Table of Contents

- Introduction

- Editor’s Choice

- Global Assistive Technology Market Size Statistics

- Medical Assistive Technology Market Statistics

- Mobility Devices Market Overview

- Demographic Insights of Mobility Aid Users

- E-learning Market Overview

- Hearing Aids Market Overview

- Hearing Aids Sales Statistics

- Hearing Aid Import Statistics

- Hearing Aid Export Statistics

- Demographic Insights of Hearing Aid Users

- Automated Transcription Usage Worldwide

- Usage of Assistive Technology Statistics

- Challenges Faced by Users

- Key Spending and Investments

- Innovations and Developments in Assistive Technology Statistics

- Regulations for Assistive Technology

- Recent Developments

- Conclusion

- FAQs

Introduction

Assistive Technology Statistics: Assistive Technology (AT) encompasses a wide range of devices and tools designed to support individuals with disabilities. Enabling them to perform tasks that might otherwise be difficult.

These technologies include mobility aids (like wheelchairs and prosthetics), communication tools (such as speech-generating devices and hearing aids), vision aids (like screen readers and Braille devices), and cognitive support tools (such as memory aids and text-to-speech software).

AT enhances independence, participation, and productivity by allowing individuals to engage more fully in daily activities, education, and work.

With the growing global demand driven by aging populations and increased accessibility awareness. The market for assistive technologies is expanding, fostering innovation and improving lives worldwide.

Editor’s Choice

- The WHO and UNICEF report that while over 2.5 billion people globally require AT. Nearly one billion are denied access, with availability in some countries as low as 3%.

- The global assistive technology market size is projected to reach USD 36.6 billion in 2033.

- In 2016, the United States emerged as the largest market for medical assistive technologies. With a market size of USD 4,439.7 million. Reflecting its advanced healthcare infrastructure and high adoption rates.

- In 2019, 19.2% of the population in India was using assistive technology (AT) products. Highlighting significant gaps in adoption and demand.

- In 2019, 39% of individuals with severe disabilities in India used assistive technology. Indicating greater reliance on these tools for functional support.

- In 2019, 23% of individuals with severe disabilities in India faced difficulties using assistive technology, the highest among all groups.

- In 2019, individuals with severe disabilities in India faced challenges using assistive products. With key issues including discomfort (21 respondents), complexity (17), and lack of product knowledge (16).

- In the United States, legislation like the Americans with Disabilities Act and the Individuals with Disabilities Education Act specifically includes provisions for assistive technology to support educational and public access needs.

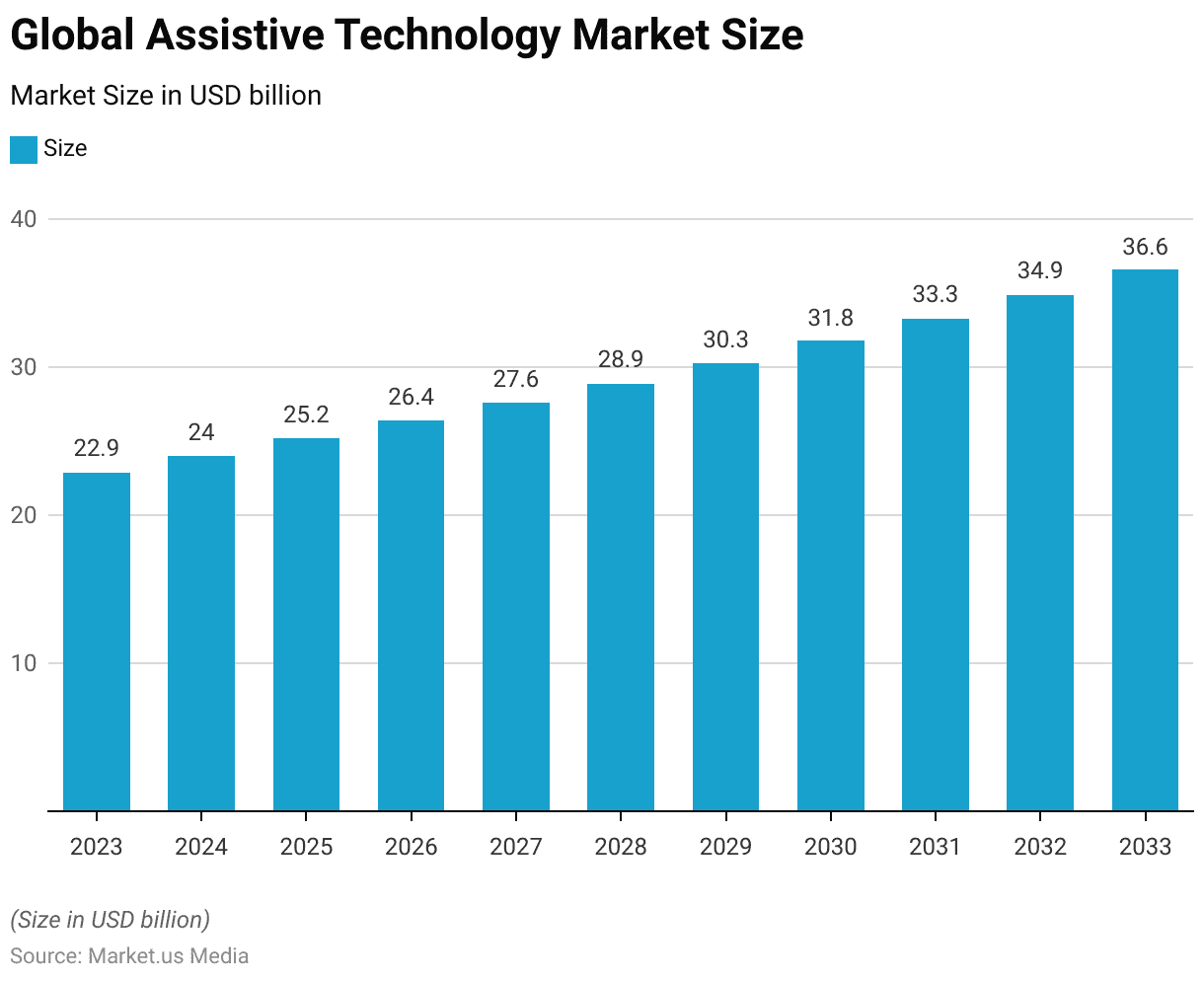

Global Assistive Technology Market Size Statistics

- The global assistive technology market is projected to experience steady growth over the coming decade at a CAGR of 4.8%.

- In 2023, the market size was estimated at USD 22.9 billion. With forecasts indicating consistent year-on-year increases.

- By 2024, the market is expected to reach USD 24.0 billion. Rising further to USD 25.2 billion in 2025 and USD 26.4 billion in 2026.

- This upward trajectory continues, with the market reaching USD 27.6 billion in 2027 and USD 28.9 billion in 2028.

- By 2029, the market size is projected to surpass USD 30.3 billion, and by the turn of the decade in 2030, it is anticipated to expand to USD 31.8 billion.

- Subsequent years see sustained growth, with the market estimated at USD 33.3 billion in 2031, USD 34.9 billion in 2032, and culminating at USD 36.6 billion in 2033.

- This consistent growth reflects the increasing demand for assistive technologies. Driven by advancements in innovation, healthcare needs, and accessibility requirements globally.

(Source: market.us)

Medical Assistive Technology Market Statistics

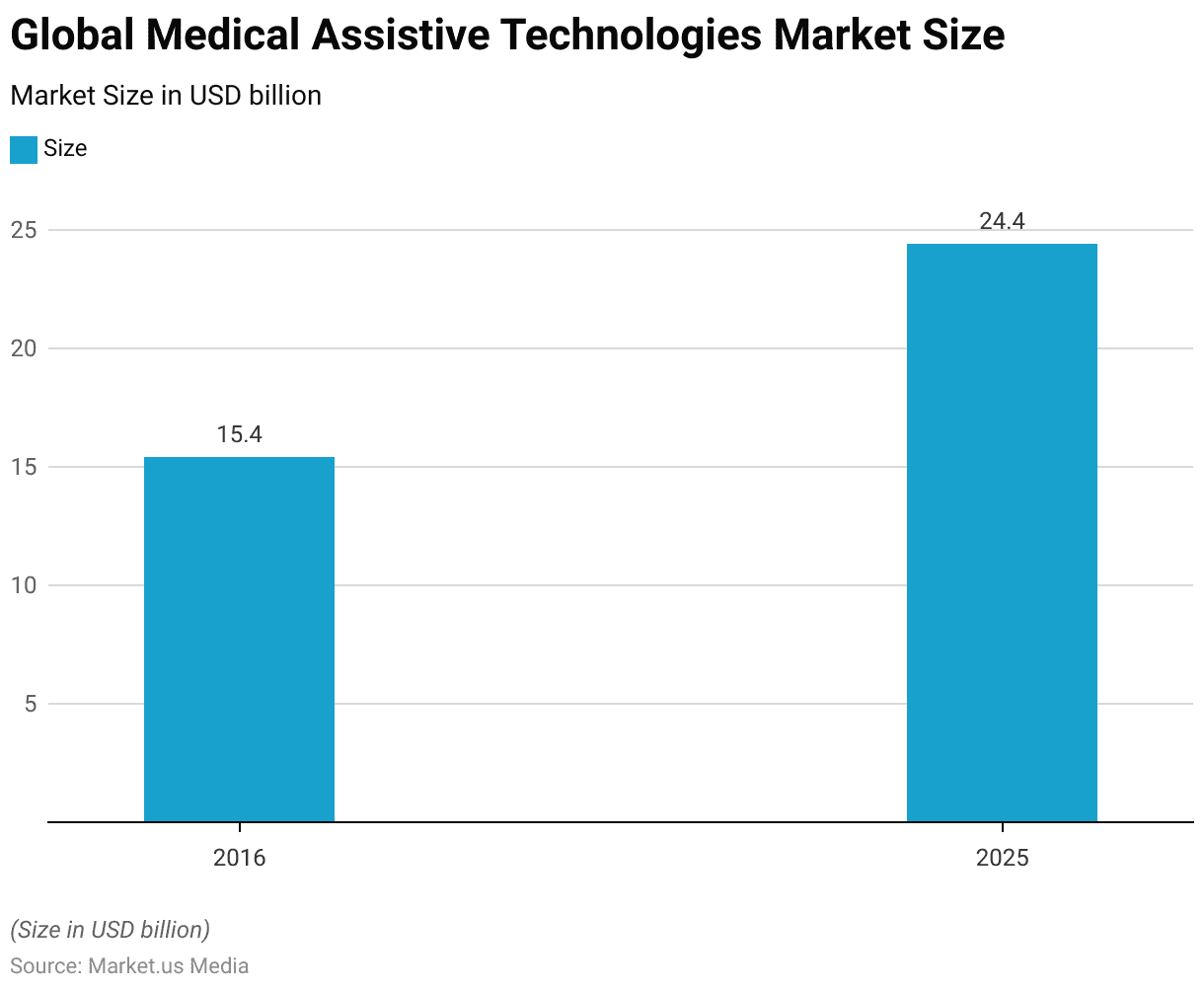

Global Medical Assistive Technology Market Size Statistics

- In 2016, the global market for medical assistive technologies was valued at USD 15.4 billion.

- This market is projected to experience significant growth. With forecasts indicating an increase to USD 24.4 billion by 2025.

- This growth underscores the rising demand for medical assistive technologies, driven by advancements in healthcare infrastructure. The increasing prevalence of chronic diseases, and a growing aging population worldwide.

(Source: Statista)

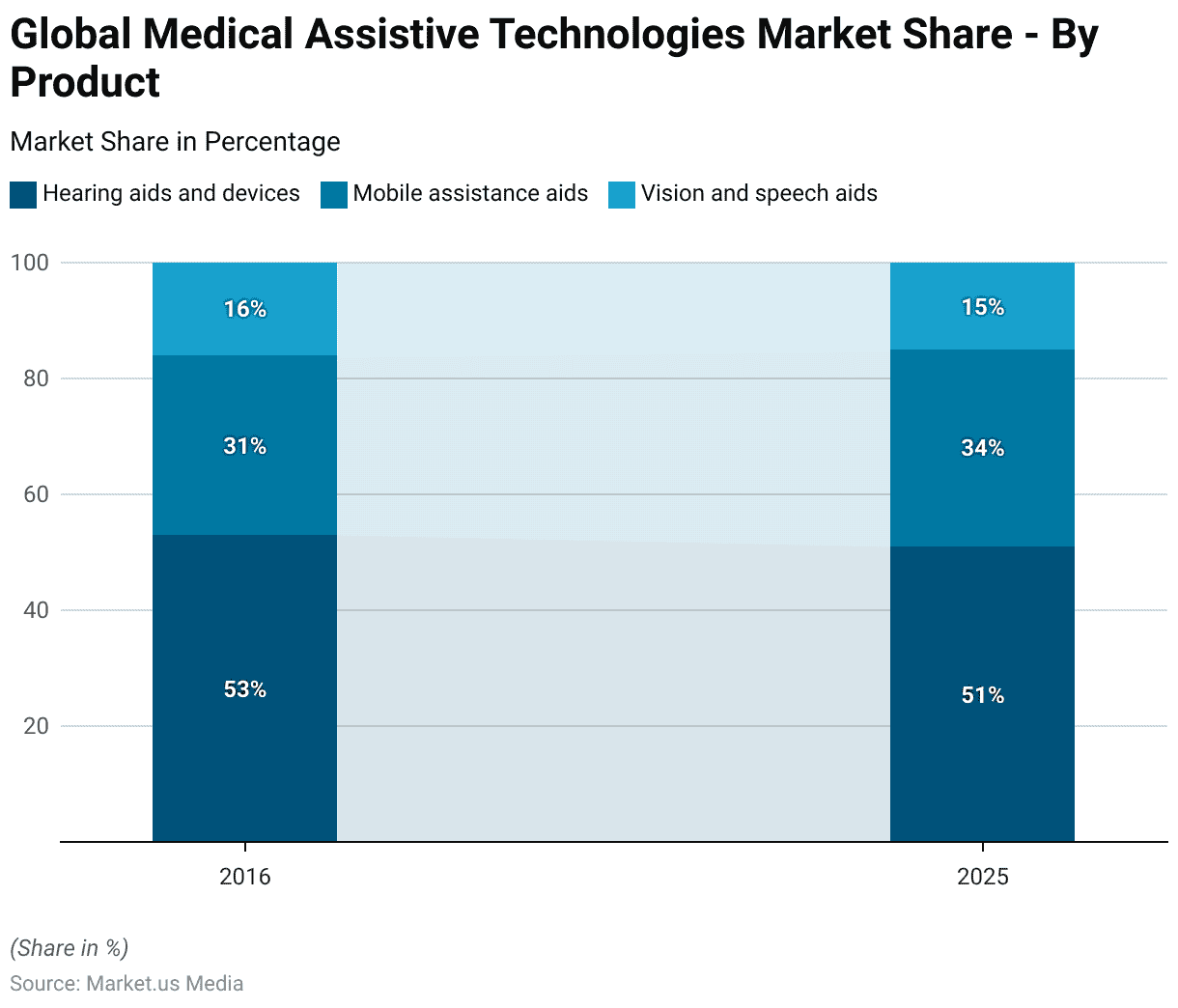

Global Medical Assistive Technology Market Share – By Product Statistics

- In 2016, hearing aids and devices held the largest share of the global medical assistive technologies market, accounting for 53% of the total.

- However, this share is forecasted to decline to 51% by 2025 slightly.

- Mobile assistance aids represented 31% of the market in 2016. Their share is projected to grow to 34% by 2025, reflecting increasing demand for mobility solutions.

- Vision and speech aids comprised 16% of the market in 2016. With a marginal decrease in their share expected, reaching 15% by 2025.

- These shifts indicate a growing emphasis on mobile assistance technologies alongside stable demand for other assistive products.

(Source: Statista)

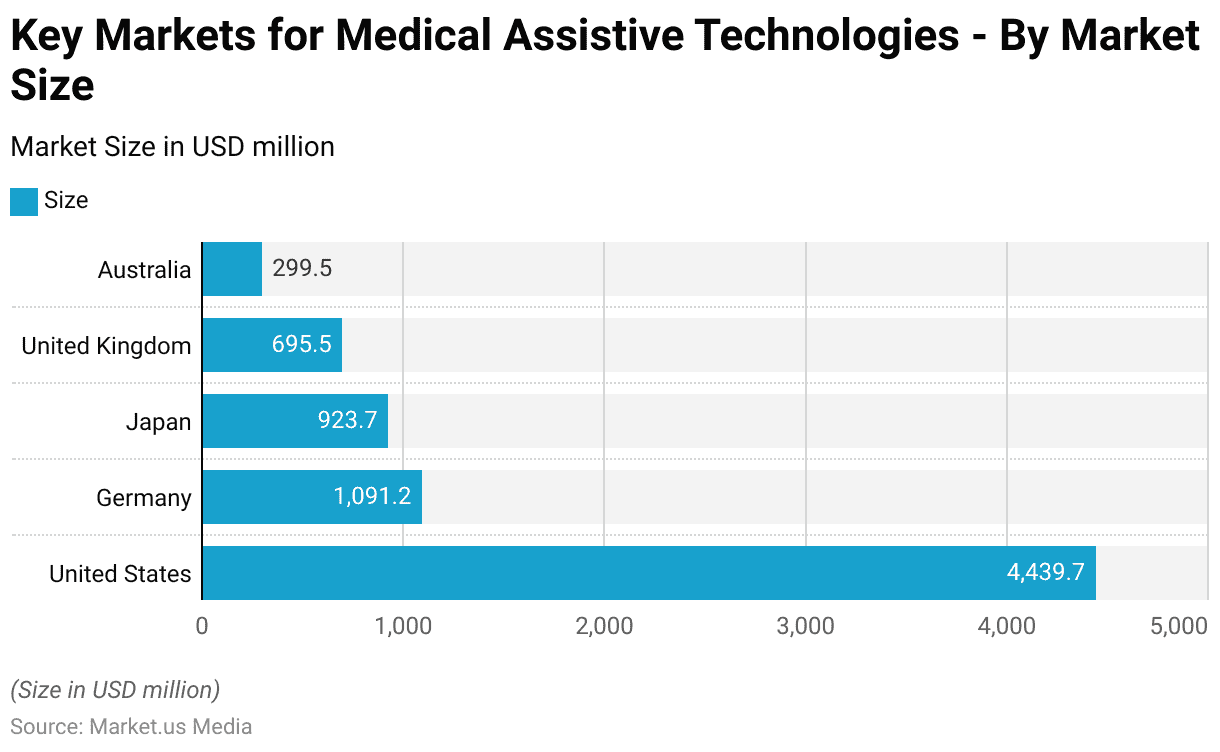

Key Markets for Medical Assistive Technology – By Market Size Statistics

- In 2016, the United States emerged as the largest market for medical assistive technologies. With a market size of USD 4,439.7 million, reflecting its advanced healthcare infrastructure and high adoption rates.

- Germany followed as the second-largest market, with a size of USD 1,091.2 million. Showcasing Europe’s strong demand for assistive technologies.

- Japan ranked third, with a market value of USD 923.7 million, driven by its aging population and focus on healthcare innovation.

- The United Kingdom had a market size of USD 695.5 million. Indicating significant adoption within the region.

- Australia, with a market size of USD 299.5 million, demonstrated a steady demand for assistive technologies, albeit on a smaller scale compared to the leading regions.

- This data highlights the geographic variation in market sizes. With developed countries leading the adoption of medical assistive technologies.

(Source: Statista)

Mobility Devices Market Overview

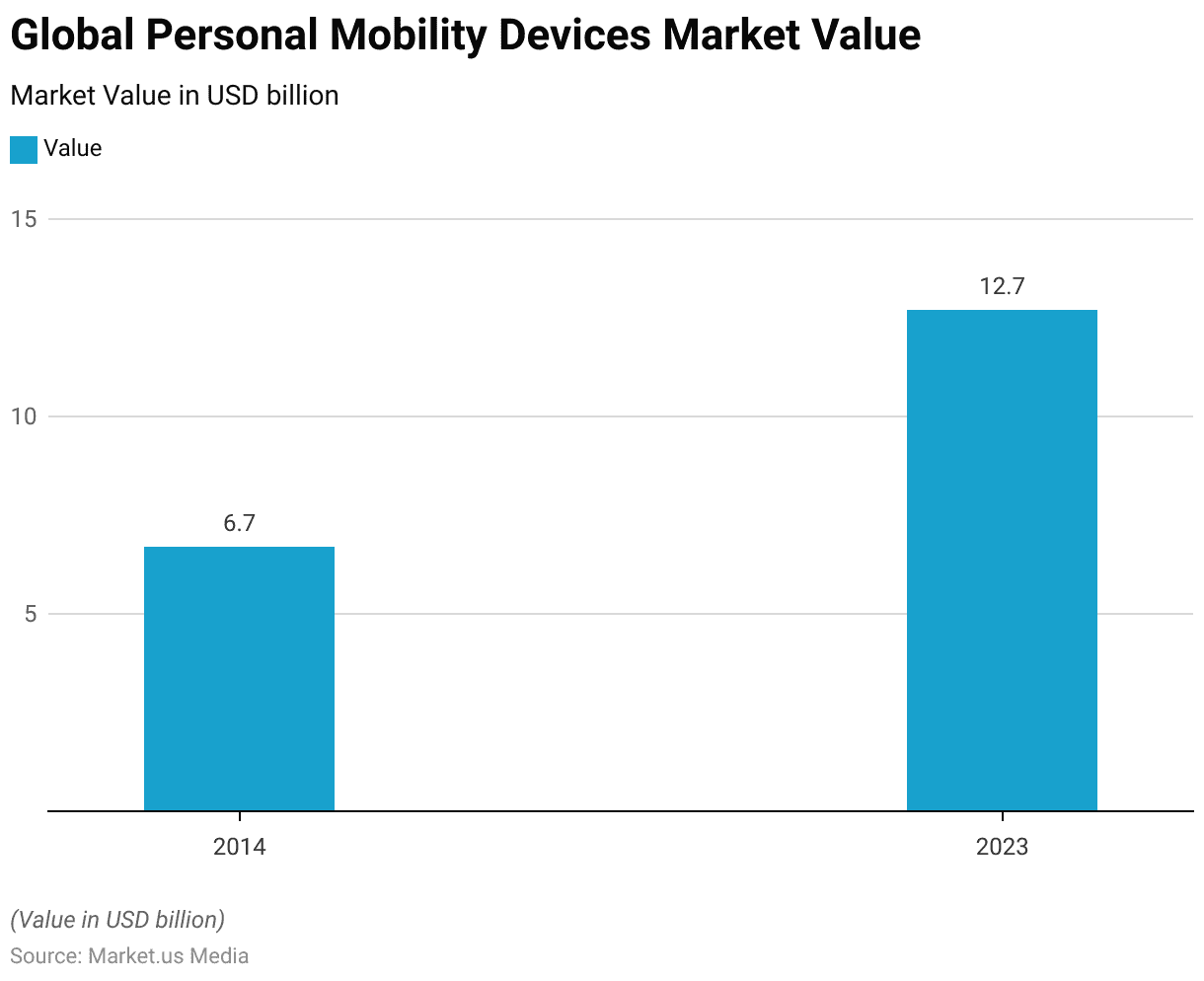

Global Personal Mobility Devices Market Value

- In 2014, the global personal mobility devices market was valued at USD 6.7 billion.

- This market has witnessed significant growth over the years. With its value projected to reach USD 12.7 billion by 2023.

- This growth highlights the increasing demand for mobility solutions, driven by factors such as an aging population. The rising prevalence of mobility impairments, and technological advancements in mobility devices.

