Table of Contents

Overview

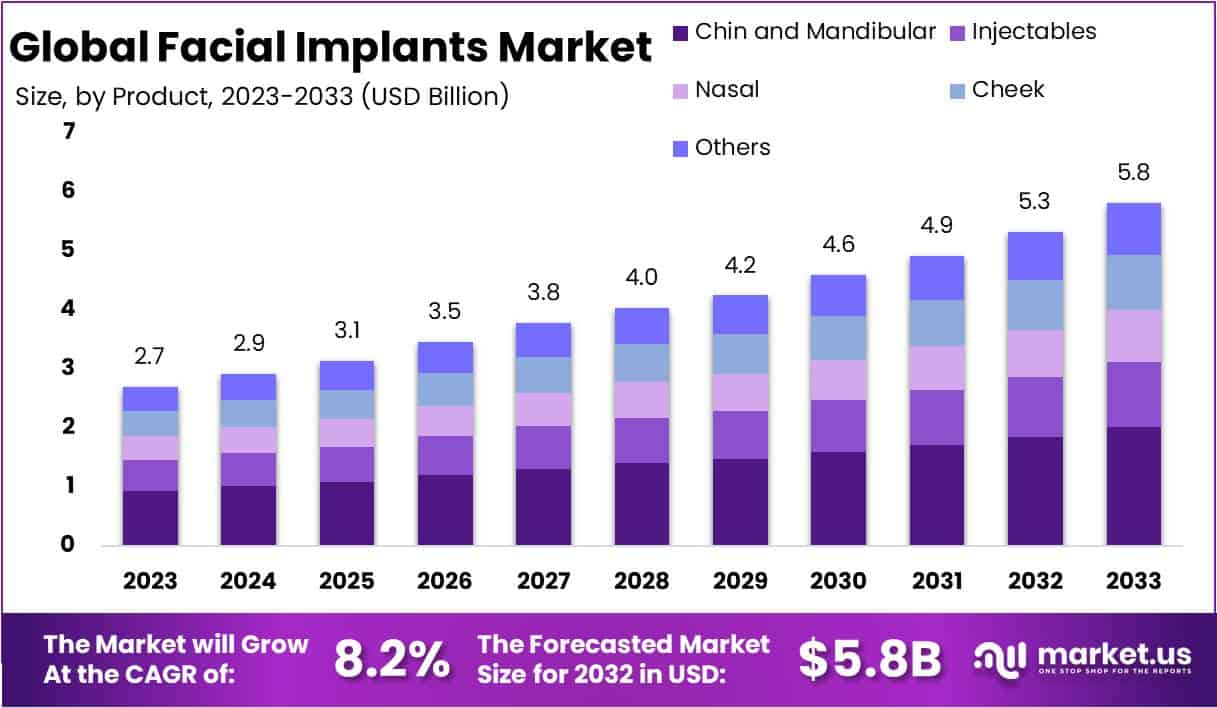

The Global Facial Implants Market is projected to reach approximately USD 5.8 billion by 2033, rising from USD 2.7 billion in 2023, at a CAGR of 8.2%. Market expansion is driven by the ageing population, higher reconstructive needs, and advancements in medical technology. By 2030, one in six people globally will be aged 60 years or older. This demographic shift increases demand for aesthetic and reconstructive facial procedures due to age-related volume loss and bone resorption. The rising older population creates a broad and sustained consumer base for facial implant treatments worldwide.

The growing incidence of trauma and congenital conditions significantly supports the market. Road traffic injuries cause approximately 1.19 million deaths each year, with millions more sustaining facial injuries requiring reconstruction. Expanding trauma care facilities, especially in developing regions, increase the number of eligible surgical patients. Similarly, congenital craniofacial disorders, including orofacial clefts, continue to drive implant use for reconstructive corrections. Improved access to pediatric and neonatal surgery ensures more patients receive timely treatment, thereby supporting consistent procedural volumes and implant adoption across hospitals and specialty clinics.

