Table of Contents

Overview

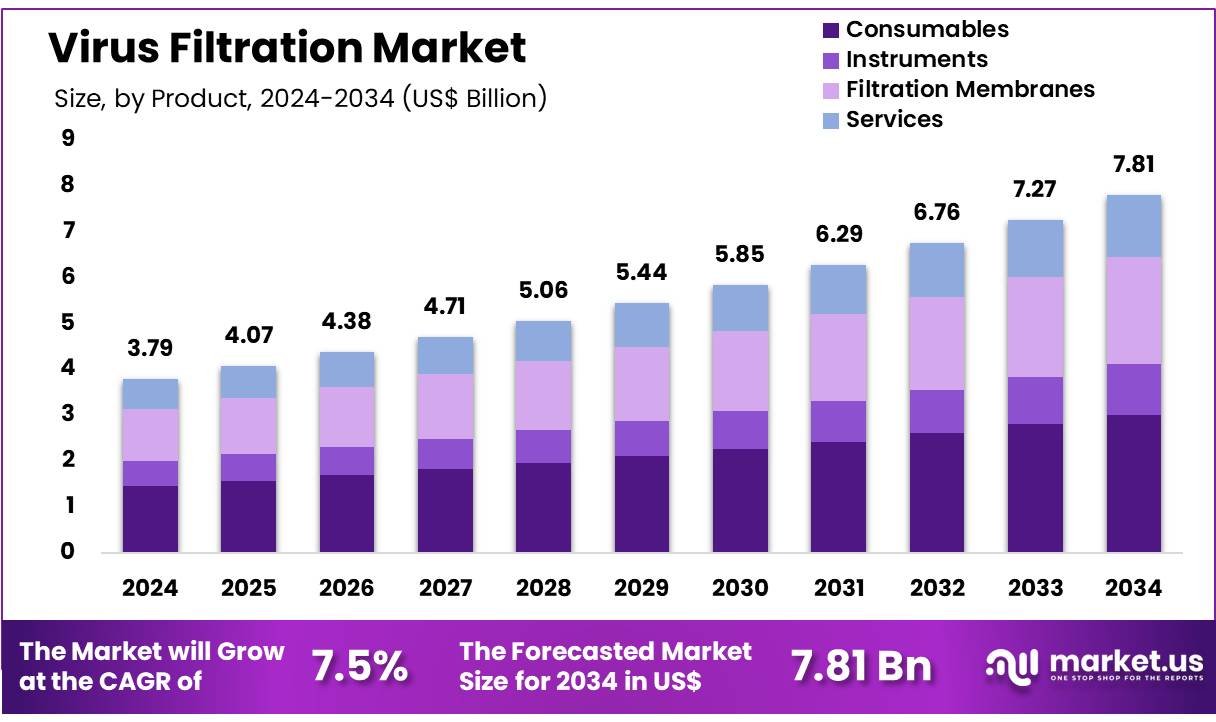

New York, NY – Nov 19, 2025 – Global Virus Filtration Market size is expected to be worth around US$ 7.81 Billion by 2034 from US$ 3.79 Billion in 2024, growing at a CAGR of 7.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 41.4% share with a revenue of US$ 1.57 Billion.

The global virus filtration market has been witnessing steady expansion, driven by increasing biopharmaceutical production and rising emphasis on product safety. Growing adoption of biological therapeutics and stringent regulatory guidelines have created significant demand for effective virus removal and virus detection solutions. The growth of the market can be attributed to advancements in filtration technologies, increased investment in life sciences research, and expanding applications across vaccines, recombinant proteins, and gene therapy products.

Virus filtration has been recognized as a critical step in downstream bioprocessing, ensuring the purity and efficacy of high-value biologics. The technology is widely utilized to safeguard products against potential viral contaminants, thereby supporting compliance with international quality standards. Membrane filters, consumables, and dedicated filtration systems continue to gain prominence as pharmaceutical manufacturers strengthen their risk-mitigation frameworks.

