Table of Contents

Overview

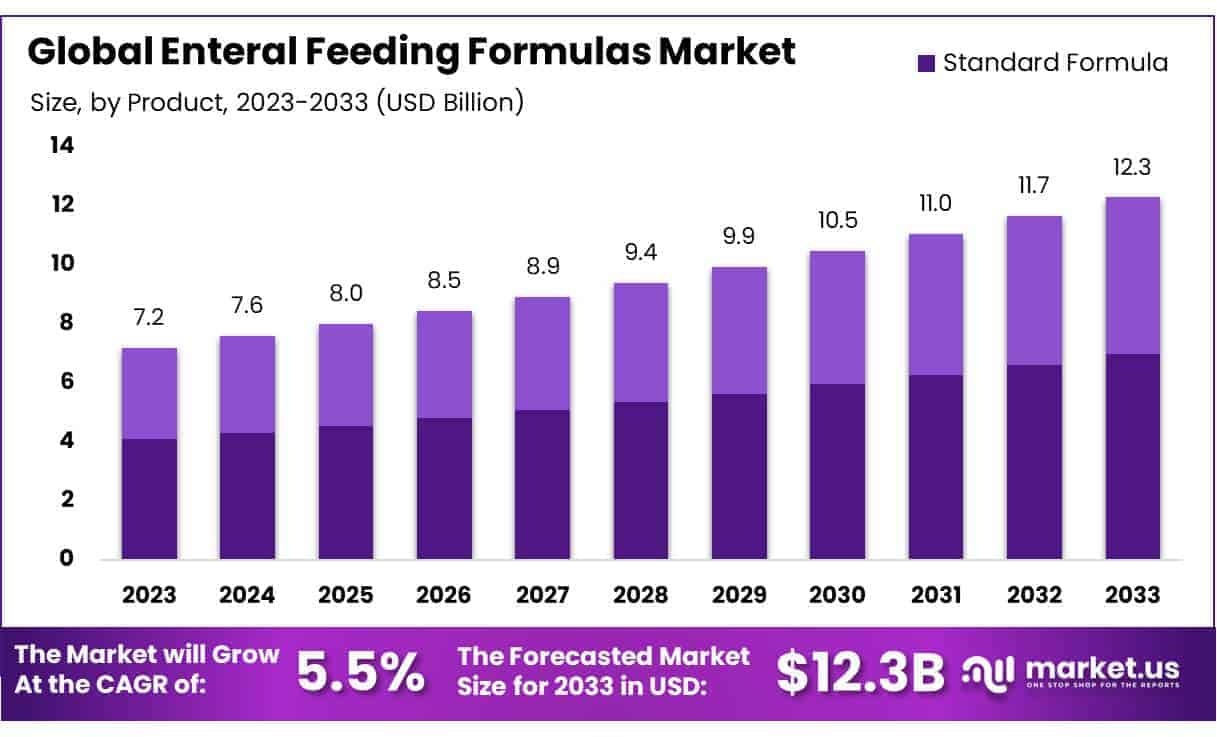

New York, NY – July 16, 2025 – Global Enteral Feeding Formulas Market size is expected to be worth around USD 12.3 billion by 2033, from USD 7.2 billion in 2023, growing at a CAGR of 5.5% during the forecast period from 2023 to 2033.

The global enteral feeding formulas market is experiencing steady growth, fueled by the increasing prevalence of chronic diseases, expanding aging population, and rising demand for clinical nutrition support. Enteral feeding formulas are specially designed liquid nutrition products administered via feeding tubes to individuals who are unable to consume food orally. These formulas are essential for maintaining adequate nutrition in patients with conditions such as cancer, neurological disorders, gastrointestinal dysfunction, and post-surgical recovery.

Standard polymeric formulas continue to dominate the market, widely used for general nutritional needs across hospital and home care settings. However, there is a growing demand for disease specific and peptide based formulas, driven by the need for tailored nutritional therapy in complex medical cases.

Hospitals remain the primary end-users, although the adoption of home enteral nutrition is rising due to improved tube feeding devices, caregiver training, and the growing emphasis on cost effective long-term care.

Geographically, North America leads the market due to advanced healthcare infrastructure and high awareness of enteral therapy. The Asia-Pacific region is projected to witness the fastest expansion, supported by healthcare reforms, increased diagnosis rates, and greater investment in clinical nutrition.

Innovations in product formulation such as fiber enriched blends, immunonutrition, and prebiotic/probiotic combinations are expected to enhance therapeutic outcomes. As the focus on patient centric care and personalized nutrition intensifies, the enteral feeding formulas market is poised for continued growth across various care settings.

