Table of Contents

Overview

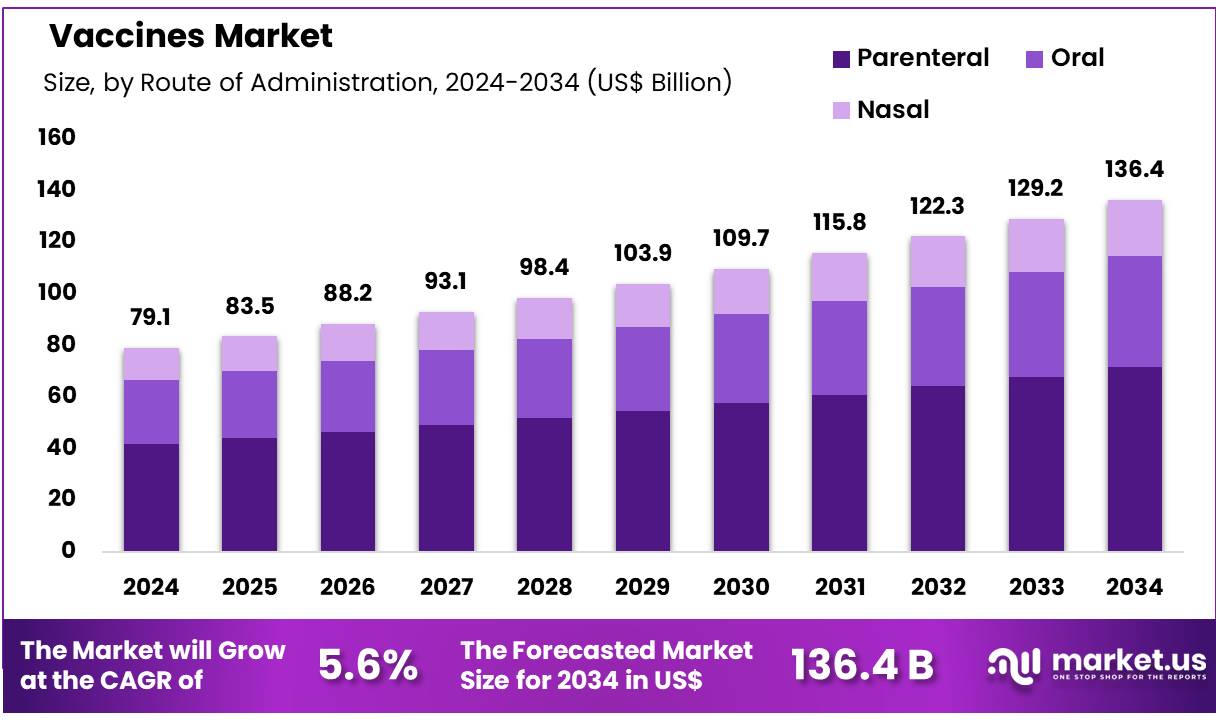

New York, NY – Nov 07, 2025 – Global Vaccines Market size is expected to be worth around US$ 136.4 billion by 2034 from US$ 79.1 billion in 2024, growing at a CAGR of 5.6% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.1% share with a revenue of US$ 33.3 Billion.

The development of vaccines continues to be recognized as one of the most effective public health interventions, as significant progress has been made in preventing infectious diseases and reducing global morbidity.

The formation of vaccines is based on the scientific principle that controlled exposure to an antigen can trigger an immune response without causing the associated illness. This principle has been applied across multiple platforms, including live attenuated, inactivated, subunit, conjugate, and mRNA technologies. Each platform has been designed to stimulate protective immunity while maintaining a strong safety profile.

The market for vaccines has been expanding, as rising disease awareness, increasing immunization coverage, and ongoing innovation have contributed to growing demand. Investment in vaccine research has been accelerated, as emphasis has been placed on rapid development, scalable manufacturing, and broader access. Advancements in biotechnology have enabled the creation of highly targeted formulations, improving both efficacy and adaptability.

The growth of the global vaccine sector has been supported by government programs, public–private partnerships, and international health organizations. These efforts have strengthened supply chains, enhanced regulatory pathways, and improved distribution infrastructures. The expansion of preventive healthcare initiatives is expected to further drive uptake, particularly in emerging economies.

The continued evolution of vaccine science reflects a commitment to safeguarding public health and preparing for future disease threats. The increasing adoption of next-generation platforms is expected to reinforce market resilience and support long-term growth across the global immunization landscape.

Key Takeaways

- In 2024, the global vaccines market generated revenue of US$ 79.1 billion, and growth has been projected at a CAGR of 5.6%, with the market expected to reach US$ 136.4 billion by 2033.

- Based on product type, the market has been categorized into subunit vaccines, viral vector vaccines, mRNA vaccines, live attenuated vaccines, and inactivated vaccines, with mRNA vaccines accounting for the largest share at 38.4% in 2023.