(Source: Statista)

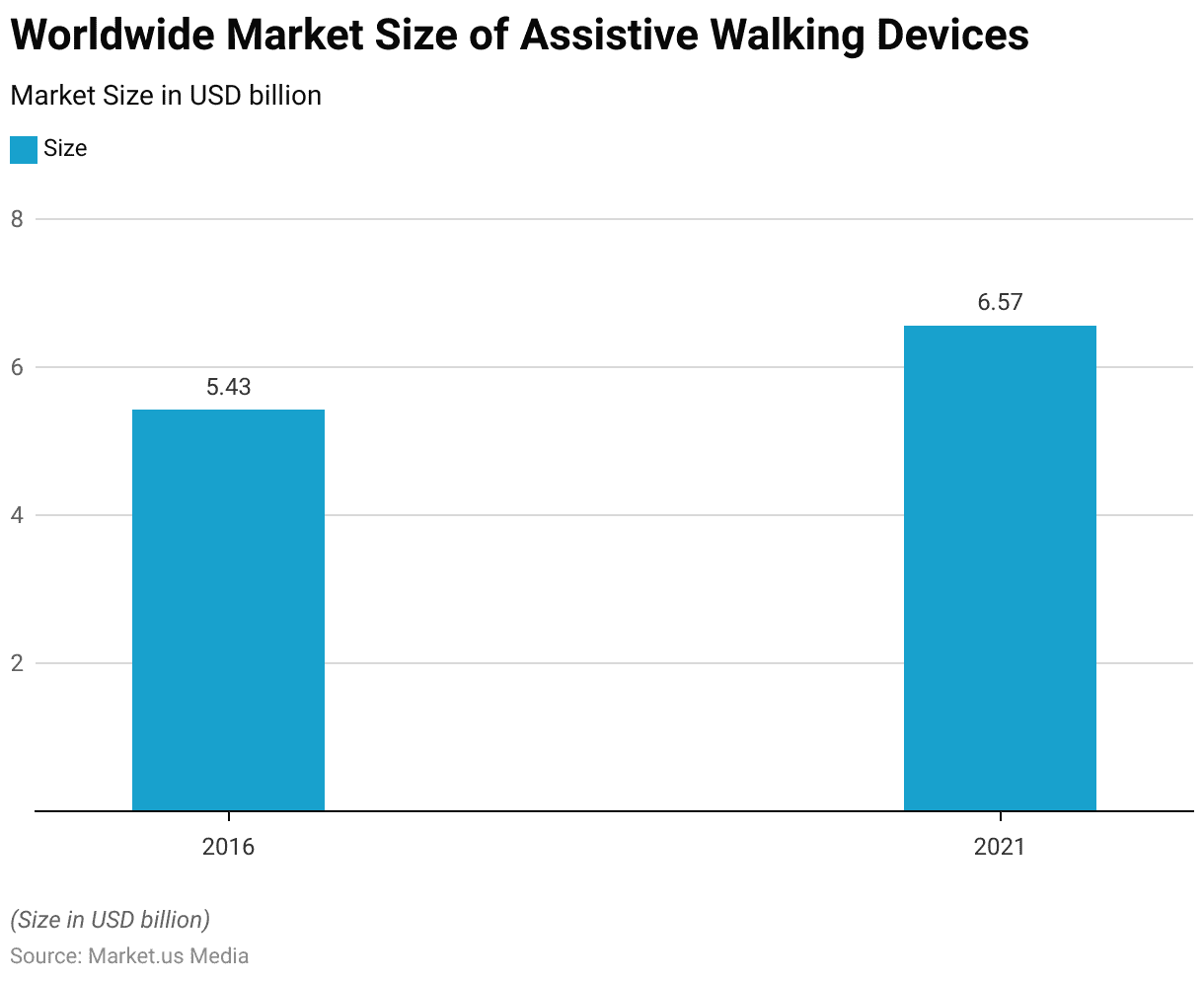

Worldwide Market Size of Assistive Walking Devices

- In 2016, the global market size for assistive walking devices was valued at USD 5.43 billion.

- By 2021, this market is projected to grow to USD 6.57 billion. Reflecting a steady increase over the next five years.

- This growth is driven by factors such as the rising elderly population. Increased prevalence of mobility-related conditions, and advancements in walking aid technologies. Which are enhancing accessibility and functionality for users worldwide.

(Source: Statista)

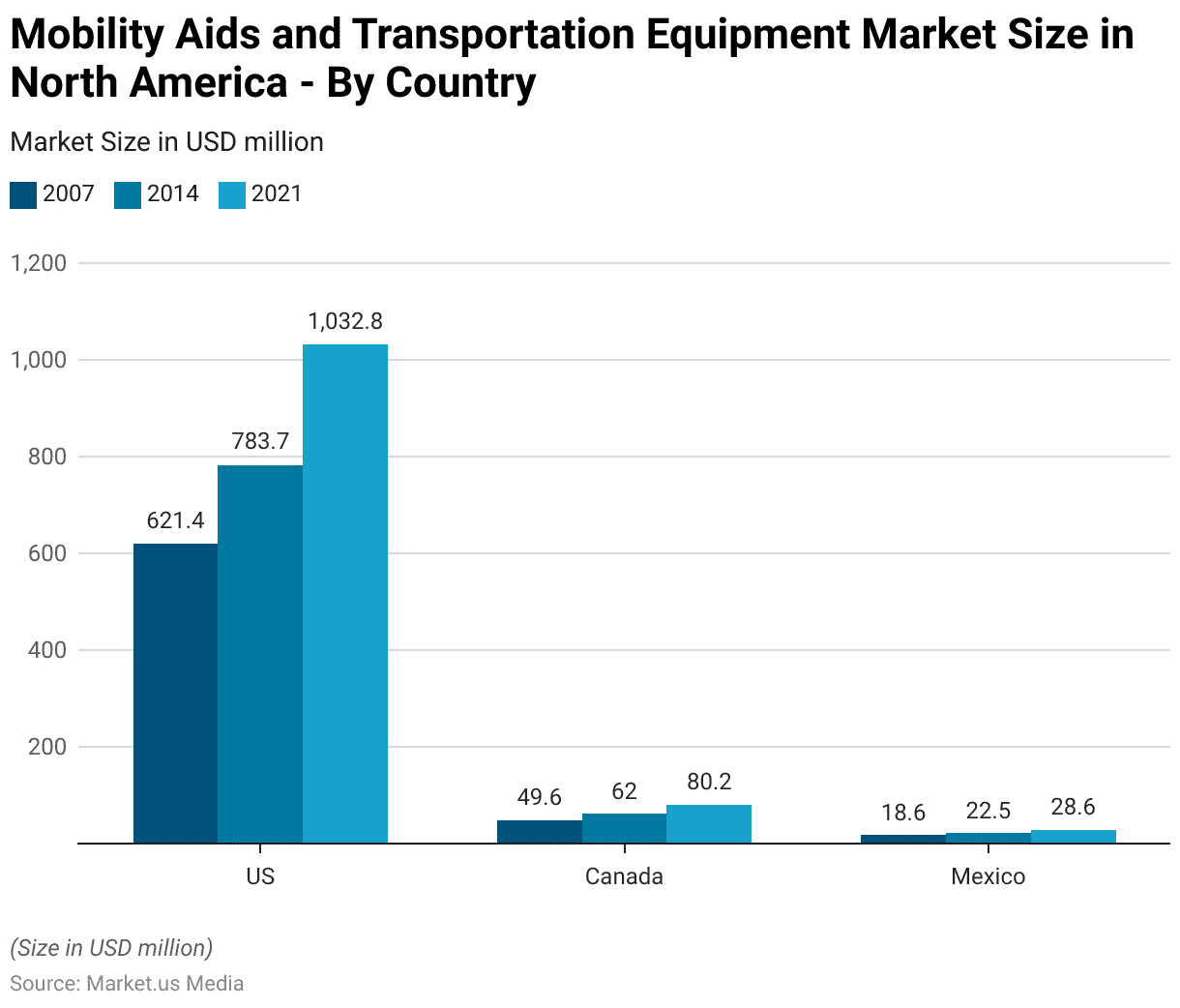

Mobility Aids and Transportation Equipment Market Size in North America – By Country

- The mobility aids and transportation equipment market in North America has exhibited consistent growth across key countries from 2007 to 2021.

- In the United States, the market size increased from USD 621.4 million in 2007 to USD 783.7 million in 2014. Further, it expanded to USD 1,032.8 million by 2021. Highlighting its position as the largest market in the region.

- Canada’s market also grew steadily, from USD 49.6 million in 2007 to USD 62 million in 2014, reaching USD 80.2 million by 2021.

- Similarly, Mexico’s market showed moderate growth. Rising from USD 18.6 million in 2007 to USD 22.5 million in 2014 and USD 28.6 million in 2021.

- This regional growth underscores the increasing demand for mobility aids and transportation equipment. Driven by aging populations, advancements in technology, and rising healthcare accessibility in North America.

(Source: Statista)

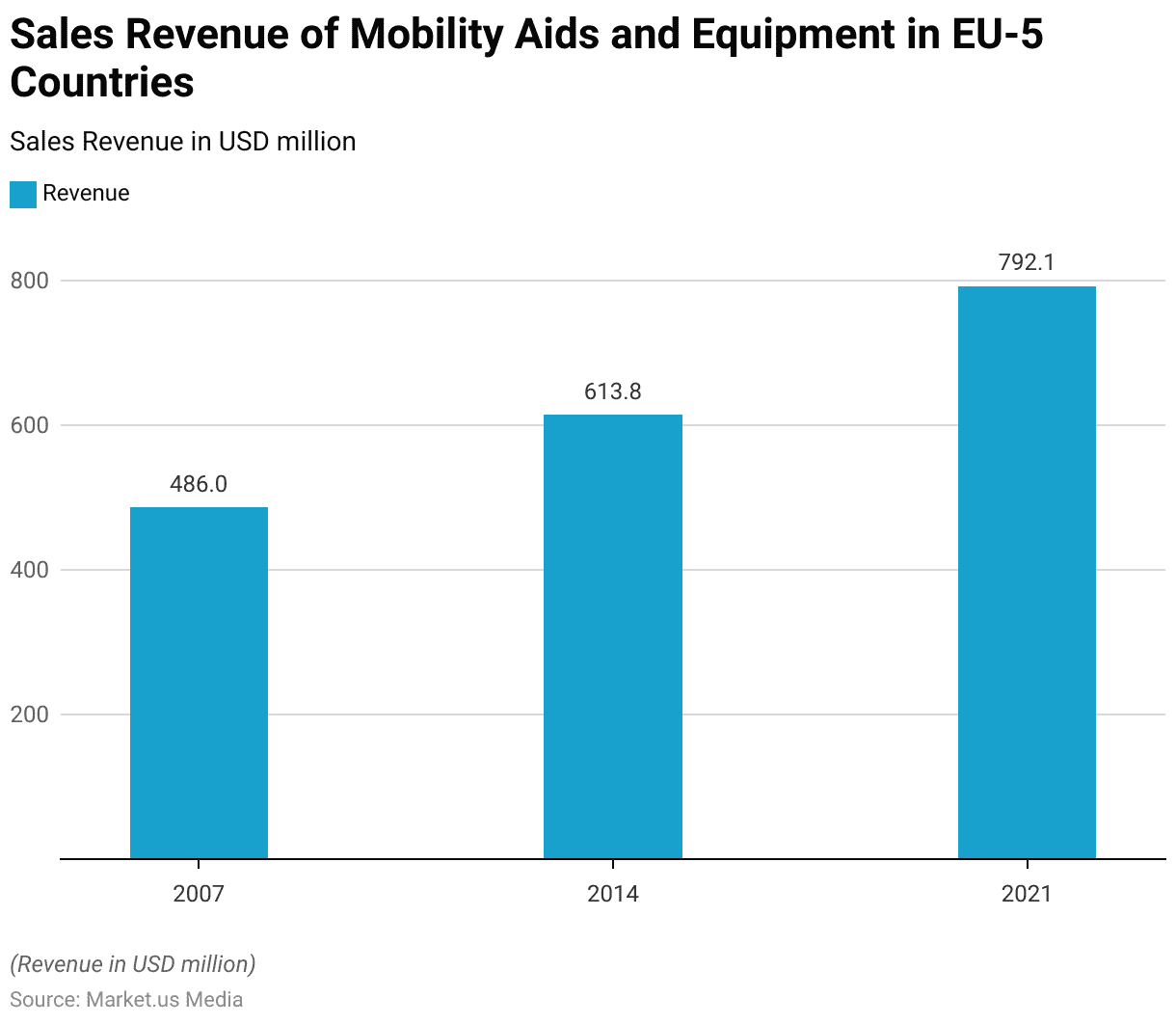

Sales Revenue of Mobility Aids and Equipment in Europe

- The revenue generated from mobility aids and transportation equipment in the EU-5 countries has shown a steady upward trend between 2007 and 2021.

- In 2007, the revenue was recorded at USD 486 million.

- By 2014, this figure had increased to USD 613.8 million. Reflecting a growing demand for these products.

- The revenue is further projected to reach USD 792.1 million by 2021. Signifying continued market expansion.

- This growth can be attributed to factors such as an aging population. The rising prevalence of mobility-related health conditions, and advancements in mobility technologies within the EU-5 region.

(Source: Statista)

Demographic Insights of Mobility Aid Users

Age

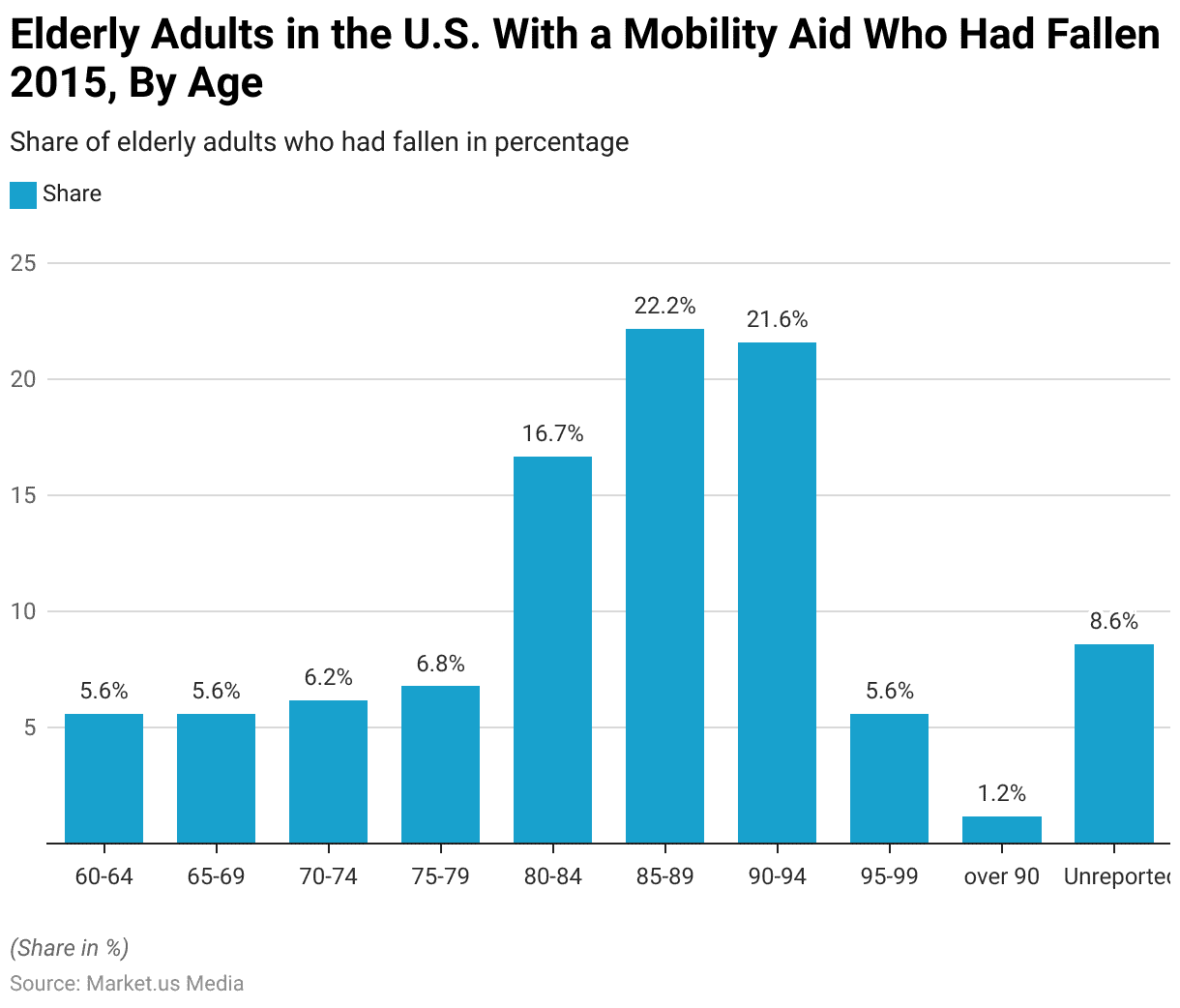

- As of 2015, the percentage of elderly U.S. adults who owned a cane or walker and had experienced a fall varied significantly across age groups.

- Among those aged 60-64 and 65-69, 5.6% reported falls. While this figure increased to 6.2% for those aged 70-74 and 6.8% for the 75-79 age group.

- A notable rise was observed in older age groups, with 16.7% of individuals aged 80-84 and 22.2% of those aged 85-89 reporting falls.

- The percentage slightly decreased to 21.6% for individuals aged 90-94 and dropped significantly to 5.6% among those aged 95-99.

- For individuals over 90 as a broader category, only 1.2% reported falls.

- Additionally, 8.6% of cases had unreported age data.

- These trends highlight a higher prevalence of falls among older age groups, particularly those between 80 and 94. Underscoring the importance of fall prevention measures in this population.

(Source: Statista)

Gender

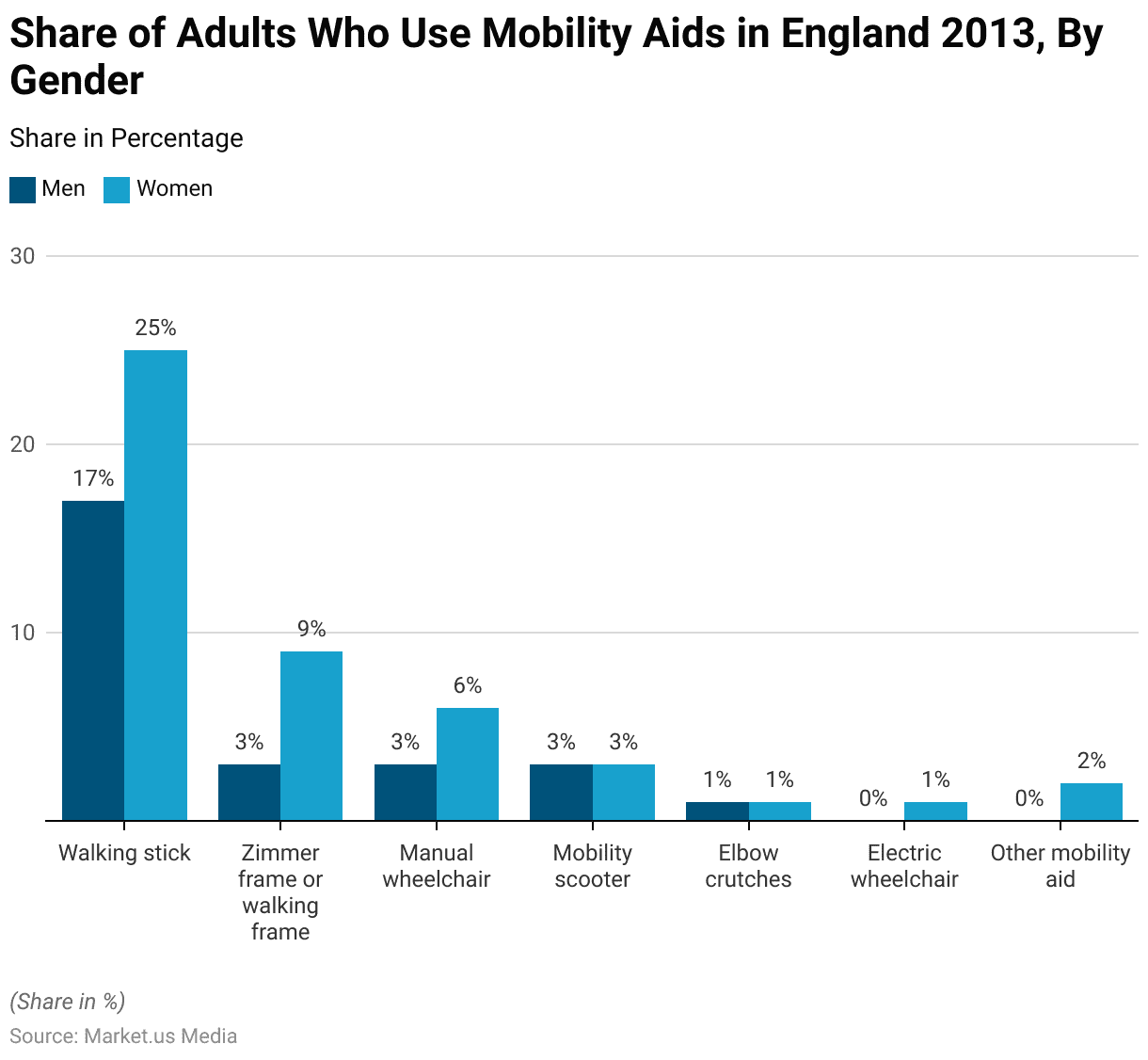

- In 2013, the use of mobility aids in England showed notable gender differences.

- Walking sticks were the most commonly used mobility aid, with 17% of men and 25% of women relying on them.

- Zimmer frames or walking frames were used by 3% of men compared to 9% of women. Indicating a higher prevalence of usage among women.

- Similarly, manual wheelchairs were utilized by 3% of men and 6% of women.

- Mobility scooters were equally used by both genders, with 3% of men and women reporting their usage.

- Elbow crutches were the choice for 1% of both men and women. While electric wheelchairs were exclusively used by 1% of women.

- Additionally, other mobility aids were reported by 2% of women and none of the men.

- These figures highlight the greater reliance of women on certain mobility aids. Particularly walking sticks and Zimmer frames, compared to men.

