Table of Contents

Introduction

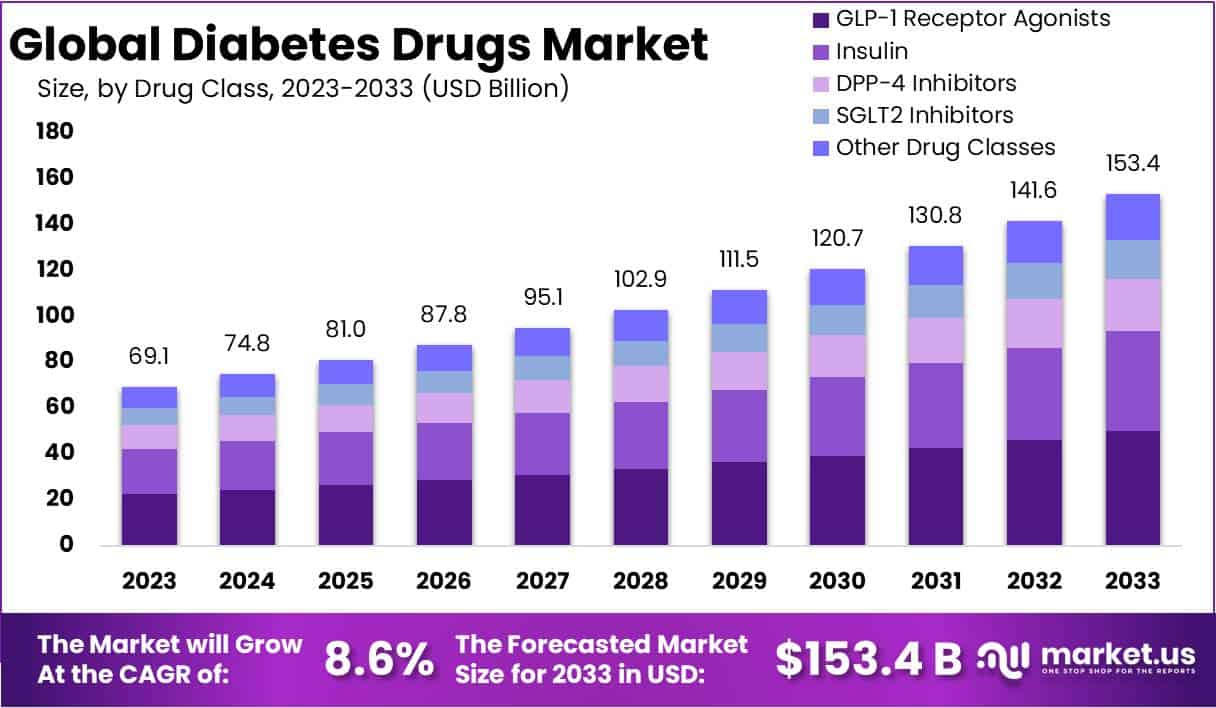

Global Diabetes Drugs Market size is expected to be worth around USD 153.4 Billion by 2033, from USD 69.1 Billion in 2023, growing at a CAGR of 8.6% during the forecast period from 2024 to 2033. In 2023, North America led the market, achieving over 51.3% share with a revenue of US$ 35.4 Million.

Several factors are driving the growth of the diabetes drug market. A key factor is the rising prevalence of diabetes globally, especially type 2 diabetes. Data from the International Diabetes Federation indicates that the number of adults with diabetes is expected to increase from 537 million in 2021 to 783 million by 2045. Furthermore, advancements in diabetes medications, such as the introduction of GLP-1 receptor agonists and SGLT-2 inhibitors, offer effective alternatives to traditional therapies, enhancing market expansion.

Recent developments in the sector include the introduction of new drugs and formulations. For example, Glenmark Pharmaceuticals launched Lirafit, a biosimilar of the popular anti-diabetic drug Liraglutide, in India in January 2024. Additionally, companies like Akums Drugs and Pharmaceuticals have been developing novel combination therapies aimed at improving treatment effectiveness and adherence among the elderly with type 2 diabetes.

Despite these advancements, the market faces challenges such as the high costs associated with diabetes drug therapies, which pose significant barriers, particularly in less developed regions. Nonetheless, the ongoing focus on diabetes care, coupled with increasing awareness and substantial research and development investments by leading companies, are anticipated to maintain the market’s growth trajectory. North America leads this market, propelled by high obesity rates and sedentary lifestyles, with the United States holding the largest share due to its significant demand for insulin and other diabetes medications.

Key Takeaways

- In 2023, the global diabetes drugs market generated USD 69.1 billion, forecasted to exceed USD 153.4 billion, growing at a CAGR of 8.3%.

- The GLP-1 receptor agonists segment led the market in 2023 with a 32.6% share.

- The type 2 diabetes segment held the largest market share in 2023 at 62.9%, due to higher global prevalence.

- Subcutaneous route of administration dominated the market in 2023 with a 45.8% share.

- Retail pharmacies secured the largest market share in 2023, accounting for 62.4% of sales due to competitive pricing.

- North America accounted for a significant 51.3% share of the diabetes drugs market in 2023.

Diabetes Drugs Statistics

- Prevalence and Cost

- The prevalence of Type 2 Diabetes in the US has nearly tripled from 1980 to 2011.

- Roughly one in three US adults are expected to develop diabetes in their lifetime.

- In 2012, the total cost of Type 2 Diabetes Mellitus was estimated at $245 billion, with direct medical expenses totaling $176 billion.

- Treatment Efficacy and Challenges

- Only 36% of patients achieve glycemic control with current diabetes therapies.

