Introduction

According to Critical Illness Insurance Statistics, Critical illness insurance is a form of coverage that provides a one-time pay-out when the policyholder is diagnosed with specific severe medical conditions like cancer, heart attack, or stroke.

Unlike regular health insurance which covers medical expenses, critical illness insurance offers financial support for non-medical costs related to the illness, such as lost income or additional expenses not covered by standard insurance.

The lump-sum payment is given upon the diagnosis of a covered critical illness, offering flexibility in how the funds are used.

This type of insurance aims to ease financial burdens during a challenging period, allowing individuals to focus on recovery without the added stress of economic consequences.

It’s essential to carefully review policy details, as coverage can vary in terms of conditions covered, exclusions, and other specifics.

Editor’s Choice

- The global Critical Illness Insurance market was valued at USD 192.3 billion in 2022.

- The cancer segment contributed to 34% of the total revenue share in 2022.

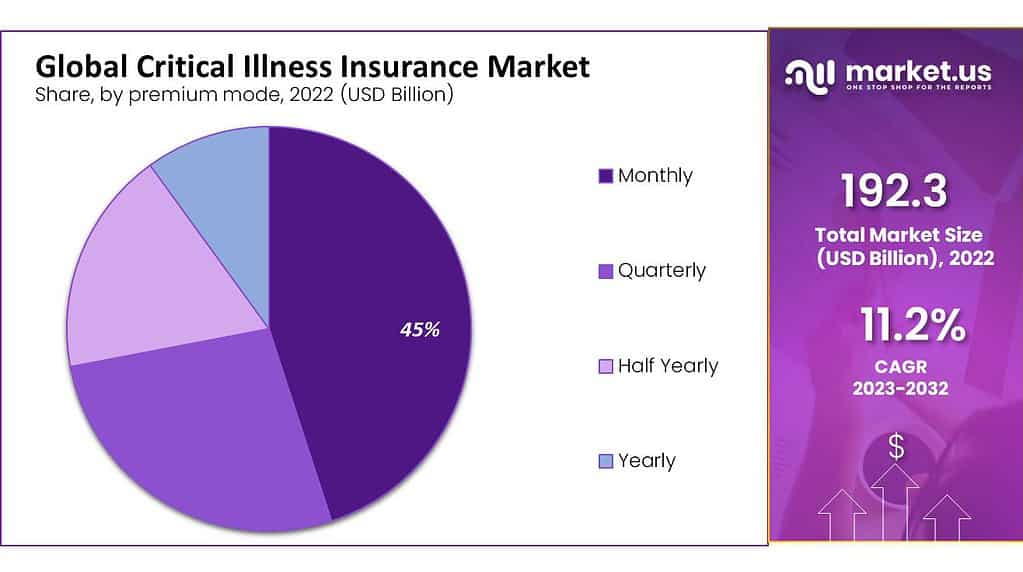

- The premium mode of payment is the most preferred type of payment with 45% of the market share.

- North America is the largest market for critical illness insurance with a 40% market share.

- The U.S. market value was at $76.9 billion in 2022.

- 92.1% of Americans were insurance holders in 2022.

- Female Breast Cancer was the top cancer type in the U.S. in 2020 with around 239,612 cases.

