Table of Contents

Overview

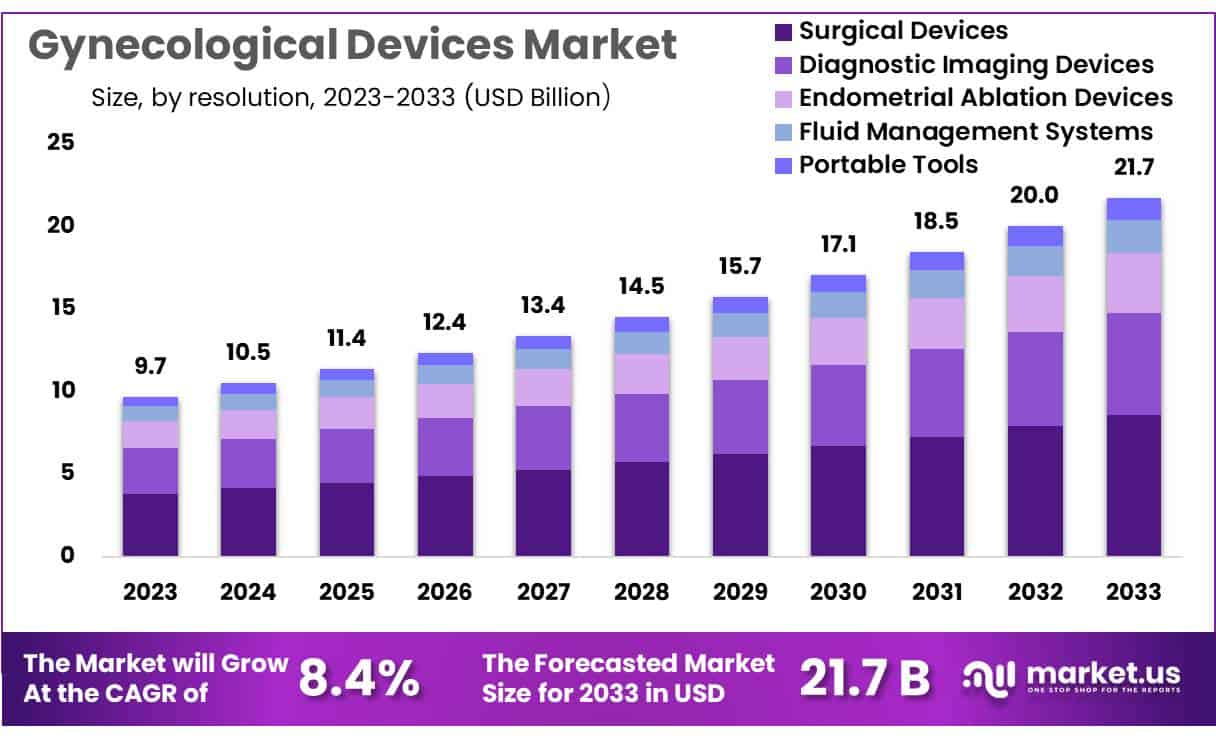

New York, NY – Jan 08, 2026 – Global Gynecological Devices Market size is expected to be worth around USD 21.7 billion by 2033 from USD 9.7 billion in 2023, growing at a CAGR of 8.4% during the forecast period 2024 to 2033.

The global gynecological devices market is witnessing consistent growth, supported by increasing awareness of women’s health, rising prevalence of gynecological disorders, and continuous technological advancements in medical devices. Gynecological devices are widely used for diagnosis, monitoring, and treatment of conditions related to the female reproductive system, including uterine fibroids, cervical cancer, and pelvic floor disorders.

The growth of the market can be attributed to the rising demand for minimally invasive procedures, which offer reduced recovery time, lower risk of complications, and improved patient outcomes. In addition, the increasing adoption of advanced diagnostic tools such as hysteroscopes, colposcopes, and endometrial ablation devices is strengthening market expansion across both developed and emerging economies.

