Table of Contents

Overview

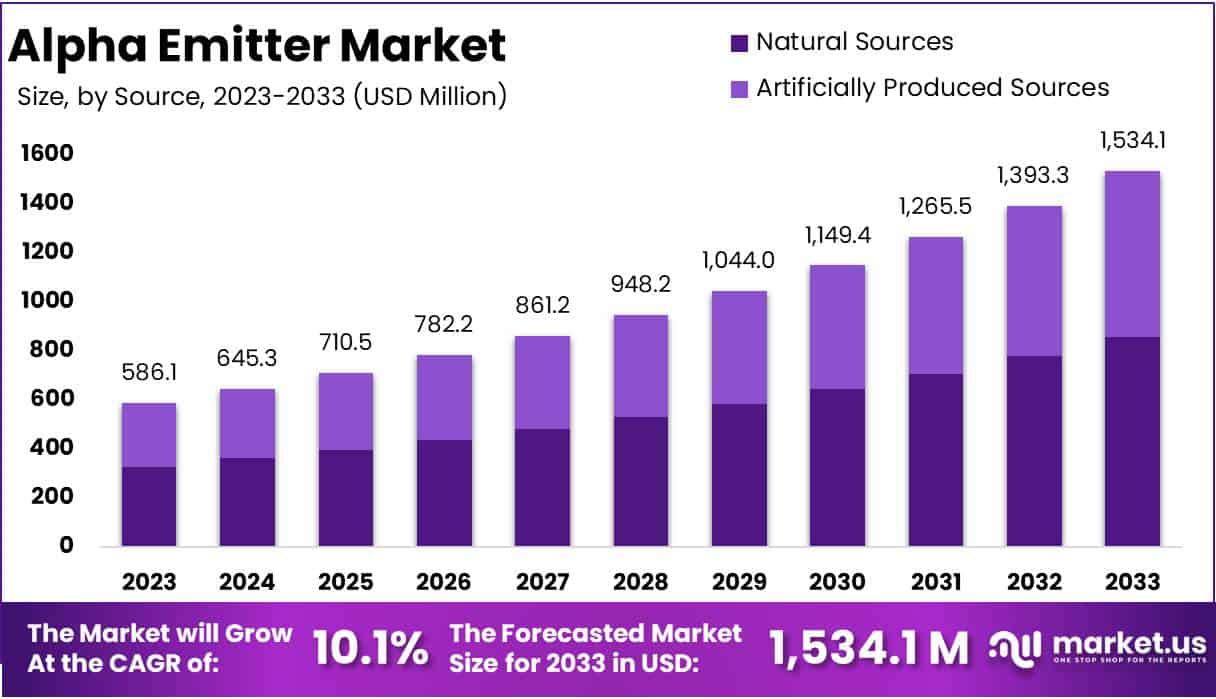

New York, NY – Feb 04, 2026 – The Global Alpha Emitter Market size is expected to be worth around USD 1534.1 Million by 2033, from USD 586.1 Million in 2023, growing at a CAGR of 10.1% during the forecast period from 2024 to 2033.

Alpha emitters are a class of radioactive materials that play a critical role in nuclear science, medical applications, and industrial research. Their formation is a natural consequence of atomic instability in heavy elements.

Alpha emission occurs when an unstable atomic nucleus contains an excess of protons and neutrons. To achieve greater stability, the nucleus releases an alpha particle, which consists of two protons and two neutrons. This process reduces the atomic number by two and the atomic mass by four, resulting in the formation of a new, lighter element. The transformation is governed by well-established principles of nuclear physics and follows predictable decay pathways.

Naturally occurring alpha emitters are commonly found among heavy elements such as uranium, thorium, and radium. These elements were formed during stellar nucleosynthesis and have persisted due to their long half-lives. In addition to natural sources, alpha-emitting isotopes can be produced artificially through nuclear reactors or particle accelerators, where target materials are bombarded with neutrons or other particles to induce nuclear reactions.

The formation and controlled use of alpha emitters are of significant importance. In healthcare, alpha-emitting isotopes are increasingly utilized in targeted radiotherapy due to their high energy and limited penetration range, which allows precise destruction of diseased cells while minimizing damage to surrounding tissue. In industry and research, alpha emitters support material analysis, power generation, and radiation standards.

