Table of Contents

Overview

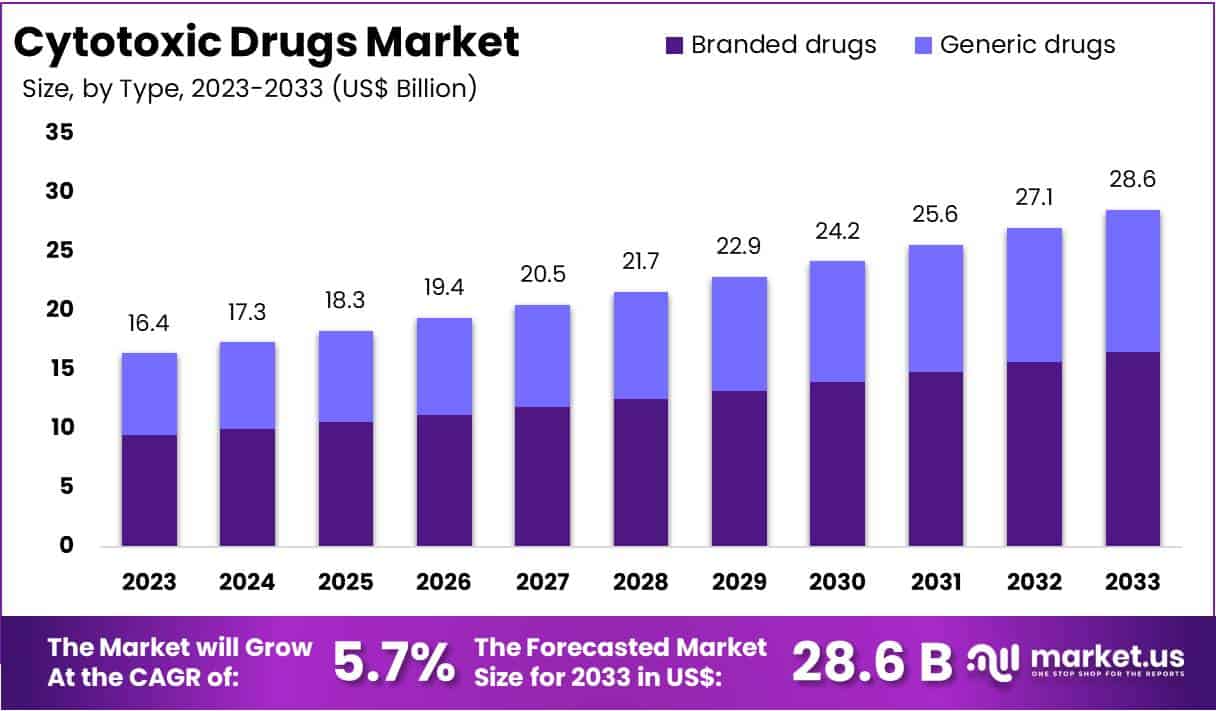

New York, NY – July 25, 2025 – The Global Cytotoxic Drugs Market Size is expected to be worth around US$ 28.6 Billion by 2033, from US$ 16.4 Billion in 2023, growing at a CAGR of 5.7% during the forecast period from 2024 to 2033. North America emerged as the leading region in the Cytotoxic Drugs Market, accounting for 38.6% of the market share, with a valuation of US$ 6.3 billion.

Cytotoxic drugs, also known as chemotherapy agents, are a cornerstone in the treatment of various cancers. These powerful drugs are designed to target and kill rapidly dividing cells, a hallmark of cancerous growth. By interfering with cellular functions such as DNA replication and cell division, cytotoxic drugs inhibit tumor growth and spread, providing a critical therapeutic tool in oncology.

Cytotoxic agents are classified into several categories, including alkylating agents, antimetabolites, and mitotic inhibitors. Each class functions in unique ways to disrupt cancer cell replication. For instance, alkylating agents attach to the DNA, preventing its normal function, while mitotic inhibitors block the division of cells by disrupting the mitotic spindle.

