Table of Contents

Overview

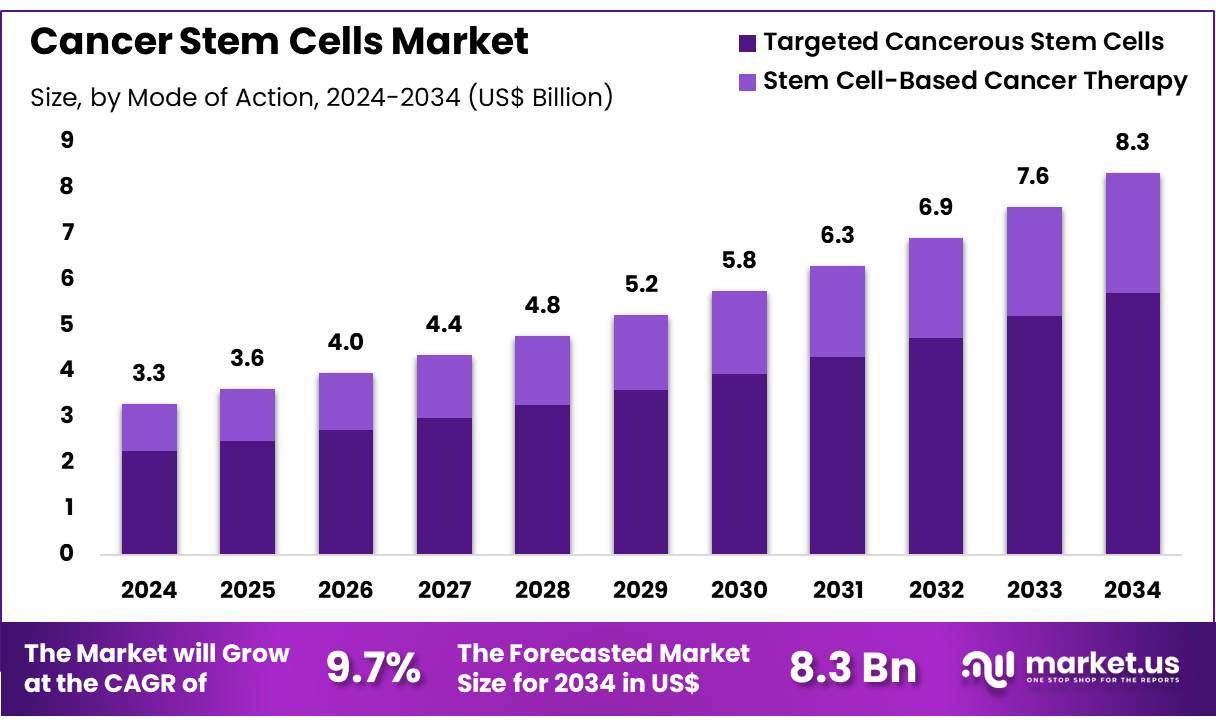

New York, NY – Dec 09, 2025 – Global Cancer Stem Cells Market size is expected to be worth around US$ 8.3 Billion by 2034 from US$ 3.3 Billion in 2024, growing at a CAGR of 9.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.6% share with a revenue of US$ 1.3 Billion.

The formation of Cancer Stem Cells (CSCs) has been recognized as a critical factor in tumor initiation, progression, and therapy resistance. CSCs are defined as a small subpopulation of cells within a tumor that possess self-renewal capabilities and the potential to differentiate into multiple cancer cell types. Their emergence is understood to be driven by a combination of genetic mutations, microenvironmental influences, and dysregulated signaling pathways.

The development of CSCs is believed to begin when normal stem or progenitor cells undergo mutations that alter key regulatory mechanisms. These mutations lead to uncontrolled proliferation, impaired differentiation, and enhanced survival. The tumor microenvironment further contributes to CSC formation through hypoxia, inflammatory signals, and interactions with stromal cells, which collectively support CSC maintenance and expansion.

Several signaling pathways, including Wnt, Notch, Hedgehog, and PI3K/Akt, have been identified as central drivers of CSC behavior. Their persistent activation promotes stemness, metastatic potential, and resistance to conventional treatments. As a result, CSCs have been associated with tumor relapse and reduced therapeutic efficacy.

