Table of Contents

Overview

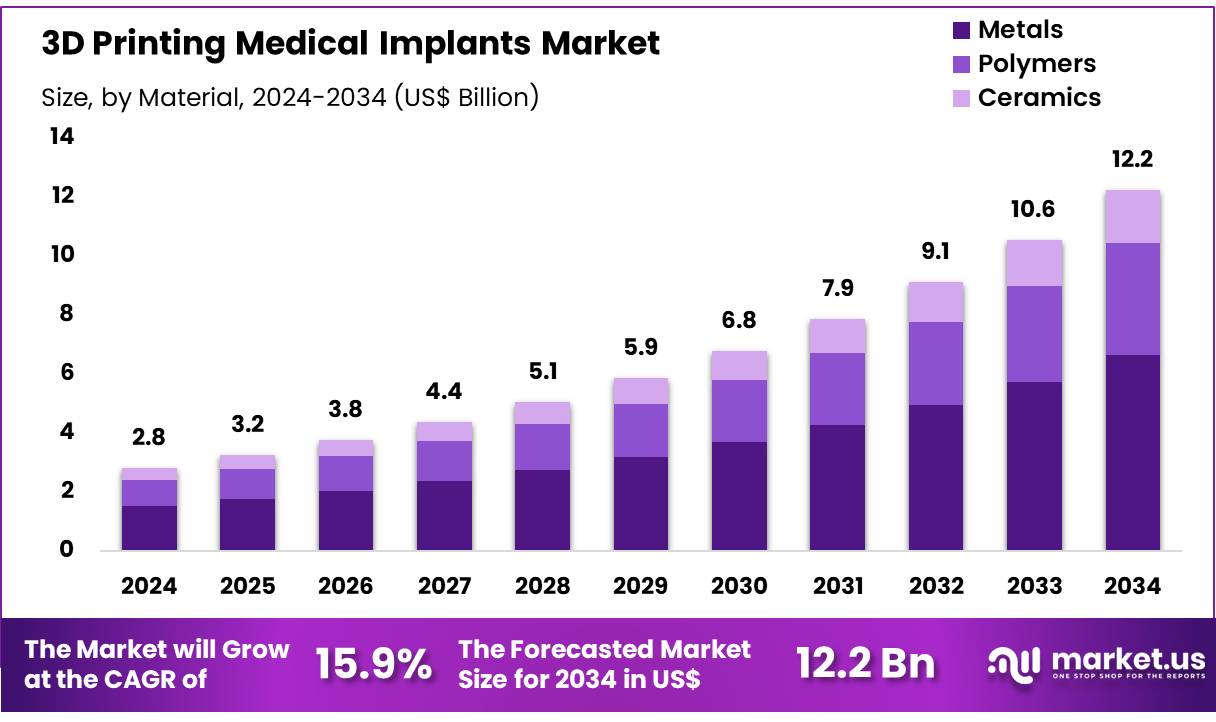

New York, NY – Dec 10, 2025 – Global 3D Printing Medical Implants Market size is forecasted to be valued at US$ 12.2 Billion by 2034 from US$ 2.8 Billion in 2024, growing at a CAGR of 15.9% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 36.6% share with a revenue of US$ 1.0 Billion.

The global 3D printing medical implants market has been witnessing steady expansion as advanced manufacturing technologies are increasingly integrated into healthcare applications. Significant progress in material science, digital modeling, and additive manufacturing processes has enabled the production of patient-specific implants with higher precision and improved clinical outcomes. The demand for customized orthopedic, dental, and craniofacial implants has been rising, as personalized solutions are increasingly preferred in surgical procedures.

Market growth has been supported by the increasing prevalence of chronic conditions, age-related degenerative diseases, and trauma cases requiring reconstructive intervention. The adoption of 3D printing technologies in hospitals and surgical centers has been strengthened by faster prototyping capabilities and reduced production timelines. Regulatory approvals for additively manufactured implants have also expanded, contributing to greater acceptance across global markets.