- By route of administration, the market has been segmented into oral, parenteral, and nasal, and the parenteral route held a dominant share of 52.6%.

- In terms of application, the market has been divided into viral diseases, bacterial vaccines, cancer vaccines, and allergy vaccines, with viral diseases representing the leading segment at 44.2% of total revenue.

- Considering distribution channels, the market includes hospital and retail pharmacies, government suppliers, and others, with government suppliers contributing the highest share at 48.5%.

- Regionally, North America led the global vaccines market, holding a 42.1% share in 2024.

Regional Analysis

North America Leading the Vaccines Market

North America accounted for the largest revenue share of 42.1%, supported by rising demand for immunization programs and continuous advancements in vaccine technology. The FDA approval of Merck & Co., Inc.’s PCV15 (Vaxneuvance) in June 2022, aimed at preventing pneumococcal disease in children, strengthened the region’s focus on expanding pediatric vaccination coverage. The increasing prevalence of infectious diseases, combined with greater awareness of preventive healthcare, contributed to higher vaccination uptake across age groups.

Government-backed initiatives and funding for routine and seasonal immunization programs reinforced overall market growth. The rapid adoption of mRNA-based platforms and next-generation vaccine technologies improved efficacy and accelerated production capabilities. In addition, private-sector investments in research and development supported the introduction of enhanced immunization solutions targeting both common and emerging pathogens.

The strong presence of established pharmaceutical companies, along with collaborations involving biotechnology firms, accelerated product innovation and strengthened distribution networks. The adoption of digital health tools further improved patient engagement, supporting adherence to recommended immunization schedules.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region has been projected to grow at the fastest CAGR, driven by rising investment in immunization programs and the development of advanced vaccine formulations. Maxvax Biotechnology’s Series C funding of USD 82.5 million in July 2024 highlighted the region’s growing commitment to vaccine innovation. Expanding healthcare infrastructure in China, India, and Japan is expected to improve accessibility and strengthen distribution capabilities.

Government-led initiatives promoting large-scale vaccination campaigns for both children and adults are anticipated to accelerate market penetration. Increased collaboration between global pharmaceutical companies and regional biotech firms is expected to support faster innovation and regulatory approvals. Rising awareness of the role of immunization in preventing respiratory and vector-borne diseases has been projected to drive demand further.

The integration of AI-driven research tools and advanced manufacturing frameworks is likely to improve production efficiency. Additionally, expanding public-private partnerships aimed at addressing vaccine hesitancy and strengthening outreach efforts are expected to support sustained market growth across the Asia Pacific region.

Emerging Trends

Significant progress has been recorded in messenger RNA (mRNA) vaccine platforms. The rapid development and deployment of mRNA vaccines during the COVID-19 pandemic have enabled their evaluation against additional infectious diseases, including influenza and respiratory syncytial virus (RSV). Advances in antigen design, involving optimized mRNA constructs and improved lipid nanoparticle formulations, are being pursued to strengthen immune responses and expand protection against emerging variants. Candidate mRNA vaccines targeting pathogens such as human immunodeficiency virus (HIV), malaria, and tuberculosis are currently being monitored in the World Health Organization’s vaccine development pipeline, which undergoes biannual updates.

Growth in vaccine valency has also been observed, with efforts focused on integrating multiple antigens into single formulations. For pneumococcal disease, higher-valency conjugate vaccines (PCV15, PCV20, and PCV21) have been introduced from 2021 to 2024 to broaden serotype coverage for invasive infections. Seasonal influenza vaccine composition continues to be updated to align with circulating strains, and the recommended hemagglutinin antigens for the 2025–2026 northern hemisphere season have been issued by the WHO to improve vaccine performance. These polyvalent and strain-tailored approaches are intended to optimize population immunity and reduce the burden of vaccine-preventable diseases.

A notable shift toward adult immunization has been documented. Vaccines previously directed primarily at pediatric populations are being extended to older age groups. RSV vaccination uptake reached approximately 38.1 percent among adults aged 60–74 years with high-risk conditions as of April 26, 2025, indicating increased acceptance of newly licensed RSV vaccines. COVID-19 vaccination continues to be recommended for all individuals aged 6 months and older, with additional doses advised to counteract waning immunity against emerging SARS-CoV-2 lineages such as Omicron JN.1 and KP.2. Expansion of adult and booster vaccination strategies is expected to reduce severe outcomes and hospitalization across all demographic segments.

Growing attention is being placed on global immunization equity and disease surveillance, as disparities in coverage are contributing to heightened outbreak risk. In 2025, declining infant vaccination rates in regions including Kenya increased vulnerability to measles, polio, and other preventable diseases. Concurrently, meningitis incidence in Africa rose to more than 5,500 suspected cases and nearly 300 deaths in the first quarter of 2025, highlighting the urgent need for strengthened immunization programs. Investments in routine vaccination systems, targeted catch-up campaigns, and community engagement are being prioritized to address these gaps and reinforce global health security.

