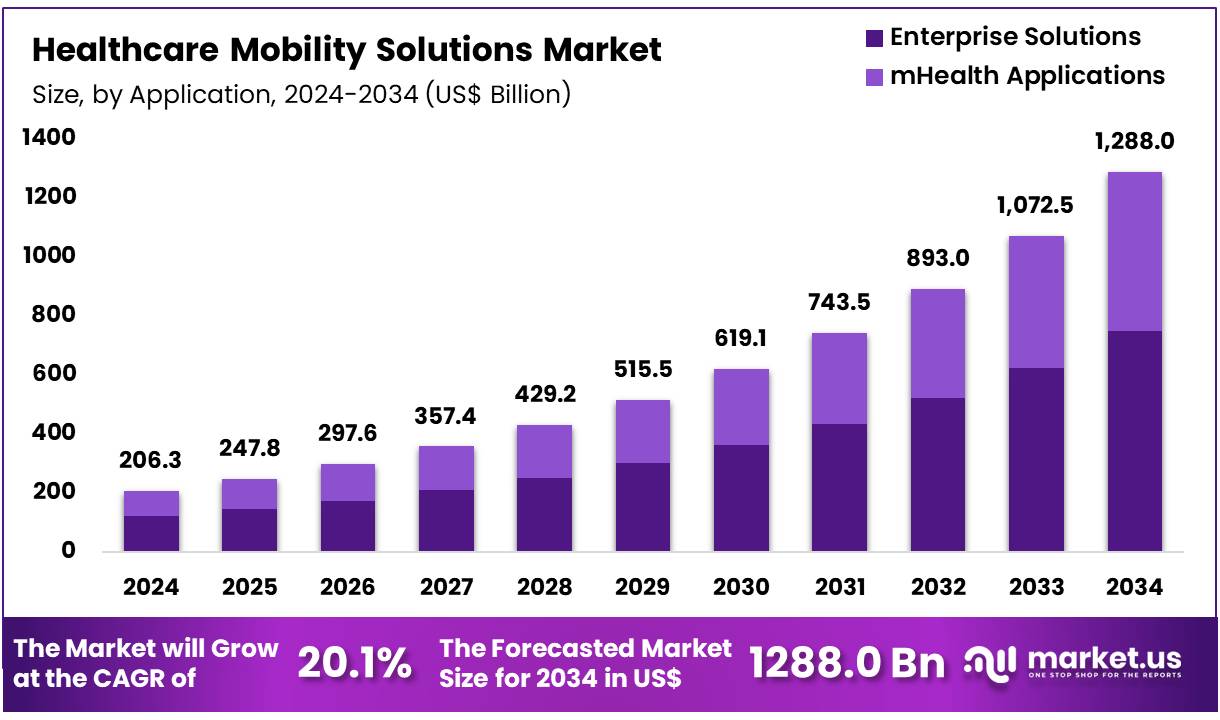

New York, NY – Dec 03, 2025 – The Global Healthcare Mobility Solutions Market size is expected to be worth around US$ 1288.0 billion by 2034 from US$ 206.3 billion in 2024, growing at a CAGR of 20.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 43.2% share with a revenue of US$ 89.1 Billion.

The global healthcare mobility solutions market is witnessing steady expansion as digital tools, mobile applications, and connected devices continue to transform care delivery. Significant demand has been observed from hospitals, clinics, and home-care providers, as mobile technologies enable faster decision-making, improved patient engagement, and enhanced operational efficiency. The growth of the market has been attributed to rising smartphone penetration, increased adoption of telehealth services, and the expansion of cloud-based clinical platforms across healthcare systems.

The deployment of mobility solutions has supported better communication among clinicians, reduced administrative burden, and strengthened care coordination. Strong emphasis has been placed on secure data exchange and compliance as health organizations integrate mobile devices into clinical workflows. Mobile computing, enterprise mobility platforms, and patient-centric applications are being adopted to streamline diagnostics, monitoring, and record management.

The rising incidence of chronic diseases and the shift toward remote patient monitoring have further stimulated market adoption. In addition, investments in health IT infrastructure and supportive regulatory initiatives have contributed to growing implementation across developed and emerging markets. North America continues to represent the leading region, while the Asia-Pacific market is expected to record accelerated growth due to expanding healthcare digitalization.

Healthcare mobility solutions are expected to remain an essential element of future healthcare ecosystems, enabling real-time data access, reducing costs, and improving patient outcomes. Continued innovation in mobile technologies is anticipated to support sustained market growth over the coming years.

Key Takeaways

- In 2024, the healthcare mobility solutions market generated US$ 206.3 billion in revenue, recorded a CAGR of 20.1%, and is projected to reach US$ 1288.0 billion by 2033.

- The product type segment includes enterprise mobility platforms, mobile applications, and mobile devices, with mobile devices leading the market by capturing 47.5% share in 2024.

- By application, the market is categorized into enterprise solutions and mHealth applications, with enterprise solutions accounting for 58.3% of the total share.

- In the end-user segment, the market is divided into healthcare payers, healthcare providers, and patients, where healthcare providers dominated with a 54.6% revenue share.

- North America emerged as the leading regional market, holding 43.2% of the global share in 2024.