The cost efficiency associated with on-demand manufacturing has encouraged healthcare providers to integrate 3D printing into treatment workflows. Titanium, stainless steel, and biocompatible polymers have been widely used due to their mechanical strength and compatibility with human tissues. Ongoing research in bioresorbable materials and tissue-engineering scaffolds is expected to widen the application scope over the coming years.

Strategic collaborations between medical device manufacturers, research institutions, and technology firms have further accelerated innovation. Investment in R&D activities has been rising, enabling the development of next-generation implants designed to improve patient recovery and procedural accuracy. The market is expected to maintain an upward trajectory as healthcare systems continue to prioritize personalized treatment, minimally invasive procedures, and advanced implant technologies.

Key Takeaways

- In 2024, the 3D printing medical implants market generated revenue of US$ 2.8 billion, recorded a CAGR of 15.9%, and is projected to reach US$ 12.2 billion by 2034.

- By material, the metals segment led the market with a 54.2% share in 2024.

- Within the application category, the dental segment accounted for the largest share at 36.6% in 2024.

- Laser Beam Melting (LBM) emerged as the leading technology, capturing around 43.0% share in 2024.

- By end user, Hospitals & Surgical Centers dominated the market with a 41.8% share in 2024.

- Regionally, North America represented the largest share of the global market, holding 36.6% in 2024.

Segmentation Analysis

- Material Analysis: The metals category accounted for 54.2% of total market value in 2024. Titanium alloys (Ti-6Al-4V, Ti-6Al-7Nb), cobalt-chromium alloys, and stainless steel remained the predominant materials due to their favorable strength-to-weight ratios, corrosion resistance, and established biocompatibility. Their use enabled the production of precise, patient-specific implant geometries. The adoption of bioactive glass coatings has been associated with improved bone–implant integration and accelerated osseointegration. In parallel, PEEK polymers were utilized for their bone-mimetic mechanical performance, thermal stability, and lower material wastage during additive manufacturing.

- Application Analysis: The dental application segment represented 36.6% of the market in 2024, supported by growing demand for customized crowns, bridges, and implant components. Zirconia ceramics were preferred for their high biocompatibility, aesthetic translucency, and resistance to discoloration, while titanium continued to serve as the benchmark for load-bearing dental implants due to its long-term durability and strong osseointegration profile. Patient-specific designs generated through CT and intraoral imaging contributed to improved fit accuracy and reduced chairside modification. Recent innovations, including translucent alumina orthodontic brackets, illustrated the widening adoption of ceramic-based additive manufacturing in digital dentistry.

- Technology Analysis: Laser Beam Melting (LBM) accounted for 43.0% of the technology share in 2024. Its dominance was attributed to the ability to fully melt metal powders into complex, high-density structures suitable for implantable devices. The technology facilitated the creation of controlled porous lattice architectures that emulate natural bone behavior, thereby mitigating stress shielding and supporting effective osseointegration. Precision in manufacturing was reinforced by the integration of CT and MRI imaging data to produce individualized implant geometries. Clinical studies on LBM-fabricated Ti6Al4V implants with engineered pore structures demonstrated increased cell proliferation and osteogenic activity.

- End-User Analysis: Hospitals and surgical centers were the leading end-user group in 2024, capturing 41.8% of total demand. The deployment of in-house 3D printing capabilities within these facilities enabled the rapid fabrication of patient-specific implants and surgical guides, contributing to improved procedural accuracy and reduced operative time. Initiatives such as the Bristol 3D Medical Centre at North Bristol NHS Trust and the customized surgical guides program at AIIMS Bhopal demonstrated measurable benefits, including reduced complication rates and enhanced postoperative outcomes. These advancements were frequently supported through targeted institutional and government research funding.

Regional Analysis

North America Leading the 3D Printing Medical Implants Market

North America accounted for the largest share of the 3D printing medical implants market, supported by its advanced healthcare infrastructure, strong investment in research and development, and early adoption of innovative medical technologies. The United States remains the primary contributor, driven by the growing emphasis on personalized medicine and the rising need for customized clinical solutions.