(Source: Statista)

E-learning Market Overview

Global Online Education/E-Learning Market Size

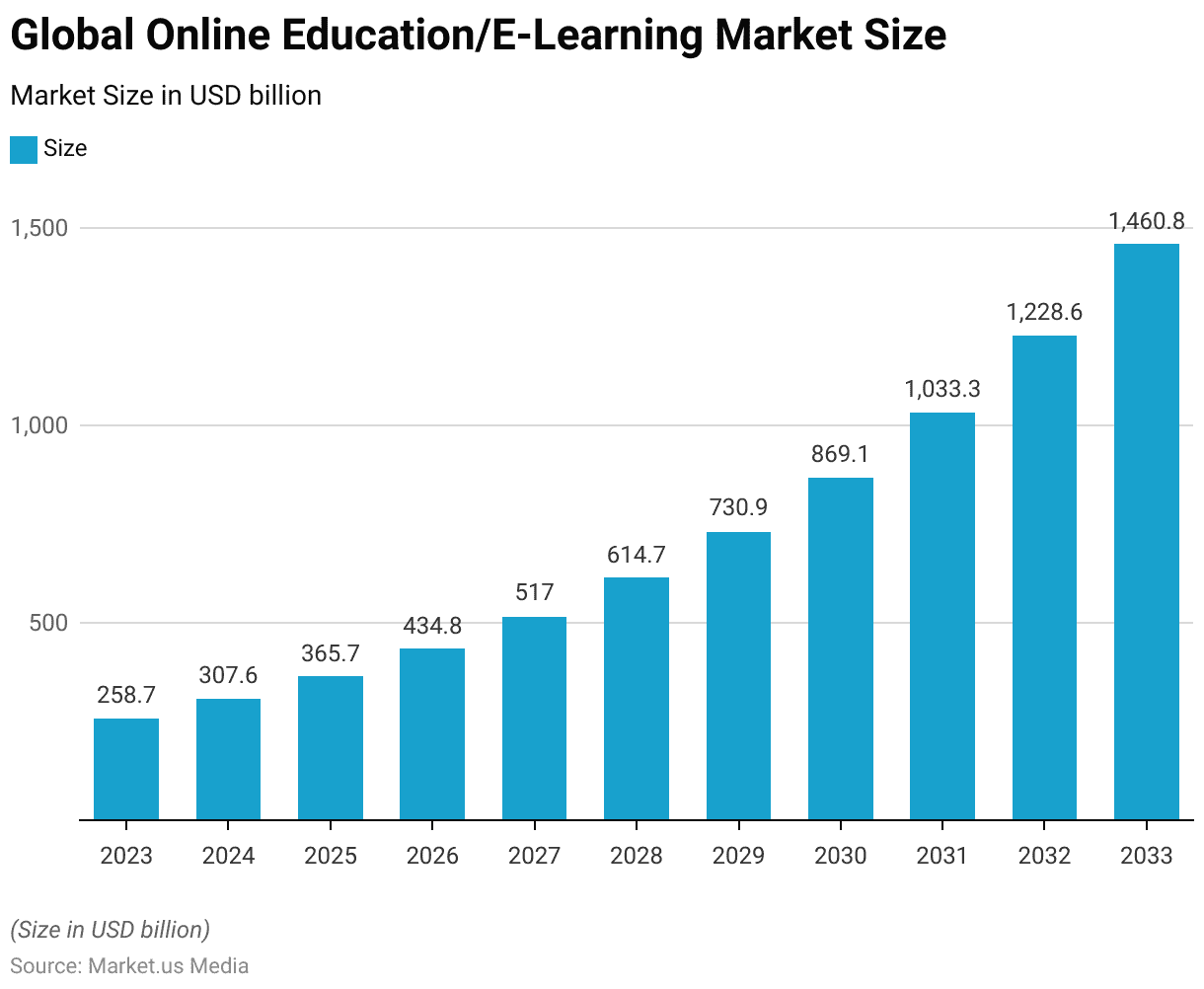

- The global online education and e-learning market is projected to experience substantial growth from 2023 to 2033.

- In 2023, the market size was estimated at USD 258.7 billion and is forecasted to increase to USD 307.6 billion in 2024 and USD 365.7 billion in 2025.

- This upward trend continues, with the market expected to reach USD 434.8 billion in 2026 and USD 517.0 billion in 2027.

- By 2028, the market is projected to grow to USD 614.7 billion. Further expanding to USD 730.9 billion in 2029 and USD 869.1 billion by 2030.

- The growth trajectory accelerates in the following years, with the market size anticipated to surpass USD 1,033.3 billion in 2031, USD 1,228.6 billion in 2032, and USD 1,460.8 billion by 2033.

- This remarkable growth reflects the increasing global adoption of digital learning solutions. Advancements in technology, and the growing emphasis on flexible, accessible education.

(Source: market.us)

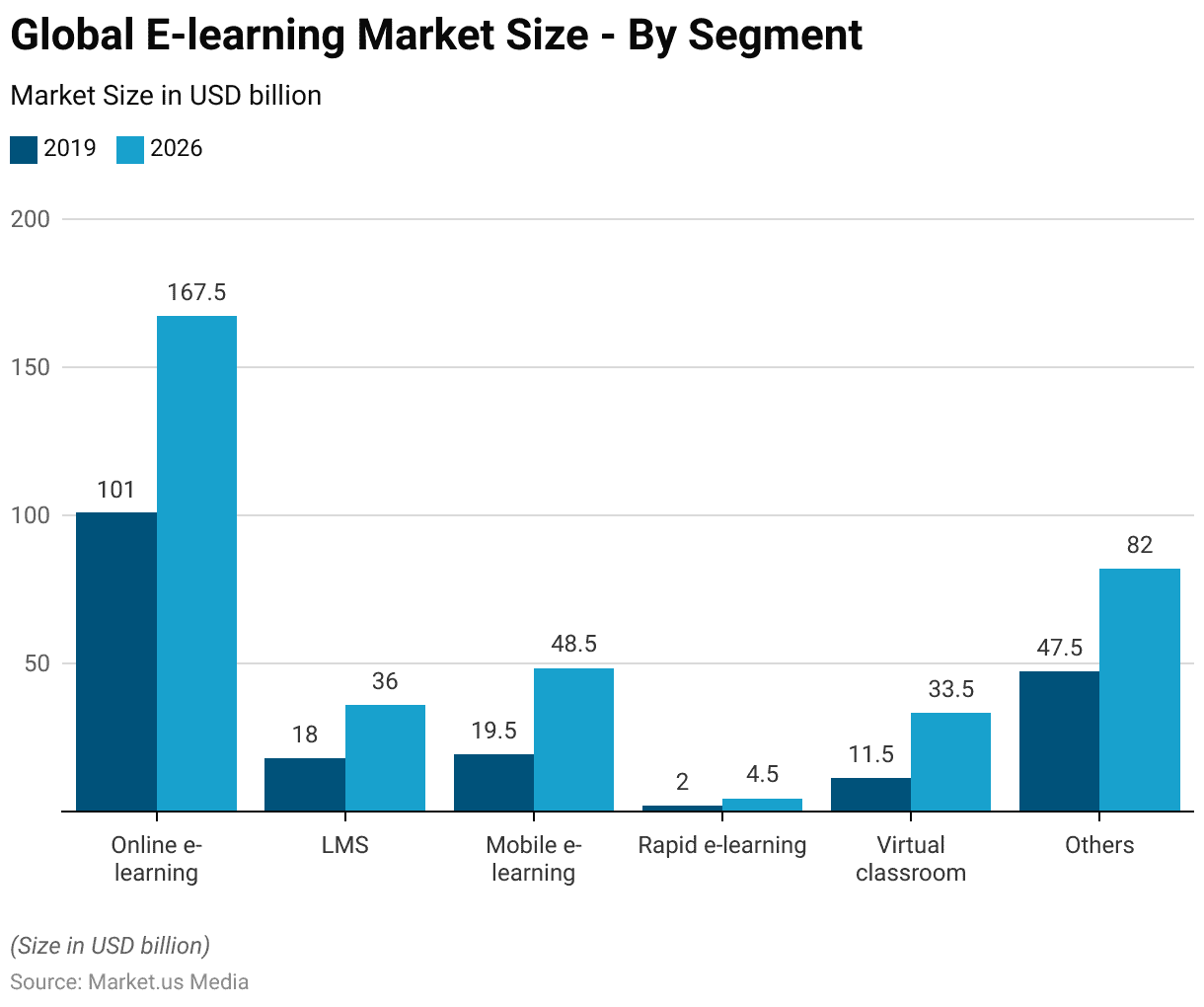

Global E-learning Market Size – By Segment

- The global e-learning market is projected to witness significant growth across various segments between 2019 and 2026.

- In 2019, the online e-learning segment led the market with a value of USD 101 billion. Which is expected to rise to USD 167.5 billion by 2026.

- Learning Management Systems (LMS) accounted for USD 18 billion in 2019, with forecasts predicting growth to USD 36 billion by 2026.

- Mobile e-learning was valued at USD 19.5 billion in 2019 and is expected to more than double, reaching USD 48.5 billion by 2026.

- The rapid e-learning segment, although smaller, is anticipated to grow from USD 2 billion in 2019 to USD 4.5 billion in 2026.

- Virtual classrooms, valued at USD 11.5 billion in 2019, are projected to grow significantly. Reaching USD 33.5 billion by 2026.

- Other e-learning solutions collectively accounted for USD 47.5 billion in 2019 and are forecasted to expand to USD 82 billion by 2026.

- These figures underscore the robust and widespread growth of the e-learning industry. Driven by advancements in technology and increased demand for flexible, digital education solutions.

(Source: Statista)

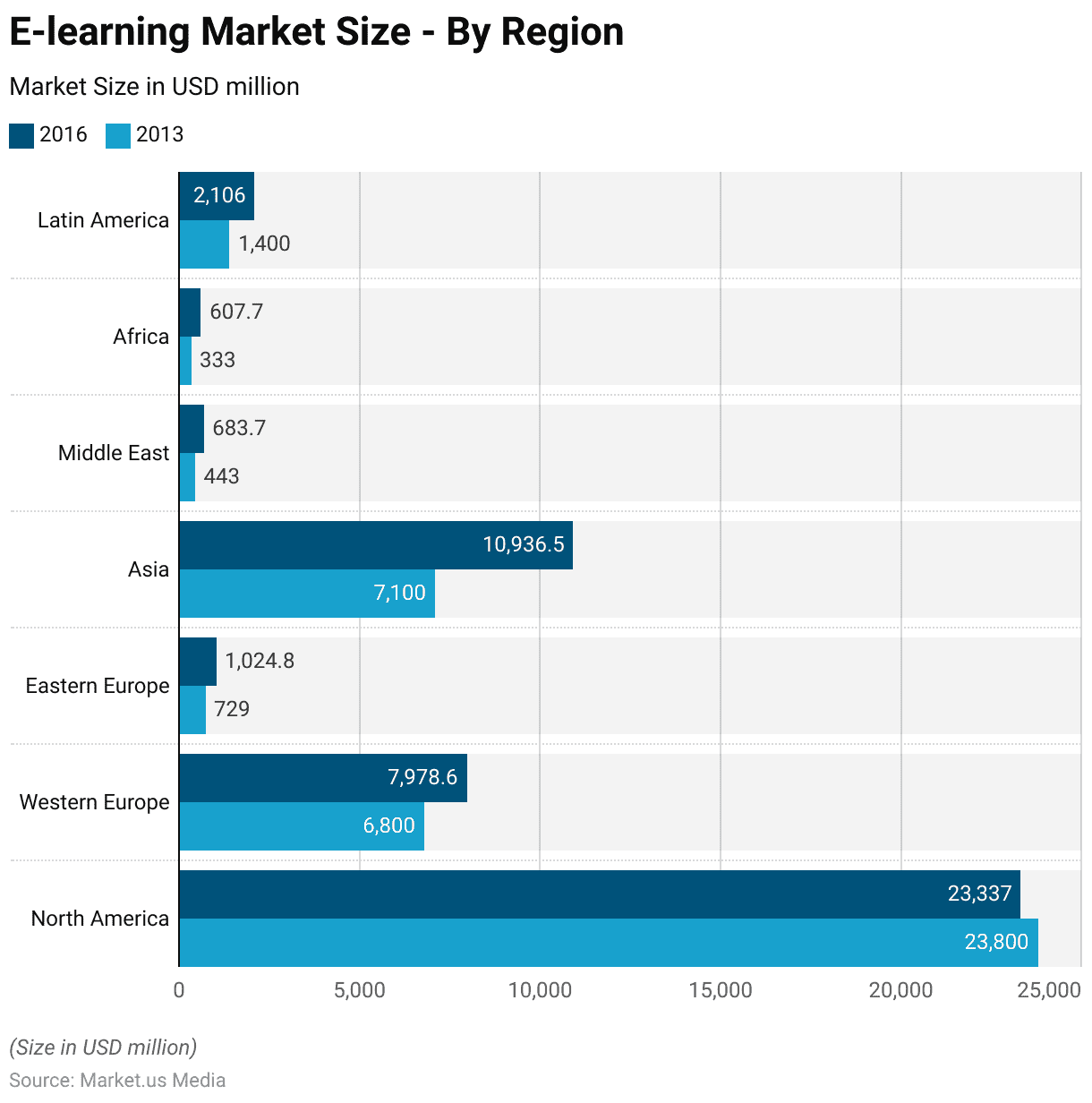

E-learning Market Size – By Region

- Between 2013 and 2016, the global e-learning market experienced significant growth across most regions.

- North America remained the largest market, with a slight decrease from USD 23,800 million in 2013 to USD 23,337 million in 2016.

- Western Europe saw substantial growth, increasing from USD 6,800 million in 2013 to USD 7,978.6 million in 2016.

- Eastern Europe experienced notable expansion as well, with the market growing from USD 729 million in 2013 to USD 1,024.8 million in 2016.

- Asia emerged as a key growth region, with the market size increasing dramatically from USD 7,100 million in 2013 to USD 10,936.5 million in 2016, reflecting a growing demand for digital education solutions.

- The Middle East’s market expanded from USD 443 million in 2013 to USD 683.7 million in 2016. Africa also saw significant growth. With the market size rising from USD 333 million to USD 607.7 million over the same period.

- In Latin America, the market grew from USD 1,400 million in 2013 to USD 2,106 million in 2016.

- This data highlights the global expansion of e-learning. Driven by technological advancements and increasing demand for accessible education across diverse regions.

(Source: Statista)

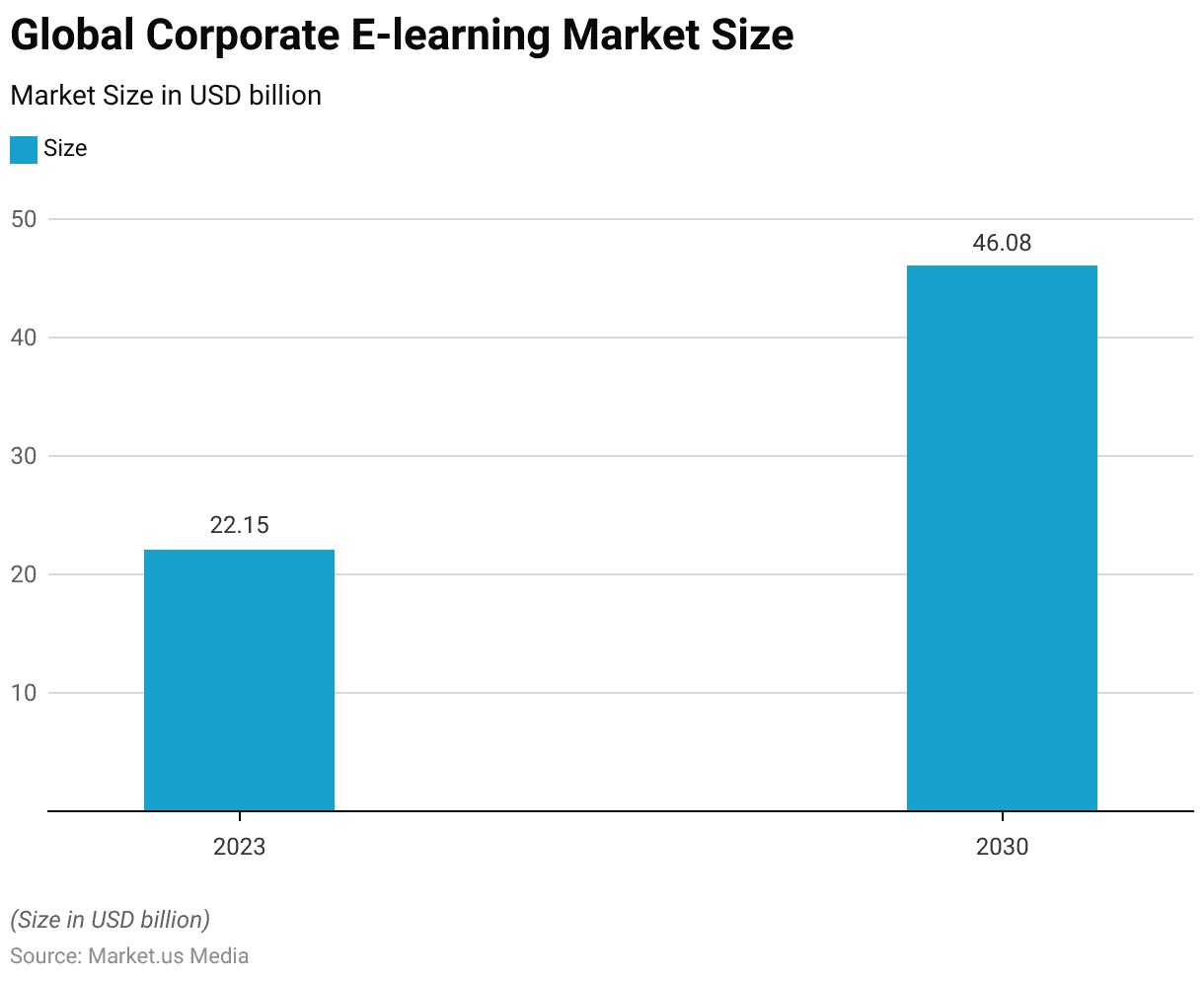

Global Corporate E-learning Market Size

- In 2023, the global corporate e-learning market was valued at USD 22.15 billion.

- This market is projected to experience significant growth. More than doubling by 2030, when it is expected to reach USD 46.08 billion.

- This expansion highlights the increasing adoption of e-learning solutions in corporate training and development. Driven by advancements in technology, cost efficiency, and the growing demand for flexible and scalable learning platforms in the business sector.

(Source: Statista)

Hearing Aids Market Overview

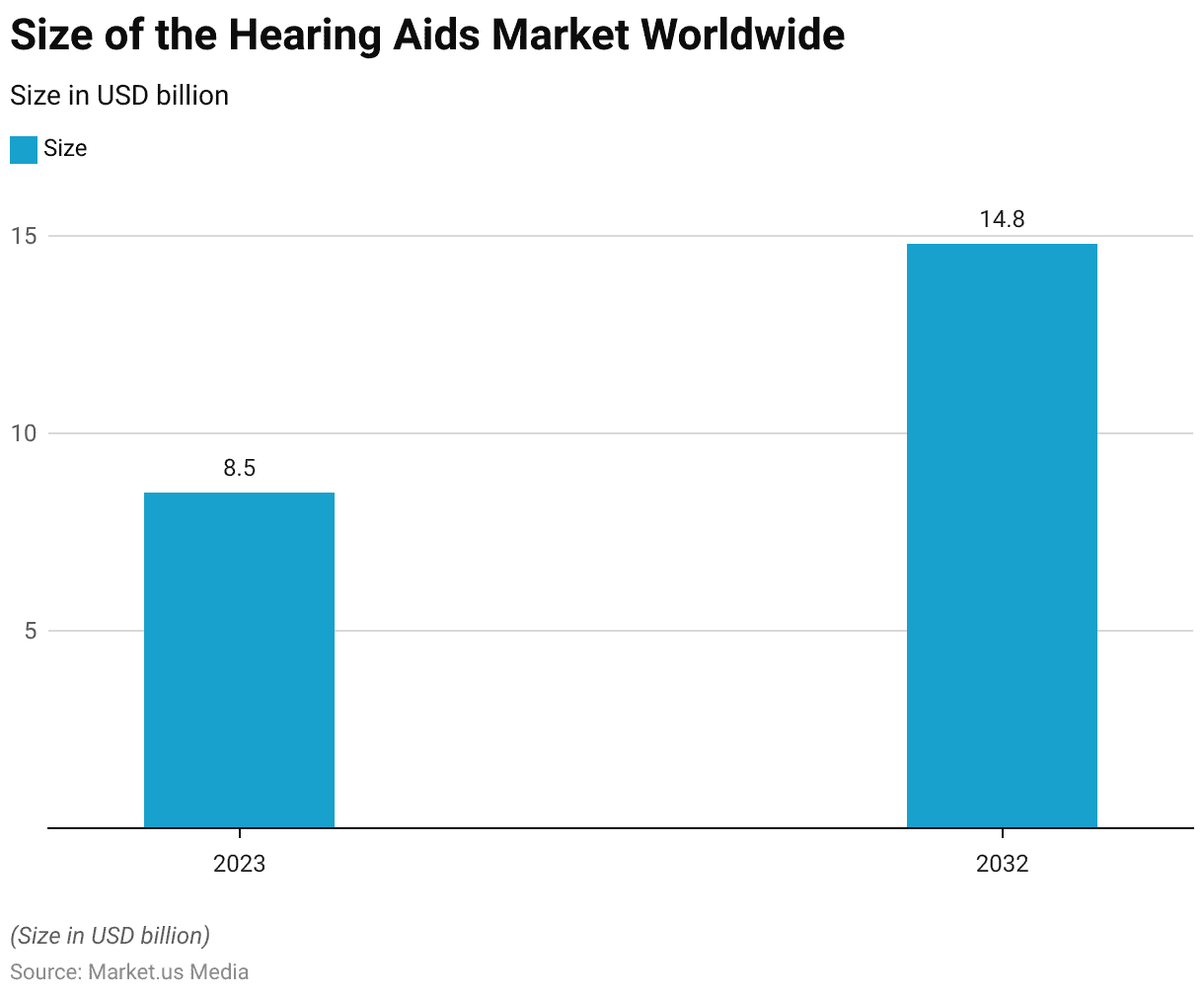

Size of the Hearing Aids Market Worldwide

- In 2023, the global hearing aids market was valued at USD 8.5 billion.

- This market is projected to grow significantly, reaching an estimated size of USD 14.8 billion by 2032.

- This substantial growth reflects an increasing demand for hearing aids, driven by a rising prevalence of hearing impairments. Advancements in hearing aid technology, and growing awareness and accessibility to auditory healthcare worldwide.

(Source: Statista)

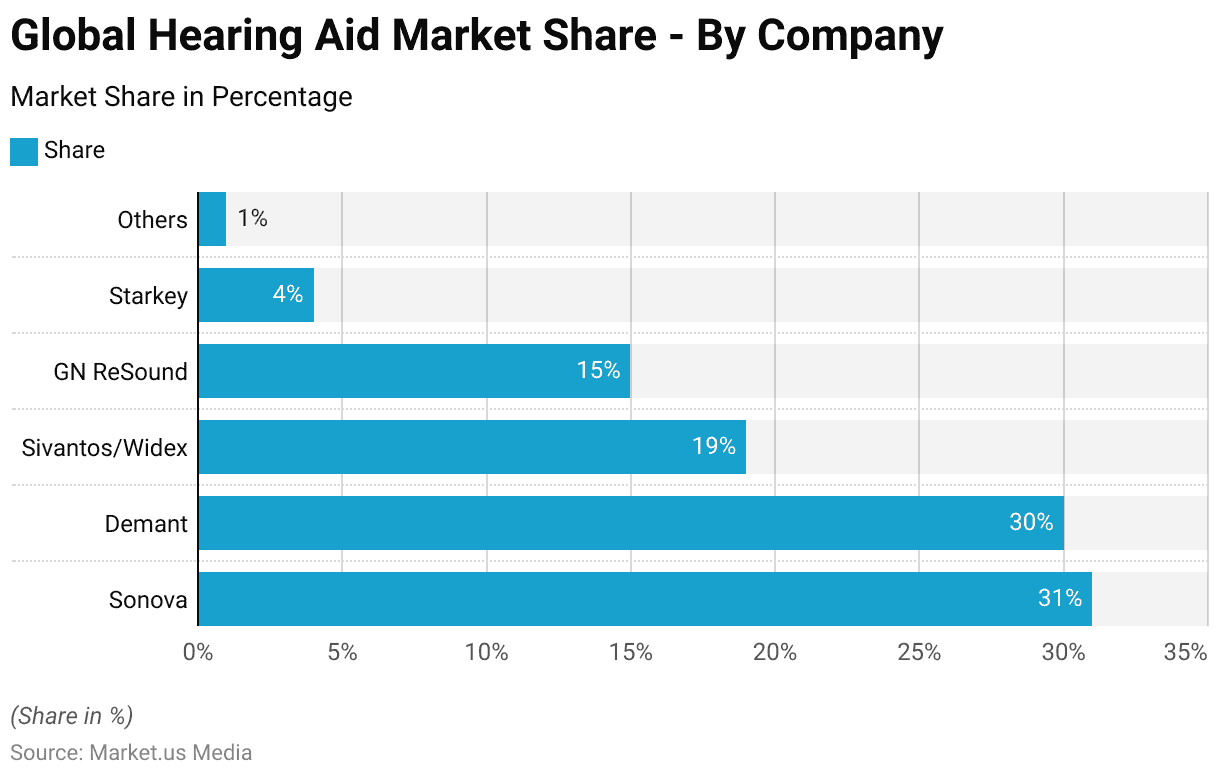

Global Hearing Aid Market Share – By Company

- As of 2019, the global hearing aid market was dominated by a few key players.

