Table of Contents

Overview

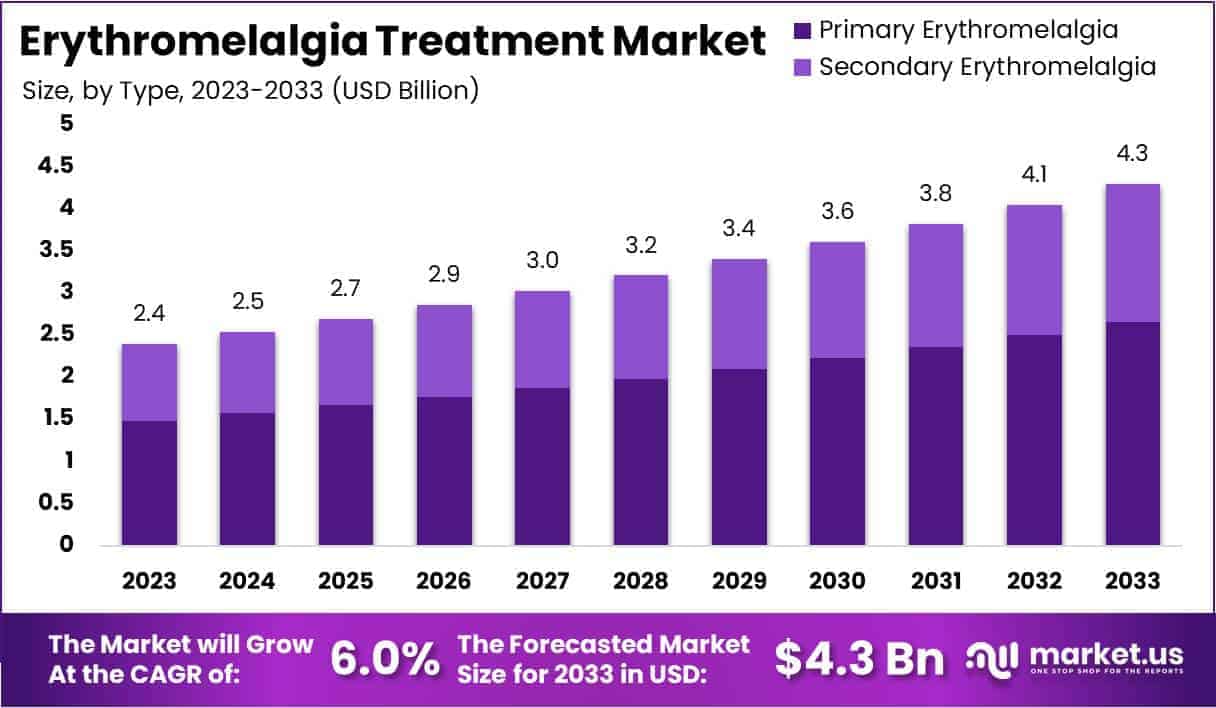

New York, NY – July 17, 2025 – The Global Erythromelalgia Treatment Market Size is expected to be worth around USD 4.3 Billion by 2033, from USD 2.4 Billion in 2023, growing at a CAGR of 6% during the forecast period from 2024 to 2033.

Erythromelalgia, a rare neurovascular condition marked by episodes of burning pain, redness, and warmth in the extremities, continues to challenge patients and healthcare providers due to its complex etiology and limited treatment options. The condition is often triggered by heat, exertion, or stress and is associated with primary genetic mutations or secondary causes such as autoimmune disorders and myeloproliferative diseases.

Current treatment strategies for erythromelalgia focus on symptom management rather than cure. Topical agents such as lidocaine, capsaicin, and amitriptyline creams are commonly used to provide localized pain relief. Systemic therapies include gabapentin, pregabalin, and tricyclic antidepressants, which aim to modulate nerve signaling and reduce neuropathic pain. For severe cases, sodium channel blockers like mexiletine and intravenous infusions of lidocaine or ketamine have shown partial effectiveness.

Emerging therapies are exploring targeted mechanisms, including the use of selective Nav1.7 sodium channel blockers, currently under clinical investigation, which could provide more personalized relief. Non-pharmacological approaches such as cooling measures, biofeedback, and lifestyle modifications remain essential adjuncts to pharmacotherapy.