Regional Analysis

North America Leading the Healthcare Mobility Solutions Market

North America accounted for the largest revenue share of 43.2%, supported by the widespread use of smartphones and tablets among healthcare professionals. High electronic health record (EHR) adoption rates reported by the ONC have increased the requirement for mobile accessibility within clinical environments. In addition, North America’s strong position in the global wearable medical devices market, as indicated in 2024 assessments, has reinforced regional growth. The launch of LillyDirect by Eli Lilly and Company in 2024 further reflects the region’s expanding reliance on mobile platforms to strengthen efficiency and accessibility in healthcare delivery.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is anticipated to register the fastest CAGR during the forecast period. By the end of 2022, the region reported 1.73 billion unique mobile subscriptions, with further expansion expected. Increasing smartphone affordability continues to support the uptake of mobile health services across emerging markets. India’s National Digital Health Mission (NDHM), initiated in 2022 to establish an integrated digital health infrastructure, is expected to advance the adoption of mobile-based healthcare solutions nationwide. Strengthening digital ecosystems across the region are contributing to broader acceptance and utilization of mHealth applications.

Emerging Trends

- Widespread Mobile EHR Utilization: The routine use of mobile devices for accessing and updating electronic health records has been observed across healthcare settings. By 2021, EHR adoption reached 88 percent among U.S. office-based physicians, and nearly 40 percent of hospitals provided patients with mobile access to their health information.

- Rapid Growth in Teleconsultations: Government-supported telemedicine services experienced significant expansion. In India, annual teleconsultations under the eSanjeevani platform increased from 0.26 crore in 2019–20 to 11.83 crore in 2023–24, indicating strengthened mobile-enabled clinical engagement.

- Enhanced Personal Health Record Portability: Federal programs such as Blue Button enabled millions of beneficiaries to download and exchange their personal health information from Defense, Health and Human Services, and Veterans Affairs systems. This has strengthened patient autonomy in mobile health data management.

- Expansion of Mobile Health Infrastructure: Central and state authorities scaled mobile health infrastructure significantly, deploying more than 1,19,000 primary-center spokes and 15,074 hubs integrated through the eSanjeevani network. This ecosystem supported 21.60 crore teleconsultations as of March 31, 2024.

Use Cases

- National Teleconsultation Service: The mobile-centric eSanjeevani platform facilitated 21.60 crore teleconsultations by March 31, 2024, connecting 1,19,029 spokes with 15,074 hubs and enabling remote specialist access for both rural and urban populations.

- Tele-Mental Health Interventions: The Centre for Tele-mental Health delivered mobile-based mental health counseling to 24,243 individuals between January 1, 2023, and March 31, 2024, improving service reach across underserved regions.

- Mobile Medical Units (MMUs): Under the National Health Mission, 1,433 mobile medical units including vans and boat clinics were operational as of December 31, 2023, providing diagnostic and treatment services in hard-to-reach areas.

- Accountable Care Enablement: By January 2025, accountable care arrangements reached 53.4 percent of Traditional Medicare beneficiaries, covering more than 14.8 million individuals. Many of these relationships were supported through mobile communication channels and remote monitoring solutions.

Frequently Asked Questions on Healthcare Mobility Solutions

- What are healthcare mobility solutions?

Healthcare mobility solutions refer to digital tools, mobile applications, and connected devices that support real-time communication, patient monitoring, data access, and workflow optimization. These solutions enable improved efficiency, faster clinical decisions, and better patient engagement across healthcare settings. - How do healthcare mobility solutions benefit hospitals?

These solutions enhance hospital operations by enabling secure mobile access to patient records, improving communication among care teams, and reducing administrative delays. Their adoption supports streamlined workflows, increased productivity, and improved clinical outcomes through timely data availability and decision support. - What technologies are commonly used in healthcare mobility solutions?

Key technologies include smartphones, tablets, mobile applications, cloud platforms, remote monitoring devices, and enterprise mobility systems. These tools facilitate seamless data exchange, enhanced coordination, and patient-centric services within healthcare organizations. - Who uses healthcare mobility solutions?

Primary users include healthcare providers, patients, and payers. Providers use mobile tools for clinical tasks, patients rely on apps for self-care and monitoring, and payers adopt mobility systems to streamline claims and enhance service delivery. - What is driving the growth of the healthcare mobility solutions market?

Market growth is driven by rising smartphone adoption, increasing telehealth usage, expanding cloud infrastructure, and a growing need for efficient clinical workflows. Strong emphasis on digital transformation also contributes to accelerating market demand. - Which region leads the healthcare mobility solutions market?

North America leads the market due to strong technological adoption, high EHR integration, and significant investment in digital health platforms. The region’s mature healthcare IT ecosystem continues to support large-scale deployment of mobility solutions. - What segment holds the largest share in the market?

In 2024, mobile devices held the leading share in the product segment, while enterprise solutions dominated by application. Healthcare providers represented the largest end-user group due to high usage across clinical and administrative operations.

Conclusion

The global healthcare mobility solutions market is expected to maintain strong momentum as digitalization advances across care settings. Growth has been supported by rising smartphone penetration, expanding telehealth utilization, and increasing reliance on cloud-based clinical platforms. North America remains the dominant region, while Asia-Pacific is projected to achieve rapid expansion due to sustained digital infrastructure development.

Enterprise mobility platforms, mobile devices, and mHealth applications continue to enhance communication, data accessibility, and care coordination. The market outlook remains positive, as ongoing innovation in mobile technologies is expected to strengthen operational efficiency, reduce costs, and improve patient outcomes over the forecast period.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)