Table of Contents

Overview

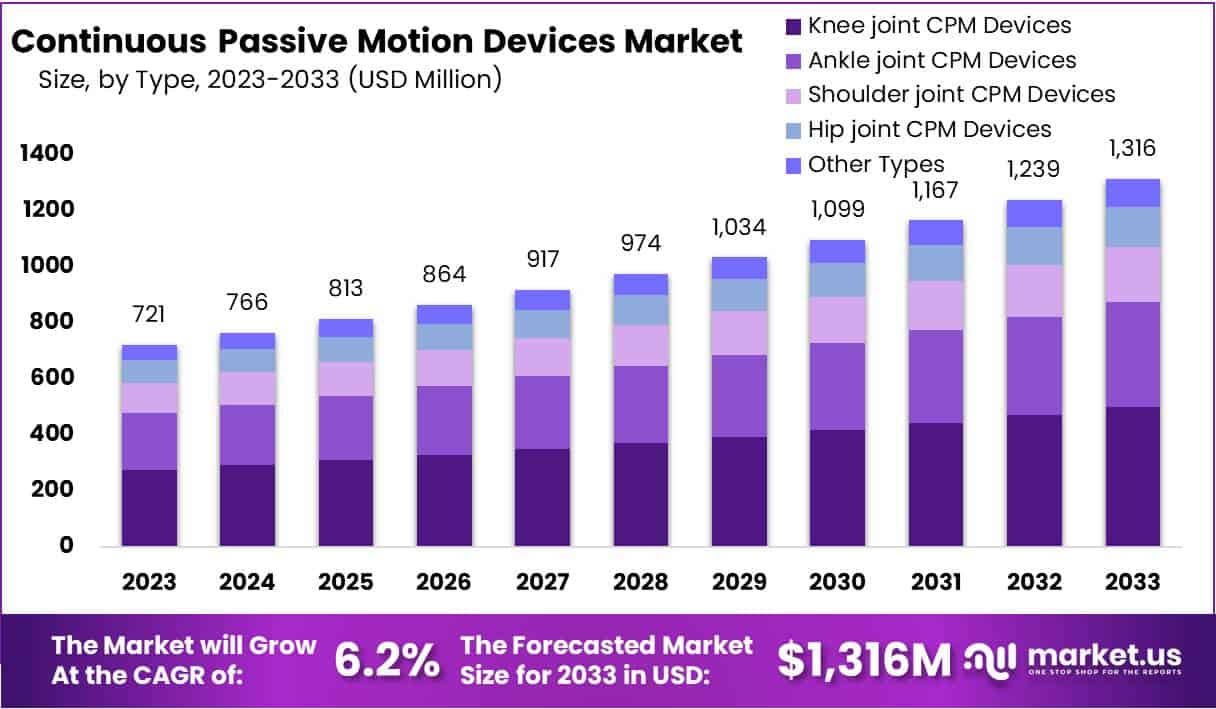

The Global Continuous Passive Motion (CPM) Devices Market is projected to reach USD 1,316 million by 2033, growing from USD 721 million in 2023 at a CAGR of 6.2% from 2024 to 2033. The growth is driven by rising orthopedic cases, increasing rehabilitation awareness, and technological advancements. These devices play a key role in post-surgical recovery by improving joint mobility, reducing stiffness, and enhancing tissue healing, particularly after orthopedic and musculoskeletal procedures.

The rising prevalence of joint injuries, degenerative bone disorders, and arthritis has increased the demand for CPM devices. These devices are vital in post-operative care, as they assist in continuous motion therapy without patient effort. The growing aging population, prone to mobility challenges and joint deterioration, further fuels demand. Older adults increasingly rely on these devices for recovery and pain reduction following surgeries like knee and hip replacements.

Technological advancements have significantly shaped the market landscape. Innovations such as compact, portable, and digitally integrated CPM systems have improved patient comfort and clinical effectiveness. These developments allow broader adoption in home-care and outpatient settings. Smart monitoring features also enable physicians to track patient progress remotely, making CPM devices more efficient and user-friendly.

