Table of Contents

Overview

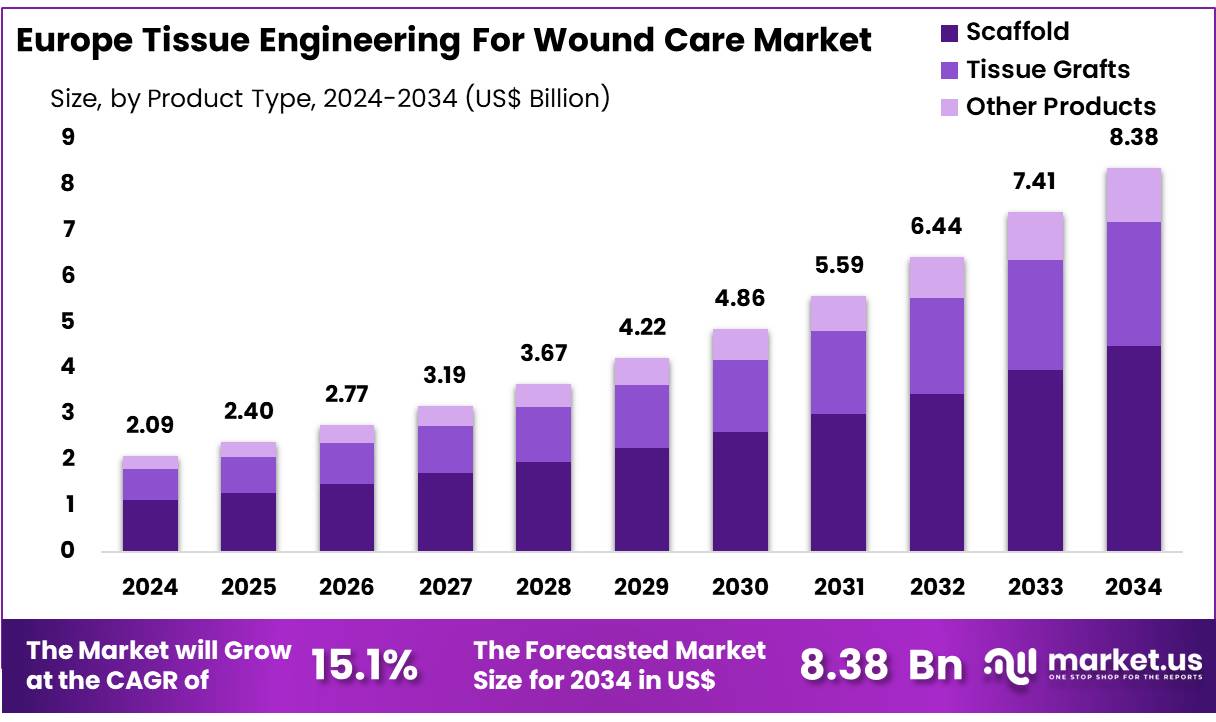

New York, NY – Nov 12, 2025 –The Global Europe Tissue Engineering for Wound Care Market size is expected to be worth around US$ 8.38 Billion by 2034 from US$ 2.09 Billion in 2024, growing at a CAGR of 15.1% during the forecast period 2024 to 2034.

The Europe tissue engineering for wound care market has witnessed substantial advancements, driven by increasing demand for effective regenerative therapies and rising prevalence of chronic wounds. The market is projected to expand steadily due to the growing geriatric population, high incidence of diabetic ulcers, and increasing adoption of bioengineered skin substitutes.

Tissue engineering has emerged as a transformative approach in wound management by integrating cells, biomaterials, and biologically active molecules to promote tissue regeneration and accelerate healing. European healthcare systems are investing significantly in advanced wound care technologies to reduce long-term treatment costs and improve patient outcomes.

Key countries such as Germany, the United Kingdom, France, and Italy are leading in clinical research and the adoption of tissue-engineered products. Regulatory support from the European Medicines Agency (EMA) and ongoing collaborations between biotechnology companies and research institutions are fostering innovation.

