Table of Contents

Overview

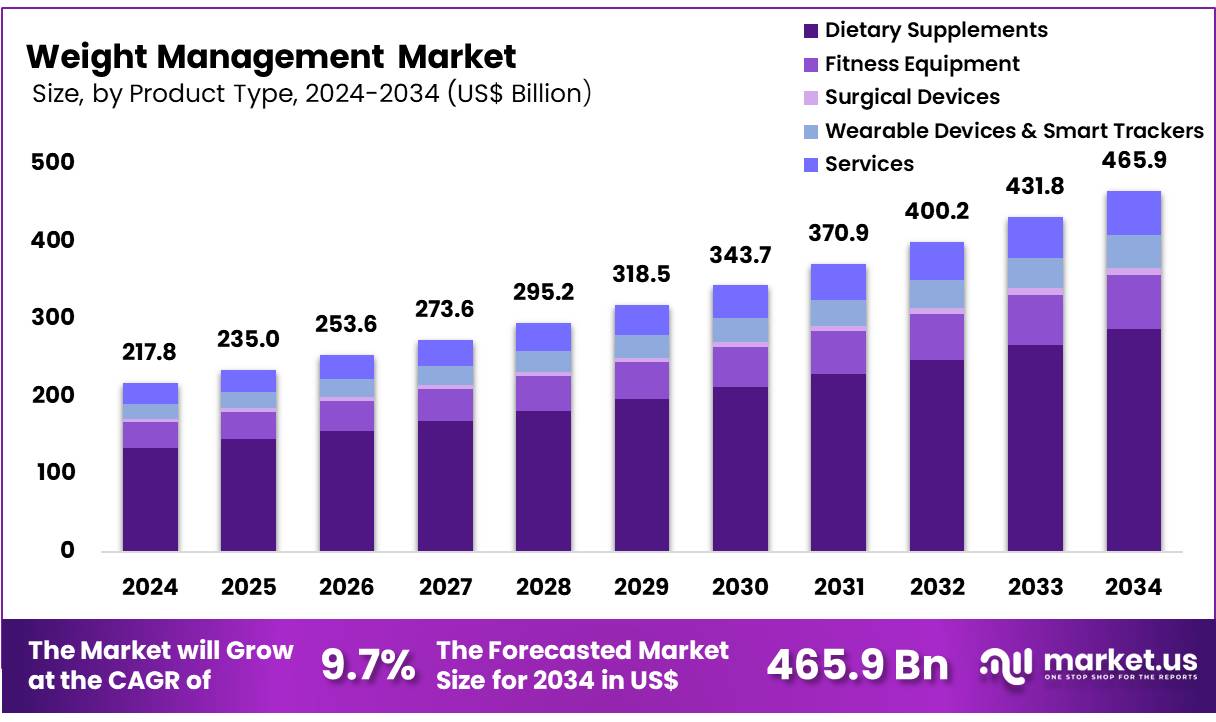

New York, NY – Nov 24, 2025 – Global Weight Management Market size is expected to be worth around US$ 465.9 Billion by 2034 from US$ 217.8 Billion in 2024, growing at a CAGR of 9.7% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 38.8% share with a revenue of US$ 84.5 Billion.

The weight management market has been experiencing steady expansion as demand for healthier lifestyles and scientifically supported nutritional solutions continues to rise. Growth in this sector has been driven by increasing awareness of obesity-related health risks, expanding adoption of preventive healthcare practices, and a rising preference for natural, low-calorie, and functional products. The demand for weight-control solutions has also been supported by changing dietary habits, higher disposable incomes, and greater accessibility to digital health platforms.

Weight-management offerings generally include meal-replacement products, dietary supplements, functional beverages, and structured fitness programs. The adoption of these solutions has been reinforced by advancements in product formulation, such as clean-label ingredients, plant-based proteins, and bioactive compounds that support metabolism. In addition, digital applications and connected devices have enabled more personalized guidance, improving adherence and long-term outcomes.

The market’s growth has further been supported by expanding retail penetration and the rapid rise of e-commerce channels, which have improved product availability across regions. Regulatory bodies have continued to emphasize product safety, ingredient transparency, and evidence-based claims, leading to increased consumer trust.

Weight-management brands are expected to benefit from continued innovation in natural ingredients, AI-enabled monitoring tools, and medically supervised programs. As consumers place greater value on holistic wellbeing, demand for integrated solutions combining nutrition, physical activity, and behavioral support is anticipated to remain strong. The sector is positioned for sustained growth as health consciousness continues to advance globally.

Key Takeaways

- The global weight management market is projected to reach US$ 465.9 billion by 2034, rising from US$ 217.8 billion in 2024.

- The market is anticipated to expand at a CAGR of 9.7% between 2025 and 2034.

- Dietary supplements constitute the leading product category, representing around 61.7% of the overall market share.

- Offline distribution channels remain dominant, accounting for approximately 57.3% of total market share.

- The Asia Pacific region is expected to lead the global market in 2024, holding about 38.8% of the total share.

Regional Analysis

In 2024, the Asia Pacific region is expected to lead the global weight management market, accounting for nearly 38.8% of the total share. This dominance is supported by a rising incidence of obesity and lifestyle-related health issues across major economies such as China, India, Japan, and South Korea. Rapid urbanization, reduced physical activity, and shifts toward high-calorie diets have increased the need for effective weight control solutions.