According to the American Academy of Orthopaedic Surgeons (AAOS), approximately 700,000 total knee replacement procedures are performed annually in the country. In 2023, Materialise manufactured more than 7,000 patient-specific implants and surgical guides in the U.S. and expanded its capabilities by establishing a new metal 3D printing facility in Michigan. The company also recorded notable growth in the use of its FDA-cleared cranial maxillofacial patient-specific implants for patients affected by cancer and trauma.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to witness the fastest growth during the forecast period. The expansion of healthcare infrastructure, combined with a large and aging population base, has been driving the demand for cost-effective and customized implant solutions. China, India, and Japan are emerging as key markets due to increasing healthcare investments and government initiatives aimed at accelerating the adoption of 3D printing technologies.

In China, government-led innovation programs have strengthened advancements in medical 3D printing, enhancing the country’s leadership position. In India, the rising need for affordable healthcare and the growing utilization of 3D printing in medical procedures have supported rapid market expansion. The country reports an 85% to 95% success rate for spinal fusion surgeries, along with a success rate above 98% for orthognathic procedures used in correcting jaw deformities.

Frequently Asked Questions on 3D Printing Medical Implants

- How are 3D-printed implants manufactured?

The manufacturing process uses digital imaging data to create a patient-specific model, which is then printed using biocompatible materials. The workflow allows high design flexibility, consistent quality, and rapid prototyping, supporting more efficient production compared to traditional implant fabrication methods. - Which materials are commonly used for 3D-printed implants?

Titanium, cobalt-chromium alloys, biodegradable polymers, and bio-ceramics are widely used materials. Their biocompatibility and mechanical strength support safety, performance, and longevity. These materials enable structural stability while promoting tissue integration, making them suitable for diverse orthopedic and dental implant applications. - What are the main benefits of using 3D-printed implants?

The technology enables patient-specific customization, accurate anatomical matching, and reduced intraoperative adjustments. Improved precision and reduced operation times contribute to better surgical outcomes. Production efficiency and material optimization further strengthen the value proposition for healthcare providers and patients. - Are 3D-printed implants considered safe for patients?

Regulatory bodies mandate rigorous evaluation for safety, biocompatibility, and performance. Manufacturers must meet strict standards before approval is granted. Continuous process validation ensures reliability and consistency, contributing to high clinical acceptance and trust in 3D-printed implant solutions. - Which healthcare segments use 3D-printed implants most frequently?

Orthopedics, dental restoration, and craniofacial surgery represent the primary application segments. Their reliance on customized implants and complex geometries encourages adoption. Rising surgical volumes and enhanced procedural precision also contribute to strong utilization across these clinical fields globally. - Which regions dominate the 3D-printed implants market?

North America and Europe maintain leading positions due to advanced healthcare infrastructure, strong regulatory frameworks, and established additive manufacturing ecosystems. Asia-Pacific is experiencing rapid adoption, driven by expanding healthcare investments and increasing demand for modern surgical technologies. - What future trends are expected in this market?

Future growth is expected from biomaterial innovations, increased automation, and integration of artificial intelligence in design processes. Expanding clinical applications and broader acceptance of personalized healthcare solutions are projected to strengthen market penetration over the coming decade.

Conclusion

The global 3D printing medical implants market is expected to maintain strong growth as advancements in additive manufacturing, biomaterials, and personalized medicine continue to accelerate adoption. The market expansion is driven by rising surgical demand, improved clinical outcomes, and increasing integration of patient-specific implant solutions across hospitals and surgical centers.

Metals and dental applications remain dominant, while technologies such as Laser Beam Melting reinforce precision and performance. North America leads in implementation, and Asia Pacific is projected to record the fastest growth. Ongoing R&D investments, regulatory support, and technological innovation are anticipated to strengthen market penetration over the next decade.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)