- An estimated 3.1 million US adults with Type 2 Diabetes were not on medication in 2011.

- The average cost for inpatient admission due to hypoglycemic events is $17,564, accumulating to $52,223,675 over a four-year study.

- Impact of Weight Management

- A 1% weight reduction over a year can decrease healthcare costs by approximately $213 per patient.

- Weight loss is linked to improved adherence to antidiabetic medications.

- Drug Classes and Innovations

- Currently, up to 14 drug classes are available for Type 2 Diabetes treatment.

- New therapies include SGLT-2 inhibitors (Canagliflozin, Dapagliflozin, Empagliflozin) and GLP-1 agents (Exenatide, Albiglutide, Dulaglutide).

- Technosphere insulin, marketed as Afrezza, represents a novel treatment option for Type 2 Diabetes.

- Recent Drug Approvals and Costs

- Canagliflozin, Dapagliflozin, and Empagliflozin were FDA approved between 2013 and 2014, with monthly costs ranging between $313.19 and $348.81.

- High-profile drugs like Ozempic, Jardiance, and Trulicity recorded sales exceeding $7 billion in 2022, highlighting significant market demand.

- Emerging Trends in Treatment

- The combination of GLP-1 medicines with FreeStyle Libre technology significantly improves HbA1c levels, showing a –2.4% reduction compared to –1.7% with GLP-1 alone.

- Real-world studies endorse the combined use of GLP-1 medicines and FreeStyle Libre technology for enhanced Type 2 Diabetes management.

Emerging Trends in Diabetes Treatment

- Popularity of SGLT2 Inhibitors and GLP-1 Receptor Agonists: SGLT2 inhibitors and GLP-1 receptor agonists are gaining traction in diabetes management due to their effectiveness in controlling blood sugar while offering additional benefits like weight loss and cardiovascular protection. Their ability to address multiple health issues makes them preferred choices among healthcare providers and patients alike. With a growing body of evidence supporting their efficacy, these drugs are becoming central to diabetes treatment strategies.

- Advancements in Biosimilar Insulin: The introduction of biosimilar insulin is set to transform diabetes care by reducing treatment costs and enhancing accessibility, especially in developing countries where insulin affordability is a significant barrier. Biosimilars provide the same therapeutic benefits as original insulin products but at a reduced cost, making treatment more accessible to a broader audience. This trend is expected to encourage widespread adoption and improve diabetes management globally.

- Technological Innovations in Drug Delivery: Technological advancements are reshaping diabetes management with developments in continuous glucose monitoring (CGM) systems and automated insulin delivery (AID) systems. These innovations offer real-time monitoring and precise insulin delivery, which greatly enhance glucose control and reduce diabetes management burdens. These systems are likely to become standard in diabetes care due to their ability to increase patient compliance and customize treatments.

- Increased R&D Investment: Pharmaceutical companies are ramping up investments in research and development to create new and more effective diabetes treatments. This includes exploring combination therapies and novel drug formulations that improve patient outcomes. Increased R&D funding is aimed at enhancing treatment efficacy, reducing side effects, and improving patients’ quality of life, demonstrating a commitment to advancing diabetes care.

- Expansion of Oral Diabetes Medications: There is an increased focus on developing oral diabetes medications to minimize reliance on injections, which many patients find burdensome. New oral formulations of drugs like GLP-1 receptor agonists and SGLT2 inhibitors have been developed and approved, offering a more convenient and less invasive treatment option. These medications are likely to play a crucial role in the future of diabetes therapy by enhancing patient adherence and improving quality of life.

Use Cases in Diabetes Management

- Type 2 Diabetes Management: Type 2 diabetes management often involves drugs like metformin and SGLT2 inhibitors, which enhance insulin sensitivity and promote glucose excretion. In India, approximately 77 million adults suffer from type 2 diabetes, underscoring the vast demand for effective management solutions.

- Type 1 Diabetes Treatment: Insulin therapy is essential for managing type 1 diabetes, requiring lifelong insulin administration. Long-acting and rapid-acting insulins are crucial for maintaining stable blood glucose levels, providing better control and mimicking natural insulin release.

- Geriatric Diabetes Care: Older adults with diabetes often benefit from fixed-dose combination therapies, which simplify treatment regimens and improve medication adherence by addressing multiple conditions simultaneously. These comprehensive treatment strategies are vital for minimizing complications and enhancing life quality for elderly patients.

- Pediatric Diabetes Management: Recent approvals of oral diabetes medications for children, such as Synjardy, improve treatment adherence and outcomes in pediatric type 2 diabetes patients. These developments are vital for consistent medication usage, controlling the condition effectively, and reducing long-term health risks.

- Hospital and Clinical Settings: Diabetes drugs are crucial in hospital settings for managing acute and chronic diabetes cases. Tailored treatment plans in these controlled environments ensure comprehensive care and better management of diabetes complications.

- Ambulatory Clinics: Ambulatory clinics play an increasing role in diabetes management by providing accessible, continuous care. These clinics are essential for regular health monitoring and personalized care, significantly contributing to improved long-term health outcomes for diabetes patients.

Conclusion

The diabetes drugs market is poised for substantial growth, driven by the increasing global prevalence of diabetes, particularly type 2, and significant advancements in therapeutic options. Innovations such as GLP-1 receptor agonists and SGLT-2 inhibitors are enhancing treatment efficacy and patient adherence, further supported by the development of biosimilars and novel drug delivery systems.

Despite challenges such as high treatment costs, continuous investment in research and development, coupled with technological advances in drug delivery and monitoring, are expected to sustain market expansion and improve diabetes management across diverse populations globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)