- Sonova held the largest share at 31%, closely followed by Demant. Which accounted for 30% of the market.

- Sivantos/Widex captured 19% of the market, while GN ReSound accounted for 15%.

- Starkey had a smaller share at 4%, and other companies collectively made up just 1% of the market.

- This distribution highlights the highly consolidated nature of the hearing aid industry. With a few major players controlling the vast majority of the market.

(Source: Statista)

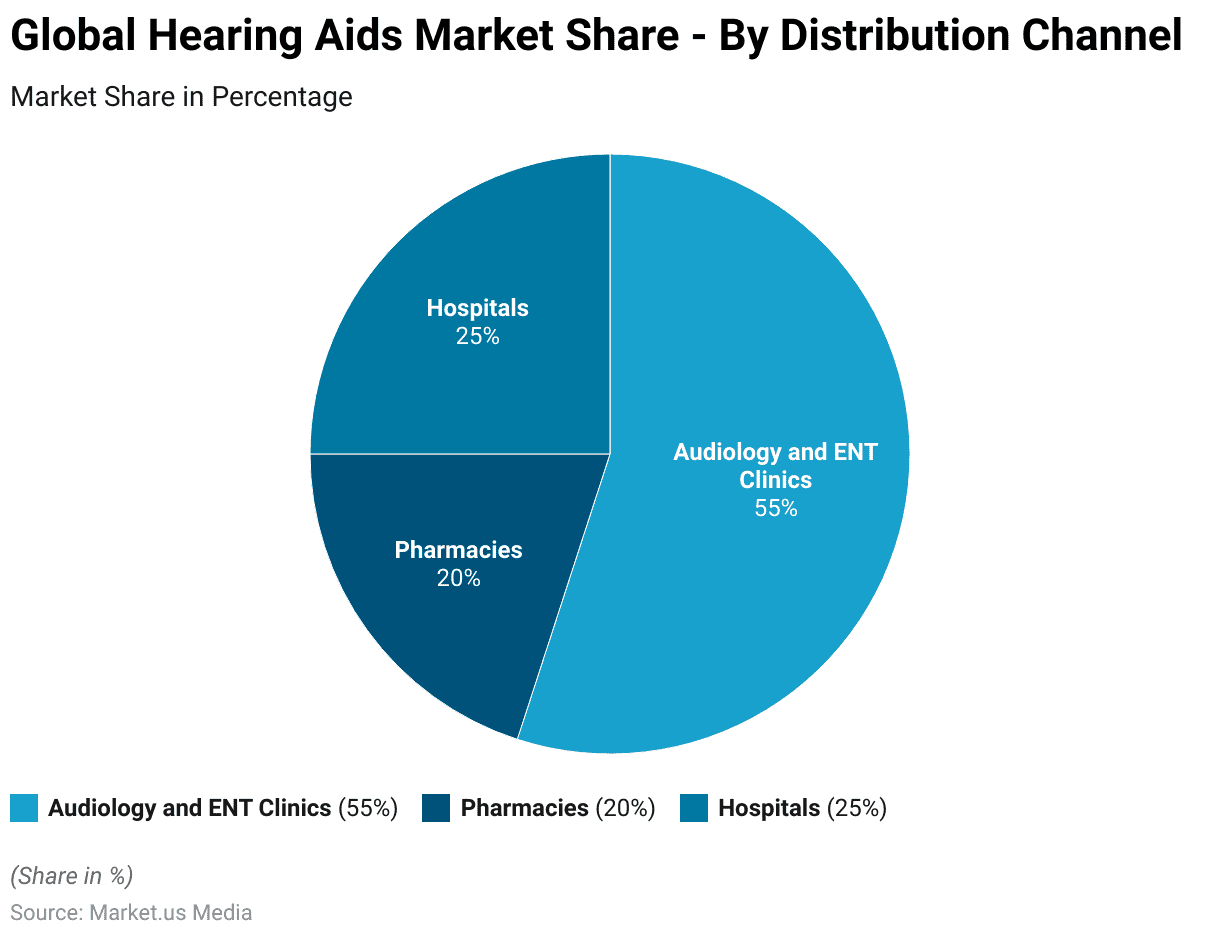

Global Hearing Aids Market Share – By Distribution Channel

- In 2018, the global hearing aids market was predominantly driven by audiology and ENT clinics. Which accounted for 55% of the distribution channel market share.

- Hospitals represented the second-largest channel, contributing 25% to the market.

- Pharmacies held a smaller share of 20%, reflecting their more limited role in hearing aid distribution compared to specialized clinics and hospitals.

- This distribution highlights the critical importance of specialized audiology services and medical facilities in the delivery and fitting of hearing aids.

(Source: Statista)

Hearing Aids Sales Statistics

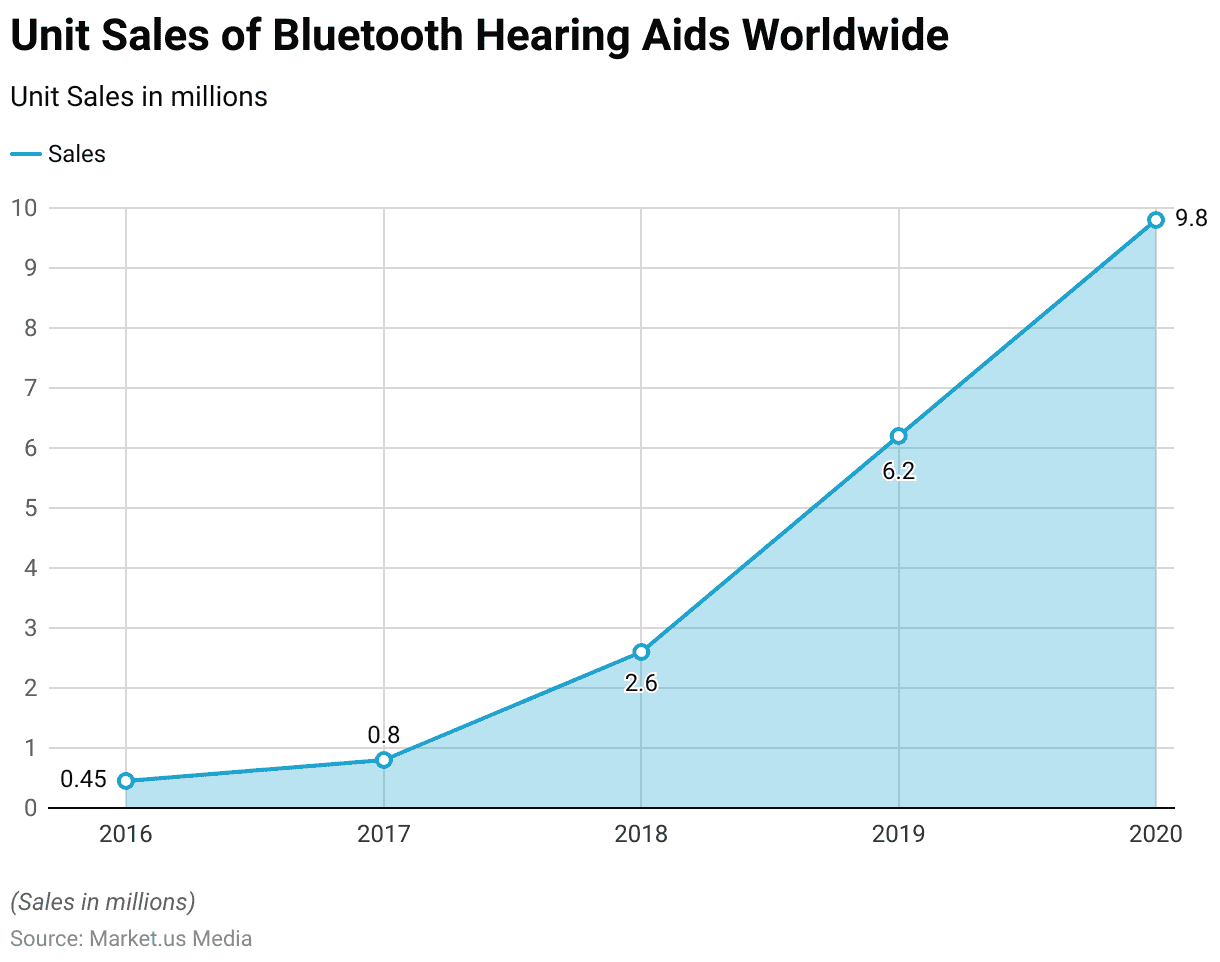

Unit Sales of Bluetooth Hearing Aids Worldwide

- The global unit sales of Bluetooth hearing aids experienced remarkable growth between 2016 and 2020.

- In 2016, sales were relatively low at 0.45 million units but nearly doubled to 0.8 million units in 2017.

- This upward trend continued, with sales significantly increasing to 2.6 million units in 2018.

- By 2019, the market had expanded further, with 6.2 million units sold. Showcasing the rapid adoption of Bluetooth-enabled hearing technology.

- The growth peaked in 2020, reaching 9.8 million units. Reflecting the rising demand for advanced hearing solutions with connectivity features.

- This trend highlights the growing popularity and acceptance of Bluetooth hearing aids globally.

(Source: Statista)

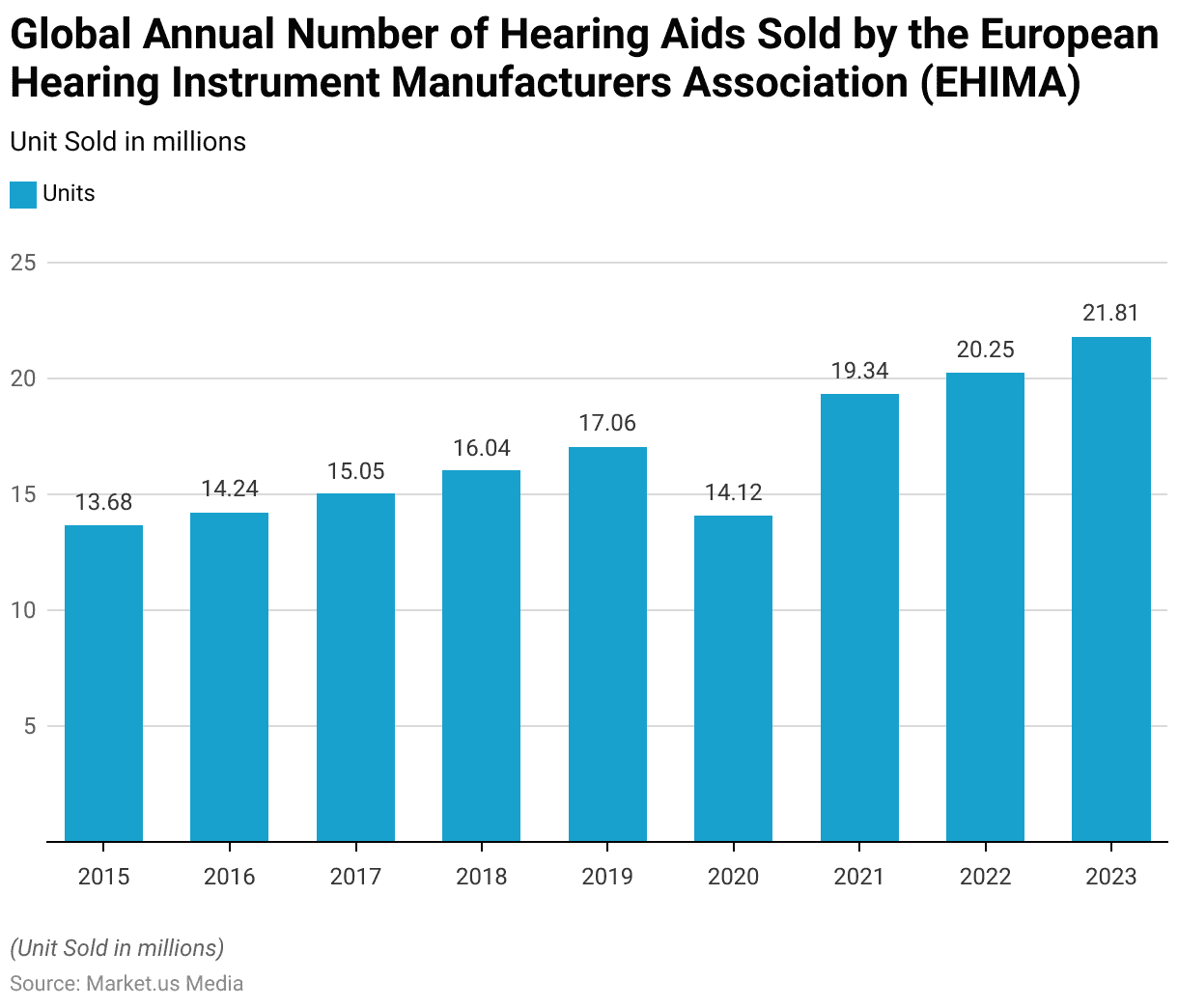

EHIMA Hearing Aid Sales Worldwide

- From 2015 to 2023, the annual global number of hearing aids sold by the European Hearing Instrument Manufacturers Association (EHIMA) demonstrated a general upward trend. With fluctuations observed in 2020 due to external factors likely impacting the market.

- In 2015, 13.68 million units were sold, increasing to 14.24 million in 2016 and 15.05 million in 2017.

- Sales continued to grow, reaching 16.04 million in 2018 and 17.06 million in 2019.

- However, a decline occurred in 2020, with sales dropping to 14.12 million. Potentially reflecting the impact of the COVID-19 pandemic.

- The market rebounded strongly in 2021, with sales surging to 19.34 million units. Followed by further growth to 20.25 million in 2022 and 21.81 million in 2023.

- This sustained growth underscores increasing global demand for hearing aids driven by rising awareness, aging populations, and technological advancements.

(Source: Statista)

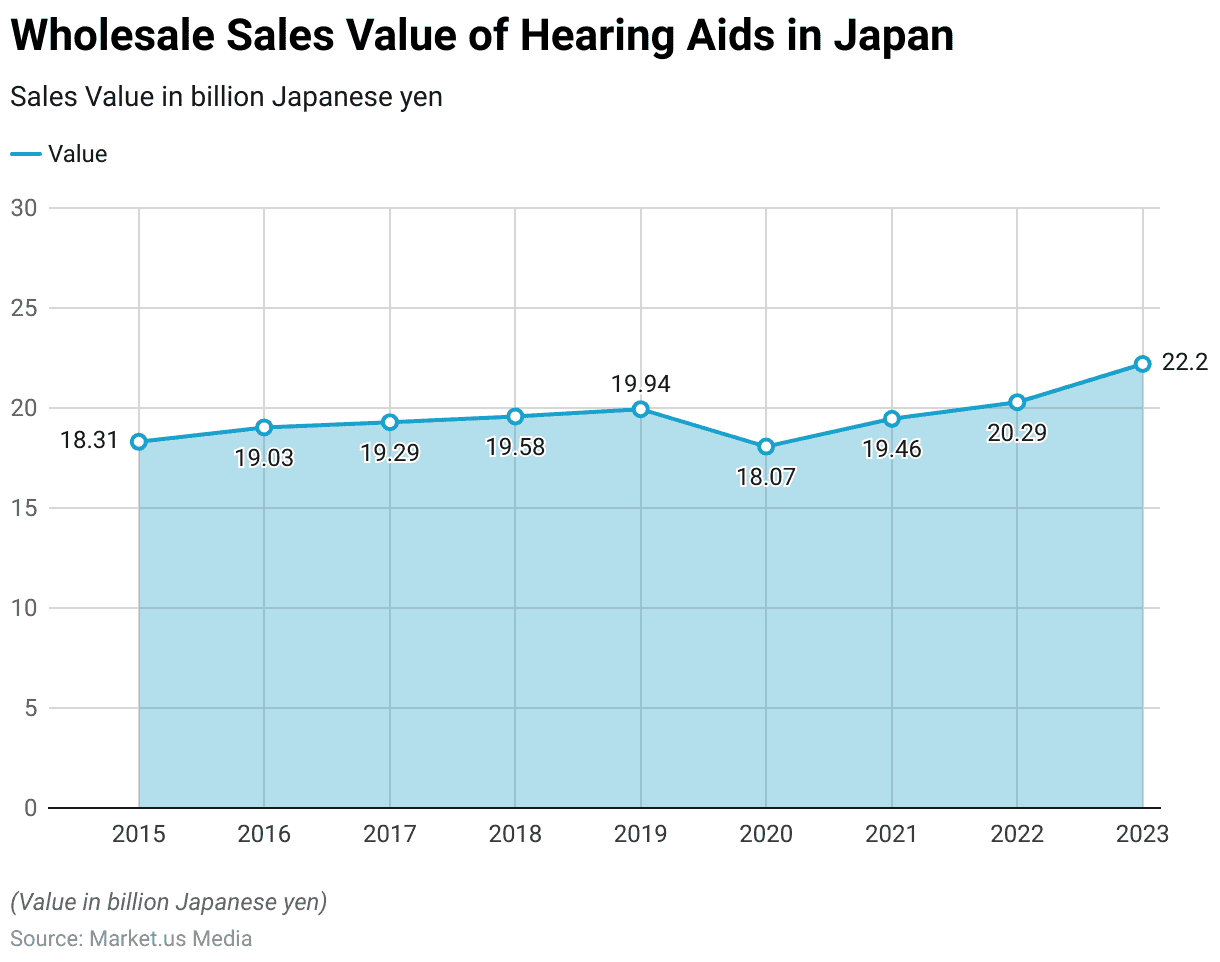

Sales Value of Hearing Aids in Japan

- Between 2015 and 2023, the wholesale sales value of hearing aids in Japan showed a generally upward trend, with some fluctuations.

- In 2015, the sales value stood at 18.31 billion Japanese yen. Rising steadily to 19.03 billion in 2016, 19.29 billion in 2017, and 19.58 billion in 2018.

- By 2019, sales had reached 19.94 billion yen.

- However, in 2020, the market experienced a decline. With sales dropping to 18.07 billion yen, likely due to the impact of the COVID-19 pandemic.

- The market rebounded in subsequent years, increasing to 19.46 billion yen in 2021 and 20.29 billion yen in 2022.

- By 2023, the sales value reached 22.2 billion yen, reflecting strong growth and a resurgence in demand for hearing aids in Japan. Driven by factors such as an aging population and advancements in hearing aid technology.

(Source: Statista)

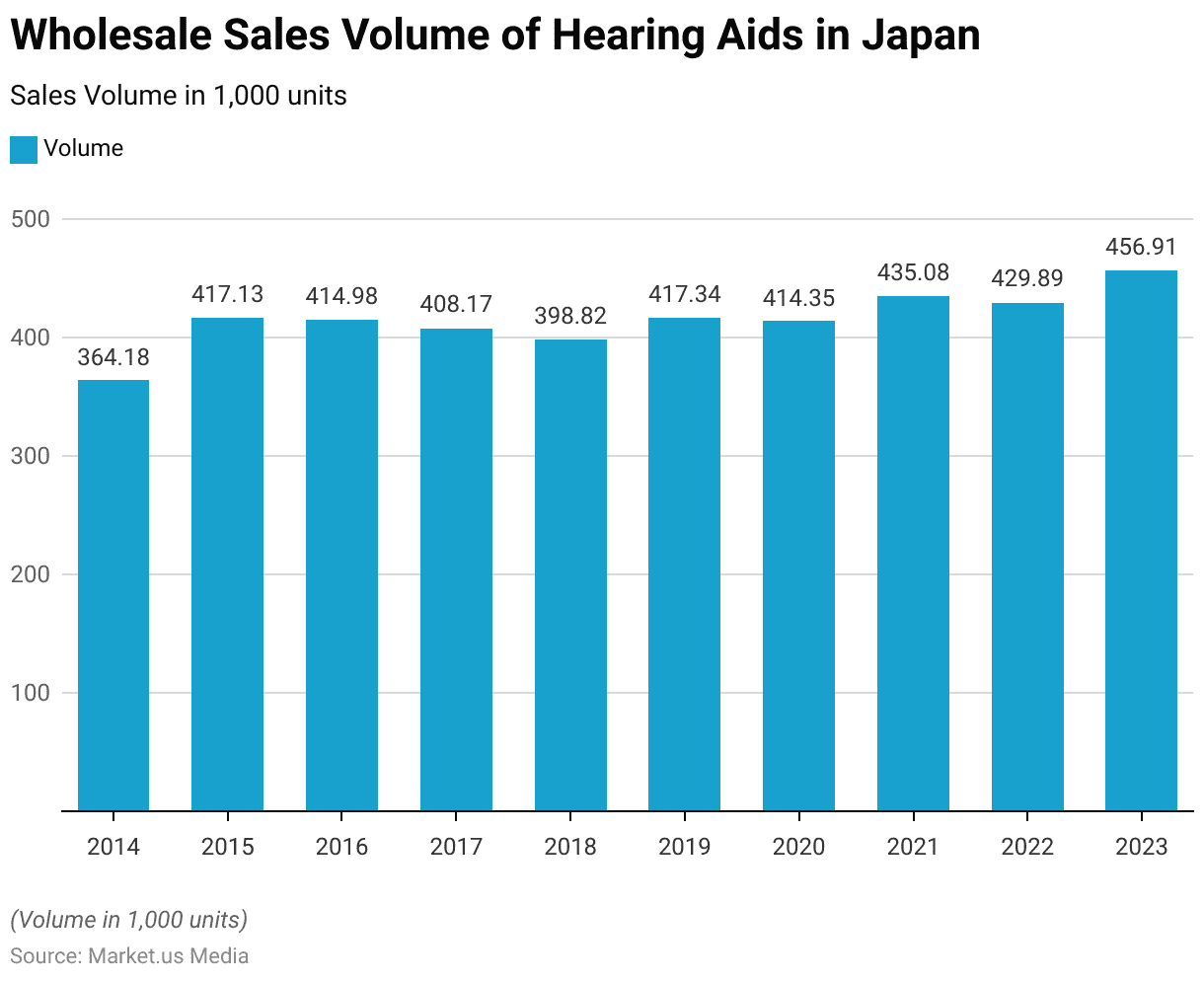

Sales Volume of Hearing Aids in Japan

- Between 2014 and 2023, the wholesale sales volume of hearing aids in Japan showed a fluctuating but generally upward trend.

- In 2014, the sales volume was 364.18 thousand units, increasing significantly to 417.13 thousand units in 2015.

- In 2016, sales slightly decreased to 414.98 thousand units and continued to decline to 408.17 thousand units in 2017 and 398.82 thousand units in 2018.

- The market rebounded in 2019, reaching 417.34 thousand units, but experienced another slight dip to 414.35 thousand units in 2020, likely due to disruptions caused by the COVID-19 pandemic.

- In the following years, the market regained momentum. With sales volumes rising to 435.08 thousand units in 2021, 429.89 thousand units in 2022, and culminating at 456.91 thousand units in 2023.

- This steady recovery highlights the increasing demand for hearing aids. Driven by the aging population and advancements in hearing aid technology in Japan.