Key Takeaways

- In 2023, the alpha emitter market generated revenue of USD 586.1 million and is projected to expand at a CAGR of 10.1%, reaching USD 1,534.1 million by 2033.

- By radionuclide type, the market is categorized into Lead-212, Actinium-225, Astatine-211, Radium-223, Bismuth-213, and others. Radium-223 dominated the segment in 2023, accounting for a market share of 23.1%.

- Based on source, the market is segmented into natural sources and artificially produced sources. Natural sources represented a substantial share, contributing 55.9% of total revenue.

- In terms of application, the market includes prostate cancer, bone metastases, pancreatic cancer, ovarian cancer, neuroendocrine tumors, and others. Prostate cancer emerged as the leading application, capturing 35.8% of the overall market revenue.

- By end user, the market is divided into hospitals, diagnostic centers, specialty clinics, and others. Hospitals held the leading position, with a revenue share of 41.7%.

- Regionally, North America dominated the alpha emitter market in 2023, securing a market share of 40.1%.

Regional Analysis

North America accounted for the largest revenue share of 40.1% in the market, primarily driven by the increasing emphasis on strategic collaborations among leading industry participants. For instance, North Star Medical Radioisotopes, a U.S.-based nuclear medicine company, formed a strategic partnership with Inhibrx, Inc., a U.S.-based clinical-stage biotechnology firm, on January 1, 2023. This collaboration aims to accelerate the development of innovative cancer theranostic solutions, reflecting the broader industry trend within the region.

The growing focus on advanced cancer theranostics continues to support market expansion in North America. These next-generation diagnostic and therapeutic approaches depend heavily on alpha-emitting isotopes, thereby increasing their adoption and strengthening regional market growth.

Europe is projected to register the fastest compound annual growth rate over the forecast period. This growth is largely attributed to significant progress in radiopharmaceutical research and development, along with the presence of a substantial number of organizations actively engaged in radiopharmaceutical-based treatment initiatives.

In addition, the high prevalence of cancer across Europe, combined with an aging population seeking more effective and targeted treatment options such as alpha emitters, is expected to further drive market growth in the region.

Emerging Trends

- Expansion of α-Emitting Radionuclide Portfolios: The development pipeline for α-emitting therapies has broadened beyond radium-223 to include isotopes such as actinium-225, astatine-211, thorium-227, bismuth-213, and terbium-149. These radionuclides differ in half-life and α-particle energy (e.g., ^225Ac: 9.9 days; ^223Ra: 11.4 days), enabling more precise matching of radiation properties to tumor size, biology, and residence time requirements.

- Progress in Radiochemistry and Chelation Technologies: Advancements in radiochemistry, particularly the optimization of chelators such as DOTA-based derivatives and engineered targeting vectors, have improved in vivo stability and biodistribution. Preclinical studies have demonstrated tumor retention rates exceeding 80% at 24 hours, alongside reduced off-target radiation exposure.

- Acceleration of α-Emitter Radioligand Therapy: α-emitting radioligand therapies are increasingly being evaluated in solid tumors beyond skeletal metastases. Actinium-225–labeled PSMA ligands for prostate cancer have progressed into Phase I/II clinical trials, with multiple additional studies expected to initiate in 2024. This trend reflects a broader transition toward precision oncology approaches.

- Regulatory Milestones and Clinical Uptake: Radium-223 dichloride remains the only FDA-approved α-emitting therapy since its approval in 2013. In metastatic castration-resistant prostate cancer, it has demonstrated an approximate 3.6-month improvement in overall survival and a 30% reduction in skeletal-related events, supporting its continued clinical adoption.

- Emergence of Combination and Pretargeted Strategies: Combination regimens involving α-emitters and other therapeutic modalities, including immune checkpoint inhibitors, are under active investigation. Pretargeted α-therapy approaches are also being explored to enhance tumor selectivity. Early preclinical models have reported synergistic tumor regression with improved therapeutic indices.

