Table of Contents

Overview

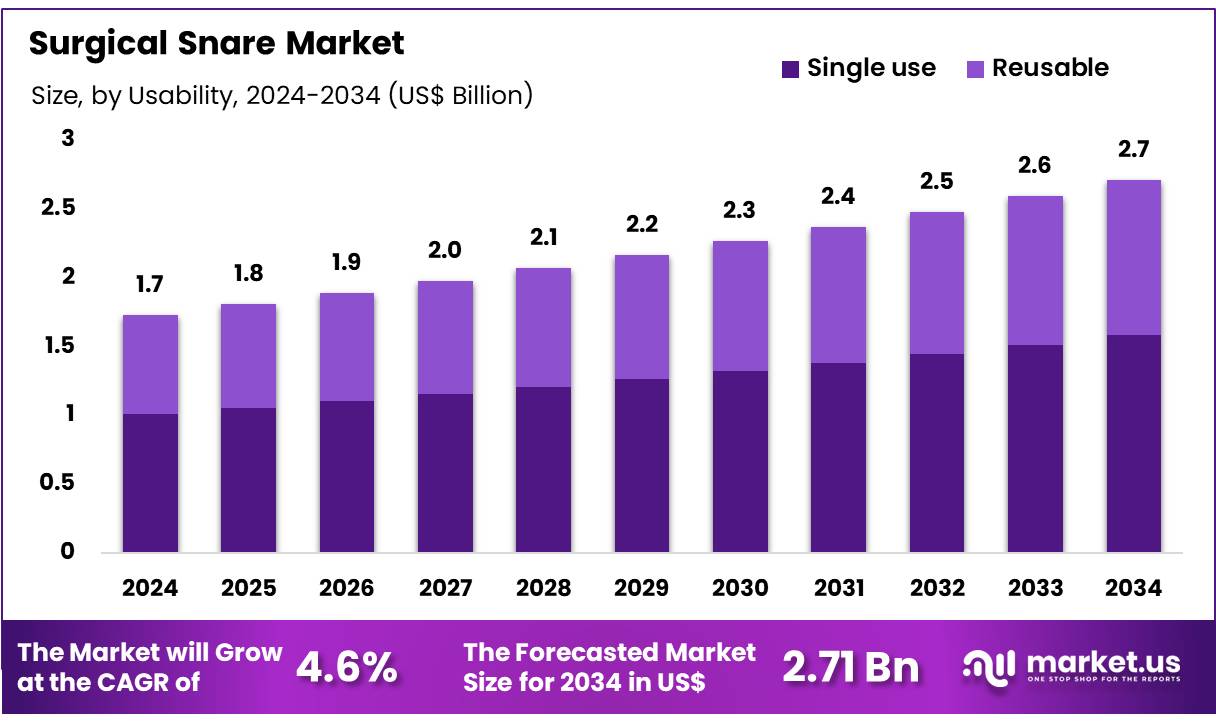

New York, NY – Nov 03, 2025 – Global Surgical Snare Market size is expected to be worth around US$ 2.71 Billion by 2034 from US$ 1.73 Billion in 2024, growing at a CAGR of 4.6% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 38.7% share with a revenue of US$ 0.67 Billion.

The introduction of an advanced surgical snare system has been announced to strengthen minimally invasive surgical capabilities across gastrointestinal, urological, and ENT procedures. The device has been developed to support precise tissue resection and polypectomy, enabling enhanced clinical outcomes through improved control and safety.

The new surgical snare is designed with high-grade stainless steel wire and reinforced sheath technology to ensure durability, flexibility, and consistent cutting performance. The adoption of ergonomic handle architecture and optimized loop configuration allows physicians to achieve greater procedural accuracy. The product has been engineered in compliance with stringent regulatory standards, ensuring safety and operational reliability across diverse clinical environments.

The demand for minimally invasive surgical tools has been expanding, driven by rising incidences of colorectal cancer, increasing screening programs, and ongoing advancements in endoscopic techniques. The introduction of this snare system is expected to support hospitals, ambulatory surgery centers, and specialty clinics in improving procedural efficiency and patient safety. Growth in early-stage diagnosis programs and adoption of technologically advanced surgical equipment has created favorable market potential.

The launch reflects a strategic focus on innovation, user-centric design, and improved therapeutic performance. Continued investment in research and collaboration with clinical professionals is planned to support broader product integration and training initiatives across global healthcare networks.

Key Takeaways

- The global surgical snare market generated revenue of US$ 73 billion in 2024 and recorded a CAGR of 4.6%. It is projected to reach US$ 2.71 billion by 2034.

- By type, the market is segmented into single-use, reusable, kallikrein inhibitors, and others. The single-use category dominated in 2024 with a 58.3% share.

- Based on application, the market includes GI endoscope, laparoscopy, urology endoscopy, gynecology endoscopy, arthroscopy, bronchoscopy, mediastinoscopy, laryngoscopy, and others. GI endoscope accounted for the largest contribution with 30.2%.

- Regarding end use, the market is categorized into hospitals and clinics. Hospitals and clinics represented the leading segment with 65.0% of revenue share in 2024.

- Regionally, North America emerged as the leading market, holding a 38.7% share in 2024.