Rising prevalence of chronic and infectious diseases has encouraged greater reliance on biologics, further accelerating demand for robust virus filtration platforms. The market has also benefited from continuous improvements in filter materials, process efficiency, and scalability, allowing manufacturers to enhance throughput while maintaining product integrity. Strategic collaborations and capacity-expansion initiatives across the biopharmaceutical sector have reinforced the adoption of virus filtration technologies globally.

Increasing research activity in cell and gene therapies, along with expanded vaccine development pipelines, is expected to support sustained market growth over the coming years. The virus filtration market is anticipated to remain an essential component of modern bioprocessing as industry stakeholders prioritize safety, regulatory compliance, and long-term innovation.

Key Takeaways

- In 2024, the virus filtration market generated revenue amounting to US$ 79 billion, supported by a CAGR of 7.5%, and is projected to reach US$ 7.81 billion by 2033.

- The product and services segment is categorized into Consumables (Kits and Reagents, Others), Instruments (Filtration Systems, Chromatography Systems), Filtration Membranes, and Services. Consumables accounted for the leading share in 2024, representing 38.6% of the overall market.

- By technology, the market is segmented into Ultrafiltration (UF), Microfiltration (MF), Nanofiltration (NF), Chromatography-Based Filtration, and Electropositive Filtration. Ultrafiltration emerged as the dominant technology, contributing 35.5% to the total market share.

- In terms of application, the market is divided into Biopharmaceuticals, Water Purification, Air Purification, Food and Beverage, Medical Devices, and Gene Therapy. The Biopharmaceuticals segment held the largest revenue share, accounting for 37.2% of the virus filtration market.

- Considering the end user perspective, the market includes Biopharmaceutical Manufacturers, Contract Manufacturing Organizations (CMOs), Research Laboratories, Hospitals and Healthcare Centers, Medical Device Companies, and Others. Biopharmaceutical Manufacturers led the segment with a 34.0% share.

- Regionally, North America dominated the global market landscape, recording a 41.4% share in 2024.

Segmentation Analysis

- Product Analysis: The consumables segment accounts for 38.6% of the virus filtration market and continues to lead due to sustained demand for kits and reagents used in laboratory and manufacturing environments. These consumables remain essential for virus removal across biotechnology and healthcare workflows. Instruments and services, although smaller in share, are recording steady growth as installation, maintenance, and operational support services become increasingly necessary. Filtration membranes also contribute significantly because of their high efficiency and consistent performance in pharmaceutical processing and water treatment applications.

- Technology Analysis: Ultrafiltration holds a dominant 35.5% share in the technology segment, supported by its optimized pore size and superior membrane characteristics that ensure reliable virus removal across pharmaceutical, biotechnology, and water treatment uses. Microfiltration remains a widely adopted approach for capturing larger viral particles, particularly in food and beverage processing. Nanofiltration follows closely, offering effective removal of smaller contaminants. In March 2025, DuPont introduced WAVE PRO, designed to enhance ultrafiltration system efficiency across diverse water treatment applications.

- Application Analysis: Biopharmaceuticals constitute the largest application segment with a 37.2% share, driven by stringent viral safety requirements in the production of biologics, vaccines, and advanced therapeutics. Virus filtration is critical for ensuring sterility and regulatory compliance in these processes. Water purification forms the second-largest segment as global concerns regarding viral contaminants in drinking water continue to intensify. Air purification has gained notable momentum following the COVID-19 pandemic. In October 2024, Asahi Kasei Medical launched Planova FG1, a high-flux virus removal filter designed to support biotherapeutic manufacturing, further advancing this segment.

