Table of Contents

Overview

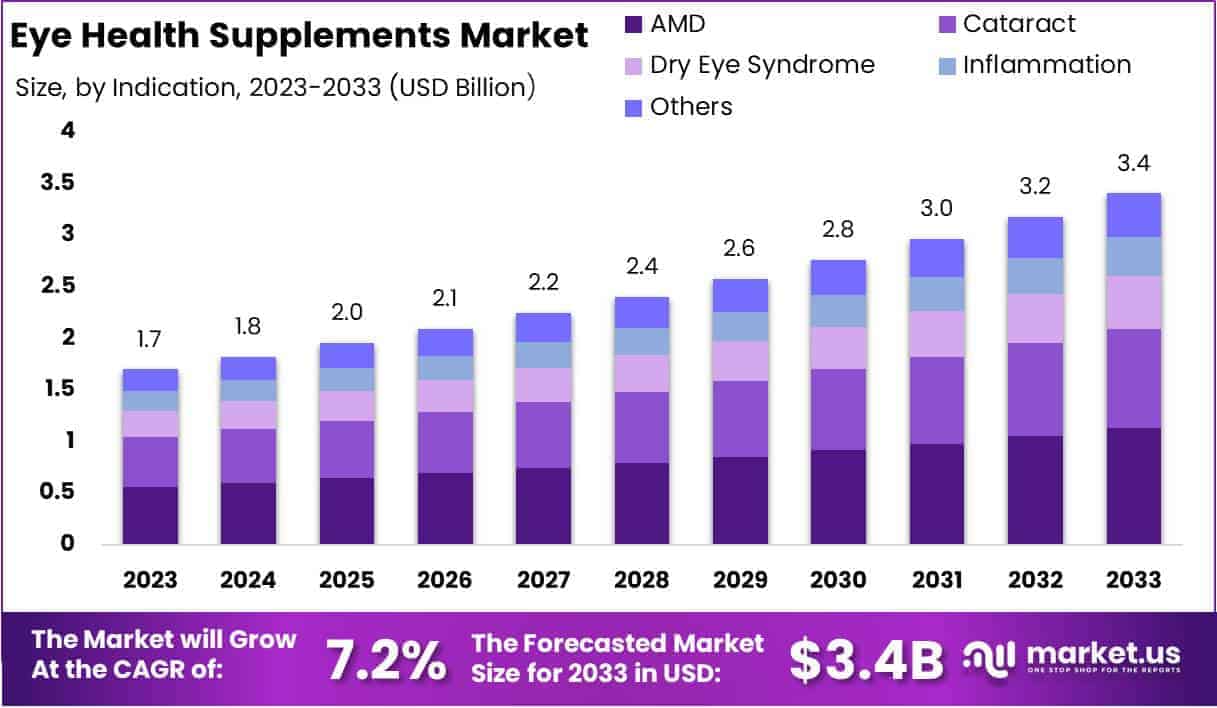

New York, NY – May 22, 2025 – The Global Eye Health Supplements Market size is expected to be worth around USD 3.4 Billion by 2033, from USD 1.7 Billion in 2023, growing at a CAGR of 7.2% during the forecast period from 2024 to 2033.

The global eye health supplements market is witnessing sustained growth, driven by increasing awareness about preventive eye care and the rising prevalence of age-related vision disorders. These supplements rich in antioxidants, vitamins, and minerals such as lutein, zeaxanthin, vitamin A, and omega-3 fatty acids are widely used to support visual function and reduce the risk of conditions such as macular degeneration, cataracts, and dry eye syndrome.

The growth of the geriatric population, combined with prolonged screen exposure across age groups, has further elevated the demand for eye health products. According to recent data from the World Health Organization (WHO), over 2.2 billion people globally suffer from some form of vision impairment, with at least 1 billion cases considered preventable or treatable. This has intensified consumer interest in dietary supplements as a proactive vision care strategy.

Retail pharmacies, online platforms, and health stores remain key distribution channels, with e-commerce gaining strong traction post-pandemic due to convenience and broader accessibility. North America currently leads the market due to high consumer health awareness and advanced healthcare infrastructure, while Asia-Pacific is expected to register the fastest growth. Ongoing product innovations, supported by clinical research and clean-label formulations, are enhancing consumer confidence and driving market expansion. The eye health supplements sector is poised for continued advancement over the coming decade.

Key Takeaways

- The global Eye Health Supplements Market is expected to grow from USD 1.7 billion in 2023 to USD 3.4 billion by 2033, registering a CAGR of 7.2%, primarily driven by an aging population and increased screen time.

- Lutein and Zeaxanthin accounted for the largest share (34.1%) in the ingredient type segment in 2023, supported by their established role in preventing age-related macular degeneration (AMD) and cataracts.

- Age-related Macular Degeneration (AMD) emerged as the leading indication segment, representing 33.1% of the market, due to rising elderly populations and increasing awareness of preventive eye care.

- Tablets represented the dominant formulation, holding a 31.2% market share in 2023, favored for their convenience, affordability, and user preference.

- North America led the global market with a 38.5% share in 2023, attributed to heightened health awareness, strong regional industry presence, and emphasis on preventive healthcare practices.

Segmentation Analysis

- By Ingredient Type: In 2023, Lutein and Zeaxanthin led the Eye Health Supplements Market with a 34.1% share, supported by their clinical efficacy in preventing AMD and cataracts. Antioxidants followed at 21.5%, driven by their ability to reduce oxidative stress. Omega-3 Fatty Acids held 17.8% due to benefits in retinal health and dry eye relief. Other segments include CoQ10 (9.3%), Flavonoids (6.2%), Alpha-Lipoic Acid (5.1%), Astaxanthin (3.8%), and Others (2.2%), reflecting a diverse demand for specialized eye health nutrients.

