Table of Contents

Overview

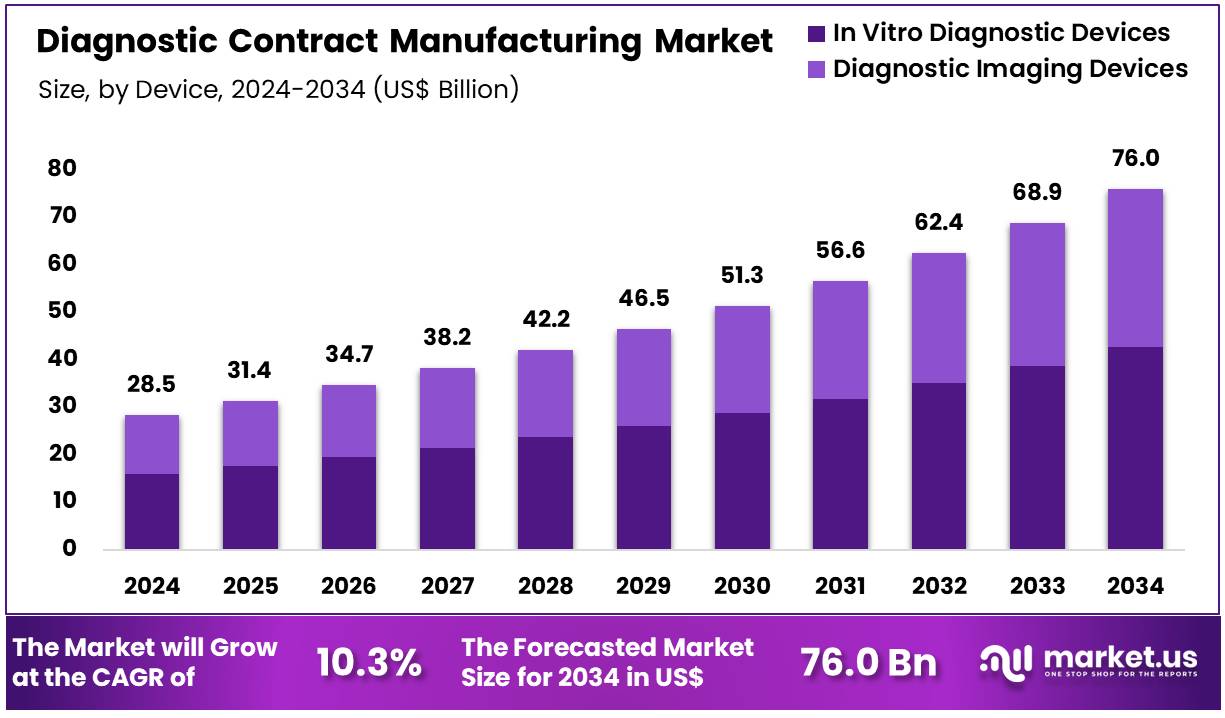

New York, NY – Dec 08, 2025 – Global Diagnostic Contract Manufacturing Market size is expected to be worth around US$ 76.0 Billion by 2034 from US$ 28.5 Billion in 2024, growing at a CAGR of 10.3% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 44.4% share with a revenue of US$ 12.6 Billion.

A strategic advancement in the diagnostic manufacturing landscape has been announced with the establishment of a specialized Diagnostic Contract Manufacturing platform designed to support the growing demand for high-quality, scalable, and compliant diagnostic solutions. The formation of this unit has been driven by the rising need for rapid development, efficient production, and reliable outsourcing partnerships across the global healthcare ecosystem.

The platform has been structured to provide end-to-end capabilities, including assay development, reagent formulation, device fabrication, and large-scale assembly. The integration of advanced manufacturing technologies and strict quality-management systems ensures that the production of diagnostic products is aligned with global regulatory standards. Emphasis has been placed on ISO-certified processes, automated workflows, and rigorous validation protocols to ensure accuracy, reliability, and batch-to-batch consistency.

The expansion of contract manufacturing services is expected to support diagnostic companies seeking to accelerate time-to-market while reducing operational costs. The growth of the market has been attributed to the rising prevalence of infectious diseases, increased adoption of point-of-care testing, and continuous innovation in molecular and immunodiagnostic technologies. Demand for flexible manufacturing capacity has increased significantly, creating opportunities for partnerships in both established and emerging markets.

The newly formed division is positioned to collaborate with diagnostic developers, biotechnology firms, and healthcare organizations to advance next-generation diagnostic solutions. Its establishment is expected to strengthen supply-chain resilience, enhance manufacturing scalability, and contribute to improved patient outcomes through broader access to reliable diagnostic products.

Key Takeaways

- The global diagnostic contract manufacturing market was valued at USD 28.5 billion in 2024 and is projected to reach USD 76.0 billion by 2034, reflecting a CAGR of 10.3%.

- The in vitro diagnostic devices segment dominated the market in 2024, accounting for 56.2% of the total revenue.

- The cardiology segment emerged as the leading application area, contributing 38.2% of the total revenue share.

- The diagnostic laboratories segment held the largest share of the end-use market, representing 65.3% of global revenue.

- North America maintained its leading regional position with a revenue share exceeding 44.4%.

Regional Analysis

The global diagnostic contract manufacturing market has been experiencing accelerated expansion, driven by rising demand for advanced diagnostic solutions and increasing outsourcing activities by healthcare companies. The market was valued at USD 28.5 billion in 2024 and is projected to reach USD 76.0 billion by 2034, reflecting a strong 10.3% CAGR over the forecast period. This growth has been supported by the expanding need for high-quality diagnostic devices, cost-efficient production models, and rapid technological innovation in the healthcare sector.

