Table of Contents

Overview

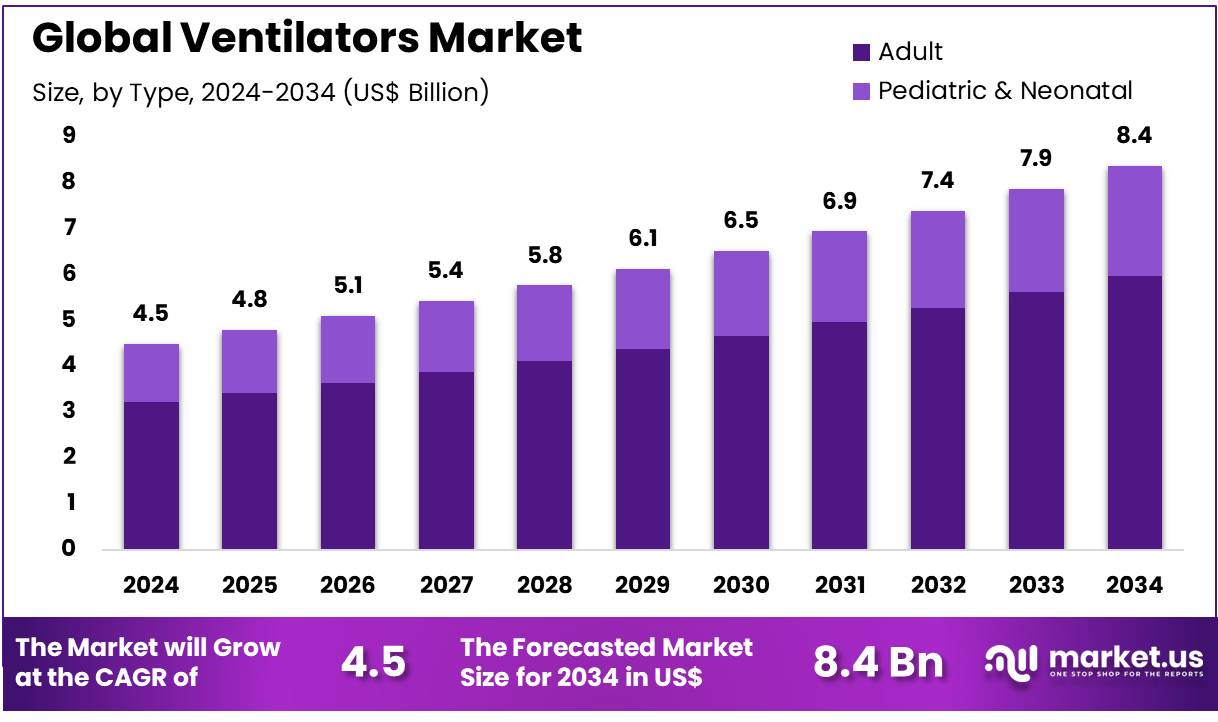

New York, NY – Nov 13, 2025 – Global Ventilators Market size is expected to be worth around US$ 8.4 Billion by 2034 from US$ 4.5 Billion in 2024, growing at a CAGR of 6.4% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 41.2% share with a revenue of US$ 1.9 Billion.

The global demand for ventilators has expanded steadily as respiratory care needs have increased across clinical settings. Ventilators are medical devices designed to support or replace spontaneous breathing by delivering controlled oxygen flow to patients who experience compromised respiratory function. Their deployment has been observed in intensive care units, emergency departments, surgical environments, and home-care settings, where the stabilization of breathing parameters is required for critical or chronic conditions.

The operational mechanism of a ventilator is based on regulated airflow, pressure control, and monitoring systems that maintain adequate oxygenation. The use of advanced sensors and microprocessor-based controls has improved patient safety, reduced the risk of ventilator-associated complications, and enhanced the precision of respiratory support. The growth of the market can be attributed to rising incidences of chronic obstructive pulmonary disease, asthma, and acute respiratory distress syndrome, along with an aging population susceptible to respiratory failure.

Demand for portable and non-invasive ventilators has increased significantly as home-care adoption continues to expand. The integration of telemonitoring and data analytics has enabled healthcare providers to track patient conditions in real time, allowing timely interventions and improved treatment outcomes. Product development activities have focused on mobility, energy efficiency, and user-friendly interfaces to support both clinical professionals and non-clinical caregivers.

Overall, ventilators have become essential components of modern healthcare infrastructure, and continued technological improvements are expected to drive sustained market growth in the coming years.

Key Takeaways

- In 2024, the ventilators market generated revenue of US$ 4.5 billion, supported by a 6.4% CAGR, and is projected to reach US$ 8.4 billion by 2033.

- The product type segment comprises ventilator machines and accessories, with ventilator machines accounting for 64.3% of the market share in 2023.

- By type, the market is divided into adult and pediatric & neonatal, where the adult segment held a dominant share of 71.5%.

- The interface segment includes non-invasive and invasive ventilators, with non-invasive ventilators leading the market with a 58.6% revenue share.

- In terms of end users, the market is categorized into hospitals & clinics, ambulatory surgical centers, home healthcare, and others. Hospitals & clinics led the segment with a 52.8% share.

- North America emerged as the leading regional market, securing 41.2% of the global share in 2023.

Regional Analysis

North America Leading the Ventilators Market

North America held the largest revenue share of 41.2%, supported by strong technological advancements and a rising burden of respiratory diseases. The introduction of software upgrades for Getinge AB’s Servo-u and Servo-n ventilators, along with the release of the Servo-u MR ventilator in April 2021, enhanced the region’s access to advanced critical care systems. The increasing prevalence of COPD, asthma, and other respiratory conditions continued to elevate the demand for sophisticated ventilation support.