Despite their efficacy, the use of cytotoxic drugs comes with side effects due to their impact on healthy cells. Common side effects include nausea, fatigue, and hair loss, as these drugs also affect non-cancerous fast-growing cells such as those in the gastrointestinal tract and hair follicles. However, continued advancements in chemotherapy regimens and the development of targeted therapies aim to minimize these adverse effects while enhancing treatment outcomes.

Cytotoxic drugs remain a primary treatment option for many cancers and continue to play an integral role in improving patient survival rates. Ongoing research and innovation in drug formulations are expected to further enhance their effectiveness and safety.

Key Takeaways

- In 2023, branded drugs led the Cytotoxic Drugs Market, commanding a substantial 57.8% of the market share due to their widespread use and strong demand.

- The antimetabolites drug class emerged as the dominant segment in the Cytotoxic Drugs Market, capturing 26.2% of the market share in 2023.

- Oral administration was the preferred route for Cytotoxic Drugs, with the oral segment holding a commanding 68.9% share in 2023.

- Hospital pharmacies were the primary distribution channel for Cytotoxic Drugs, securing the largest share of 40.7% in 2023.

- North America remained the leading region in the Cytotoxic Drugs Market, accounting for 38.6% of the market share and a market value of US$ 6.3 billion in 2023.

Segmentation Analysis

- Type Analysis: In 2023, the Branded drugs segment dominated the Cytotoxic Drugs Market, capturing 57.8% of the market share, benefiting from strong brand loyalty and proven efficacy. These drugs are often preferred due to their established reliability and the trust healthcare professionals place in their clinical benefits. Conversely, the Generic drugs segment offers affordable alternatives, expanding as patents for key cytotoxic drugs expire. This shift is enhancing competition and making treatments more accessible, especially in regions with limited healthcare budgets.

- Drug Class Analysis: The Antimetabolites drug class led the Cytotoxic Drugs Market in 2023, holding a 26.2% market share. These drugs, vital in treating cancers like leukemia and ovarian cancer, disrupt DNA/RNA replication, halting cancer cell growth. Antitumor antibiotics, which block DNA replication, also play a significant role in cancer therapies. Plant Alkaloids and Alkylating agents target cancer cell division and DNA replication, respectively, while ‘Other Drug Classes’ address specific mutations, expanding treatment options and supporting market growth.

- Route of Administration Analysis: In 2023, the Oral segment dominated the Cytotoxic Drugs Market with a 68.9% share due to its ease of administration and high patient compliance. Oral medications, commonly used at home, reduce hospital stays and healthcare costs. The Parenteral route, though less convenient, is crucial for drugs that require immediate action or cannot be absorbed effectively through the digestive system. Both routes play critical roles in delivering effective cancer treatments, with oral drugs driving market growth due to their convenience.

- Application Analysis: Oncology remains the primary application for cytotoxic drugs, driven by the growing global prevalence of cancer and ongoing advancements in drug formulations. Cytotoxic drugs also play a key role in treating severe rheumatoid arthritis, multiple sclerosis, and autoimmune diseases like psoriasis and lupus. Their expanding use in managing kidney diseases highlights their broad therapeutic potential. Ongoing research is uncovering new applications for cytotoxic drugs, suggesting a future where they address a wider range of conditions previously resistant to traditional treatments.

- Distribution Channel Analysis: In 2023, Hospital pharmacies led the Cytotoxic Drugs Market, capturing 40.7% of the market share. These pharmacies are integral to chemotherapy administration and the precise handling of cytotoxic drugs. Retail pharmacies also play an essential role by providing access to medications for outpatient treatments. Online pharmacies are gaining popularity due to their convenience and competitive pricing, allowing patients to receive medications discreetly at home. These distribution channels collectively ensure broad access to cytotoxic drugs, meeting diverse patient needs and treatment protocols.

Market Segments

By Type

- Branded drugs

- Generic drugs

By Drug Class

- Antimetabolites

- Antitumor antibiotics

- Plant alkaloids

- Alkylating agents

- Other drug classes

By Route of Administration

- Oral

- Parenteral

By Application

- Oncology

- Rheumatoid arthritis

- Multiple sclerosis

- Other applications

By Distribution Channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

Regional Analysis

In 2023, North America dominated the Cytotoxic Drugs Market, accounting for over 38.6% of the market share, valued at US$ 6.3 billion. This dominant position is driven by the region’s advanced healthcare infrastructure and substantial investment in oncology research. North America’s focus on accelerating the approval of innovative cytotoxic therapies has solidified its market leadership. High per capita healthcare spending, along with strategic partnerships between biotechnology firms and research institutions, further supports sustained market growth.