Regional Analysis

The North American surgical snare market accounts for 38.7% of global revenue, supported by advanced healthcare infrastructure, substantial healthcare spending, and a strong shift toward minimally invasive surgical procedures.

The United States and Canada represent key markets, where hospitals, outpatient facilities, and ambulatory surgical centers conduct a high volume of endoscopy, laparoscopy, and urology procedures requiring surgical snares.

Market demand is being influenced by the increasing prevalence of chronic conditions, including gastrointestinal disorders, cancer, and urological diseases, alongside a growing elderly population.

The adoption of technologically enhanced snare systems, including electrosurgical and robot-assisted variants, has been contributing to improved procedural efficiency and clinical outcomes. Favorable reimbursement frameworks and rising utilization of minimally invasive techniques in clinical practice are expected to sustain market expansion across the region.

Emerging Trends

- Shift Toward Disposable Systems: The use of single-use snares has expanded to minimize infection risks and streamline sterilization processes. FDA classification of disposable polypectomy snares as Class II devices indicates strong regulatory support and increasing clinical adoption across endoscopy settings.

- Expansion of Therapeutic Indications: Surgical snares are now applied beyond traditional gastrointestinal procedures. Their utilization in cardiovascular interventions for intravascular foreign-body retrieval has grown, supported by device approvals such as the Radius Snare for vascular object management.

- Integration With Electrosurgical Platforms: Combined mechanical and electrocautery-based snares have become widely adopted for precise tissue resection with coagulation control. FDA-cleared flexible snares under product code FDI illustrate significant reliance on dual-mode electrosurgical capabilities in modern practices.

- Heightened Post-Market Vigilance: Regulatory oversight has intensified, reflected by FDA safety actions including recalls like the Captivator Polypectomy Snare. These measures emphasize structured surveillance to mitigate risks such as bleeding or perforation, ensuring continued device safety.

Use Cases

- Colorectal Polyp Resection: Electrosurgical snares are routinely used to excise colonic polyps during colonoscopy. High procedure volumes in the United States, indicated by more than 14 million colonoscopies in 2002, underscore widespread clinical dependence on snare-based polypectomy.

- Management of Early Barrett’s Esophagus: Snare-assisted endoscopic mucosal resection is applied for early malignant lesions in Barrett’s esophagus. Clinical evidence has demonstrated its feasibility and therapeutic value, supporting its role in minimally invasive gastrointestinal cancer management.

- Cardiovascular Foreign-Body Retrieval: Vascular snares are employed to remove or reposition intravascular devices such as coils or guidewires. The FDA-cleared Radius Snare enables minimally invasive retrieval techniques within the cardiovascular system, improving safety and procedural efficiency.

- Gynecologic Polyp Excision: Hysteroscopic snares, including devices like the KSEA HF-Snare, are indicated for the removal of uterine polyps and related pathology. Their clinical use has been established under appropriate surgical protocols in gynecologic care.

Frequently Asked Questions on Surgical Snare

- How does a surgical snare work?

The device operates through a wire loop that is placed around the tissue and gradually tightened. This action results in controlled excision. The procedure is commonly performed through endoscopic systems, ensuring precise tissue removal with limited bleeding. - What types of surgical snares are available?

Different types include cold snares, hot or electrosurgical snares, and rigid versus flexible variants. These options enable physicians to select appropriate devices depending on tissue size, anatomical location, and procedure complexity for improved clinical outcomes. - Which medical procedures use surgical snares?

Surgical snares are used in gastrointestinal endoscopy, ENT procedures, and gynecological surgeries. The technique is frequently applied to remove colon polyps, nasal lesions, and cervical polyps, supporting early diagnosis and treatment of abnormal growths. - Are surgical snares reusable or disposable?

Both reusable and single-use snares are available. Disposable snares are widely preferred due to their sterility and convenience. Reusable options are used in settings focused on cost efficiency and controlled cleaning protocols to maintain device integrity. - What are the benefits of using surgical snares?

Key benefits include precise tissue removal, reduced bleeding risks, and minimal scarring. The method supports outpatient procedures and faster recovery times. The accuracy and reliability make it suitable for routine and advanced clinical interventions across specialties. - Which regions lead the surgical snare market?

North America dominates due to high healthcare spending and screening adoption. Europe follows with strong medical infrastructure, while Asia-Pacific is witnessing rapid expansion supported by population growth, improving hospital access, and rising endoscopic procedure numbers. - Who are the key market participants?

Major participants include medical device manufacturers specializing in endoscopic instruments. Companies focus on product advancements, precision engineering, and ergonomic designs. Competitive strategies emphasize distribution partnerships, research investments, and regulatory compliance to support market penetration.

Conclusion

The market for surgical snares is positioned for steady expansion, driven by increasing adoption of minimally invasive procedures, rising disease screening programs, and continuous innovation in device design and electrosurgical integration.

Growth is supported by strong demand from hospitals and specialty centers, alongside regulatory approval pathways that encourage safe clinical use. Advancements in disposable technology, broadened applications across gastrointestinal, cardiovascular, and gynecologic interventions, and heightened post-market surveillance reinforce market progression.

North America maintains a leading position due to advanced healthcare infrastructure and reimbursement support. Continued investment in product development and clinical collaboration will sustain competitive advantage and global adoption.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)