Key Use Cases

- Treatment of Bone Metastases in Prostate Cancer: Radium-223 is widely used in metastatic castration-resistant prostate cancer with bone involvement. More than 95% of its emitted energy is delivered as α particles with a tissue penetration range of less than 100 µm, enabling highly localized cytotoxicity. Clinical data indicate an improvement in median overall survival from 11.3 months to 14.9 months.

- Diffusing Alpha-Emitter Radiation Therapy (DaRT): As of July 2025, at least six clinical trials evaluating DaRT devices are registered across multiple solid tumor indications, including pancreatic, lung, head and neck squamous cell carcinoma, and recurrent malignancies. Individual studies are enrolling up to 100 patients to assess safety, feasibility, and tumor control outcomes.

- α-Emitter PRRT in GEPNENs: Recent clinical investigations of α-emitting peptide receptor radionuclide therapy for gastroenteropancreatic neuroendocrine neoplasms have reported objective response rates above 60% and disease control rates exceeding 80%. These results support the initiation of expanded clinical trials planned for 2025.

- Preclinical Applications in Ovarian Cancer and Glioblastoma: Preclinical DaRT studies in ovarian and glioblastoma mouse models (n = 113 tumors) have demonstrated effective diffusion lengths ranging from 0.2 to 0.7 mm and clearance rates between 10% and 90%. These findings confirm the feasibility of achieving adequate tumor coverage using microcurie-scale dosages.

- PSMA-Targeted α-Therapy in Advanced Prostate Cancer: Early-phase clinical trials of actinium-225–PSMA therapies in metastatic prostate cancer have shown that more than 50% of treated patients achieved prostate-specific antigen reductions of at least 50%. Median overall survival has been estimated at 10–17 months in heavily pretreated populations, with larger Phase II studies ongoing in 2025.

Frequently Asked Questions on Alpha Emitter

- How do alpha emitters differ from beta and gamma emitters?

Alpha emitters release heavy, positively charged particles with limited penetration, unlike beta or gamma radiation. As a result, alpha radiation poses minimal external risk but can be hazardous if inhaled or ingested. - What are common examples of alpha-emitting isotopes?

Common alpha emitters include isotopes such as uranium-238, radium-226, polonium-210, and americium-241. These materials are widely used in nuclear research, smoke detectors, radiotherapy, and scientific instrumentation. - Why are alpha emitters used in medical applications?

Alpha emitters are used in targeted radiotherapy due to their ability to destroy cancer cells with high precision. Their short travel distance limits damage to surrounding healthy tissue, improving treatment efficacy and patient safety. - Are alpha emitters dangerous to human health?

Alpha emitters are considered dangerous only when radioactive material enters the body. Internal exposure can damage biological tissue due to intense ionization, while external exposure is generally considered low risk under regulated conditions. - What factors are driving the growth of the alpha emitter market?

Market growth is driven by rising demand for targeted cancer therapies, increased nuclear research funding, and advancements in radiopharmaceutical production. Expanded applications in oncology are expected to support steady market expansion over time. - Which industries are the primary consumers of alpha emitters?

The healthcare sector represents the largest consumer of alpha emitters, followed by nuclear energy, research institutions, and industrial testing. Demand is largely influenced by clinical trials, diagnostic innovation, and government-funded research programs. - What is the future outlook for the alpha emitter market?

The alpha emitter market is expected to experience moderate but stable growth, supported by oncology innovation and precision medicine trends. Ongoing research investments and expanding therapeutic pipelines are anticipated to create long-term commercial opportunities.

Conclusion

The alpha emitter market is positioned for sustained growth, driven by advances in nuclear medicine, precision oncology, and radiopharmaceutical innovation. Strong clinical evidence supporting targeted alpha therapies, particularly in prostate cancer and bone metastases, continues to reinforce adoption across healthcare systems.

Ongoing expansion of radionuclide portfolios, improvements in radiochemistry, and rising clinical trial activity are expected to broaden therapeutic applications. Regionally, North America maintains leadership through strategic collaborations, while Europe demonstrates high growth potential due to research intensity and demographic trends. Overall, alpha emitters are expected to play an increasingly strategic role in next-generation cancer treatment and nuclear research.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)