Cancer-related reconstruction adds another strong demand segment. According to WHO and IARC, cancers of the lip and oral cavity present significant global caseloads. Surgical excision of tumors often requires maxillofacial reconstruction using implants to restore structure and function. With improved early detection and higher survival rates, post-oncologic reconstructive procedures are increasing steadily. Health systems investing in cancer treatment capacity are also expanding reconstructive surgery capabilities, strengthening the role of facial implants in restorative and functional rehabilitation.

Rising global healthcare expenditure further fuels market growth. WHO reported global health spending of about USD 9.8 trillion in 2021, accounting for over 10% of global GDP. Increased spending expands surgical infrastructure, reduces procedure backlogs, and supports elective and medically necessary surgeries. Simultaneously, advances in 3D printing and customization technologies enhance surgical precision and patient outcomes. Regulatory guidance from the U.S. FDA on additive manufacturing and silicone elastomer implants has improved product quality and physician confidence, encouraging broader adoption of standardized, patient-specific implants.

Clear regulatory standards ensure device safety and traceability, reinforcing market stability. Regular FDA 510(k) clearances indicate continuous innovation in implant design and material development. Improved design controls, labeling standards, and post-market surveillance have strengthened hospital confidence in facial implant systems. As healthcare access expands globally, demand for reconstructive and aesthetic procedures continues to rise. Supported by demographic, clinical, and technological factors, the facial implants market is expected to maintain a robust growth trajectory through 2033.

Key Takeaways

- The global facial implants market is projected to reach USD 5.8 billion by 2033, registering an impressive compound annual growth rate of 8.2%.

- In 2023, chin and mandibular implants accounted for more than 34.7% of total revenue, indicating strong consumer preference for facial structure enhancement.

- Polymers emerged as the leading material segment with a 39% market share in 2023, valued for their lightweight, flexible, and durable properties.

- Eyelid surgery represented the most preferred procedure, capturing 41% of the market in 2023, highlighting growing interest in subtle facial rejuvenation.

- Market expansion is primarily driven by evolving beauty standards, technological innovation in materials, and increasing demand among the aging demographic.

- High procedure costs, postoperative complications, limited insurance coverage, and persistent social stigma continue to restrict the market’s broader adoption.

- Untapped emerging markets, rising customization trends, and integration of 3D printing technology present lucrative opportunities for future growth.

- Industry dynamics are shaped by a shift toward non-invasive solutions, demand for natural results, and advancements in bioabsorbable implant technologies.

- In 2023, North America led with a 38% share, supported by high disposable incomes, advanced healthcare infrastructure, and aesthetic awareness.

- Regions such as Europe and Asia-Pacific are witnessing rapid growth, fueled by evolving aesthetic preferences and increasing healthcare access.

Regional Analysis

In 2023, North America dominated the Facial Implants Market, holding a share exceeding 38%. The regional market was valued at USD 1.02 billion, highlighting its strong position and influence. This dominance was driven by growing aesthetic awareness and a rising preference for facial enhancement procedures. The high acceptance of cosmetic surgeries and a developed healthcare infrastructure further strengthened North America’s standing, making it the leading contributor to global market revenues.

The region’s market growth was also influenced by advancements in implant materials and surgical technologies. Continuous innovation, supported by strong research and development efforts, has enhanced the safety and precision of facial implants. The presence of major industry players has encouraged competition, fostering product diversification and the adoption of advanced implant solutions. Such developments have enabled the region to maintain a technological edge and attract a wide consumer base seeking aesthetic improvements.

Economic stability and high disposable income levels across North America have significantly supported market expansion. Consumers in the region show greater willingness to spend on facial aesthetic procedures, viewing them as lifestyle investments. Accessibility to specialized healthcare services and well-established cosmetic clinics has further contributed to market penetration. These factors collectively position North America as a lucrative hub for facial implant manufacturers and service providers.

Although North America remains dominant, other regions such as Europe and Asia-Pacific are gaining momentum. The growth in these markets is driven by changing beauty standards, increased healthcare awareness, and a growing focus on personal appearance. Rising affordability and medical tourism are also accelerating adoption. To sustain competitiveness, market players must closely monitor evolving regional trends, ensuring strategic investments that align with shifting consumer preferences and technological advancements in facial aesthetics.