(Source: Statista)

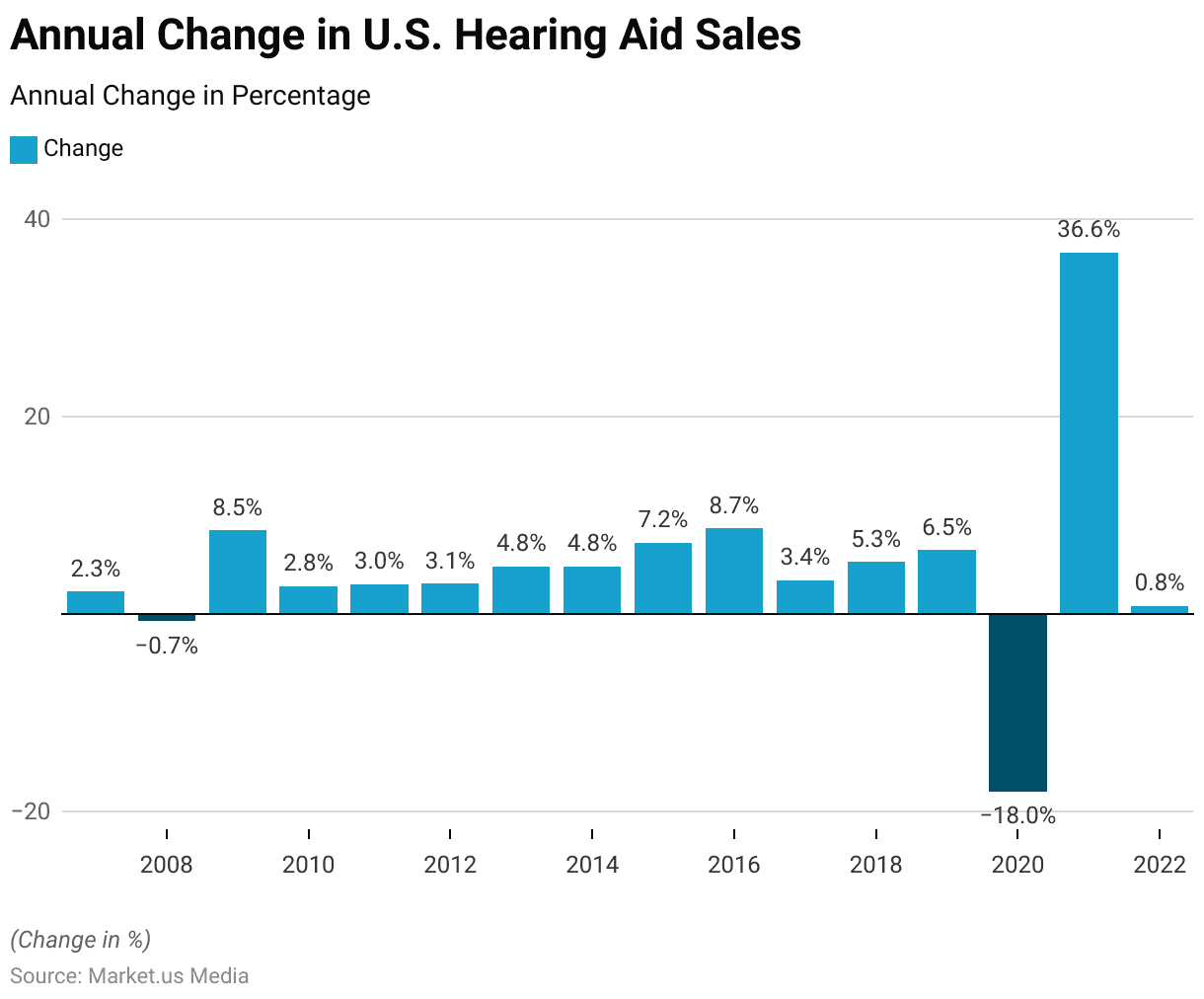

Annual Change in U.S. Hearing Aid Sales

- Between 2007 and 2022, the annual change in U.S. hearing aid sales demonstrated considerable variability, reflecting market fluctuations and external factors.

- In 2007, sales grew modestly by 2.3%, followed by a decline of 0.7% in 2008. Likely due to economic challenges.

- A rebound occurred in 2009, with an 8.5% increase, and sales continued to grow at 2.8% in 2010, 3% in 2011, and 3.1% in 2012.

- Growth accelerated in 2013 and 2014, with consistent increases of 4.8% each year.

- The upward trend continued in 2015 with a 7.2% rise, peaking in 2016 at 8.7%.

- However, growth slowed to 3.4% in 2017 and 5.3% in 2018, followed by a 6.5% increase in 2019.

- In 2020, sales saw a sharp decline of 18%, likely due to disruptions caused by the COVID-19 pandemic.

- This was followed by a strong recovery in 2021, with a significant surge of 36.6%.

- In 2022, growth stabilized at 0.8%, marking a return to more typical market conditions.

- This pattern illustrates the industry’s resilience and its responsiveness to economic, demographic, and external factors.

(Source: Statista)

Hearing Aid Import Statistics

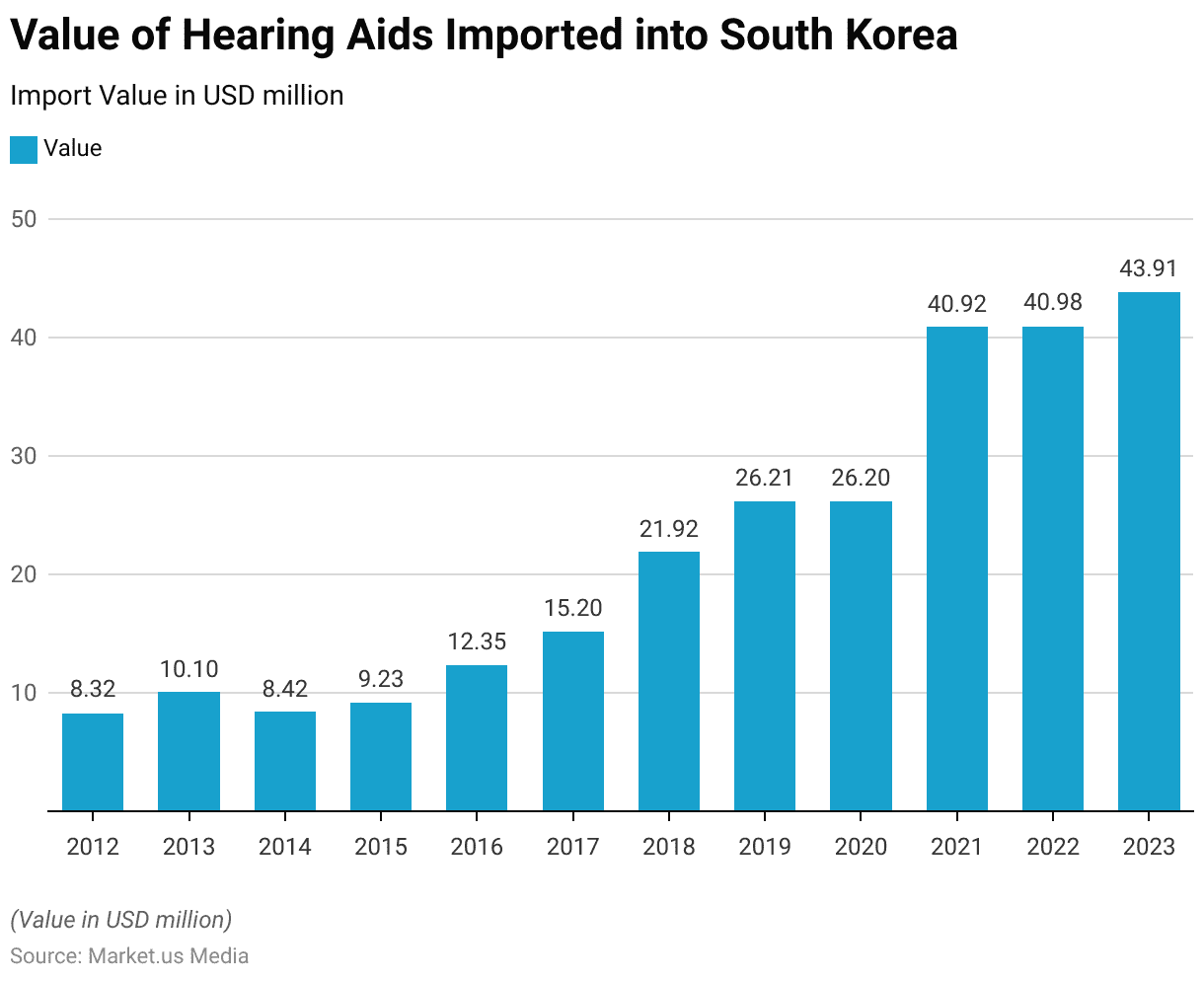

Value of Hearing Aids Imported into South Korea

- Between 2012 and 2023, the value of hearing aids imported into South Korea demonstrated significant growth, reflecting increasing demand and market expansion.

- In 2012, the import value stood at USD 8.32 million, rising to USD 10.1 million in 2013.

- A slight dip occurred in 2014, with imports valued at USD 8.42 million, followed by a modest recovery to USD 9.23 million in 2015.

- Import values began to climb steadily in subsequent years, reaching USD 12.35 million in 2016 and USD 15.2 million in 2017.

- This upward trend accelerated in 2018, with imports increasing to USD 21.92 million, and continued through 2019, when the value reached USD 26.21 million.

- Despite a slight stagnation in 2020, with imports holding steady at USD 26.2 million. The market experienced a significant surge in 2021, with values jumping to USD 40.92 million.

- This growth persisted in 2022, with imports valued at USD 40.98 million and further increased to USD 43.91 million in 2023.

- This dramatic rise in import values over the decade underscores the growing adoption of hearing aids in South Korea. Driven by technological advancements, an aging population, and increased awareness of auditory health.

(Source: Statista)

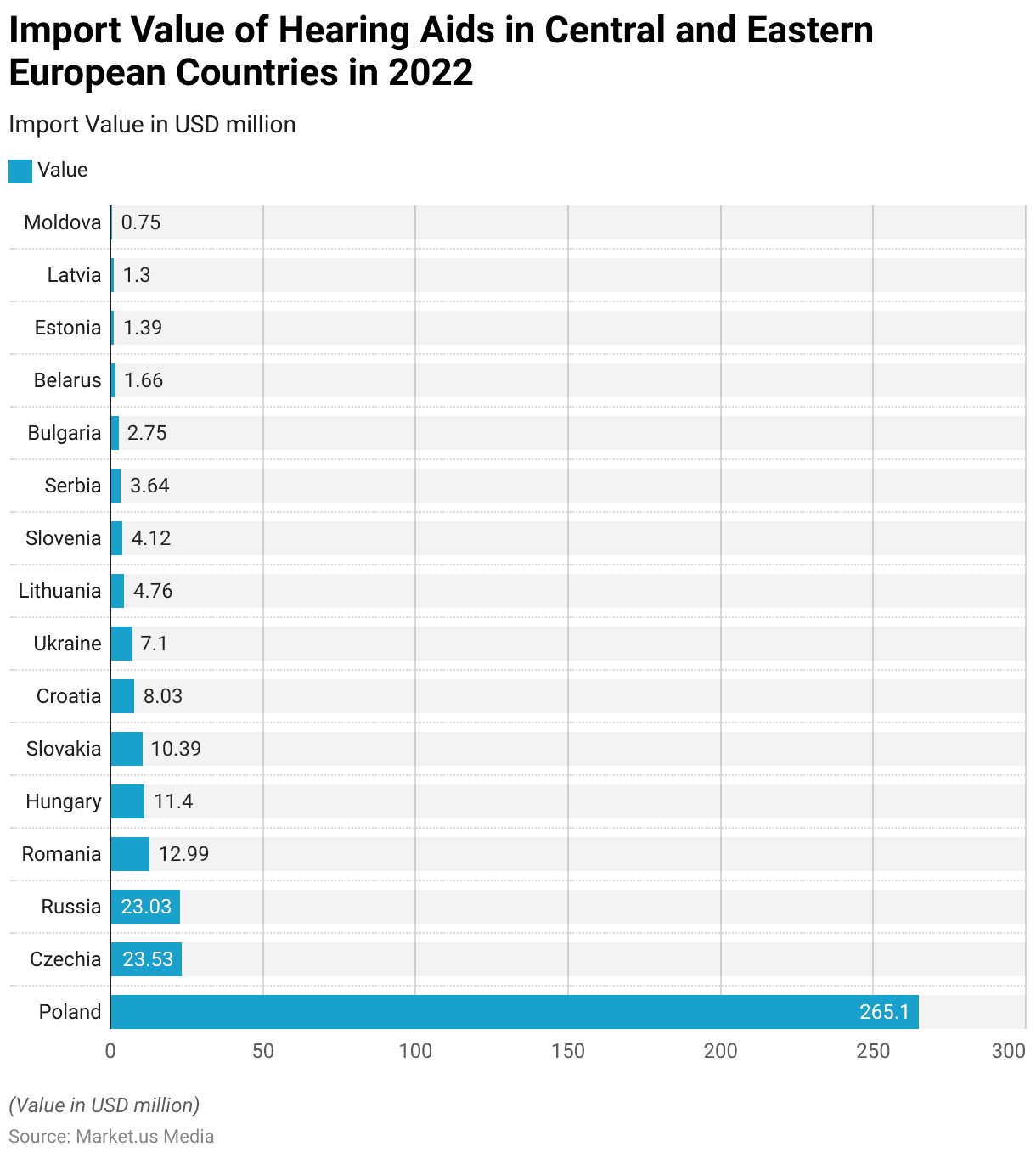

Import Value of Hearing Aids in Central and Eastern European Countries

- In 2022, the import value of hearing aids in Central and Eastern European countries revealed significant disparities between nations.

- Poland led the region with a substantial import value of USD 265.1 million. Far surpassing other countries.

- Czechia and Russia followed with imports valued at USD 23.53 million and USD 23.03 million, respectively.

- Romania recorded an import value of USD 12.99 million. Followed by Hungary at USD 11.4 million and Slovakia at USD 10.39 million.

- Croatia and Ukraine had smaller import values of USD 8.03 million and USD 7.1 million, respectively.

- The import values decreased further for smaller markets. Including Lithuania (USD 4.76 million), Slovenia (USD 4.12 million), and Serbia (USD 3.64 million).

- Bulgaria, Belarus, Estonia, Latvia, and Moldova reported significantly lower import values. Ranging from USD 2.75 million in Bulgaria to USD 0.75 million in Moldova.

- This data highlights Poland’s dominant position in the regional hearing aid market and the varying levels of market penetration across Central and Eastern European countries.

(Source: Statista)

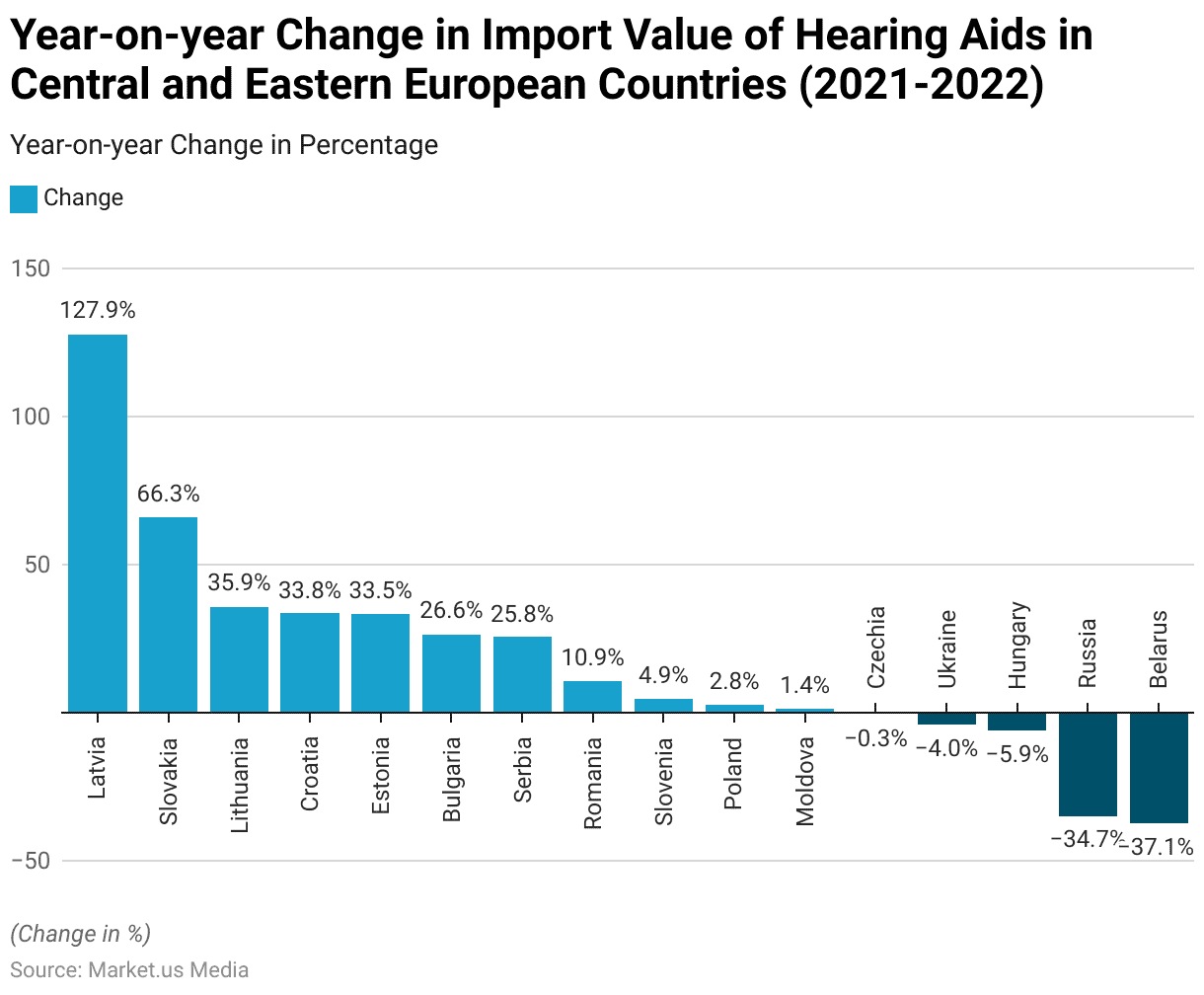

Year-on-year Change in Import Value of Hearing Aids in Central and Eastern European Countries

- Between 2021 and 2022, the year-on-year change in the import value of hearing aids in Central and Eastern European countries displayed a wide range of growth rates, with notable disparities among nations.

- Latvia experienced the most significant growth, with an impressive 127.9% increase in import value.

- Slovakia followed with a 66.3% rise, while Lithuania, Croatia, and Estonia saw notable increases of 35.9%, 33.8%, and 33.5%, respectively.

- Bulgaria and Serbia also reported substantial growth. With year-on-year increases of 26.6% and 25.8%, respectively.

- Romania recorded a more modest growth of 10.9%, and Slovenia and Poland posted smaller increases of 4.9% and 2.8%, respectively.

- Moldova saw a minimal growth of 1.4%.

- Conversely, some countries experienced declines. Czechia reported a slight decrease of 0.3%. While Ukraine and Hungary experienced more substantial declines of 4% and 5.9%, respectively.

- Russia and Belarus faced significant reductions. With year-on-year declines of 34.7% and 37.1%, respectively.

- These variations reflect differing market conditions, economic factors, and geopolitical influences across the region.

(Source: Statista)

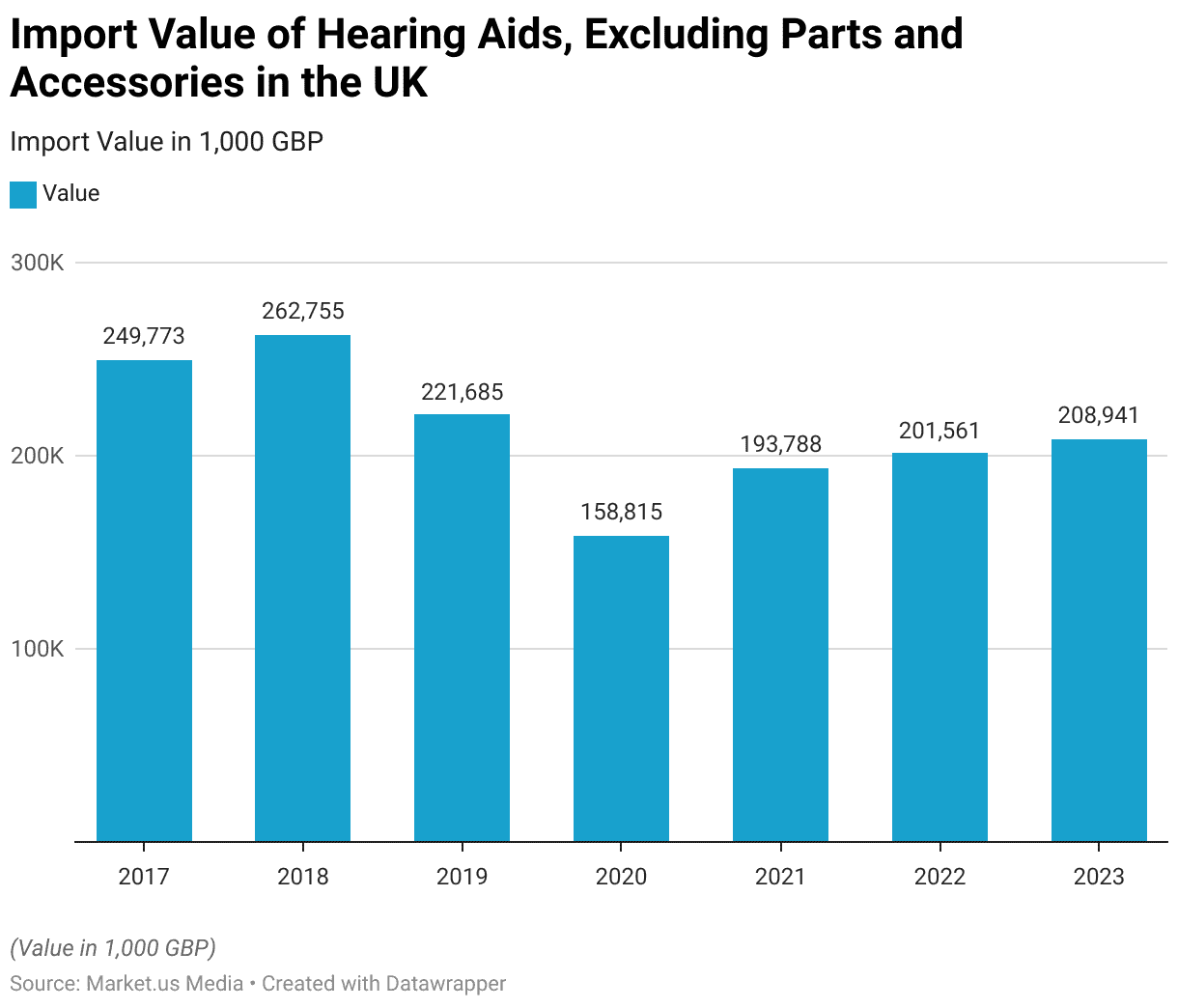

Import Value of Hearing Aids, Excluding Parts and Accessories in the United Kingdom (UK)

- Between 2017 and 2023, the import value of hearing aids (excluding parts and accessories) in the United Kingdom experienced fluctuations, reflecting varying market dynamics.

- In 2017, the import value stood at £249,773,000, rising to £262,755,000 in 2018. Marking the highest value in the observed period.

- However, in 2019, the import value decreased significantly to £221,685,000. The decline continued in 2020, with the import value dropping further to £158,815,000. Likely due to the impact of the COVID-19 pandemic.

- The market showed signs of recovery in 2021, with imports increasing to £193,788,000. Followed by further growth to £201,561,000 in 2022.

- By 2023, the import value had reached £208,941,000, indicating a gradual upward trend post-pandemic.

- These figures highlight the market’s resilience and recovery amid external challenges and shifting demand patterns for hearing aids in the UK.