Hospitals and specialty clinics continue to represent the largest end-user segment, driven by improved healthcare infrastructure and the availability of skilled medical professionals. Furthermore, favorable government initiatives aimed at improving maternal and reproductive healthcare services are supporting wider access to gynecological treatments.

North America currently holds a significant share of the gynecological devices market due to high healthcare expenditure and early adoption of advanced technologies. Meanwhile, the Asia-Pacific region is expected to register notable growth over the forecast period, supported by a large patient population and increasing investment in healthcare facilities.

Overall, the gynecological devices market is expected to maintain positive momentum, driven by innovation, growing patient awareness, and the global focus on improving women’s healthcare outcomes.

Key Takeaways

- Market Size: The gynecological devices market is projected to reach approximately USD 21.7 billion by 2033, rising from USD 9.7 billion in 2023.

- Market Growth: Market expansion is anticipated at a compound annual growth rate (CAGR) of 8.4% throughout the 2024–2033 forecast period.

- Product Type Analysis: In 2023, the surgical devices segment emerged as the leading category, accounting for 39.4% of total market revenue.

- Application Analysis: The hospitals and clinics segment represented the largest end-user group in 2023, capturing a 55.5% market share.

- Regional Analysis: North America led the global gynecological devices market in 2023, contributing the highest revenue share of 39.7%.

- Technological Advancements: Ongoing innovations in minimally invasive surgical technologies are improving patient recovery outcomes and accelerating device adoption across healthcare settings.

- Market Drivers: Market growth is primarily driven by the increasing demand for personalized treatment solutions and enhanced access to healthcare services.

Regional Analysis

North America Leads the Gynecological Devices Market

North America accounted for the largest share of the gynecological devices market in 2023, generating 39.7% of total revenue. Market leadership is supported by heightened awareness of women’s health, widespread adoption of early diagnostic practices, and a growing aging population, which has increased the demand for advanced diagnostic and therapeutic solutions. Continuous investments in healthcare infrastructure and medical technologies have further enabled the rapid integration of innovative gynecological devices across hospitals and specialty clinics.

Technological innovation remains a key contributor to regional growth. For instance, in March 2022, Endoluxe introduced the Endoluxe eVS, a high-definition wireless endoscopic camera integrated with TowerTech, designed to enhance visualization during gynecological and other surgical procedures. The growing preference for minimally invasive surgeries has also strengthened demand for advanced surgical instruments, supporting improved clinical outcomes and patient recovery.

Asia Pacific Expected to Register the Highest CAGR

The Asia Pacific gynecological devices market is projected to record the highest CAGR during the forecast period, driven by a rising burden of gynecological disorders and increasing awareness of women’s healthcare. Expanding healthcare infrastructure in countries such as India and China is improving access to advanced medical technologies. In September 2022, Olympus Corporation launched the VISERA ELITE III surgical visualization platform, reinforcing regional innovation. Supportive government initiatives focused on women’s health are expected to further accelerate market growth.

Emerging Trends

- Integration of Mobile Technology in Clinical Practice: The adoption of mobile technology in obstetrics and gynecology clinical practice has increased substantially. A survey conducted among obstetrics and gynecology residents in California indicated universal smartphone ownership, with tablet usage reported by approximately three-quarters of respondents. Clinical utilization of these devices was reported by the vast majority of participants, primarily for pregnancy monitoring tools, cervical cancer screening protocols, and contraceptive eligibility reference applications. This trend reflects a growing reliance on digital tools to support clinical decision-making and workflow efficiency.

- Advancements in Minimally Invasive Surgical Techniques: Recent clinical literature demonstrates notable progress in minimally invasive surgical approaches within benign gynecology. These innovations are designed to reduce procedural invasiveness, shorten postoperative recovery periods, and lower complication rates, while maintaining or improving clinical outcomes. The continued evolution of these techniques is contributing to improved patient safety and procedural efficiency.