The expansion of rehabilitation services and healthcare infrastructure supports market growth, especially in developing regions. The trend toward home-based rehabilitation aligns with the demand for convenient, cost-effective recovery solutions. Patients increasingly prefer at-home therapy due to its flexibility, lower costs, and faster recovery benefits. This shift has expanded the market reach of portable CPM devices across various demographics.

Moreover, the applications of CPM devices have extended beyond knee therapy to multiple joints, including the shoulder, ankle, hip, and elbow. The inclusion of CPM therapy in clinical guidelines has reinforced its medical importance. Healthcare professionals recognize its role in preventing joint stiffness and improving mobility outcomes. With supportive medical training and rising patient awareness, the CPM devices market is poised for sustained growth during the forecast period.

Key Takeaways

- The market is projected to reach USD 1,316 million by 2033, expanding at a CAGR of 6.2% between 2024 and 2033.

- The devices play a vital role in postoperative rehabilitation, especially following knee surgeries, facilitating effective joint mobility recovery and faster healing.

- Regulatory compliance with FDA and EMA standards is crucial to maintain product credibility, ensure patient safety, and strengthen market trust.

- Private sector investments have increased by 30%, significantly accelerating innovation and technological development within the continuous passive motion device industry.

- The knee joint CPM device segment dominates the market, accounting for 38% share, driven by the high incidence of knee replacement surgeries globally.

- Portable device designs hold a leading 57% market share, reflecting growing demand for convenience, mobility, and home-based rehabilitation solutions.

- Hospitals represent the largest end-user segment, capturing 44.2% of the market, due to higher adoption of advanced rehabilitation technologies and skilled medical supervision.

- The market growth is primarily driven by the increasing prevalence of musculoskeletal disorders and the rising number of joint surgeries worldwide.

- The high cost of devices and limited reimbursement policies remain key challenges, restricting accessibility and broader market expansion.

- Technological advancements and product innovations present significant opportunities to improve adoption rates and strengthen competitive positioning in the global market.

Regional Analysis

In 2023, North America held a leading position in the Continuous Passive Motion (CPM) Devices Market, accounting for over 34.4% of the total share with a market value of USD 249.4 million. This dominance can be linked to strong healthcare infrastructure and the early adoption of advanced medical technologies. The rising incidence of orthopedic disorders such as osteoarthritis and an increasing number of joint replacement surgeries further supported regional growth, creating a strong demand for CPM devices in rehabilitation and recovery applications.

The United States significantly contributed to this dominance due to its high healthcare spending and favorable reimbursement policies for medical devices. A large aging population, coupled with a growing preference for non-invasive rehabilitation methods, further increased CPM device usage. Continuous technological innovations by U.S.-based manufacturers have also enhanced device performance, usability, and patient outcomes. These advancements have made CPM devices more accessible and efficient, strengthening their adoption across hospitals, clinics, and home care settings.

Strategic initiatives by key players, including mergers, acquisitions, and new product launches, have further boosted North America’s market presence. Such initiatives aim to expand product portfolios and meet the evolving needs of healthcare providers. Supportive regulations from authorities like the U.S. Food and Drug Administration (FDA) have ensured product safety and quality. These policies have built trust among medical professionals and patients, promoting wider adoption of CPM devices for post-operative rehabilitation and pain management throughout the region.

Segmentation Analysis

In 2023, the Knee Joint Continuous Passive Motion (CPM) Devices segment held the dominant share of over 38% in the market. This leadership was due to the devices’ key role in post-surgical rehabilitation, especially after knee surgeries. These devices help reduce stiffness, restore joint mobility, and speed up recovery. Growing cases of knee disorders, sports injuries, and osteoarthritis among older adults have fueled demand. Endorsement from healthcare professionals for early postoperative mobilization further strengthens this segment’s market position.

