Table of Contents

Overview

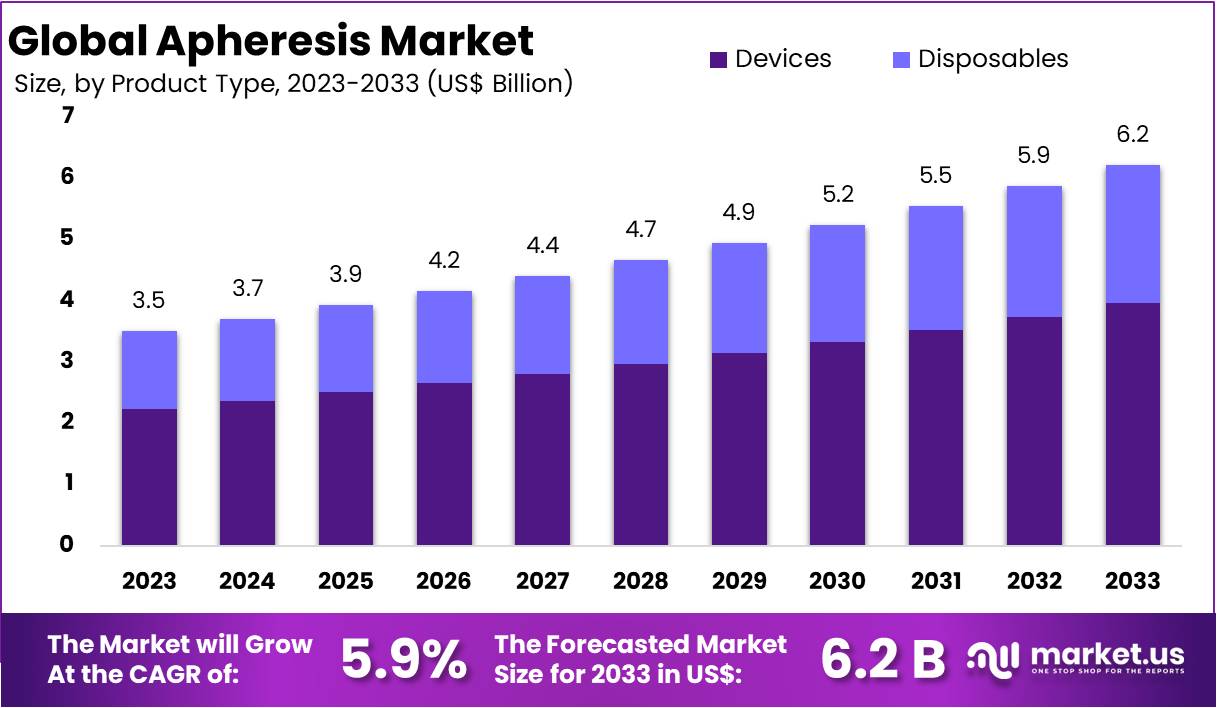

New York, NY – Feb 12, 2026 –The Global Apheresis Market size is expected to be worth around US$ 6.2 Billion by 2033, from US$ 3.5 Billion in 2023, growing at a CAGR of 5.9% during the forecast period from 2024 to 2033. North America maintained a dominant position in the apheresis market, accounting for over 36.3% of the market share and a market value of US$ 1.3 billion.

Apheresis is a medical procedure in which specific blood components are separated and collected, while the remaining components are returned to the patient or donor. The process is widely used for both therapeutic and donation purposes. In therapeutic applications, apheresis is performed to remove abnormal or excess blood components associated with various medical conditions. In donation settings, it enables the collection of targeted components such as platelets, plasma, or red blood cells, improving efficiency compared to whole blood donation.

The procedure is conducted using automated apheresis machines that separate blood through centrifugation or membrane filtration techniques. Blood is drawn through a sterile, single-use kit, processed within the device, and the desired component is isolated. The remaining blood components are safely reinfused into the individual. The entire process is typically completed within one to two hours, depending on the component being collected.

Apheresis has become an essential component of modern transfusion medicine and specialty care. It supports the management of conditions such as autoimmune disorders, hematologic diseases, and certain neurological conditions. Additionally, the increasing demand for plasma-derived therapies and platelet transfusions has strengthened the adoption of advanced apheresis technologies across healthcare facilities.