Global Critical Illness Insurance Market Overview

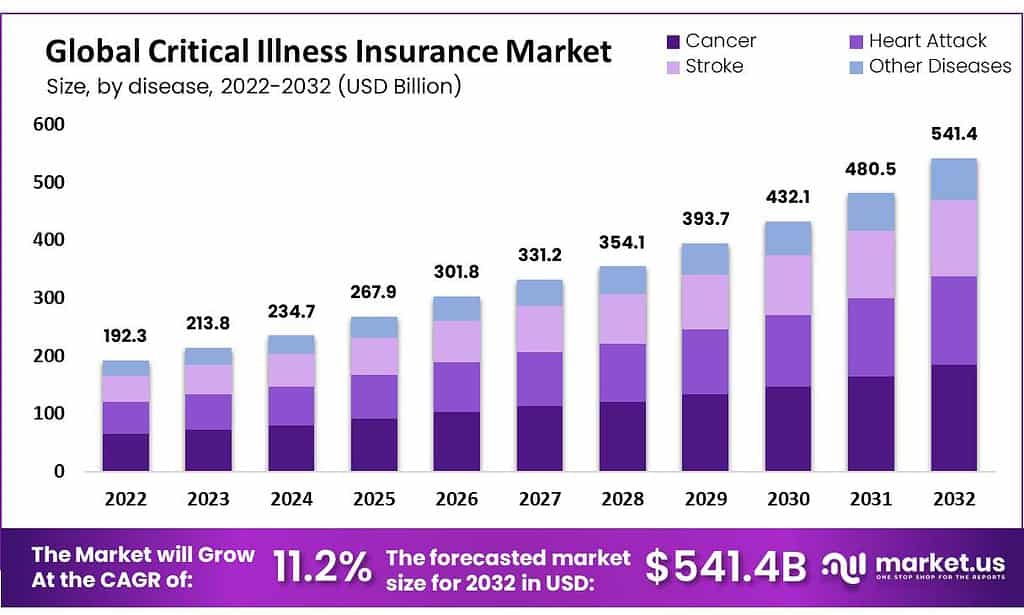

- As of 2022, the global critical illness insurance market reached a value of USD 192.3 billion, with an expected growth of USD 541.4 billion by 2032. Over the period from 2023 to 2032, this market is predicted to experience a Compound Annual Growth Rate (CAGR) of 11.2%.

- The global critical illness insurance market was valued at 192.3 billion USD in 2022. In 2023, the market saw an increase to 213.8 billion USD.

- The trend continued with values of 234.7 billion USD in 2024, 267.9 billion USD in 2025, and 301.8 billion USD in 2026.

- Subsequent years showed a progressive rise, reaching 331.2 billion USD in 2027 and 354.1 billion USD in 2028.

- The values continued to climb, reaching 393.7 billion USD in 2029 and 432.1 billion USD in 2030.

- The positive trajectory persisted with values of 480.5 billion USD in 2031, and it peaked at 541.4 billion USD in 2032.

Modes of Payment for Critical Illness Insurance

- In the global critical illness insurance market, premium modes are divided into monthly, quarterly, half-yearly, and yearly payment options.

- Among these, the monthly premium mode is forecasted to be the most lucrative segment in 2022, accounting for a substantial 45% market share and demonstrating a projected Compound Annual Growth Rate (CAGR) of 14.4%.

- Premium mode, in this context, refers to how often policyholders make their premium payments, and insurers typically offer a range of choices to cater to diverse policyholder preferences.

- The monthly premium mode entails policyholders making monthly payments towards their premiums.

Diseases covered Under Critical Illness Insurance

- The critical illness insurance market is categorized by the specific diseases it covers, such as cancer, heart attacks, strokes, and others.

- Among these, the cancer segment is projected to be the most profitable, with an expected annual growth rate of 11.4%.

- In 2022, the cancer segment holds a substantial 34% share of the total revenue.

- Insurance policies in this category may provide coverage for conditions like heart attacks or strokes and may include benefits such as bypass surgery, stenting, and angioplasty.

Universal Health Coverage

- Slow Progress Toward Universal Health Coverage (UHC): Achieving UHC, a goal set by the Sustainable Development Goals (SDGs) for 2030, is facing obstacles. Improvements in health service coverage have come to a halt since 2015.

- Increasing Catastrophic Out-of-Pocket Spending: The number of people experiencing catastrophic out-of-pocket health spending has been consistently growing since 2000, indicating a global trend seen across regions and countries.

- Limited Growth in UHC Service Coverage Index: Although the UHC service coverage index went up from 45 to 68 between 2000 and 2021, recent progress has significantly slowed. Between 2015 and 2021, the index only increased by 3 points and has remained unchanged since 2019.

- Substantial Population Lacks Essential Health Services: While there was a 15% reduction in the population without essential health services from 2000 to 2021, progress has been minimal since 2015, leaving around 4.5 billion people without full coverage in 2021.

- Financial Hardship for Billions: About 2 billion people are facing financial difficulties due to health costs. This includes 1 billion dealing with catastrophic out-of-pocket health spending, leading to 344 million people falling further into extreme poverty.

- Impact of COVID-19 Disruptions: The COVID-19 pandemic disrupted essential health services in 92% of countries in 2021, and as of 2022, 84% of countries still report ongoing disruptions.