Technological advancements have significantly influenced the growth of Knee Joint CPM devices. Modern designs now feature customizable motion ranges, programmable settings, and smart interfaces. These features improve user comfort, enhance therapy effectiveness, and ensure better patient adherence. Smart technology integration also allows remote monitoring and data tracking, promoting personalized treatment. As technology continues to evolve, these innovations are expected to improve therapy outcomes and patient satisfaction, further cementing the segment’s growth potential in rehabilitation settings.

The Portable Devices segment dominated the Design category in 2023, capturing more than 57% of the market share. The rising preference for portable CPM devices is linked to their user-friendly and convenient design, which enables home-based rehabilitation. These devices help reduce hospital stays and healthcare costs while ensuring continuous therapy. Their compact design, ergonomic features, and efficient battery life appeal to both patients and medical professionals. Increased incidences of bone and joint disorders, coupled with a growing elderly population, have strengthened their market adoption worldwide.

In 2023, hospitals led the End-User segment with over 44.2% of the market share. Their dominance was supported by the growing integration of CPM devices in orthopedic and neurological rehabilitation. Hospitals invest heavily in advanced technologies and employ trained staff to enhance patient outcomes. The consistent rise in post-surgical rehabilitation cases has maintained strong device demand. With improved healthcare infrastructure in developing regions and a focus on recovery efficiency, hospital adoption of CPM devices is projected to continue growing steadily in the coming years.

Key Players Analysis

The Continuous Passive Motion (CPM) Devices Market is led by several key players including Surgi-Care Inc., Furniss Corporation, Bio-Med Inc., BTL Corporate, and Chattanooga. These companies play a vital role in advancing rehabilitation technologies. Surgi-Care Inc. is known for its innovative CPM solutions that enhance post-surgery recovery. The company focuses on designing user-friendly and efficient devices that improve patient outcomes. Its products are widely adopted across hospitals and rehabilitation centers, reflecting its strong market presence and commitment to patient care and technological advancement.

Furniss Corporation emphasizes patient comfort and compliance through ergonomic CPM devices. Its designs are preferred by healthcare professionals for promoting smooth rehabilitation processes. The company’s focus on ease of use and long-term reliability strengthens its competitive edge in the market. Bio-Med Inc. stands out with its continuous investment in research and development. The company integrates cutting-edge technologies to improve therapy effectiveness. Its innovation-driven strategy ensures a steady introduction of advanced rehabilitation solutions tailored to clinical needs.

BTL Corporate provides durable and reliable CPM devices primarily suited for clinical and hospital environments. The company is recognized for its robust engineering standards and quality control. BTL’s devices are valued for their efficiency in supporting patient recovery and long-term mobility. Chattanooga, on the other hand, offers an extensive portfolio of CPM devices supported by clinical validation. The company’s evidence-based approach and broad product range strengthen its reputation as a trusted brand in physical rehabilitation technologies worldwide.

Other significant players include OPED, Chinesport Rehabilitation, Medival, and Rimec. These companies specialize in developing CPM devices catering to specific rehabilitation needs. Their products are often customized to address diverse orthopedic and neurological conditions. The presence of multiple manufacturers increases market competition, driving product innovation and affordability. Collectively, these companies contribute to the expanding demand for non-invasive rehabilitation solutions. Their focus on patient safety, advanced design, and clinical efficacy continues to shape the global CPM devices market landscape positively.

Conclusion

The global continuous passive motion devices market is expected to grow steadily in the coming years. The rise in orthopedic surgeries, aging populations, and increasing demand for home-based rehabilitation are key factors driving growth. Technological improvements have made these devices more comfortable, portable, and efficient, supporting better patient recovery. Expanding healthcare infrastructure and awareness about post-surgical rehabilitation also strengthen market prospects. Leading manufacturers are focusing on innovation, quality, and user-friendly designs to enhance treatment outcomes. Overall, continuous passive motion devices are becoming an essential part of modern rehabilitation, helping patients recover faster and improving joint mobility across various medical settings.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)