Growing scientific interest has highlighted the importance of targeting CSCs to achieve long-term cancer control. Research efforts are focused on developing therapies that disrupt CSC signaling, inhibit niche support, or sensitize CSCs to existing treatments. The understanding of CSC formation is expected to support innovative therapeutic strategies and improve clinical outcomes across multiple cancer types.

Key Takeaways

- In 2024, the cancer stem cells market generated revenue of US$ 3.3 billion, and the market is projected to reach US$ 8.3 billion by 2034, driven by a CAGR of 9.7%.

- The mode of action segment is classified into targeted cancerous stem cells and stem cell-based cancer therapy, with the targeted cancerous stem cells segment accounting for 68.5% of the market in 2024.

- Based on cancer type, the market is segmented into breast, pancreatic, and others, with the breast cancer segment holding a dominant 52.3% share.

- North America emerged as the leading regional market, capturing 38.6% of the global share.

Regional Analysis

North America Maintains a Leading Position in the Cancer Stem Cells Market

North America accounted for the largest share of the Cancer Stem Cells Market, representing 38.6% of global revenue. The region’s dominance can be attributed to the rising cancer incidence, strong government support for oncology research, and an active environment for new drug approvals. According to the Centers for Disease Control and Prevention (CDC), the United States reported 1,851,238 new cancer cases in 2022, reflecting a substantial disease burden that continues to drive demand for advanced therapeutic modalities, including those aimed at targeting cancer stem cells, which are recognized for their role in tumor initiation, progression, and recurrence.

Government funding has played a pivotal role in strengthening the research landscape. The National Cancer Institute (NCI) received approximately US$7.22 billion in fiscal year 2024, further supporting basic science initiatives and translational programs that facilitate the development of next-generation cancer treatments. In addition, the U.S. Food and Drug Administration (FDA) sustained a strong pace of oncology drug approvals in 2023 and 2024, reflecting a favorable regulatory environment for innovative cancer therapies that may influence cancer stem cell populations.

Commercial activity in the oncology sector has also supported market expansion. Pfizer reported US$11.63 billion in oncology revenue for 2023, while Merck’s Keytruda generated US$29.48 billion in sales in 2024. These figures illustrate the strong financial momentum within the broader cancer therapeutics landscape, which indirectly supports continued advancements in the understanding and targeting of cancer stem cells.

Asia Pacific Expected to Register the Fastest CAGR During the Forecast Period

The Asia Pacific region is projected to record the highest CAGR in the Cancer Stem Cells Market. This growth is driven by increasing cancer prevalence, substantial healthcare investments, and expanded research and innovation capabilities. China alone reported an estimated 3,246,625 new cancer cases in 2024, highlighting the significant patient pool in the region.

Governments across Asia Pacific continue to prioritize biotechnology and healthcare advancements. In China, public funding for biotechnology including cancer-related research is estimated to have exceeded CNY 20 billion (approximately US$2.6 billion) in 2023, strengthening support for novel therapeutic development. Improvements in diagnostic infrastructure, expanded access to screening programs, and broader public awareness initiatives regarding early cancer detection are further expected to enhance patient identification and treatment eligibility.

The combined efforts of national health agencies and research organizations to address the growing cancer burden are anticipated to accelerate the adoption of advanced therapies targeting cancer-initiating cells. This supportive ecosystem positions Asia Pacific as a high-growth region throughout the forecast period.

Emerging Trends

- Targeting Developmental Signaling Pathways: The inhibition of core developmental pathways including Wnt, Notch, and Hedgehog has been increasingly pursued to eliminate cancer stem cells (CSCs). The suppression of these pathways is intended to disrupt self-renewal mechanisms that maintain CSC populations, thereby lowering the likelihood of tumor recurrence and metastatic progression.

- Plasticity and State Transitions: CSCs have been observed to alternate between proliferative (“plastic”) states and quiescent (“rigid”) states. This dynamic behavior enables adaptation to therapeutic stress, contributing to drug resistance. Current research is directed toward mapping the regulatory molecular networks that control these transitions to identify new therapeutic intervention points.