- End-User Analysis: Biopharmaceutical manufacturers represent the leading end-user group with a 34.0% market share, driven by regulatory obligations that necessitate high-performance virus filtration systems for vaccine and drug production. Contract manufacturing organizations follow closely, using advanced filtration technologies to support outsourced bioprocessing activities. In May 2024, Asahi Kasei Medical completed its third assembly plant for Planova virus removal filters in Japan, reflecting strong global demand and reinforcing the company’s position within CDMO and biosafety operations.

Regional Analysis

North America has been recognized as the leading region in the Virus Filtration Market. The dominance of the region can be attributed to a well-established healthcare infrastructure, rigorous regulatory frameworks, and sustained demand for advanced filtration technologies across pharmaceuticals, biotechnology, and healthcare applications. The expansion of the biopharmaceutical industry has served as a central growth driver, as regulatory bodies mandate comprehensive viral safety protocols in the production of vaccines, biologics, and therapeutic proteins.

Regulatory authorities such as the U.S. Food and Drug Administration (FDA) enforce strict virus filtration requirements for biologic manufacturing, which has strengthened the adoption of high-performance filtration systems. The presence of significant investments in research and development, particularly in biotechnology, cell therapy, and gene therapy, has further supported the need for reliable and efficient virus filtration solutions.

The COVID-19 pandemic also increased the emphasis on enhanced air and water filtration technologies, thereby reinforcing the region’s market position. Moreover, the presence of major industry participants, including Merck, Pall Corporation, and Thermo Fisher Scientific, has contributed to technological advancements and sustained leadership in the North American market.

Frequently Asked Questions on Virus Filtration

- How does virus filtration work?

Virus filtration works through size-exclusion mechanisms, where membrane pores are engineered to retain viruses while allowing target molecules to pass. This approach provides consistent virus clearance and is considered a critical step in biologics production and other regulated manufacturing workflows. - Why is virus filtration important in biopharmaceutical manufacturing?

Virus filtration is important because it ensures the removal of potential viral impurities from vaccines, monoclonal antibodies, and plasma-derived products. Compliance with regulatory standards requires robust virus clearance steps to maintain patient safety and strengthen product reliability. - What types of filters are used in virus filtration?

Virus filtration typically uses nanofiltration membranes made from polymers such as polyethersulfone. These filters are optimized to capture small, non-enveloped viruses and deliver reproducible performance, supporting advanced manufacturing processes across biopharmaceutical and biotechnology applications. - Which industries use virus filtration technology?

Virus filtration is used across biologics manufacturing, vaccine production, gene therapy development, and plasma-derived product processing. The technology supports safety and regulatory compliance in sectors that rely on high-purity products for clinical use and global commercial distribution. - What are the key advantages of virus filtration?

Key advantages include high viral clearance capability, minimal impact on product quality, and strong regulatory acceptance. Virus filtration provides predictable performance with simple integration into upstream or downstream workflows, making it a preferred method in critical purification processes. - Which regions dominate the virus filtration market?

North America dominates due to advanced bioprocessing infrastructure and strong regulatory oversight. Europe follows with growing biopharma production, while Asia-Pacific is expanding rapidly as manufacturing capacity increases and regional governments invest in biotechnology development programs. - Which end-use industries contribute most to the market?

Biopharmaceutical companies contribute the largest share, followed by research institutes and contract manufacturing organizations. These segments rely on virus filtration to ensure consistent purity in biologics, vaccines, and advanced therapeutics that require stringent contamination-control protocols.

Conclusion

The virus filtration market has been characterized by sustained growth, driven by expanding biologics production, strict regulatory expectations, and rising adoption of advanced therapeutics. Continuous innovation in membrane materials, consumables, and filtration systems has enhanced process efficiency and strengthened viral safety across biopharmaceutical workflows.

Increasing prevalence of chronic and infectious diseases has reinforced the need for reliable viral clearance technologies, while growing investments in cell and gene therapy research continue to stimulate market demand. With strong contributions from biopharmaceutical manufacturers and dominance of technologically advanced regions such as North America, the market is expected to maintain a steady, long-term growth trajectory.