The presence of major pharmaceutical companies in North America, particularly in the U.S., significantly contributes to the market’s success. These companies lead the development of advanced cytotoxic drugs, essential for treating a range of cancers. Their continuous research and development efforts, supported by both public and private funding, strengthen the drug development pipeline. Additionally, the region’s strong regulatory framework ensures the efficient approval and distribution of new therapies, maintaining market momentum.

Looking ahead, the North American cytotoxic drugs market is expected to experience continued growth. The increasing prevalence of cancer and the rising demand for effective treatment options are key drivers. Moreover, the growing emphasis on personalized medicine, which relies heavily on cytotoxic drugs for targeted cancer therapy, will further propel market demand. Technological advancements in drug delivery systems are anticipated to improve treatment efficacy and minimize side effects, reinforcing North America’s market dominance.

Emerging Trends

- Adaptive Dose Reduction: Research is increasingly focused on whether standard cytotoxic regimens can be given at lower doses without losing effectiveness. Studies have shown that lower doses of certain chemotherapies can reduce side effects such as nausea and fatiguewhile maintaining tumor killing activity, improving patient quality of life during treatment.

- Targeted Delivery via Antibody–Drug Conjugates (ADCs): A growing number of cytotoxic agents are being linked to antibodies that recognize cancer specific markers. These ADCs deliver the toxic payload directly into tumor cells, sparing healthy tissue and reducing systemic toxicity. In April 2024, the FDA approved an ADC for platinum resistant ovarian cancer, illustrating how this approach is expanding clinical options.

- Genomic Driven Personalization: Advances in genomic profiling are enabling oncologists to tailor cytotoxic regimens to the molecular features of each patient’s tumor. Personalized dosing and drug selection are being guided by genetic signatures and drug response assays, which are contributing to more precise and effective treatments.

- Rising Global Demand: The World Health Organization projects that the number of cancer cases worldwide will nearly double over the next twenty years. Consequently, the consumption of cytotoxic drugs is expected to rise substantially, placing increased emphasis on supply chain resilience and equitable access to essential medicines.

Use Cases

- Pediatric Acute Lymphoblastic Leukemia (ALL):

- Incidence: Approximately 4.8 new cases of childhood leukemia per 100,000 children each year in the U.S..

- Outcomes: With modern multi agent cytotoxic regimens, the 5 year relative survival for lymphoid leukemias (mostly ALL) has reached 96% in children aged 1–4, 94% in those aged 5–9, and 86% in ages 10–14.

- Childhood Acute Myeloid Leukemia (AML):

- Treatment Response: Contemporary induction protocols achieve remission in 85%–90% of pediatric AML patients.

- Survival Rates: Five year overall survival now ranges from 55% to 70% across biological subtypes, marking significant improvement over past decades.

- Adjuvant Chemotherapy in Early Breast Cancer:

- Subtype Prevalence: Hormone receptor–positive/HER2 negative (HR+/HER2–) tumors account for about 70% of breast cancer cases, with an age adjusted incidence of 91.3 new cases per 100,000 women.

- Survival Benefit: Cytotoxic agents used after surgery contribute to a 5 year relative survival of 95.6% in this subtype, underscoring the critical role of adjuvant chemotherapy in reducing recurrence risk

Conclusion

Cytotoxic drugs remain essential in cancer treatment, offering significant therapeutic benefits despite associated side effects. In 2023, branded drugs and antimetabolites dominated the market, with North America leading in market share. Emerging trends, such as adaptive dose reduction, targeted delivery via antibody-drug conjugates, and genomic-driven personalization, are enhancing treatment precision and minimizing side effects.

The rising global cancer burden further drives demand for cytotoxic therapies. Ongoing advancements in drug formulations and delivery systems promise to improve patient outcomes, solidifying the role of cytotoxic drugs in oncology and potentially expanding their use in other medical applications.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)