- Niche-Driven Immunotherapy Resistance: The tumor microenvironment and CSC niche have been linked to reduced responsiveness to immunotherapies. Protective signals from stromal and immune cells can shield CSCs from immune-mediated clearance. Combination strategies that integrate niche-modulating agents with immune checkpoint inhibitors are being evaluated to enhance clinical efficacy.

- Glycosylation as a Functional Indicator: Altered glycosylation profiles on CSC surfaces have been associated with increased stemness, invasiveness, and immune escape. Investigations into CSC-specific glycan patterns are supporting the development of early-stage biomarkers and informing the design of glycan-targeted therapeutic approaches.

Use Cases

- High-Throughput Drug Screening (Phase 0/1 Studies): CSCs are being incorporated into early-phase clinical screening platforms to evaluate the safety and preliminary efficacy of investigational compounds. A Phase 0/1 open-label study, for instance, assessed drug responses across CSC cultures to prioritize candidates for advanced development.

- Active Immunotherapy Investigations (Phase I/II Trials): CSC-derived antigens are being employed in vaccine-based immunotherapy trials at the Phase I/II stage. These programs are designed to induce targeted immune responses against CSC subsets with the objective of reducing minimal residual disease and delaying disease recurrence.

- ChemoID-Guided Chemotherapy Optimization: The ChemoID assay quantifies chemosensitivity in patient-derived CSCs to support personalized chemotherapy selection. Clinical assessments have demonstrated its potential to anticipate patient responses and refine therapeutic decision-making.

- Quantitative CSC Frequency Analysis: CSCs typically represent between 0.05% and 1% of the total tumor cell population. Accurate quantification of this fraction is considered essential for prognosis and treatment planning. High-sensitivity flow cytometry and functional assays are being applied to measure CSC frequency in clinical samples.

Frequently Asked Questions on Cancer Stem Cells

- What are cancer stem cells?

Cancer stem cells are a small, self-renewing population within tumors responsible for initiating cancer growth. These cells possess the ability to differentiate into various cancer cell types, contributing to tumor progression, metastasis, and therapeutic resistance across multiple malignancies. - Why are cancer stem cells important in cancer research?

Cancer stem cells are considered critical because they drive tumor initiation and recurrence. Their unique survival mechanisms allow them to persist after treatment, prompting intensive research into targeted therapies that could eliminate these cells and improve long-term patient outcomes. - How do cancer stem cells contribute to treatment resistance?

Cancer stem cells exhibit enhanced DNA repair ability, slow cell-cycle progression, and strong drug-efflux mechanisms. These characteristics enable them to survive chemotherapy and radiotherapy, resulting in disease relapse and reduced treatment effectiveness in several cancer types. - How are cancer stem cells identified?

Cancer stem cells are identified using specific biomarkers, functional assays, and molecular profiling techniques. Methods such as sphere-forming assays, fluorescence-activated cell sorting, and surface marker evaluation help researchers isolate and characterize these highly resilient tumor-initiating cells. - What therapeutic strategies target cancer stem cells?

Targeted strategies include pathway inhibitors, immunotherapies, and agents disrupting self-renewal mechanisms. These approaches aim to eliminate cancer stem cells more effectively, thereby reducing tumor recurrence and supporting the development of more durable treatment responses in patients. - Which regions dominate the cancer stem cells market?

North America currently dominates the market due to strong research funding, high cancer incidence, and an active drug-approval environment. Asia Pacific is anticipated to experience the fastest growth owing to expanding healthcare investments and rising cancer burden.

Conclusion

The Cancer Stem Cells (CSC) market is advancing due to rising cancer prevalence, strong research initiatives, and increasing investment in targeted therapies. CSCs have been recognized as key drivers of tumor initiation, progression, and treatment resistance, reinforcing the need for innovative therapeutic approaches.

Market expansion is supported by robust funding, active clinical development, and technological improvements in CSC detection and characterization. North America maintains a dominant position, while Asia Pacific is projected to exhibit the fastest growth. Continued focus on CSC-targeted strategies is expected to enhance long-term treatment outcomes and shape the future landscape of oncology.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)