Key Takeaways

- Market Growth Outlook: The global enteral feeding formulas market is projected to grow significantly, expanding from 2023 to 2033 at a compound annual growth rate (CAGR) of 5.5%. This growth is supported by increasing healthcare needs and rising demand for clinical nutrition.

- Dominance of Standard Formulas: Standard enteral formulas accounted for 56.8% of the market in 2023. These formulations remain the preferred option for general nutritional support in patients without specific medical conditions.

- Prevalence of Intermittent Feeding: Intermittent feeding emerged as the most utilized feeding type in 2023, capturing over 89% market share. This method is well-suited for patients who can tolerate larger volumes per feeding session.

- High Usage Among Adults: Adults represented the primary user group in 2023, holding a market share of 90.4%, attributed to the widespread prevalence of malnutrition and gastrointestinal disorders in this demographic.

- Leading Indication Segment – ‘Others’: The ‘Others’ category led the indication segment, accounting for 37% of the market in 2023. This reflects the diverse and specialized nutritional requirements of many patients.

- Institutional Sales Channel Strength: Institutional settings, such as hospitals and long-term care facilities, accounted for 51.6% of market sales, emphasizing the importance of monitored nutrition delivery.

- Shift Toward Home-Based Care: Home care usage surpassed 61.4% in 2023, indicating a growing trend toward home-based patient management and self-administered nutritional support.

- Asia-Pacific Market Leadership: The Asia-Pacific region led the global market with a 48% share in 2023. Factors such as an aging population and rising rates of chronic diseases contributed significantly to this regional dominance.

Segmentation Analysis

Product Analysis: In 2023, standard formulas led the enteral feeding formulas market with a 56.8% share due to their wide use in patients without specific dietary needs. These formulas provide essential nutrition and are favored in both hospital and home settings. Meanwhile, disease-specific formulas addressed targeted nutritional needs for conditions such as diabetes and renal disorders. Their precise compositions supported better health outcomes for patients with chronic illnesses, driving steady demand in specialized clinical applications.

Flow Type Analysis: Intermittent feeding dominated the market in 2023 with over 89% share, favored for its compatibility with patients who can tolerate larger volumes in spaced intervals. This method enhances digestion and mimics normal meal patterns. In contrast, continuous feeding is used for patients needing steady, slow nutrient delivery, often in intensive care or with compromised gastrointestinal function. The segmentation reflects growing customization of feeding methods based on patient tolerance and underlying health conditions.

Stage Analysis: Adults accounted for 90.4% of the enteral feeding formulas market in 2023, reflecting the high incidence of malnutrition and gastrointestinal conditions among aging populations. Their significant share is attributed to broader clinical applications and increased chronic disease management. While the pediatric segment was smaller, it showed promising growth due to rising diagnosis rates and awareness around congenital and developmental disorders requiring enteral nutrition, leading to increased demand for age-specific, nutrient-dense formulas.

Indication Analysis: The “Others” category led indication-based segmentation in 2023 with a 37% share, covering diverse and complex nutritional needs outside standard classifications. Cancer care represented a significant portion, driven by the high use of enteral feeding during treatment. Indications such as Alzheimer’s, chronic kidney disease, and diabetes followed closely. Emerging areas like dysphagia, GI disorders, and orphan diseases attracted attention due to targeted product innovation and the rising need for specialized nutritional support.

Sales Channel Analysis: Institutional sales dominated in 2023, accounting for 51.6% of the market, primarily through hospitals and clinics where monitored nutritional care is essential. Retail channels followed closely, supported by growing caregiver demand for convenient access through pharmacies and health stores. Online sales, while smaller, showed strong momentum due to increasing consumer preference for e-commerce, home delivery, and broad product selection. The multichannel approach supports diverse access to enteral formulas across professional and consumer markets.

End-use Analysis: Home care led the market in 2023, capturing over 61.4% share, reflecting a shift toward patient-managed nutrition outside traditional clinical environments. This trend is supported by cost-efficiency, convenience, and advancements in enteral feeding technology. Hospitals remained vital, particularly in critical care and oncology departments, where close monitoring is required. The evolving preference for home-based care signifies a transformation in enteral nutrition delivery, aiming for improved quality of life and resource optimization across care settings.

Market Segments

By Product

- Standard Formula

- Disease-specific Formulas

By Flow Type

- Intermittent Feeding Flow

- Continuous Feeding Flow

By Stage

- Adults

- Pediatrics

By Indication

- Alzheimer’s

- Nutrition Deficiency

- Cancer Care

- Diabetes

- Chronic Kidney Diseases

- Orphan Diseases

- Dysphagia

- Pain Management

- Malabsorption/GI Disorder/Diarrhea

- Others

By End-use

- Hospitals

- Cardiology

- Neurology

- Critical Care (ICU)

- Oncology

- Home Care

By Sales Channel

- Online Sales

- Retail Sales

- Institutional Sales

Regional Analysis

In 2023, the Asia-Pacific (APAC) region emerged as the leading market for enteral feeding formulas, accounting for over 48% of the global market share. This leadership is primarily driven by the rising incidence of chronic illnesses such as cancer and gastrointestinal disorders, combined with the region’s rapidly aging population particularly in countries like Japan and China.