The expansion of ICU capacities in hospitals and long-term care centers further contributed to market growth. The adoption of AI-enabled and remote monitoring features improved patient management efficiency and strengthened clinical outcomes. Government investments in pandemic preparedness and respiratory care initiatives also stimulated innovation. Additionally, the growing elderly population increased the need for non-invasive and home-based ventilation devices, reinforcing overall market expansion in North America.

Asia Pacific Expected to Record the Highest CAGR

Asia Pacific is projected to achieve the fastest CAGR due to increasing healthcare expenditure and rising incidences of respiratory disorders. Vyaire Medical, Inc.’s donation of ventilators, CPAP/BIPAP systems, and oxygen concentrators to India in May 2021 highlighted the region’s requirement for advanced respiratory care.

The high prevalence of pollution-related respiratory conditions is expected to drive strong uptake of mechanical ventilation systems. Government initiatives aimed at improving critical care infrastructure and emergency readiness are anticipated to support further growth. Strategic collaborations between global device manufacturers and regional healthcare organizations are expected to enhance access to quality respiratory support technologies.

Growing adoption of portable and home-care ventilation devices is likely to strengthen chronic disease management, while the expansion of private healthcare networks and increasing focus on telehealth integration are projected to accelerate the demand for advanced ventilatory solutions across Asia Pacific.

Emerging Trends

- Widening Global Capacity Gaps: Significant disparities in ventilator availability continue to be observed across income groups. Low-income countries report an average of 0.14 ventilators per 100,000 people, while upper-middle-income countries average 2.49 per 100,000. These gaps are being mitigated through international assistance and targeted capacity-building initiatives.

- Pandemic Surge Planning: Health systems have incorporated predictive models to estimate peak ventilator requirements during public health crises. In the United States, assessments suggest hospitals could integrate an additional 26,200 to 56,300 ventilators during a severe influenza pandemic, guiding national stockpile strategies and regional allocation planning.

- Strategic National Stockpiling: Centralized ventilator reserves have been institutionalized to enhance emergency response capabilities. The U.S. Strategic National Stockpile maintains a dedicated inventory of mechanical ventilators that can be rapidly distributed to states and healthcare systems during critical public health events.

Use Cases

- Management of COPD with COVID-19: Hospital data from the United States indicate that 19.5% of patients with chronic obstructive pulmonary disease (COPD) and COVID-19 required invasive mechanical ventilation, demonstrating its essential role in stabilizing individuals experiencing acute respiratory deterioration.

- Support in Severe RSV Infections: Surveillance of respiratory syncytial virus (RSV) cases across 12 U.S. states from July 2022 to June 2023 shows that 4.8% of patients required mechanical ventilation. This reflects the device’s importance in managing severe respiratory distress, particularly among pediatric and older adult groups.

Frequently Asked Questions on Ventilators

- What is a ventilator?

A ventilator is a medical device used to support respiratory function by delivering controlled airflow into the lungs when natural breathing becomes inadequate. It is widely utilized in intensive care units to stabilize patients with severe respiratory failure. - How does a ventilator work?

A ventilator functions by pushing air or an oxygen-rich mixture into the lungs through preset pressure or volume modes. The device ensures consistent ventilation, maintaining vital gas exchange and supporting patients who cannot sustain spontaneous breathing. - When is a ventilator used?

A ventilator is used when respiratory function becomes compromised due to conditions such as pneumonia, ARDS, COPD exacerbations, or trauma. It provides temporary breathing support until the patient regains sufficient lung strength to resume independent respiration. - What are the major types of ventilators?

Ventilators are categorized into invasive, non-invasive, and portable systems. Each type is designed to meet different clinical requirements, offering varying levels of respiratory support for emergency care, intensive care units, and home-care environments. - Are ventilators safe for long-term use?

Ventilators are considered safe for prolonged use when closely monitored by medical professionals. Continuous assessment ensures appropriate settings, reduces complications, and supports patient recovery while sustaining adequate oxygenation during extended respiratory support. - Which regions dominate the ventilators market?

North America and Europe currently dominate the ventilators market due to advanced healthcare infrastructure, higher adoption of critical-care technologies, and strong reimbursement systems. Significant expansion is also being observed across Asia-Pacific, supported by rapidly improving hospital capacities. - What are key trends in the ventilators market?

Key market trends include the adoption of portable ventilators, increasing preference for non-invasive solutions, and integration of digital monitoring technologies. Advancements in automation and connectivity are enhancing treatment efficiency and improving overall patient management. - Who are the major players in the ventilators market?

Major market participants include Philips Healthcare, GE Healthcare, Medtronic, Hamilton Medical, and Draeger. These companies dominate through strong product portfolios, significant research investments, and extensive distribution networks supporting global demand for respiratory care equipment.

Conclusion

The global ventilators market is expected to expand steadily, driven by rising respiratory disease prevalence, increasing adoption of non-invasive and portable systems, and ongoing technological advancements.

Strong demand across hospitals, home-care settings, and emergency care continues to support market growth, while regional trends highlight North America’s leadership and Asia Pacific’s rapid expansion. Capacity-building programs, strategic stockpiling, and pandemic preparedness efforts are strengthening global readiness for future health emergencies.

As innovations in AI, telemonitoring, and patient-centric design progress, ventilators are expected to remain essential components of critical and chronic respiratory care, ensuring sustained market momentum over the forecast period.