As awareness and understanding of erythromelalgia improve, collaborative efforts between clinicians, researchers, and patient advocacy groups are expected to drive innovation in treatment approaches. Continued research and clinical trials are crucial to develop effective, safe, and long-term management strategies for this debilitating condition.

Key Takeaways

- The erythromelalgia treatment market is anticipated to expand from USD 2.4 billion in 2023 to USD 4.3 billion by 2033, registering a CAGR of 6.0% during the forecast period.

- In 2023, the primary erythromelalgia segment accounted for the largest share of 61.8%, largely attributed to the prevalence of idiopathic cases with unclear underlying causes.

- The medication segment emerged as the dominant treatment category, securing a 72.7% market share in 2023. Commonly prescribed therapies include nonsteroidal anti-inflammatory drugs (NSAIDs) and aspirin.

- Oral administration remains the preferred route of drug delivery, holding 67.9% of the market share in 2023. This dominance is supported by patient convenience and adherence.

- Hospitals represented over 40% of the end-user market share in 2023, benefiting from their ability to provide multidisciplinary care and specialized erythromelalgia treatment protocols.

- Retail pharmacies led the distribution channel segment, capturing a 43.9% share due to broad accessibility, over-the-counter availability, and consumer convenience.

- North America dominated the regional landscape in 2023, accounting for 37% of global revenue, equivalent to approximately USD 0.9 billion. This leadership is supported by well-established healthcare systems and early adoption of therapeutic advancements.

Segmentation Analysis

- Type Analysis: In 2023, primary erythromelalgia led the market with a 61.8% share, driven by the increasing prevalence of idiopathic cases. This type is marked by unexplained burning pain and redness in the extremities, requiring ongoing clinical attention. Advancements in genetic research have further supported targeted treatment approaches. In contrast, secondary erythromelalgia linked to conditions like autoimmune or myeloproliferative disorders shows potential for future growth as awareness and diagnostic precision for underlying causes continue to improve.

- Treatment Analysis: The medication segment dominated the treatment landscape in 2023, capturing over 72.7% of the market. Widely used drugs such as NSAIDs and aspirin offer symptom control and easy accessibility. This segment benefits from continued R&D investment to enhance drug efficacy and discover new therapies. In contrast, surgical interventions like sympathectomy are limited to severe cases but are expected to gain traction with advancements in minimally invasive techniques and improved patient outcomes in refractory conditions.

- Route of Administration Analysis: Oral administration held the dominant position in 2023 with a 67.9% market share, attributed to high patient compliance and convenience. The segment also benefits from advancements in drug formulation technologies that increase oral bioavailability. While less prominent, the topical route remains valuable for localized symptom relief with fewer systemic side effects. Its growth is supported by research into novel delivery systems. Overall, the market is shifting toward patient-centric solutions supported by regulatory approvals and formulation innovation.

- End-User Analysis: Hospitals led the end-user segment in 2023, accounting for over 40% of the market due to their comprehensive services and specialized treatment protocols. Their capacity to manage complex cases with multidisciplinary teams enhances patient outcomes. Specialty clinics followed closely, offering expertise in personalized care. Homecare services are increasingly favored for long-term management, especially for patients requiring convenience and continuity. Other end-users, including outpatient centers, are gradually expanding to meet growing demand for accessible and cost-efficient care.

- Distribution Channel Analysis: Retail pharmacies dominated the distribution channel in 2023 with a 43.9% share, attributed to their accessibility and role in frontline pain management. These outlets often provide essential guidance and medication availability, supporting high patient engagement. Hospital pharmacies, while critical for inpatient care, held a smaller share due to outpatient-oriented treatments. Online pharmacies are emerging strongly, driven by rising e-commerce use and the demand for home delivery. This trend is expected to continue, especially in post-pandemic healthcare ecosystems.

Market Segments

Type

- Primary Erythromelalgia

- Secondary Erythromelalgia

Treatment

- Medication

- Surgery

Route of Administration

- Oral

- Topical

End-User

- Hospitals

- Homecare

- Specialty Clinics

- Others

Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Regional Analysis

In 2023, North America led the erythromelalgia treatment market, securing over 37% of the global share, equivalent to a market value of USD 0.9 billion. This leadership is attributed to the region’s advanced healthcare infrastructure, widespread awareness of erythromelalgia, and ready access to treatment options. Additionally, significant investments in pharmaceutical research and development, particularly in the United States and Canada, continue to strengthen the region’s position in the global market.