Continuous technological advancements and growing clinical applications are contributing to the steady expansion of the global apheresis market, supported by rising awareness, improved healthcare infrastructure, and increasing prevalence of chronic diseases worldwide.

Key Takeaways

- Market Expansion: The global apheresis market is anticipated to attain a valuation of US$ 6.2 billion by 2033, progressing at a compound annual growth rate (CAGR) of 5.9% during the forecast period from 2024 to 2033.

- Regional Leadership: North America accounted for more than 36.3% of the global revenue share in 2023, with a market value of approximately US$ 1.3 billion, positioning the region as the leading contributor worldwide.

- Devices Segment Performance: The devices category represented the largest share of 63.7% in 2023, reflecting its critical role in blood component separation and therapeutic apheresis procedures.

- Plasmapheresis Utilization: Plasmapheresis emerged as the leading procedure type, capturing 42.9% of the total market share in 2023, driven by its extensive application in the management of autoimmune and chronic disorders, including myasthenia gravis.

- Technology Preference: Centrifugation technology maintained market dominance with a 66.2% share in 2023, attributed to its established efficiency in separating blood components based on density.

- Application in Hematological Disorders: The use of apheresis in the treatment of hematological conditions, such as leukemia and lymphoma, accounted for 35.9% of the market share in 2023, underscoring its significance in patient care and disease management.

Regional Analysis

In 2023, North America maintained a leading position in the global apheresis market, accounting for over 36.3% of total revenue and reaching a market value of US$ 1.3 billion. This leadership is supported by a well-established healthcare infrastructure, characterized by advanced hospitals, specialized treatment centers, and prominent research institutions that facilitate the widespread adoption of apheresis procedures in clinical practice.

The rising prevalence of chronic conditions, including cancer and autoimmune disorders, has significantly increased the demand for therapeutic apheresis across the region. These diseases often require specialized blood component management, strengthening the integration of apheresis into standard treatment protocols.

Market expansion is further supported by favorable regulatory frameworks and strong funding initiatives from public health authorities. Continuous technological advancements by major medical device manufacturers have enhanced procedural efficiency and safety. In addition, structured training programs, broad insurance coverage, and high per capita healthcare expenditure collectively ensure accessibility and sustained growth of the apheresis market in North America.

Emerging Trends in Apheresis and Blood Component Collection

Stabilized Blood Collections with Rising Apheresis Contribution

- In 2023, approximately 11.6 million units of whole blood and apheresis-derived red blood cells were collected in the United States, reflecting a marginal 1.7% decline compared to 2021 levels. Despite this slight contraction in total collections, platelet procurement through apheresis demonstrated measurable expansion. Around 1.26 million platelet units were collected via apheresis, representing a 3.6% increase. Notably, pathogen-reduced platelet treatments expanded significantly, recording a 49.2% increase, underscoring a strategic shift toward enhanced transfusion safety.

Increasing Adoption of Pathogen-Reduced Platelets

- Pathogen-reduced platelet units reached approximately 1.26 million in 2023, marking a 49% increase from 2021. This growth reflects heightened emphasis on transfusion-related infection control and regulatory compliance. The trend indicates sustained investment in blood safety technologies and standardization of pathogen inactivation protocols across collection centers.

Expansion of Apheresis-Derived RBC Collections

- Between 2019 and 2021, red blood cell collections obtained via apheresis increased from 1.8 million to 1.93 million units, representing a 7.3% rise. This expansion highlights a growing preference for component-specific donation strategies, enabling optimized inventory management and improved clinical matching.

Adoption of Advanced Apheresis Technologies

- Innovative systems such as Spectra Optia are being increasingly deployed to enhance separation efficiency and procedural precision. In parallel, immunoadsorption methods utilizing protein A column technologies are gaining traction, particularly in targeted therapeutic applications. These advancements contribute to improved operational efficiency, reduced procedure time, and enhanced patient safety outcomes.