The market growth is also driven by an increasing number of clinical trials focusing on stem cell therapy and 3D bioprinting applications for complex wounds. However, high treatment costs and regulatory complexities remain significant challenges.

Overall, the Europe tissue engineering for wound care market is poised for consistent growth, supported by technological innovation, strong R&D pipelines, and growing awareness of advanced wound management solutions. The segment is expected to play a crucial role in shaping the future of regenerative medicine and healthcare sustainability across the region.

Key Takeaways

- In 2024, the Europe Tissue Engineering for Wound Care market generated a revenue of US$ 2.09 billion and is projected to reach US$ 8.38 billion by 2034, registering a CAGR of 15.1%.

- By Product Type: The market is segmented into Scaffold, Tissue Grafts, and Other Products, with Scaffold leading in 2024, accounting for 53.6% of the total market share.

- By Material: The market is divided into Synthetic Material and Biologically Derived Material, among which Biologically Derived Material held a dominant share of 58.3% in 2024.

- By Type of Wound: The market is categorized into Chronic Wounds and Acute Wounds, with the Chronic Wounds segment leading, representing 64.9% of the total revenue.

- By Application: The market is segmented into Skin Regeneration, Bone and Cartilage Regeneration, Soft Tissue Repair, and Organ Regeneration. Skin Regeneration emerged as the largest application segment with a 51.2% share.

- By End-User: The market is classified into Hospitals, Specialty Centers and Clinics, and Ambulatory Surgical Centers, where Hospitals accounted for the largest share of 62.5% in 2024.

Emerging Trends

- Rising Regulatory Submissions: In 2024, seven Marketing Authorisation Applications (MAAs) for advanced therapy medicinal products (ATMPs) were submitted to the European Medicines Agency (EMA), compared with four in 2023. This upward trend indicates growing development momentum and investment in tissue-based therapeutic innovations across Europe.

- Enhanced Scientific Engagement: EMA’s Committee for Advanced Therapies processed 61 scientific-advice requests for ATMPs in 2024, an increase from 57 in 2023. The higher engagement level reflects developers’ proactive efforts to strengthen clinical study design, ensure regulatory compliance, and enhance product quality at early development stages.

- Expansion of PRIME Designations: Six ATMPs were granted PRIME (PRIority MEdicines) status in 2024, highlighting the regulatory emphasis on accelerating access to transformative therapies for unmet medical needs. This initiative reinforces the prioritisation of innovative tissue engineering solutions within the European healthcare ecosystem.

- Broadened Clinical Applications: Recent EMA authorisations demonstrate a diversification of tissue engineering applications. Vyjuvek, approved in April 2025, targets dystrophic epidermolysis bullosa wounds, while Aucatzyl, with a positive opinion in May 2025, addresses B-cell precursor acute lymphoblastic leukaemia. These approvals indicate expanding clinical relevance beyond regenerative wound care to oncology and genetic disorders.

Use Cases

- Corneal Surface Reconstruction (Holoclar): Holoclar, approved in February 2015 as Europe’s first tissue-engineered therapy, enables corneal surface restoration by transplanting cultivated limbal stem cells for patients suffering from ocular burns. It has been used in over 100 patients, significantly reducing repeat surgeries and improving visual outcomes.

- Knee Cartilage Regeneration (MACI): Matrix-Associated Autologous Chondrocyte Implantation (MACI), authorised in June 2013, treats full-thickness cartilage lesions measuring 3–20 cm² in adult knees. In the United Kingdom, an estimated 200–500 patients annually qualify for this treatment, which uses between 500,000 and 1,000,000 autologous chondrocytes per cm² to regenerate durable, hyaline-like cartilage tissue.

- Articular Cartilage Defect Repair (Spherox): Spherox (chondrosphere), approved in July 2017, is indicated for treating symptomatic articular cartilage defects up to 10 cm². Data from German clinical registries show an average treated defect size of 3.7 cm², with 42 % of cases resulting from trauma. The therapy has expanded options for patients with persistent cartilage damage unresponsive to conventional microfracture repair techniques.