Regional Analysis of Critical Illness Insurance

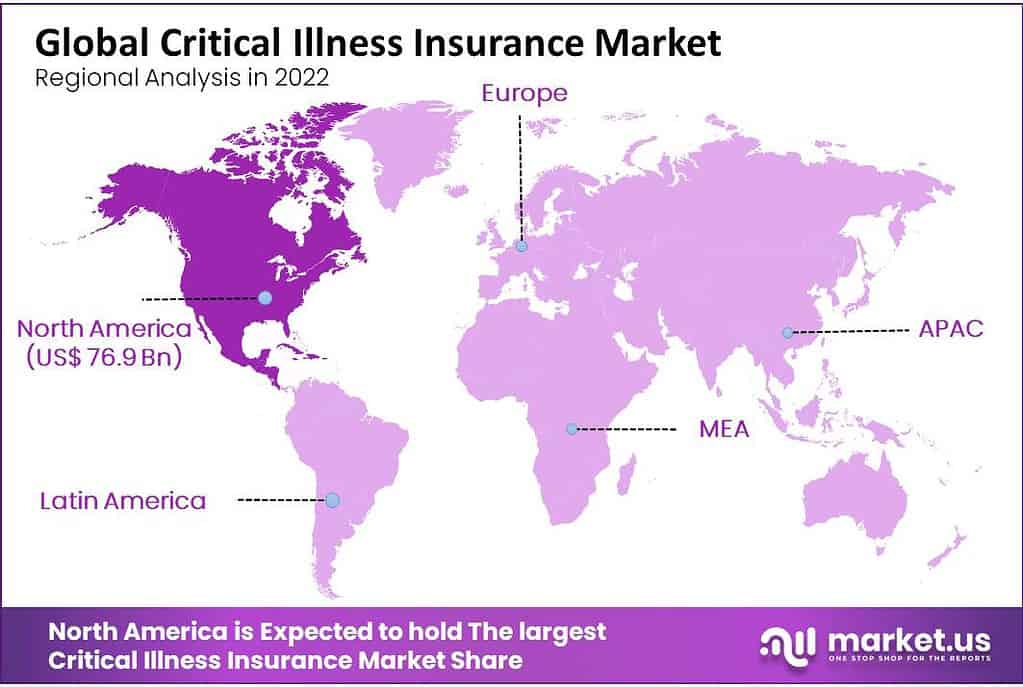

- North America is the leader in the global critical illness insurance market, accounting for the largest share of 40%. During the forecast period, it is projected to experience a steady growth rate of 14.6%.

- The United States, in particular, plays a pivotal role in driving this growth within North America with a $76.9 billion market value.

- In Europe, the critical illness insurance market also holds substantial importance, ranking as the second-largest globally. Countries like the United Kingdom, Germany, and France are the primary drivers of this market within the European region.

The United States of America

- In 2022, the majority of Americans had health insurance, with a slightly higher percentage (92.1%) compared to the previous year (91.7%), as reported by the U.S. Census Bureau.

- Approximately 8.4% or 27.6 million American adults faced periods without healthcare coverage during the year.

- This disparity in coverage affected Hispanic and Black working-age adults more significantly than White/Non-Hispanic or Asian adults.

- Nearly 25% of adults revealed that they either skipped taking medicine, cut pills in half, or didn’t fill a prescription in the past year due to financial constraints.

- Moreover, about four in 10 adults (41%) reported having outstanding medical or dental bills, contributing to the issue of medical debt.

- When it came to managing expenses, dental services were the most frequently postponed type of healthcare (35%), followed by vision services (25%) and doctor’s visits (24%).