(Source: Statista)

Hearing Aid Export Statistics

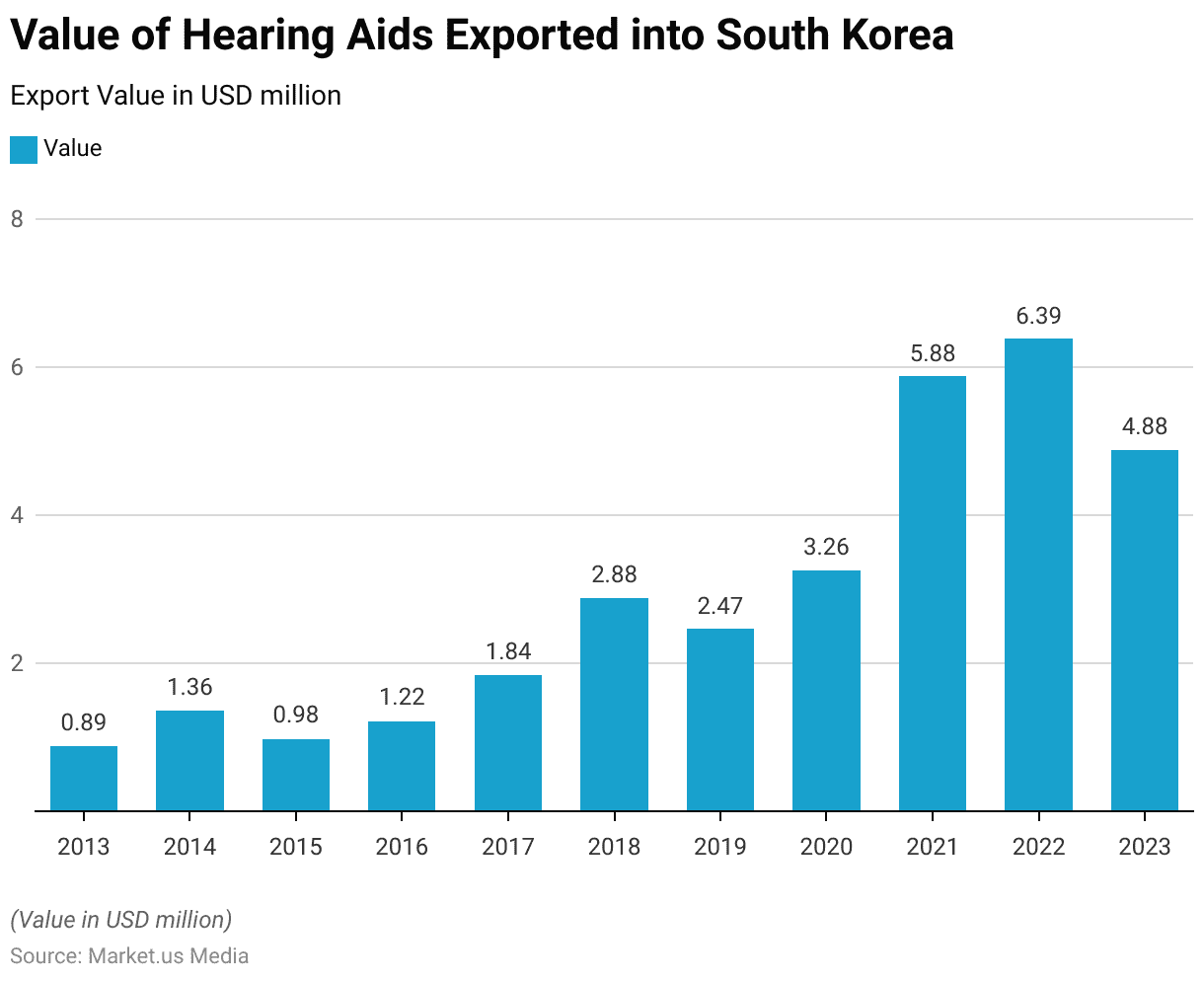

Value of Hearing Aids Exported into South Korea

- From 2013 to 2023, the export value of hearing aids from South Korea exhibited a notable upward trend, with fluctuations in recent years.

- In 2013, the export value was USD 0.89 million, which increased steadily to USD 1.36 million in 2014 and USD 1.22 million in 2016, after a slight decline in 2015 to USD 0.98 million.

- Growth accelerated in 2017 with an export value of USD 1.84 million. Followed by a significant jump to USD 2.88 million in 2018.

- However, in 2019, exports decreased slightly to USD 2.47 million before rebounding to USD 3.26 million in 2020.

- The export market experienced substantial growth in 2021. With exports reaching USD 5.88 million and peaking at USD 6.39 million in 2022.

- In 2023, the export value decreased to USD 4.88 million, indicating some contraction.

- This trajectory reflects South Korea’s growing presence in the global hearing aid market, supported by advancements in technology and manufacturing, despite recent market volatility.

(Source: Statista)

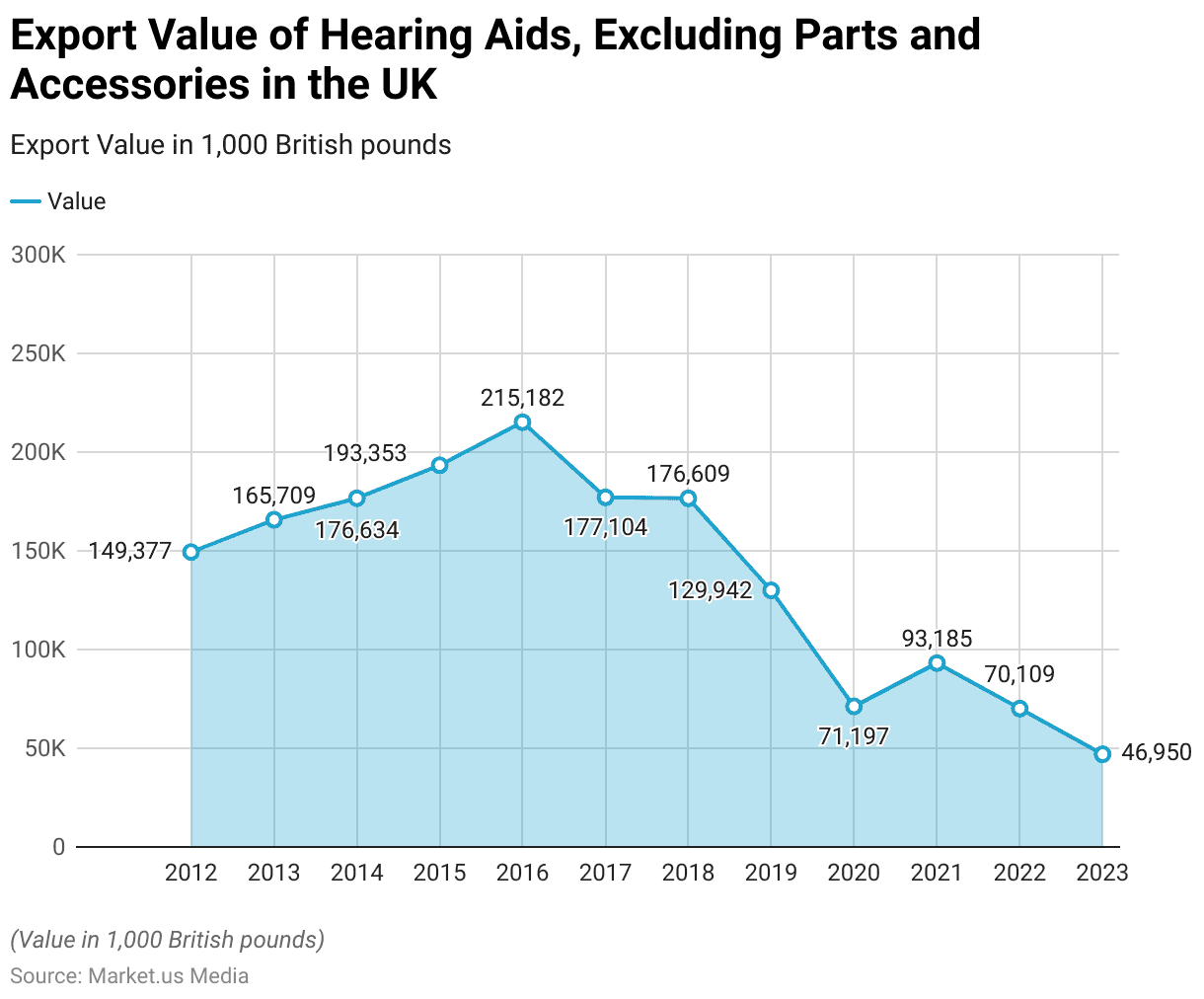

Export Value of Hearing Aids, Excluding Parts and Accessories in the United Kingdom (UK)

- Between 2012 and 2023, the export value of hearing aids (excluding parts and accessories) from the United Kingdom experienced significant fluctuations.

- In 2012, the export value was £149.38 million, which steadily increased over the next four years, reaching £215.18 million in 2016, the highest value recorded during this period.

- However, in 2017, exports declined to £177.10 million, followed by a slight drop to £176.61 million in 2018.

- By 2019, the export value fell significantly to £129.94 million.

- The decline continued into 2020, with exports dropping further to £71.20 million, likely reflecting disruptions caused by the COVID-19 pandemic.

- A modest recovery was seen in 2021, with export values increasing to £93.19 million.

- However, subsequent years saw a downward trend, with exports valued at £70.11 million in 2022 and £46.95 million in 2023.

- This data highlights both the peak of the UK’s hearing aid exports in the mid-2010s and the substantial challenges faced by the sector in more recent years.

(Source: Statista)

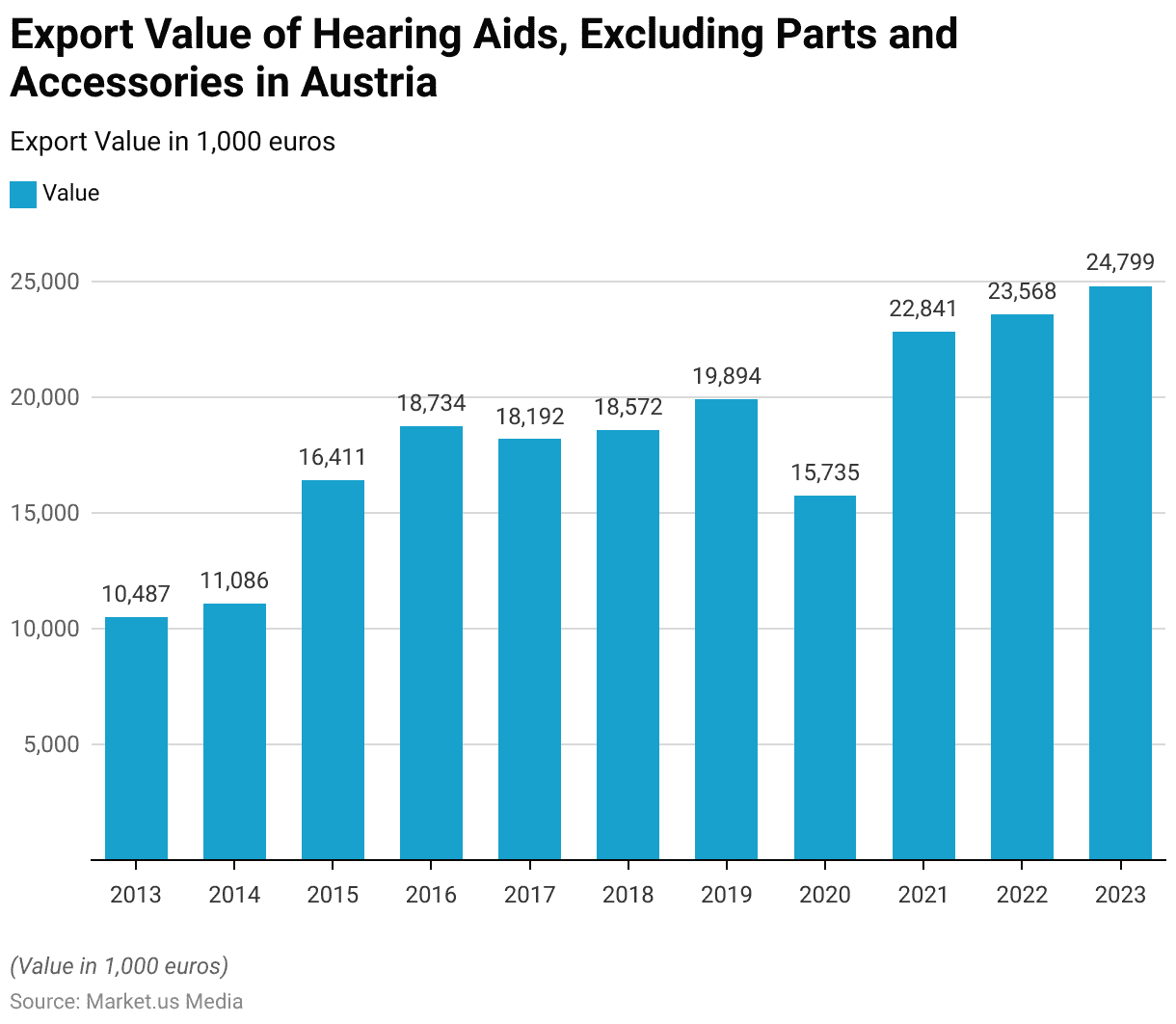

Export Value of Hearing Aids, Excluding Parts and Accessories in Austria

- From 2013 to 2023, the export value of hearing aids (excluding parts and accessories) from Austria demonstrated a steady upward trend, with occasional fluctuations.

- In 2013, the export value was €10.49 million, which increased modestly to €11.09 million in 2014.

- A significant rise occurred in 2015, with exports reaching €16.41 million, followed by further growth to €18.73 million in 2016.

- Although the export value slightly decreased to €18.19 million in 2017, it recovered to €18.57 million in 2018 and continued to grow, reaching €19.89 million in 2019.

- The market faced a temporary decline in 2020, with export values falling to €15.73 million, likely due to the global impact of the COVID-19 pandemic.

- However, strong growth resumed in 2021, with exports surging to €22.84 million, followed by further increases to €23.57 million in 2022 and €24.80 million in 2023.

- This consistent growth highlights Austria’s expanding role in the global hearing aid market, supported by advancements in production capabilities and rising international demand.

(Source: Statista)

Hearing Aids Exported to the World from Spain – By Country

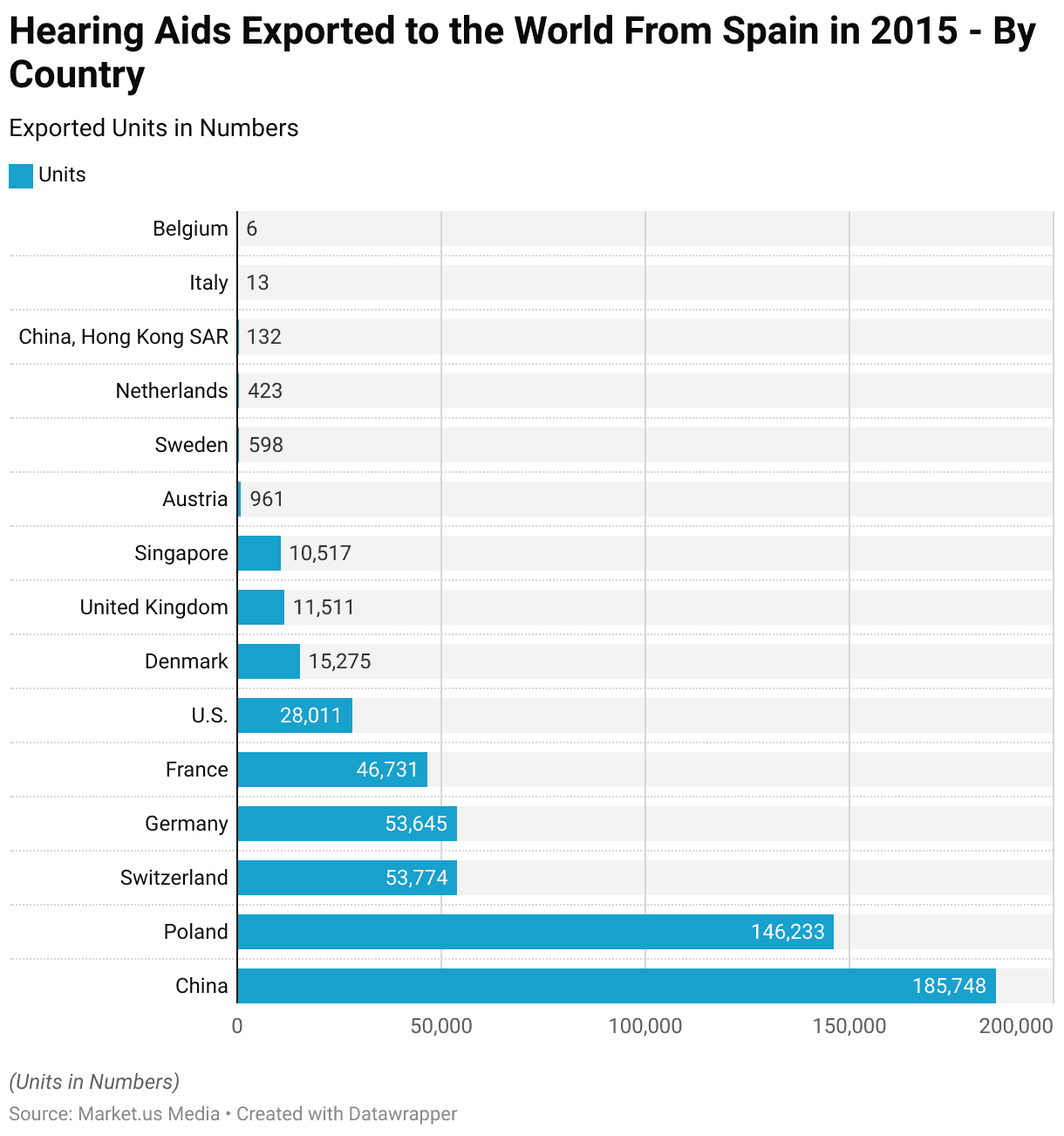

- In 2015, Spain exported hearing aids to various countries, with China being the largest destination, receiving 185,748 units.

- Poland followed as the second-largest importer, with 146,233 units.

- Switzerland and Germany each received similar quantities, with 53,774 units and 53,645 units, respectively.

- France imported 46,731 units, making it another significant destination.

- The United States accounted for 28,011 units, while Denmark imported 15,275 units.

- Other notable destinations included the United Kingdom, with 11,511 units, and Singapore, with 10,517 units.

- Smaller importers of Spanish hearing aids included Austria (961 units), Sweden (598 units), the Netherlands (423 units), and Hong Kong SAR (132 units).

- Minimal exports were recorded for Italy and Belgium, which received only 13 and 6 units, respectively.

- This distribution highlights the diverse global reach of Spain’s hearing aid exports, with significant trade relationships in both Europe and Asia.

(Source: Statista)

Demographic Insights of Hearing Aid Users

By Age

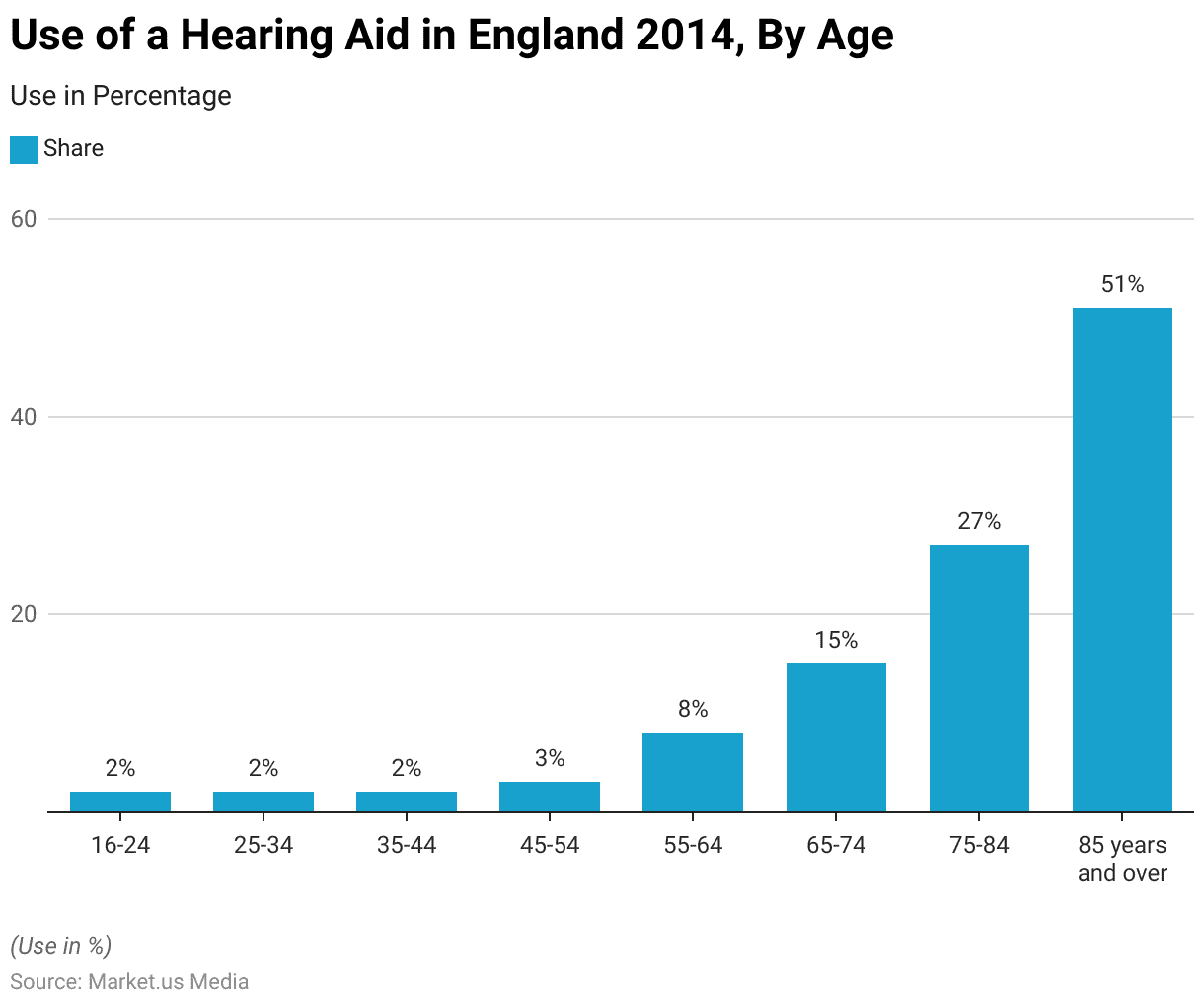

- In 2014, the prevalence of hearing aid use in England varied significantly by age group.

- Among younger age groups, the share of respondents who had ever used a hearing aid was minimal, with 2% reported for individuals aged 16-24, 25-34, and 35-44.

- This figure slightly increased to 3% among those aged 45-54.

- The prevalence grew notably in older age groups, with 8% of respondents aged 55-64 and 15% of those aged 65-74 having used a hearing aid.

- Among individuals aged 75-84, the prevalence rose to 27%, and it peaked at 51% for those aged 85 years and over.

- These figures reflect the increasing reliance on hearing aids as individuals age, correlating with the higher incidence of hearing loss in older populations.