Regional Analysis

Key players operating in the Europe Tissue Engineering for Wound Care market include Integra LifeSciences Corporation, Organogenesis Inc., Mimetic Bio, Acelity (now part of 3M), Smith & Nephew, Prent Corporation, Advanced Tissue Sciences (acquired by Stryker), Wright Medical Group N.V. (acquired by Stryker), Molnlycke Health Care, Kerecis, Vericel Corporation, Collagen Matrix, Inc., SyntheMed, Inc. (now part of Allergan), Axolotl Biologix, Tissue Regenix Group PLC, and several others.

Integra LifeSciences Corporation is recognized for its dermal regeneration templates such as Integra, designed for chronic wound management. These templates utilize a scaffold-based system that facilitates tissue growth and healing. Organogenesis Inc. is another major participant offering Apligraf, a living cell-based wound care solution that supports tissue regeneration for chronic ulcers and burn injuries. Kerecis stands out with its innovative fish-skin-based graft technology, which uses natural fish collagen to enhance tissue regeneration and accelerate healing, particularly in chronic wounds.

Frequently Asked Questions on Europe Tissue Engineering for Wound Care

- What is tissue engineering for wound care?

Tissue engineering for wound care refers to the application of scaffold materials, grafts, and biological constructs to promote the repair and regeneration of damaged tissues. These technologies aim to accelerate healing, reduce scarring and provide structural support especially in complex or non-healing wounds. - Why is the Europe region significant for the tissue engineering wound-care sector?

Europe has a significant ageing population and rising incidence of chronic conditions such as diabetes and vascular disease, which increase demand for advanced wound-care therapies. This demographic and clinical profile creates favourable conditions for tissue-engineering solutions in the wound-care segment. - Which product types and materials lead the market segmentation?

In the Europe tissue engineering for wound-care market, scaffolds hold the leading share of product types (around 53.6 % in 2024) and biologically derived materials dominate the materials segment (approximately 58.3 %) owing to their regenerative performance and clinical acceptance. - Which wound types and applications dominate in this market context?

Chronic wounds (including diabetic ulcers, venous ulcers and pressure ulcers) represent the dominant wound-type segment with roughly 64.9 % share in 2024. Skin regeneration is the leading application (around 51.2 %) as it addresses the majority of complex wound cases. - Who are the typical end-users of tissue-engineering wound-care products in Europe?

The primary end-users are hospitals, which held about 51.2 % share in 2024. Additionally, specialty clinics and ambulatory surgical centres are gaining share as outpatient and minimally invasive treatment settings expand for advanced wound-care therapies. - What are the key market trends to watch in Europe?

Key trends include the integration of 3D bioprinting and bioactive scaffolds, personalised regeneration strategies, growing public-private research partnerships, and increasing market focus on home-care and outpatient advanced wound-management models to reduce hospital stays. - What opportunities exist for new entrants or existing players?

Opportunities exist in developing cost-effective biologically derived scaffolds, expanding into under-served geographic segments in Europe, leveraging digital wound-monitoring adjuncts, forming strategic alliances for clinical validation, and targeting chronic-wound segments where unmet need remains high and outcomes can be improved.

Conclusion

The Europe tissue engineering for wound care market is positioned for robust long-term expansion, driven by rising demand for regenerative therapies, strong regulatory support, and technological innovation. Increasing prevalence of chronic wounds, an ageing population, and advancements in biomaterials and cell-based therapies are strengthening market fundamentals.

Ongoing clinical research in 3D bioprinting, stem cell applications, and bioengineered skin substitutes is enhancing treatment efficacy and patient recovery outcomes. Despite cost and regulatory barriers, the region’s collaborative R&D ecosystem and progressive healthcare investments are expected to sustain steady growth, reinforcing Europe’s leadership in regenerative wound care and advanced therapy development.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)