Government-backed initiatives to strengthen healthcare infrastructure, along with supportive reimbursement frameworks, are further accelerating market adoption. Additionally, increasing awareness among healthcare professionals and patients regarding the benefits of enteral nutrition is fostering growth in the region.

North America also holds a significant share in the global market, supported by a well-established healthcare system, high healthcare spending, and a growing elderly population. The widespread prevalence of chronic conditions, including diabetes and cancer, continues to drive demand for enteral nutrition. Moreover, advancements in feeding technologies and the growing trend of home-based healthcare further enhance market potential.

In Europe, strong healthcare systems and a high burden of chronic diseases especially in Germany, France, and the United Kingdom contribute substantially to market expansion. Meanwhile, Latin America and the Middle East & Africa are witnessing steady growth, supported by rising healthcare investments, improved access to nutritional therapies, and increasing acceptance of clinical nutrition solutions.

Emerging Trends

- Proliferation of Formula Options: It has been observed that, over the past 25 years, the number and variety of enteral feeding formulas have increased dramatically. Well over 100 distinct formulas are now available, enabling more precise matching of patient needs to formula composition.

- Variation in Caloric Density: It is noted that enteral formulas now commonly range from 1.0kcal/mL to 2.0kcal/mL. This flexibility allows clinicians to tailor energy provision to individual energy requirements, such as providing higher density feeds for patients with fluid restrictions.

- Early Initiation and Goal Oriented Delivery: Clinical practice guidelines recommend that enteral nutrition be initiated within 48 hours of intensive care admission, with an aim to achieve at least 90 % of calculated nutritional targets. Such prompt, goal oriented feeding has been associated with reduced muscle wasting and preservation of mucosal integrity.

- Increased Use of Specialized Additives: The inclusion of specialized components such as soluble and insoluble fiber, medium chain triglycerides, and immunonutrients (e.g., omega 3 fatty acids, glutamine) is becoming more widespread. These additives are intended to support gut health, modulate immune response, and reduce inflammation, particularly in critically ill and oncology patients.

- Expansion of Home Based Nutrition Coverage: Policy updates have standardized reimbursement for home enteral nutrition. For example, Medicare’s supply allowance permits one unit of enteral formula per day, reflecting a trend toward supporting long term outpatient and home administration to reduce hospital stays.

Use Cases

Critical Care Nutrition: Enteral feeding is routinely employed in intensive care units for patients unable to eat by mouth. Approximately 38% of ICU patients are moderately to severely malnourished on admission, and up to 69% experience further nutritional decline without support. Early enteral feeding blunts the catabolic response, reducing infection risk and shortening length of stay.

Stroke Related Dysphagia Management: Dysphagia occurs in 20.7% of acute stroke patients and persists in over half of those cases at discharge. Of these dysphagic patients, about 30.5% require nasogastric tube feeding to maintain adequate nutrition and prevent complications such as aspiration pneumonia and further functional decline.

Neurological Disorders with Swallowing Impairment: Enteral nutrition is often indicated for conditions that impair swallowing such as amyotrophic lateral sclerosis, Parkinson’s disease, and severe traumatic brain injury. By providing complete macro and micronutrients, enteral formulas support lean body mass maintenance and improve overall clinical outcomes.

Oncology and Cachexia Support: In patients with head and neck cancers or gastrointestinal malignancies, enteral feeding formulas are used to counteract treatment‑related anorexia and cachexia. Immunonutrition enriched formulas have been shown to reduce postoperative infection rates and support wound healing, although exact percentages vary by protocol.

Pediatric and Geriatric Home Care: Long term home enteral nutrition is essential for children with congenital metabolic disorders and older adults with chronic dysphagia. Standard protocols deliver 1–2 kcal/mL formulas via gastrostomy tubes, ensuring growth and functional preservation. Home administration reduces hospitalization needs and improves quality of life.

Conclusion

The global enteral feeding formulas market is poised for sustained growth, driven by the increasing prevalence of chronic diseases, an aging population, and rising demand for personalized nutritional support. Advancements in formula development, home-based care adoption, and favorable reimbursement policies are transforming clinical nutrition delivery across regions.

With Asia-Pacific leading in market share and North America and Europe showing steady progress, the market reflects a strong shift toward patient-centric, long-term nutritional care. Emerging trends such as immunonutrition, goal-directed feeding, and expanded use cases in critical and home care settings will continue to shape the market’s future trajectory.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)