- Utilization of Big Data for Personalized Gynecological Care: The application of big data and advanced analytics in gynecology is reshaping patient care models. The use of large-scale clinical datasets enables enhanced diagnostic accuracy, individualized treatment planning, and improved patient stratification. This data-driven framework supports more targeted interventions across the continuum of women’s health, leading to improved clinical effectiveness and resource optimization.

Use Cases

- Intrauterine Devices (IUDs) for Contraception: Intrauterine devices are increasingly recognized as an effective and appropriate contraceptive option across diverse patient populations, including adolescents and nulliparous women. Although utilization remains highest among women aged 25–34, clinical acceptance among younger age groups continues to expand. Leading medical authorities, including the American Congress of Obstetricians and Gynecologists and the World Health Organization, recommend long-acting reversible contraceptive methods such as IUDs due to their safety profile, efficacy, and long-term benefits.

- Surgical Mesh in the Treatment of Pelvic Organ Prolapse and Stress Urinary Incontinence: Surgical mesh devices used in the management of pelvic organ prolapse and stress urinary incontinence have undergone extensive clinical evaluation. Evidence derived from multiple randomized controlled trials conducted between 2013 and 2023 indicates that stress urinary incontinence mini-slings demonstrate clinical effectiveness comparable to traditional mid-urethral slings over a 36-month follow-up period. Rates of adverse events and re-intervention were reported to be similar across both treatment modalities.

- Regulatory Oversight of Urogynecologic Surgical Mesh: In response to safety and performance considerations, regulatory oversight of urogynecologic surgical mesh has been strengthened. The U.S. Food and Drug Administration reclassified surgical instrumentation associated with these devices from Class I to Class II, introducing enhanced regulatory controls. This reclassification mandates premarket notification and compliance with defined safety and effectiveness requirements, reinforcing patient protection and product accountability.

Frequently Asked Questions on Gynecological Devices

- What are the commonly used gynecological devices?

Commonly used gynecological devices include hysteroscopes, colposcopes, endometrial ablation systems, vaginal speculums, contraceptive devices, and surgical instruments designed to support minimally invasive diagnostic and therapeutic gynecological procedures. - What are the key applications of gynecological devices?

Gynecological devices are widely applied in routine examinations, fertility treatments, diagnostic imaging, cancer screening, pregnancy-related care, and minimally invasive surgeries, enabling improved clinical outcomes, early disease detection, and enhanced patient safety. - What factors influence the adoption of gynecological devices?

The adoption of gynecological devices is influenced by technological advancements, increasing awareness of women’s health, rising prevalence of gynecological disorders, preference for minimally invasive procedures, and expanding access to advanced healthcare infrastructure globally. - What is driving growth in the gynecological devices market?

Market growth is primarily driven by rising gynecological disorder incidence, increasing demand for minimally invasive surgeries, technological innovations, expanding geriatric female population, and growing healthcare expenditure focused on women’s health management. - Which regions dominate the gynecological devices market?

North America and Europe dominate the gynecological devices market due to advanced healthcare systems, high adoption of innovative technologies, and strong clinical awareness, while Asia-Pacific is witnessing accelerated growth from improving healthcare access. - What are the key trends shaping the gynecological devices market?

Key market trends include the shift toward minimally invasive devices, increased use of disposable instruments, integration of digital imaging technologies, and growing emphasis on outpatient procedures to reduce treatment costs and hospital stays.

Conclusion

The global gynecological devices market is positioned for sustained growth, supported by rising awareness of women’s health, increasing prevalence of gynecological disorders, and continuous technological innovation. Strong demand for minimally invasive procedures has improved clinical outcomes while reducing recovery time and procedural risks.

Hospitals and specialty clinics remain the primary end users, benefiting from advanced infrastructure and skilled professionals. North America continues to lead due to early technology adoption, while Asia Pacific is expected to witness the fastest growth. Overall, innovation, supportive policies, and expanding healthcare access are expected to drive long-term market expansion.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)