(Source: Statista)

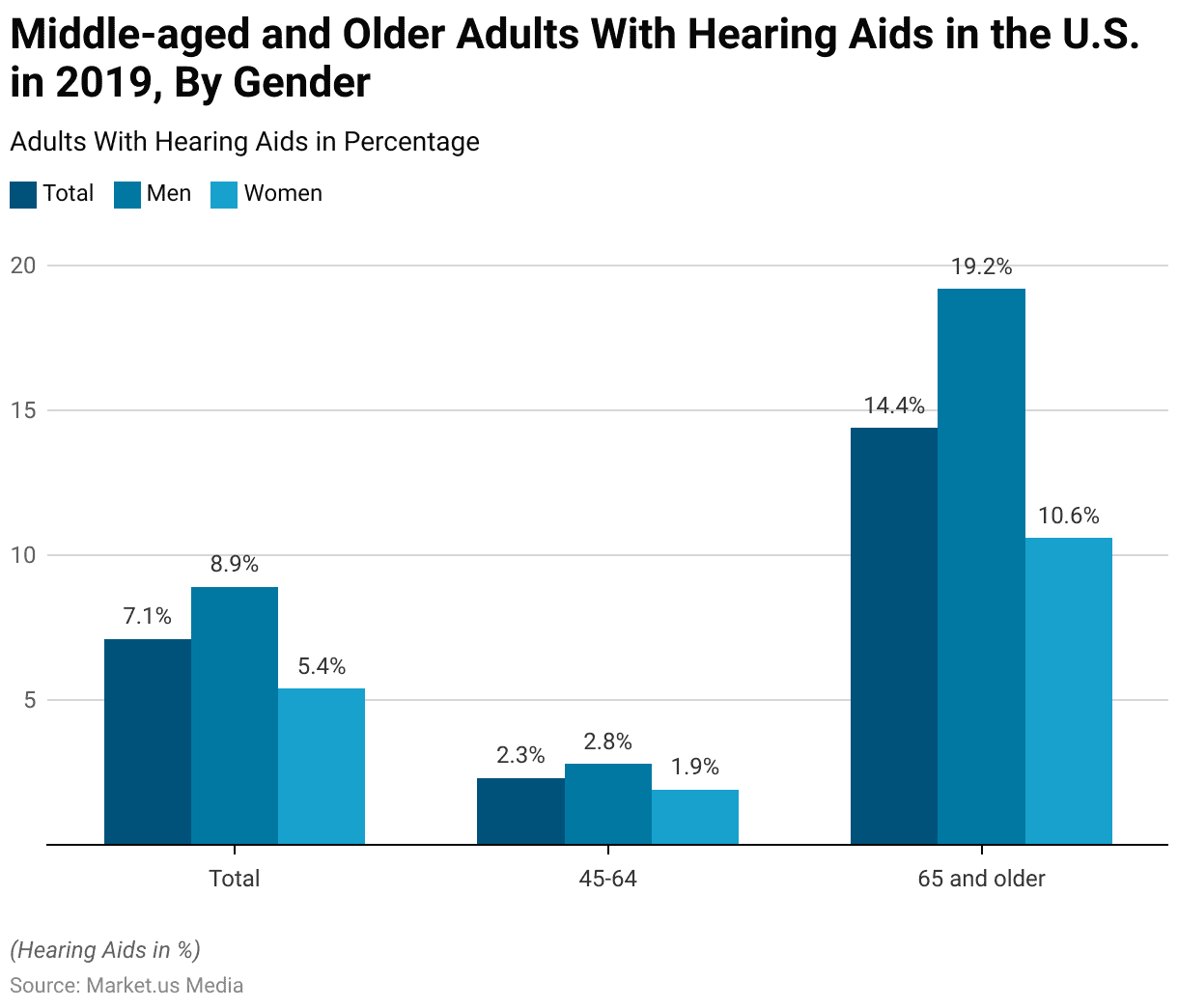

By Gender

- In 2019, 7.1% of adults aged 45 years and older in the United States reported using a hearing aid, with notable differences observed between genders and age groups.

- Among men, the overall usage rate was higher at 8.9%, compared to 5.4% for women.

- For individuals aged 45-64, 2.3% reported hearing aid use, with 2.8% of men and 1.9% of women within this age group utilizing the devices.

- Hearing aid usage increased significantly among those aged 65 and older, with 14.4% of respondents in this age category using hearing aids.

- Within this older group, 19.2% of men reported using hearing aids, compared to 10.6% of women.

- These figures highlight the higher prevalence of hearing aid usage among men and the increasing reliance on such devices with advancing age.

(Source: Statista)

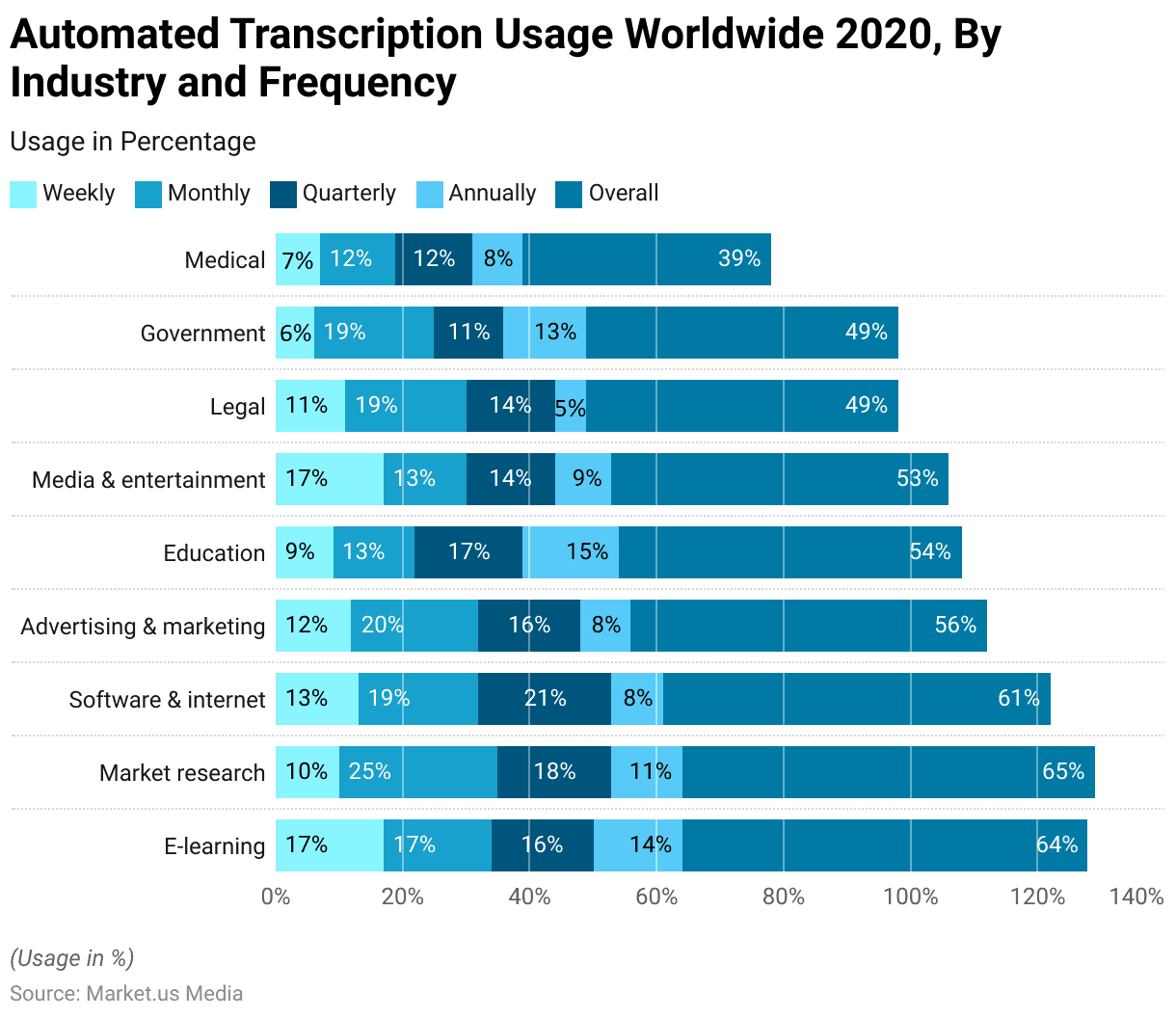

Automated Transcription Usage Worldwide

- In 2020, the usage of automated speech-to-text transcription varied across industries and by frequency of use.

- Among industries, market research had the highest overall adoption rate at 65%, with 25% using the technology monthly, 18% quarterly, 10% weekly, and 11% annually.

- The e-learning industry followed closely with an overall usage rate of 64%, distributed as 17% weekly, 17% monthly, 16% quarterly, and 14% annually.

- Software and internet industries showed a 61% overall adoption, with 13% using it weekly, 19% monthly, 21% quarterly, and 8% annually.

- Advertising and marketing demonstrated a 56% overall adoption rate, with 12% using the technology weekly, 20% monthly, 16% quarterly, and 8% annually.

- Education showed a 54% usage rate overall, with 9% weekly, 13% monthly, 17% quarterly, and 15% annually.

- Media and entertainment had a 53% adoption rate, with 17% using it weekly, 13% monthly, 14% quarterly, and 9% annually.

- In the legal and government sectors, the overall usage rate was 49%, though their usage patterns differed slightly.

- Legal usage was highest at 19% monthly, while the government sector also had 19% monthly use but with more significant annual use at 13%.

- The medical sector had the lowest overall adoption rate at 39%, with 7% using it weekly, 12% monthly, and 12% quarterly.

- These figures highlight the varied adoption of automated transcription based on the unique needs and workflows of different industries.

(Source: Statista)

Usage of Assistive Technology Statistics

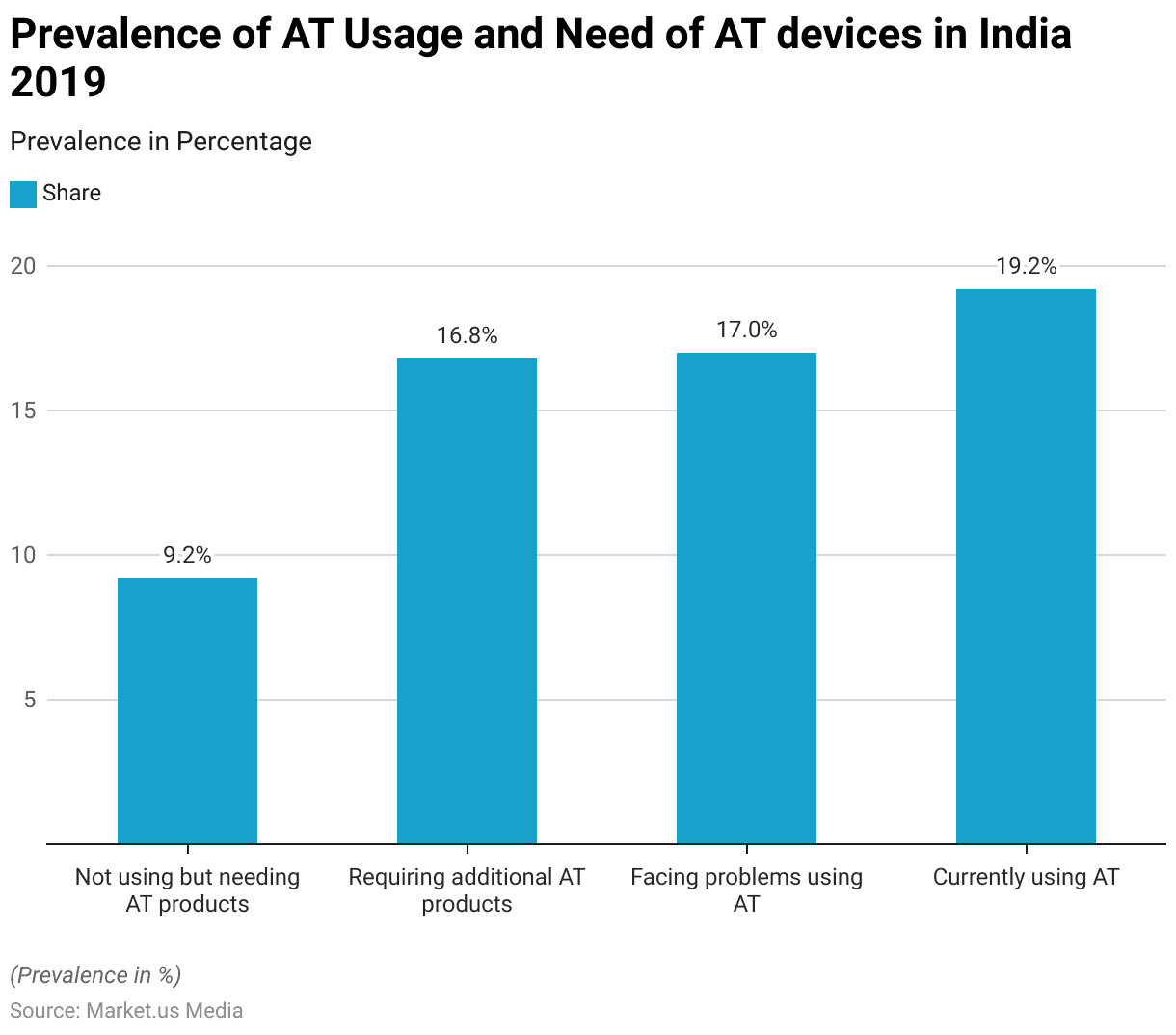

Assistive Technology Usage and Demand Statistics

- In 2019, the use and demand for assistive technology (AT) in India revealed significant gaps and challenges.

- Among the population, 19.2% were currently using AT products, reflecting the existing adoption levels.

- However, 9.2% of individuals were not using AT but expressed a need for such products, highlighting a gap in access.

- Additionally, 16.8% of AT users required additional assistive technology to meet their needs, indicating unmet demands within the user base.

- Furthermore, 17% of individuals faced problems using the AT products available to them, underscoring challenges in usability, compatibility, or accessibility.

- This data emphasizes the need for enhanced availability, functionality, and support for assistive technology in India.

(Source: Statista)

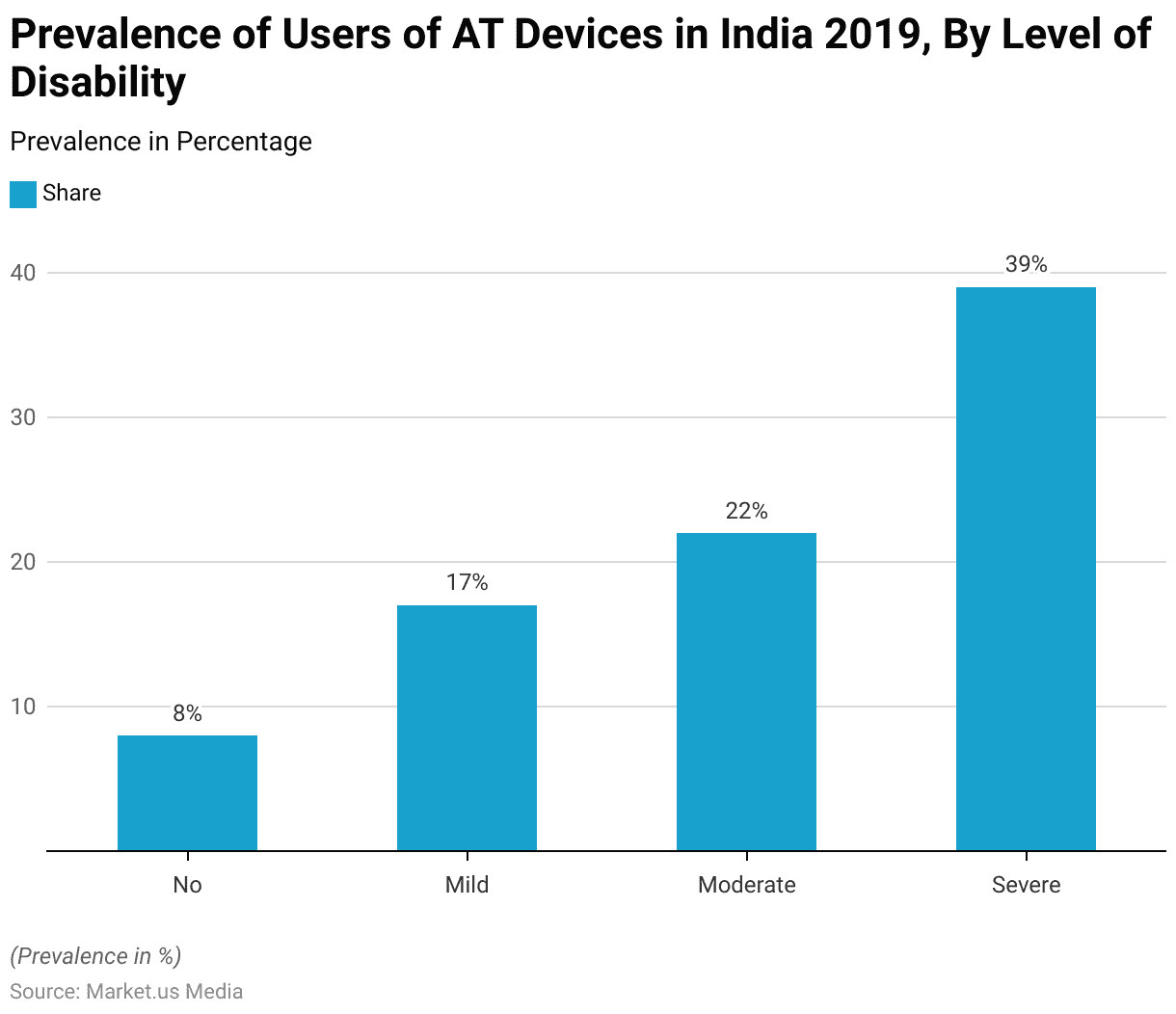

Usage of Assistive Technology – By Disability Level Statistics

- In 2019, the use of assistive technology (AT) among disabled individuals in India varied significantly depending on the severity of their disability.

- Among individuals with severe disabilities, 39% used AT products, reflecting the higher reliance on such tools in addressing significant functional challenges.

- For those with moderate disabilities, 22% utilized AT, while 17% of individuals with mild disabilities reported using assistive devices.

- Interestingly, even among those without disabilities, 8% used AT products, potentially indicating preventative or supplementary usage.

- This data highlights a positive correlation between the severity of disability and the adoption of assistive technology in India.

(Source: Statista)

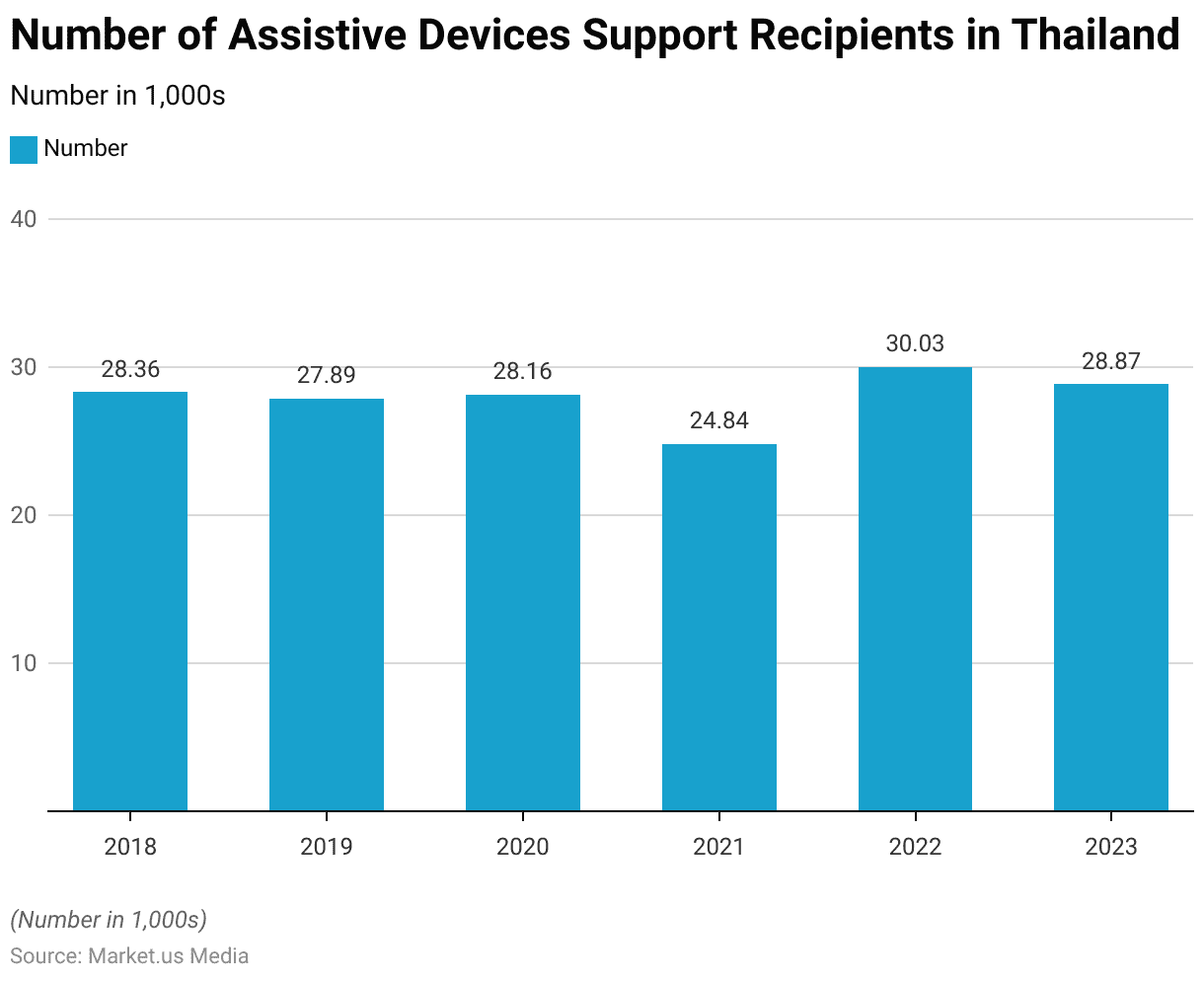

Assistive Devices Support Recipients

- From fiscal year 2018 to 2023, the number of people in Thailand who received assistive device support experienced fluctuations.

- In 2018, 28,360 individuals received support, which slightly decreased to 27,890 in 2019.

- The number rebounded slightly in 2020, reaching 28,160.

- However, a notable decline occurred in 2021, with 24,840 individuals receiving assistance, possibly due to disruptions caused by the COVID-19 pandemic.

- By 2022, the number surged to its highest during this period, with 30,030 individuals supported, followed by a slight decline to 28,870 in 2023.

- These trends reflect both the challenges and efforts in providing assistive devices to those in need in Thailand over this timeframe.