Europe followed closely, supported by rising healthcare expenditures and the increasing prevalence of autoimmune disorders common triggers for secondary erythromelalgia. Well-established healthcare frameworks and supportive policies in key countries such as Germany, the United Kingdom, and France further facilitate market expansion across the region.

Asia-Pacific is projected to register the fastest growth during the forecast period. Factors such as improved healthcare infrastructure, heightened disease awareness, and the rising incidence of erythromelalgia-related conditions are driving regional demand. Moreover, growing healthcare investments in developing economies like China and India are expected to fuel significant market advancements.

Latin America and the Middle East & Africa are anticipated to experience moderate growth. These regions are witnessing gradual improvements in healthcare delivery and treatment accessibility, supported by government-led initiatives aimed at enhancing public health outcomes and infrastructure development.

Emerging Trends

- Selective Nav1.7 Ion Channel Blockade: Novel oral agents targeting the voltage gated sodium channel Nav1.7 have entered clinical testing. In a Phase 2a crossover study of vixotrigine (BIIB074), eight adults with primary inherited erythromelalgia received three daily doses for four weeks. Although no significant pain reduction was seen at the dose tested (mean weekly pain score change of –0.05 on BIIB074 vs –1.37 on placebo), the study established safety and tolerability, paving the way for dose optimization trials.

- Neuromodulation via Spinal Cord and Dorsal Root Ganglion Stimulation: Case reports and small series have demonstrated that electrical stimulation of the spinal cord or dorsal root ganglia can markedly reduce refractory burning pain. For example, a 21 year old man with a nine year history of severe limb pain achieved substantial relief using high frequency, paresthesia free dorsal column stimulation. This trend reflects growing interest in minimally invasive neuromodulation as part of a multimodal pain regimen.

- Immunomodulatory Therapy for Secondary Forms: In patients with erythromelalgia secondary to autoimmune or hematologic disorders, intravenous immunoglobulin (IVIG) has shown promise. A 49 year old woman with a 16 year history of refractory symptoms received IVIG at 400 mg/kg/day for five days every month over six months. Complete resolution of pain and erythema was reported, with no recurrence at 18 months follow up. This suggests that adaptive immune mechanisms may be targeted in selected cases.

Use Cases

- Vixotrigine (BIIB074) Phase 2a Trial: In a randomized, double blind, crossover study (NCT02917187), eight adults received vixotrigine 3 times daily for four weeks. Pain was measured weekly on a 0–10 scale. The mean change was –0.05 with vixotrigine versus –1.37 with placebo, indicating the need for further dose and population refinement.

- High Frequency Spinal Cord Stimulation: A single patient case involved a 21 year old male with nine years of refractory erythromelalgia. After implantation of a paresthesia free dorsal column stimulator, pain episodes decreased by an estimated 70%, enabling return to daily activities within three months.

- Intravenous Immunoglobulin in Secondary EM: A 49 year old woman with sporadic erythromelalgia underwent six monthly cycles of IVIG (400 mg/kg/day for five days). Complete relief of burning pain and erythema was achieved by month 6, and no flare was observed at 18 month follow up.

- Dorsal Root Ganglion Stimulation in Pediatric EM: In a pediatric case series, dual lead DRG stimulators were implanted in a teen with primary erythromelalgia. Eight months post implantation, the patient reported >60% reduction in daily pain scores and no device related complications.

Conclusion

The global erythromelalgia treatment market is undergoing steady expansion, driven by rising awareness, improved diagnostics, and evolving therapeutic strategies. While current management remains largely symptomatic, advancements in pharmacologic research, neuromodulation techniques, and immunomodulatory therapies are paving the way for more targeted and effective interventions.

North America leads the market, supported by robust healthcare infrastructure, with Asia-Pacific showing the fastest projected growth. Ongoing clinical trials and innovative case applications highlight the potential of emerging treatments. As research efforts intensify, the market is expected to offer more personalized and sustainable solutions, ultimately improving patient outcomes in this challenging condition.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)