Use Cases

COVID-19 vaccines have been widely utilized to reduce morbidity and mortality across age groups. For the 2024–2025 season, monovalent XBB.1-strain vaccines from Moderna, Pfizer-BioNTech, and Novavax were recommended for individuals aged 6 months and older. Interim evidence indicated that the 2024–2025 formulation decreased the risk of influenza-like illness and hospitalization among children and adults. Additional doses authorized under FDA Emergency Use Authorization for individuals aged 6 months to 11 years (Moderna, Pfizer-BioNTech) and 12 years and older (Novavax) have been employed to sustain immunity against evolving SARS-CoV-2 variants.

Seasonal influenza vaccines continue to serve a critical public health function by reducing outpatient visits and hospital admissions. During the 2024–2025 season, manufacturers forecasted supply of up to 148 million doses in the United States. Interim effectiveness findings showed reductions in outpatient visits and hospitalizations across all age groups, supporting CDC and ACIP guidance recommending annual vaccination for persons aged 6 months and older. These outcomes reinforce the public health value of widespread influenza immunization.

Human papillomavirus (HPV) vaccines have been expanded or newly adopted in several countries to prevent cervical cancer and other HPV-associated diseases. In 2024, four countries introduced HPV vaccination programs, and 25 countries transitioned to the WHO-endorsed single-dose schedule, which has simplified delivery and improved uptake. This expansion is expected to reduce HPV transmission and related malignancies, particularly in low- and middle-income regions where cervical cancer remains a leading cause of mortality among women.

RSV vaccines have been recommended for older adults and specific high-risk groups to mitigate severe respiratory disease. As of April 2025, vaccination coverage of 38.1 percent among adults aged 60–74 years with risk factors was reported. Immunization in this segment is projected to significantly reduce hospitalizations and healthcare utilization during peak RSV activity. Ongoing surveillance of vaccine-preventable respiratory diseases continues to guide RSV vaccine policy and supports targeted immunization efforts in long-term care settings and community environments.

Frequently Asked Questions on Vaccines Market

- What are vaccines?

Vaccines are biological preparations designed to stimulate the immune system to recognize and combat infectious agents. Their use results in reduced disease burden, improved population health, and long-term protection against various viral and bacterial threats. - How do vaccines work?

Vaccines work by introducing antigens that trigger an immune response without causing illness. This process enables the body to develop memory cells that recognize pathogens, ensuring rapid protection during future exposures to the same infectious agent. - Why are mRNA vaccines gaining prominence?

mRNA vaccines are gaining prominence due to their ability to generate strong immune responses and their rapid development timelines. Their adaptability to emerging pathogens makes them a preferred choice for manufacturers and healthcare systems worldwide. - Which region leads the global vaccines market?

North America leads the global vaccines market due to strong healthcare infrastructure, technological innovation, and government support for immunization. Established pharmaceutical companies and consistent investments in research further reinforce the region’s dominant position. - Why is Asia Pacific expected to grow fastest?

The Asia Pacific region is expected to grow fastest owing to increased healthcare investment, expanding vaccination campaigns, and rising awareness. Strengthening infrastructure and collaborations between global pharmaceutical firms and regional biotech companies support accelerated market growth. - What are the main applications of vaccines?

Vaccines are widely used for preventing viral and bacterial diseases, supporting cancer immunization initiatives, and managing allergy-related conditions. Their broad application range enhances public health outcomes and reduces long-term healthcare costs for populations. - How do government initiatives support vaccine adoption?

Government initiatives support vaccine adoption by funding immunization programs, improving access, and promoting public awareness. These efforts strengthen disease prevention strategies, enhance coverage rates, and ensure timely vaccination across different population groups. - What role does technology play in vaccine development?

Technology plays a major role in accelerating vaccine development by enabling advanced platforms such as mRNA, viral vectors, and AI-driven research. These innovations improve manufacturing efficiency, reduce timelines, and enhance the overall effectiveness of modern immunization solutions.

Conclusion

The vaccines market has been characterized by sustained growth, driven by rising immunization coverage, technological innovation, and strong government support. Increased investment in advanced platforms, including mRNA, conjugate, and high-valency formulations, has enhanced efficacy and expanded protection against emerging pathogens.

Strengthening healthcare infrastructure, particularly in Asia Pacific, is expected to accelerate future adoption. Continued focus on adult immunization, global health equity, and improved surveillance systems is reinforcing long-term market resilience.

Overall, the sector is positioned for steady expansion as preventive healthcare initiatives intensify and next-generation vaccine technologies gain broader acceptance worldwide.