(Source: Statista)

Challenges Faced by Users

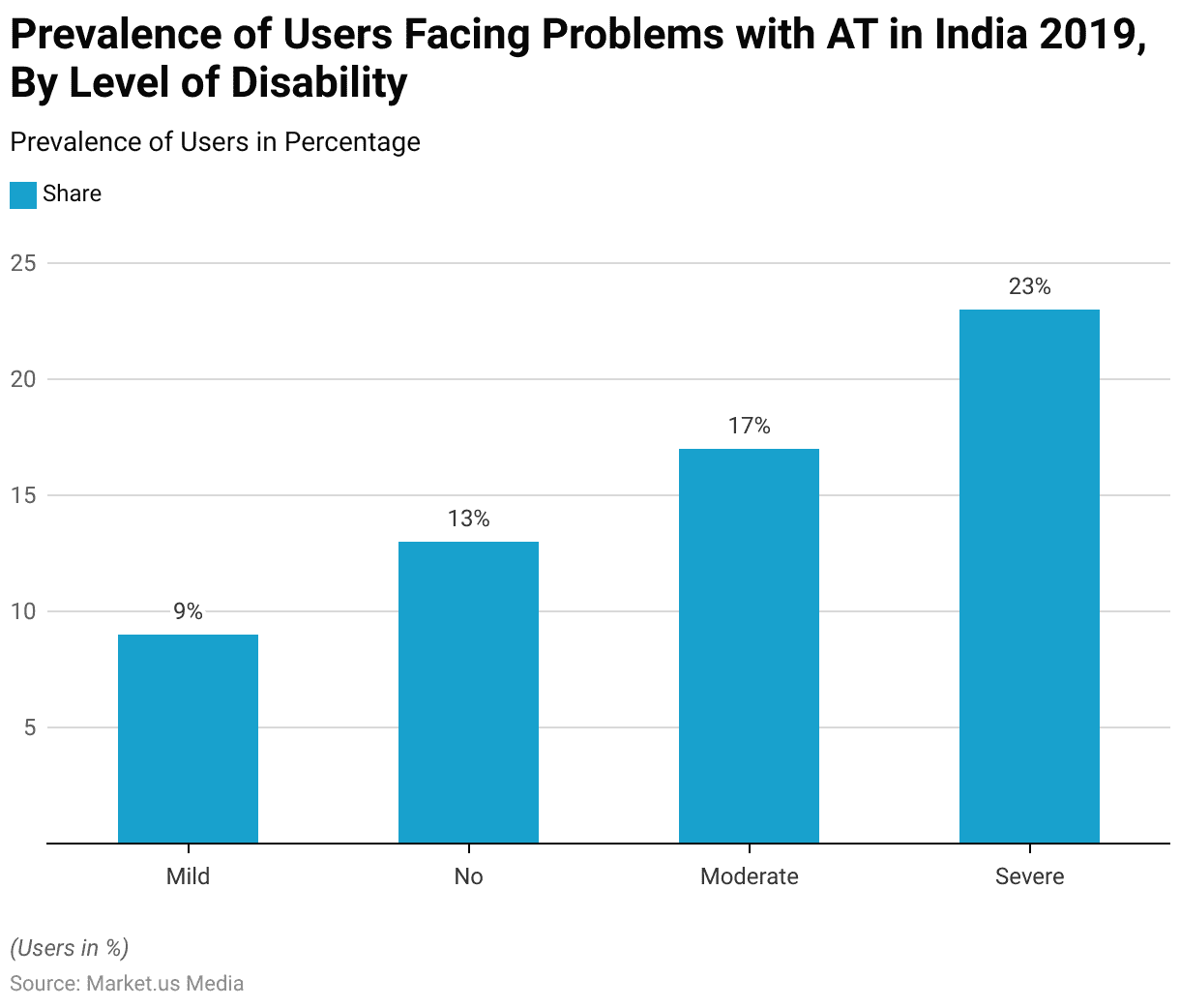

Users Facing Problems with Assisted Technology – By Level of Disability

- In 2019, the share of users in India facing problems while using assistive technology (AT) varied by level of disability.

- Among individuals with severe disabilities, 23% reported difficulties in using AT, the highest proportion across all categories.

- This was followed by 17% of users with moderate disabilities encountering issues.

- Interestingly, 13% of individuals with no disabilities who used AT also faced challenges, indicating potential usability or compatibility issues.

- Meanwhile, 9% of those with mild disabilities reported problems with their assistive technology.

- These findings highlight the need for improvements in the design, accessibility, and support systems for AT products to serve diverse user needs better.

(Source: Statista)

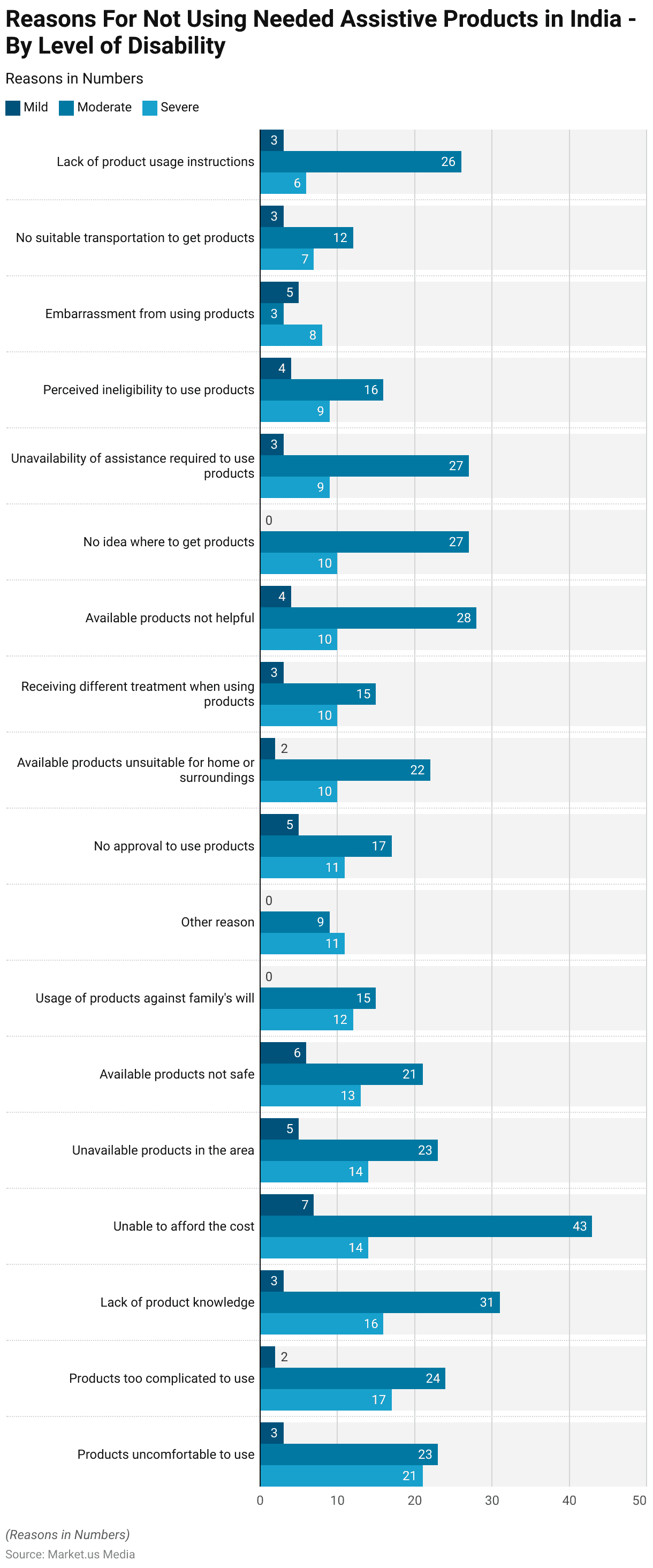

Reasons for Not Using Needed Assistive Products – By Level of Disability

- In 2019, a variety of reasons prevented users in India from utilizing needed assistive products, with challenges differing by the severity of disability.

- Among individuals with severe disabilities, the most cited issues included discomfort using products (21 respondents), products being too complicated to use (17), and a lack of product knowledge (16).

- Additionally, 14 respondents from this group reported being unable to afford the cost, having products unavailable in their area, and having products unsuitable for their surroundings.

- For individuals with moderate disabilities, affordability was the most significant barrier, reported by 43 respondents, followed by a lack of product knowledge (31), unavailable assistance to use products (27), and uncertainty about where to obtain products (27).

- Furthermore, 24 respondents highlighted complications in product use, and 23 found the products uncomfortable or unavailable in their area.

- Concerns such as unsuitability for home environments (22) and unsafe products (21) were also common.

- Among those with mild disabilities, affordability (7 respondents) and embarrassment (5) were significant barriers, while other issues, such as unsafe products, unavailable options, and a perceived lack of eligibility to use the products, were reported by 4-6 respondents.

- Across all disability levels, factors such as a lack of product instructions, family disapproval, unsuitable transportation, and societal stigma played a role, albeit to varying extents.

- These findings underscore the multifaceted challenges that must be addressed to improve access to and usability of assistive products in India.

(Source: Statista)

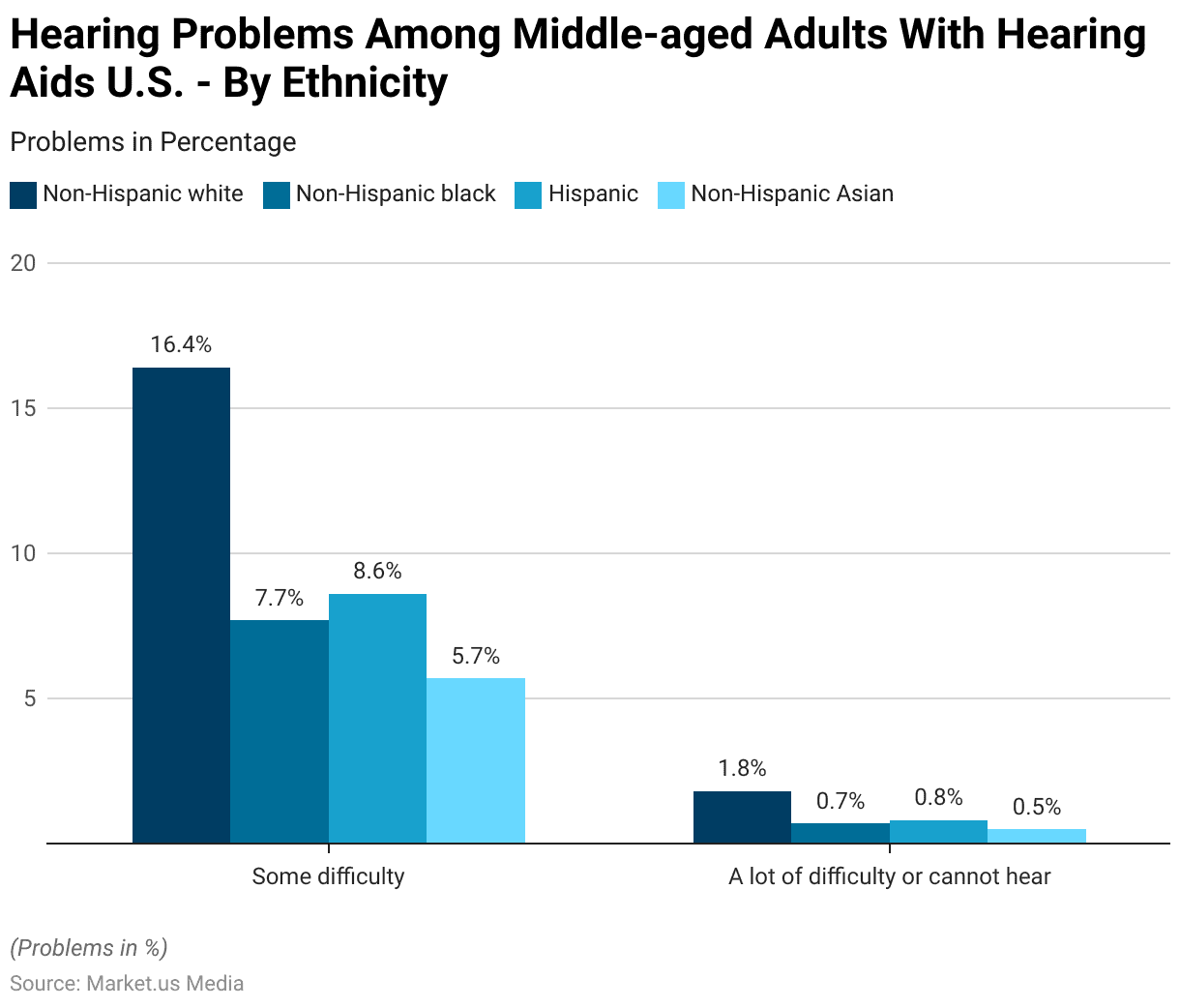

Hearing Problems Among Middle-Aged Adults with Hearing Aids

- In 2019, the percentage of U.S. adults aged 45 to 64 years who reported difficulty hearing, even when using a hearing aid, varied by ethnicity.

- Among non-Hispanic white adults, 16.4% reported some difficulty, and 1.8% experienced a lot of difficulty or were unable to hear.

- For non-Hispanic Black adults, these figures were lower, with 7.7% reporting some difficulty and 0.7% experiencing significant difficulty or inability to hear.

- Hispanic adults had similar rates, with 8.6% reporting some difficulty and 0.8% reporting a lot of difficulty or inability to hear.

- Among non-Hispanic Asian adults, 5.7% reported some difficulty, and 0.5% reported significant difficulty or inability to hear.

- These findings highlight disparities in hearing-related challenges across ethnic groups in the U.S.

(Source: Statista)

Key Spending and Investments

Top Funded Digital Health Categories Worldwide

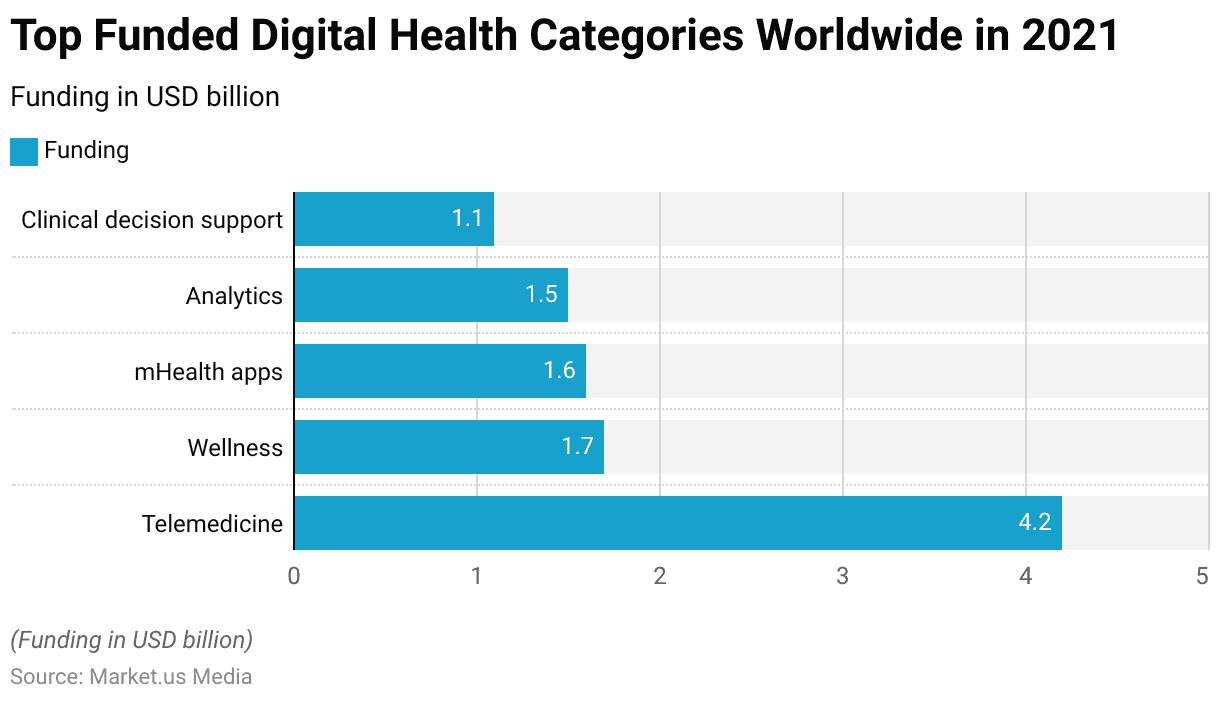

- In the first half of 2021, telemedicine emerged as the most heavily funded digital health category globally, attracting USD 4.2 billion in investment.

- Wellness technologies followed with USD 1.7 billion in funding, reflecting a growing interest in preventive and holistic health solutions.

- Mobile health (mHealth) apps received USD 1.6 billion in funding, emphasizing their increasing role in healthcare accessibility and management.

- Analytics solutions secured USD 1.5 billion, highlighting the importance of data-driven insights in healthcare decision-making.

- Additionally, clinical decision support systems garnered USD 1.1 billion in funding, underscoring their critical role in enhancing diagnostic accuracy and treatment planning.

- This distribution of funding demonstrates the priorities and growth areas within the digital health sector in 2021.

(Source: Statista)

Assistive Tech Venture Investment

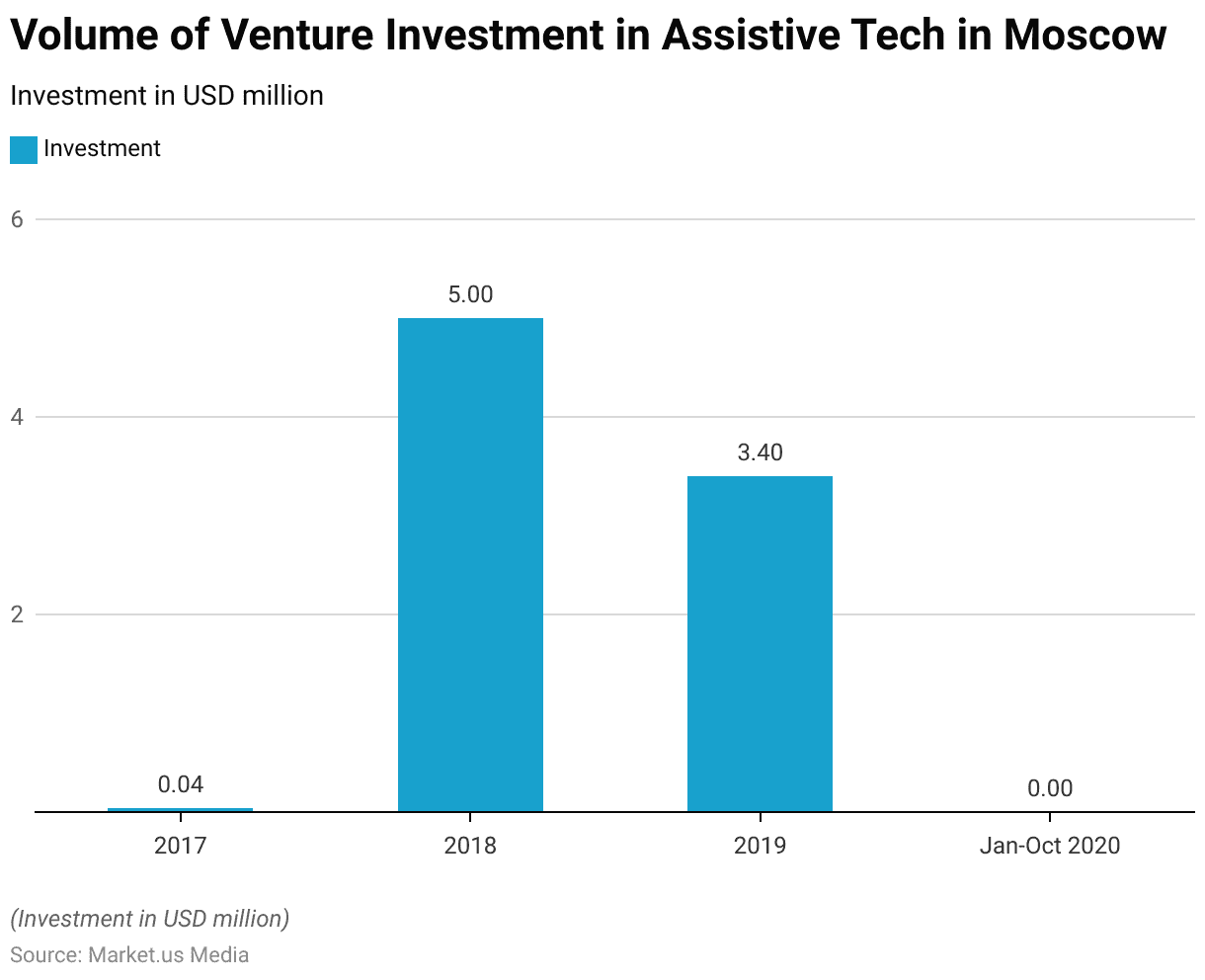

- From 2017 to October 2020, the volume of venture investment in assistive technology in Moscow exhibited notable fluctuations.

- In 2017, investments were minimal, amounting to just USD 0.04 million.

- A significant surge occurred in 2018, with investment volume rising to USD 5 million, highlighting increased interest and funding in the sector.

- However, this momentum slowed in 2019, with investments declining to USD 3.4 million.

- From January to October 2020, no venture investments were recorded in the assistive technology sector, reflecting a potential market pause, possibly due to economic disruptions or shifting investment priorities during the COVID-19 pandemic.

(Source: Statista)

Innovations and Developments in Assistive Technology Statistics

- In 2023, the landscape of assistive technology showcased remarkable innovations aimed at enhancing the quality of life for individuals with disabilities.

- At notable platforms such as the Consumer Electronics Show (CES), a plethora of advanced products were introduced, targeting enhanced independence for the disabled community.

- Noteworthy developments included eSight Go smart glasses, which facilitate vision through real-time image enhancement, and Sony’s Project Leonardo, a customizable gaming controller designed for gamers with limited motor skills.

- Additionally, L’Oreal’s HAPTA, a motorized makeup applicator, and Samsung’s Relumino Mode for visual enhancement on TVs reflect the trend toward integrating assistive technology into consumer goods.

- The convergence of assistive technologies with mainstream consumer electronics is evident in the growth of these innovations, as seen in a WIPO report, which highlighted significant advancements in areas such as autonomous wheelchairs, advanced prosthetics, and sensory wearables.

- This integration not only broadens the user base but also facilitates wider accessibility in daily technology use.

- The evolution of these technologies underscores a pivotal shift towards a more inclusive technology landscape, promising greater independence and societal participation for people with disabilities.

(Source: Accessibility.Com, World Intellectual Property Organization)

Regulations for Assistive Technology

- Regulatory frameworks for assistive technology (AT) are crucial in ensuring that individuals with disabilities can access the necessary tools to enhance their participation and inclusion in society.

- Globally, initiatives such as the World Health Assembly’s resolution WHA71.8 advocate for the development and implementation of policies to improve AT access, aligning with goals for universal health coverage and the rights of persons with disabilities as outlined in the UN Convention.

- In the United States, legislation like the Americans with Disabilities Act and the Individuals with Disabilities Education Act specifically includes provisions for assistive technology to support educational and public access needs.

- Despite these efforts, significant disparities in access remain, particularly in low- and middle-income countries. For instance, the WHO and UNICEF report that while over 2.5 billion people globally require AT, nearly one billion are denied access, with availability in some countries as low as 3%.

- This gap underscores the need for enhanced global cooperation and investment in AT to not only support individuals’ rights but also contribute to broader societal and economic benefits.

- Efforts to expand access are ongoing, with international guidance aiming to assist countries in establishing comprehensive AT policies that are integrated within broader health and social systems.

(Sources: Ecta Center, Unicef, World Health Organization (Who))

Recent Developments

Acquisitions and Mergers:

- Control Bionics’ Partnership with Double R&D: In April 2022, Control Bionics partnered with Double R&D to introduce NeuroNode technology in Japan. This collaboration aims to expand Control Bionics’ reach, providing assistive solutions for conditions like ALS, cerebral palsy, and stroke.

Product Launches:

- Apple’s AirPods Pro 2 as Hearing Aids: In September 2024, Apple announced that AirPods Pro 2 could function as clinical-grade hearing aids, targeting users with mild to moderate hearing loss. This innovation addresses a $13 billion market opportunity and aims to increase awareness of hearing health.

Funding:

- Prepared’s Series B Funding: In October 2024, Prepared, a provider of assistive 911 technology, raised $27 million in Series B funding. The investment will support the expansion of its AI-powered platform, Prepared Assist, enhancing emergency response efficiency.

Conclusion

Assistive Technology Statistics – Assistive technology (AT) is vital for improving the quality of life for individuals with disabilities and functional limitations, driven by an aging population and advancements in technology.

Despite its benefits, barriers such as affordability, accessibility, usability, and stigma hinder widespread adoption.

Addressing these challenges requires collaborative efforts to enhance product availability, financial support, and user education.

Tailored strategies and investments in innovation can bridge accessibility gaps, empower individuals, and promote inclusive societies globally.

FAQs

Assistive technology refers to devices, equipment, or systems that help individuals with disabilities or functional limitations perform tasks more effectively, improving their independence and quality of life.

AT benefits individuals with physical, sensory, cognitive, or developmental disabilities, as well as older adults and those recovering from injuries or illnesses.

Examples include hearing aids, screen readers, mobility aids (wheelchairs, walkers), prosthetics, communication devices, and adaptive tools for daily living.

Costs vary widely depending on the device or solution. Some are affordable, while others, like high-tech prosthetics or advanced communication devices, can be costly. Financial aid and insurance coverage may be available.

Common challenges include high costs, lack of awareness, limited accessibility in some regions, and stigma associated with its use.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)