United Kingdom

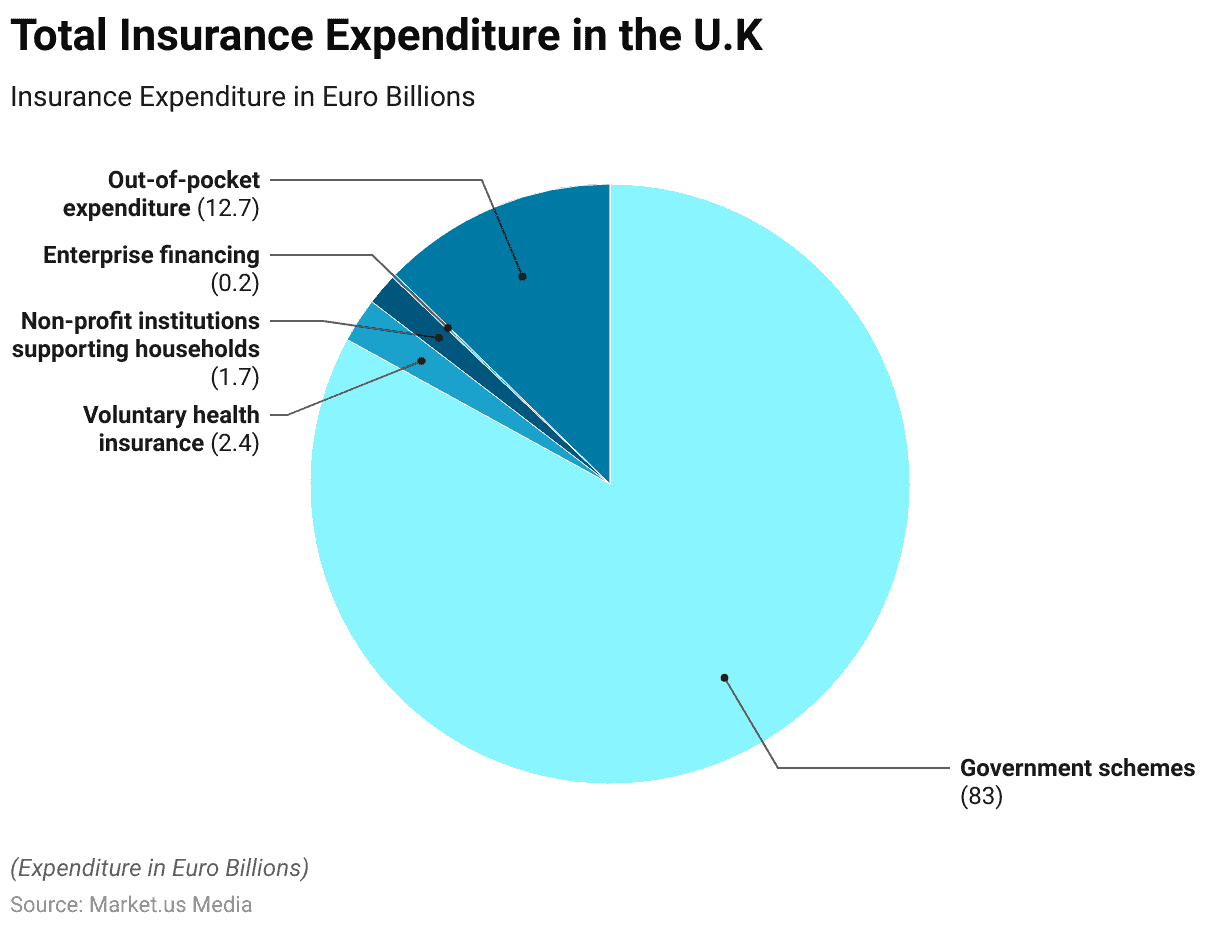

- In 2021, the UK’s overall spending on healthcare reached $352.62 billion, which translates to an average of $5261 per person.

- In 2021, Government schemes accounted for 83% of total expenditure, totaling $202.82 billion.

- Voluntary health insurance contributed 2.4% or $8.67 billion to the overall expenditure.

- Non-profit institutions supporting households made up 1.7% of the total, amounting to $6.03 billion.

- Enterprise financing represented 0.2% or $0.75 billion of the total healthcare expenditure.

- Out-of-pocket expenditure comprised 12.7% of the total healthcare spending, which equals $44.72 billion.

India

- As per the Insurance Regulatory and Development Authority of India (IRDAI), India is anticipated to achieve the status of the sixth-largest insurance industry within the next ten years.

- In FY23, the Indian government allocated approximately 2.1% of the GDP for healthcare spending, which slightly decreased from FY22 (2.2%) but is a significant increase from FY21 (1.6%).

- This reflects the government’s recognition of the importance of a strong healthcare system.

- The share of the budget dedicated to healthcare services has risen from 21% in FY19 to 26% in FY23.

- In 2021, health insurance plans in India covered about 514 million people, which represents only 37% of the total population in the country.

- Approximately 41% of households in India have at least one member covered by health insurance, leaving a significant portion of the population without adequate coverage.

- Only 30% of women aged 15-49 and 33% of men in the same age group have health insurance between 2019-2021.

- State health insurance schemes cover 46% of those with insurance, while 16% are covered by the Rashtriya Swasthya Bima Yojana (RSBY).

- A smaller percentage of women (3-6%) and men (4-7%) are covered by the Employee State Insurance Scheme (ESIS) or the Central Government Health Scheme (CGHS).

- Rajasthan (88%) and Andhra Pradesh (80%) have the highest proportions of households with health insurance coverage.

Brazil

- The SUS (Sistema Único de Saúde), Brazil’s healthcare system, had its beginnings in the 1980s as part of the movement for the country’s re-democratization. It was officially established in 1988 through the adoption of the new Brazilian constitution.

- In 2015, Brazil allocated 9.1% of its Gross Domestic Product (GDP) towards healthcare, with public spending contributing 42.8% of this total.

- Notably, the SUS (Sistema Único de Saúde) offers healthcare coverage to all residents and even visitors, including undocumented individuals, encompassing a wide range of healthcare services.

- Around 27% of total healthcare expenses come from out-of-pocket payments, which can pose a significant financial burden, especially for lower-income households.

- In 2014, about 5.3% of households had to prioritize healthcare expenses over non-health-related spending due to high costs, with medication expenses being a major factor.

- This is because only specific drugs are available for free under the Unified Health System.

- The percentage of private health plans requiring copayments has risen from 22% to 52% over the past decade.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)