In 2024, the in vitro diagnostic (IVD) devices segment emerged as the dominant product category, accounting for 56.2% of total revenue. Its prominence can be attributed to the increasing use of IVD devices in disease detection, personalized medicine, and routine health monitoring. The cardiology application segment also held a significant position, capturing 38.2% of the overall market share due to the rising global burden of cardiovascular diseases.

From an end-use perspective, diagnostic laboratories accounted for 65.3% of the total revenue, reflecting the growing dependence on outsourced diagnostic services for enhanced operational efficiency. Regionally, North America maintained its leading position with a 44.4% revenue share, supported by advanced healthcare infrastructure, high adoption of diagnostic technologies, and the presence of major industry players.

Overall, the diagnostic contract manufacturing market continues to show robust potential, driven by technological advancements and increasing global healthcare needs.

Use Cases

- Rapid COVID-19 Test Kit Production: Large-scale production of molecular diagnostic kits was enabled through contract manufacturing during the early phase of the pandemic. More than 50 million molecular test kits were filled and labeled between April and December 2020 to support national testing capacity. Flexible manufacturing lines allowed next-day production scale-ups, ensuring uninterrupted supply for public health laboratories across the country.

- Multiplex Respiratory Panels for Surveillance: Contract manufacturers are involved in producing multiplex respiratory panels designed to detect multiple pathogens in a single assay. Participation in CLRN’s SARS-CoV-2 Proficiency Test Program increased by over 400% by mid-2021, reflecting the rising demand for comprehensive surveillance tools. These panels support simultaneous detection of influenza A/B, RSV, and SARS-CoV-2, reducing laboratory labor and reagent costs by up to 30%.

- Genomic Sequencing Kits for Outbreak Response: The CDC’s AR Lab Network redirected sequencing resources to strengthen COVID-19 genomic surveillance. Contract manufacturers provided more than 5,000 customized library preparation kits in 2020, enabling the sequencing of 4,700 SARS-CoV-2 genomes. These kits were supplied with pre-aliquoted reagents and barcoding primers, allowing decentralized laboratories to join national sequencing activities quickly.

- Emergency Stockpile Maintenance: Strategic stockpiles of diagnostic reagents are supported through ongoing contract manufacturing under HHS agreements. A CDC cooperative agreement allocated $2.1 billion through the Coronavirus Response and Relief Supplemental Funds to strengthen national detection capacity, including the replenishment of reagent buffers and controls. This framework ensures that critical diagnostic components can be mobilized within days during future public health emergencies.

Frequently Asked Questions on Diagnostic Contract Manufacturing

- Why do companies outsource diagnostic manufacturing?

Diagnostic companies outsource to reduce production costs, increase scalability, and access advanced technologies. Outsourcing supports faster market entry, mitigates supply chain risks, and allows companies to focus on innovation, assay development, and commercialization activities without heavy manufacturing infrastructure requirements. - What services are typically offered by diagnostic contract manufacturers?

These manufacturers provide services such as assay development, reagent production, device assembly, packaging, sterilization, labeling, and quality testing. Integrated capabilities are offered to support end-to-end development and manufacturing needs across molecular, immunoassay, clinical chemistry, and point-of-care diagnostics. - Which diagnostic products are commonly manufactured under contract?

Products include lateral flow assays, molecular diagnostics kits, ELISA kits, PCR consumables, biosensors, clinical chemistry reagents, and point-of-care testing devices. Manufacturers support both high-volume production and specialized small-batch runs to meet diverse client requirements. - What quality standards govern diagnostic contract manufacturing?

Manufacturers typically operate under ISO 13485, FDA 21 CFR Part 820, and other regional regulatory standards. These frameworks ensure that diagnostic products meet safety, performance, and traceability requirements essential for clinical use and global market approvals. - What are the cost advantages of diagnostic contract manufacturing?

Outsourcing reduces capital expenditure related to equipment, labor, and facility maintenance. The model improves operational efficiency, supports flexible production volumes, and helps companies optimize overall manufacturing cost structures while maintaining high-quality outputs and regulatory compliance. - What is driving growth in the diagnostic contract manufacturing market?

Market growth is driven by rising demand for advanced diagnostics, increasing prevalence of chronic diseases, expansion of point-of-care testing, and strong outsourcing trends. Manufacturers’ investments in automation and high-throughput technologies further support sustained industry expansion. - Which regions dominate the diagnostic contract manufacturing market?

North America and Europe dominate due to established diagnostic industries, strong regulatory frameworks, and high adoption of outsourced manufacturing. Asia-Pacific is rapidly emerging as a competitive region driven by cost-efficient production and expanding healthcare infrastructure. - What technological trends are shaping the market?

Automation, microfluidics, high-throughput production systems, and digital quality management platforms are shaping the market. These technologies improve manufacturing efficiency, reduce errors, and support scalable production of advanced diagnostic kits and instruments.

Conclusion

The diagnostic contract manufacturing market is projected to demonstrate sustained expansion as demand for advanced, scalable, and cost-efficient diagnostic solutions continues to rise. Growth has been supported by increasing outsourcing activities, strong adoption of IVD technologies, and the need for rapid, compliant production capabilities.

The formation of specialized manufacturing platforms is expected to strengthen supply-chain resilience, enhance operational efficiency, and accelerate time-to-market for diagnostic innovators. With North America maintaining a leading position and emerging regions gaining momentum, the market is positioned for continued advancement, driven by technological innovation and the global shift toward high-quality outsourced diagnostic manufacturing.