Segmentation Analysis

In 2023, the Facial Implants market was led by the Chin and Mandibular segment, which held a share of over 34.7%. The segment’s dominance reflects the growing demand for facial enhancement procedures that redefine and contour the face. Injectables also played a major role due to their non-invasive and quick results. Their accessibility and safety have made them a preferred choice among individuals seeking facial augmentation. Nasal and cheek implants further contributed to the market’s diversity, offering refined and youthful facial enhancements.

The market, by material, was dominated by Polymers, accounting for more than 39% share in 2023. Their versatility, lightweight nature, and durability made them ideal for facial reconstruction and aesthetics. Biological materials followed closely due to their biocompatibility and natural integration with tissues. Metal-based implants maintained a strong market presence, offering structural strength and long-lasting results. Ceramics, though smaller in share, gained attention for their natural bone-like appearance. Together, these materials supported a wide range of patient needs and surgeon preferences.

In terms of procedures, Eyelid Surgery held the largest market share of over 41% in 2023, driven by rising demand for rejuvenation and correction of sagging or puffy eyelids. Facelift procedures followed, emphasizing comprehensive facial improvement and anti-aging effects. Rhinoplasty also held a significant share as consumers increasingly sought facial balance and symmetry. Other emerging procedures catered to niche aesthetic goals, contributing to market diversity. This growing procedural variety reflects evolving consumer preferences and advancements in cosmetic technologies.

Key Players Analysis

Stryker Corporation has established a strong foothold in the facial implants market through its advanced technological expertise and wide product portfolio. The company’s focus on continuous research and development supports innovation in facial implant design, ensuring superior outcomes for patients. Its strategic initiatives and investments in precision-driven solutions strengthen its global position. Stryker’s emphasis on customized and patient-specific implants enhances procedural efficiency and safety, positioning it as a market leader driving innovation and quality advancement across the facial implant industry.

Hanson Medical Inc. demonstrates a notable presence in the market with its dedication to precision manufacturing and high-quality implant production. The company’s commitment to superior design standards and patient satisfaction reinforces its brand reliability. By focusing on durable materials and advanced fabrication processes, Hanson Medical ensures the creation of implants that meet diverse clinical needs. Its focus on surgical accuracy and post-procedure outcomes underscores its contribution to improved facial reconstruction and enhancement practices across global healthcare systems.

Integra LifeSciences continues to play a key role in expanding the facial implants landscape through its comprehensive and diversified product offerings. The company’s extensive portfolio addresses various reconstructive and aesthetic requirements. Strategic collaborations and technological advancements have enhanced its ability to meet evolving patient and surgeon demands. With a strong international presence and focus on R&D, Integra LifeSciences has strengthened its market influence, promoting innovation and accessibility in facial augmentation procedures across multiple regions.

Zimmer Biomet stands out for its extensive experience, innovation-driven strategies, and patient-centric approach. The company’s global footprint and robust product range contribute significantly to market expansion. Zimmer Biomet emphasizes safety, precision, and biocompatibility, aligning with regulatory standards and clinical needs. Alongside key players such as Depuy Synthes, KLS Martin Group, Xilloc, Medartis AG, and OsteoMed, it supports a competitive ecosystem that fosters continuous innovation, improved surgical outcomes, and long-term patient satisfaction in the global facial implants market.

Conclusion

The global facial implants market is expected to show steady growth over the coming years, supported by an aging population, rising reconstructive needs, and rapid medical technology development. Increasing demand for aesthetic enhancement and reconstructive surgeries continues to strengthen the market outlook. Advances in 3D printing, customized implant design, and biocompatible materials are improving treatment outcomes and patient satisfaction. Although high costs and limited insurance coverage pose challenges, emerging markets and growing cosmetic awareness present strong opportunities. With continued innovation and wider healthcare access, the facial implants market is projected to maintain a positive and sustainable growth path globally.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: inquiry@market.us

View More

Craniomaxillofacial Devices Market | Facial Injectable Market | Craniofacial Implants Market | Facial Fat Injections Market | Acne Treatment Market | Acne Scar Treatment Market | Acne Medicine Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)