Pediatric-Focused Safety Enhancements

- Specialized equipment configurations and clinical protocols have been standardized in pediatric apheresis settings to mitigate procedural risks. Key risk management areas include blood volume loss, hypocalcemia, and catheter-related infections. Enhanced monitoring frameworks and customized flow settings have improved safety margins for smaller and hemodynamically sensitive patient populations.

Key Clinical Use Cases of Apheresis

- Plateletpheresis (Donor Collection): Plateletpheresis enables the collection of six to ten times more platelets compared to pooled whole blood-derived donations. Quality benchmarks typically require a minimum yield of ≥3×10¹¹ platelets per collection, with a pH level maintained at ≥6.2 to ensure product viability and storage stability. This method supports high-efficiency inventory management and reduces donor exposure risk for recipients.

- Therapeutic Plasma Exchange (Plasmapheresis)

- Therapeutic plasma exchange is widely utilized in the management of autoimmune and immune-mediated disorders, including:

- Guillain-Barré syndrome

- Goodpasture’s syndrome

- Myasthenia gravis

- Thrombotic thrombocytopenic purpura

- Its application has also been explored in severe COVID-19 cases, where preliminary evidence suggests limited but potentially beneficial clinical outcomes.

- Leukapheresis: Leukapheresis is implemented to reduce elevated white blood cell counts in conditions such as leukemia and leukostasis. Additionally, it facilitates granulocyte collection (approximately 1×10¹⁰ cells per procedure) for transfusion in patients with refractory infections, particularly in immunocompromised populations.

- Stem Cell Harvesting (Peripheral Blood Stem Cell Collection): Peripheral blood stem cell (PBSC) collection is conducted following hematopoietic stem cell mobilization using agents such as G-CSF. The harvested stem cells are subsequently used for autologous or allogeneic transplantation. Clinical research, including NCT00562601, has examined combined plasma and white blood cell collection methodologies to enhance therapeutic efficiency.

- LDL and Lipoprotein(a) Apheresis: LDL and lipoprotein(a) apheresis is indicated for patients with severe lipid abnormalities, particularly Familial hypercholesterolemia. The procedure effectively reduces LDL-cholesterol and Lp(a) concentrations and is classified as a Class I indication by leading apheresis societies. Expanded reimbursement discussions supported by CMS public commentary further reinforce its clinical and economic significance.

Frequently Asked Questions on Apheresis

- How does the apheresis procedure work?

The procedure is performed using an automated device that separates blood components through centrifugation or membrane filtration. Blood is withdrawn through a sterile kit, processed within the system, and targeted components are isolated before reinfusion. - What medical conditions require therapeutic apheresis?

Therapeutic apheresis is commonly used in the management of autoimmune disorders, neurological diseases, hematological conditions, and certain metabolic disorders. It supports the removal of harmful antibodies, excess cells, or abnormal proteins from circulation. - Is apheresis safe?

Apheresis is generally considered safe when conducted by trained healthcare professionals. Modern devices incorporate advanced safety features, and single-use disposable kits reduce infection risks, ensuring patient safety and procedural efficiency. - Which region dominates the apheresis market?

North America holds a leading share of the global market due to advanced healthcare infrastructure, high disease prevalence, favorable reimbursement policies, and strong presence of major medical device manufacturers supporting continuous innovation. - Which segment holds the largest market share?

The devices segment accounts for the largest revenue share, as automated apheresis systems are essential for therapeutic and donor-based procedures. Continuous innovation in device efficiency and safety further strengthens segment dominance. - What is the future outlook for the apheresis market?

The market is projected to witness steady expansion over the coming decade, supported by increasing clinical applications, growing awareness regarding plasma donation, technological improvements, and rising healthcare expenditure globally.

Conclusion

The global apheresis market is positioned for sustained growth, supported by expanding clinical applications, technological advancements, and rising demand for component-specific blood collection. Increasing prevalence of chronic, autoimmune, and hematological disorders continues to drive therapeutic adoption, while growth in plasma-derived therapies strengthens donation-based utilization.

Dominance of advanced centrifugation technologies and device-driven procedures underscores the importance of innovation in operational efficiency and patient safety. North America remains the leading regional contributor due to strong healthcare infrastructure and reimbursement support. Overall, stable blood collections combined with rising apheresis utilization indicate a resilient and progressively evolving market landscape through 2033.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)