- By Indication: Age-related Macular Degeneration (AMD) dominated the market in 2023, accounting for 33.1% of the share, driven by aging populations and preventive care awareness. Cataract followed at 25.4%, supported by rising UV exposure and lens aging. Dry Eye Syndrome held 21.8%, fueled by digital screen use and environmental stressors. Inflammation contributed 12.3%, reflecting demand for anti-inflammatory nutrients. The remaining 7.4% was captured by the Others category, including glaucoma and diabetic retinopathy, showing niche but growing supplement adoption.

- By Formulation: Tablets led the formulation segment in 2023 with a 31.2% market share due to their convenience and low cost. Capsules followed at 26.8%, appreciated for ease of use and nutrient bioavailability. Powdered supplements accounted for 18.5%, favored for dosage flexibility. Softgels, at 14.7%, were popular for lipid-based ingredients. Liquid forms held 6.3%, often preferred by children and seniors. The Others segment, including gummies and chewables, contributed 2.5%, targeting consumers seeking more appealing and innovative supplement formats.

Market Segments

Ingredient Type

- Lutein & Zeaxanthin

- Antioxidants

- Omega-3 Fatty Acids

- Coenzyme Q10

- Flavonoids

- Alpha-Lipoic Acid

- Astaxanthin

- Others

By Indication

- Age-related Macular Degeneration (AMD)

- Cataract

- Dry Eye Syndrome

- Inflammation

- Others

By Formulation

- Tablets

- Capsules

- Powder

- Softgels

- Liquid

- Others

Regional Analysis

The Eye Health Supplements Market demonstrates varied regional dynamics, with North America leading in 2023 by accounting for 38.5% of the global market share, equivalent to a valuation of USD 0.654 billion. This dominance is attributed to heightened awareness of eye health and the strong presence of key industry participants actively promoting supplement use.

In Europe, market growth is primarily driven by an aging population that is increasingly affected by age-related eye disorders. The availability of targeted supplements addressing conditions such as dry eye syndrome and age-related macular degeneration further supports demand.

The Asia Pacific region is experiencing rapid expansion, fueled by rising healthcare spending and growing public awareness of preventive eye care. Large populations and a rising incidence of vision-related conditions in countries like China and India are significantly contributing to market growth.

Meanwhile, the Middle East & Africa and Latin America are showing steady development. Increased health consciousness, urbanization, rising disposable incomes, and improvements in healthcare infrastructure are making eye health supplements more accessible to a broader consumer base in these emerging regions.

Emerging Trends

- Evidence-Based Formulations for AMD: It has been observed that specialized dietary supplements based on the Age-Related Eye Disease Studies (AREDS and AREDS2) are increasingly adopted to slow progression of intermediate age-related macular degeneration (AMD). Long-term data indicate that the benefits of these formulations persist for at least ten years following initiation.

- Growing Preventive Demand Driven by AMD Prevalence: With an estimated 19.8 million (12.6 %) Americans aged 40 and older living with AMD in 2019, there has been heightened interest in preventative supplementation among both patients and clinicians.

- Heightened Focus on Dry Eye Management: The prevalence of dry eye disease has been reported at 2.7 % among adults aged 18–34, rising to 18.6 % in those 75 and older. This age-related increase is driving interest in supplements—particularly omega-3 fatty acids and vitamin A—to support tear film stability and ocular surface health.

- Global Vitamin A Supplementation in Childhood: In regions with high rates of vitamin A deficiency, an estimated 250 000–500 000 preschool children become blind annually due to xerophthalmia. Public health programs that deliver large-dose vitamin A supplementation (e.g., 100 000–200 000 IU every 4–6 months) have been shown to prevent new cases of blindness and reduce mortality.

Use Cases

- Slowing AMD Progression in Older Adults: Approximately 1.49 million (0.94 %) Americans aged ≥40 were living with vision-threatening AMD in 2019. AREDS2 supplements are recommended for individuals with intermediate AMD to delay progression to advanced stages. Long-term studies report sustained benefit over ten years.

- Supporting Tear Film in Dry Eye Disease: In the U.S., up to 43.8 % of adults aged 60–79 experience dry eye syndrome. Oral omega-3 supplementation has been studied for its role in improving tear production and reducing inflammation, while vitamin A support is indicated in clinical deficiency. Such interventions are being integrated into management plans for older adults.

- Preventing Childhood Xerophthalmia: Global health initiatives have delivered vitamin A supplements to 59 % of targeted children under five years of age. Large-dose supplementation has reduced Bitot’s spots by 58 %, night blindness by 68 %, and xerophthalmia by 69 % in high-risk populations.

- Public Health Screening and Supplement Referral: Ophthalmology clinics and community health centers are incorporating vision screening data—such as the 12.6 % AMD prevalence among adults ≥40—to identify candidates for nutritional intervention. Referral pathways for AREDS2 supplements and dietary counseling are being formalized in care protocols.

Conclusion

The global Eye Health Supplements Market is poised for steady expansion, driven by rising awareness of preventive eye care and the growing burden of age-related vision disorders. Key ingredients such as lutein, zeaxanthin, omega-3 fatty acids, and antioxidants are gaining widespread use in managing conditions like AMD, cataracts, and dry eye.

With strong demand across regions, particularly in North America and Asia Pacific, and supported by public health initiatives and evidence-based formulations, the market is expected to grow significantly. Continued innovations and targeted supplementation strategies will further enhance visual health outcomes and support long-term market sustainability.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)