Growing health awareness and higher disposable incomes are encouraging consumers to adopt dietary supplements, fitness equipment, and smart health-monitoring devices. The expanding fitness-oriented population across the region has further supported this trend. Public health programs initiated by governments and healthcare organizations to address obesity and promote preventive healthcare are also influencing market expansion.

In addition, strong participation from both domestic and global companies, combined with the rapid rise of e-commerce platforms, has improved product availability and accessibility. These factors position the Asia Pacific region as a highly attractive market for stakeholders in the weight management industry.

Emerging Trends

- High Prevalence of Obesity and Overweight: Recent findings showed that 40.3% of U.S. adults were classified with obesity during August 2021–August 2023, while 73.6% were overweight or obese combined. This elevated prevalence continues to reinforce the need for comprehensive management strategies and preventive health policies.

- Expansion of Telehealth and Digital Lifestyle Programs: Weight management offerings have expanded through online, in-person, distance learning, and hybrid delivery models. The CDC’s National Diabetes Prevention Program now includes hundreds of providers delivering its evidence-based year-long curriculum through both remote and traditional sessions.

- Emphasis on Prediabetes Identification: An estimated 96 million American adults—or more than one-third of the population—are living with prediabetes. This group represents a critical target for early interventions designed to prevent progression to type 2 diabetes through structured weight management strategies.

- Growing Adoption of GLP-1 Receptor Agonists: Pharmacological options have broadened with FDA-approved GLP-1 agonists for long-term weight management. Semaglutide, marketed as Wegovy, received approval on June 4, 2021, with a standard maintenance dose of 2.4 mg weekly, underscoring a shift toward medicalized obesity care.

- Strengthened Nutritional Labeling Policies: Calorie labeling requirements under the Affordable Care Act have been associated with declines in calories purchased from restaurants and an estimated $8 billion in net savings over 20 years. These measures support weight control by facilitating informed consumer decision-making.

Use Cases

- Lifestyle Change Programs for Prediabetes: The original Diabetes Prevention Program demonstrated strong engagement, as 2,776 of 3,149 eligible participants representing 88% continued into the extended Outcomes Study. This reflects sustained interest in structured lifestyle interventions that emphasize weight control.

- Flexible Delivery of the National DPP: The CDC’s registry of recognized organizations provides the PreventT2 curriculum via online, in-person, distance, and hybrid formats. This flexible delivery framework has supported broader enrollment and improved accessibility for diverse demographic groups.

- GLP-1 Agonist Therapy for Cardiovascular Risk Reduction: Wegovy became the first weight-loss medication approved to reduce the risk of major cardiovascular events in adults with obesity or overweight who also have cardiovascular disease. This demonstrates a more integrated approach to managing weight and associated comorbidities.

- Insurance Coverage Dynamics: Approximately half of private employer-sponsored health plans include coverage for GLP-1 receptor agonists for weight management. In contrast, coverage remains limited under Medicare Part D and many Medicaid programs, affecting accessibility to pharmacological treatment options.

Frequently Asked Questions on Weight Management

- What is weight management?

Weight management is defined as a systematic approach that focuses on maintaining healthy body weight through balanced nutrition, controlled calorie intake, physical activity, and behavioral adjustments. Sustainable practices are emphasized to support metabolic health, prevent obesity, and reduce chronic disease risks. - Why is weight management important?

Weight management is considered essential because it improves metabolic functions, reduces cardiovascular risks, enhances physical performance, and supports long-term health outcomes. Balanced weight reduces the burden of lifestyle diseases and contributes to improved quality of life across diverse population groups. - What factors influence weight management?

Weight management outcomes are influenced by diet quality, physical activity levels, genetic predisposition, sleep cycles, and hormonal balance. Environmental variables, including food availability and lifestyle patterns, also shape overall success in achieving and maintaining healthy weight levels over time. - What are common strategies for weight management?

Key strategies include structured calorie control, regular exercise routines, increased protein intake, portion monitoring, and behavioral tracking. These methods are widely adopted to promote gradual weight change, enhance metabolic efficiency, and prevent weight regain through sustainable lifestyle adjustments. - What is driving the growth of the weight management market?

Market growth is attributed to rising obesity prevalence, increased consumer interest in preventive healthcare, and broader acceptance of digital wellness tools. Expanding demand for natural ingredients and personalized solutions also supports sustained development across global weight management segments. - Which segments dominate the weight management market?

Major segments include dietary supplements, functional foods, fitness services, and weight-loss programs. Supplement and meal replacement categories demonstrate strong adoption due to convenience, while digital tracking platforms gain traction as consumers prioritize accessible and personalized weight-related solutions. - What trends are shaping the weight management market?

Significant trends include personalized nutrition, AI-based wellness platforms, plant-based product expansion, and medical-grade weight-loss therapies. Increased interest in metabolic health and preventive care continues to influence consumer preferences and industry innovation across global markets.

Conclusion

The weight management market is positioned for sustained expansion as rising health consciousness, obesity prevalence, and demand for natural, science-backed solutions continue to influence consumer behavior. Steady adoption of dietary supplements, functional products, and digital monitoring tools reinforces market growth, supported by advancements in formulation and personalized guidance.

Strong momentum across Asia Pacific, combined with evolving regulatory support and broader access through retail and e-commerce channels, is expected to enhance market penetration. Increasing utilization of medical therapies, preventive programs, and integrated lifestyle solutions further strengthens long-term prospects, ensuring continued progression of the global weight management industry.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)