Table of Contents

Overview

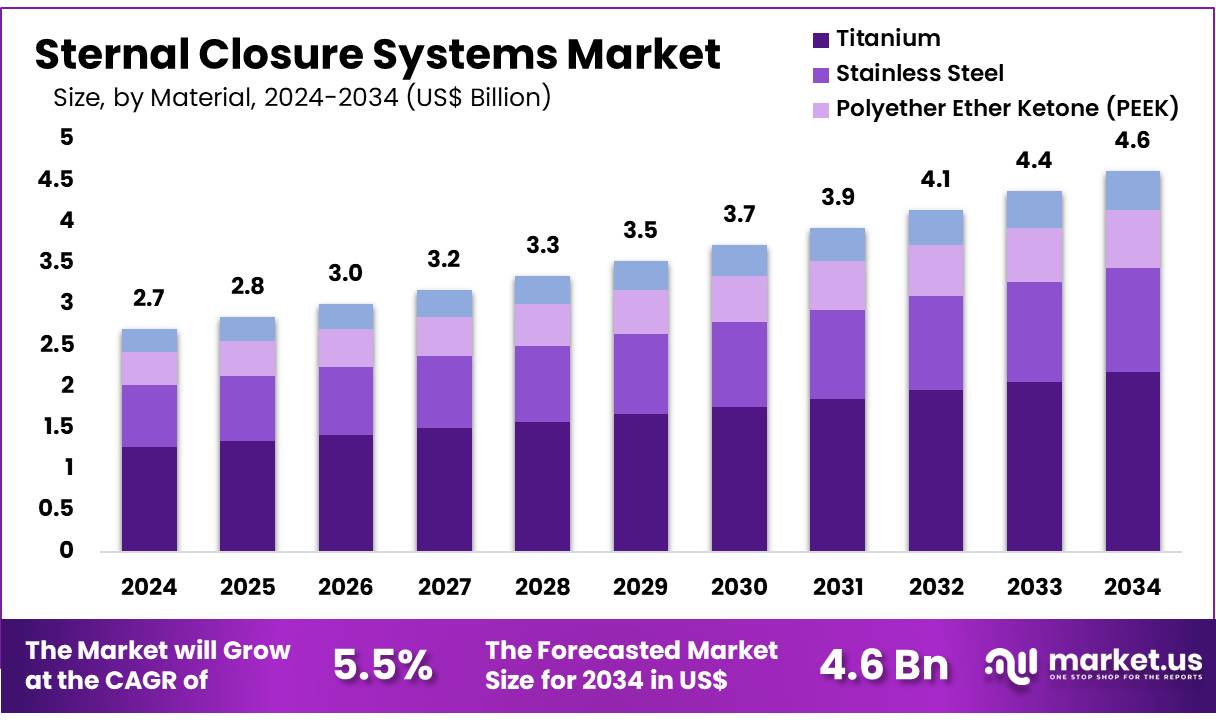

New York, NY – Nov 25, 2025 – Global Sternal Closure Systems Market size is expected to be worth around US$ 4.6 billion by 2034 from US$ 2.7 billion in 2024, growing at a CAGR of 5.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 37.9% share with a revenue of US$ 1.0 Billion.

The global sternal closure systems market is being shaped by steady demand for advanced cardiac surgery solutions and a rising focus on postoperative stability. Growth of the market can be attributed to the increasing prevalence of cardiovascular diseases, the expanding volume of open-heart surgeries, and continuous innovation in biocompatible materials. Adoption of rigid fixation systems has been rising, as these devices have been associated with improved stability, reduced complications, and enhanced recovery outcomes.

Technological progress has accelerated the transition from traditional wire-based closure methods to plates, screws, and novel polymer-based systems. The use of titanium plates and absorbable materials has been expanding due to their strength, compatibility, and lower risk of infection. In addition, the aging population and the growing incidence of obesity have contributed to increased surgical interventions requiring reinforced sternal fixation.

Hospitals and specialty cardiac centers remain the primary end users, supported by investments in minimally invasive procedures and enhanced postoperative care. North America has maintained a leading position due to high surgical volumes and rapid product adoption, while Asia-Pacific is exhibiting a growing trajectory driven by expanding healthcare infrastructure.

Strategic collaborations, new product launches, and regulatory approvals have been observed as central competitive strategies across the market. Continued emphasis on patient safety and long-term clinical outcomes is expected to sustain innovation, thereby supporting the positive outlook for the global sternal closure systems market.

Key Takeaways

- In 2024, the sternal closure systems market generated revenue of US$ 2.7 billion, supported by a CAGR of 5.5%, and the market is projected to reach US$ 4.6 billion by 2033.

- The product landscape is categorized into closure devices and bone cement, with closure devices emerging as the leading segment in 2024, accounting for 58.5% of total revenue.

- Based on material, the market is segmented into stainless steel, polyether ether ketone (PEEK), titanium, and other materials. Titanium remained the most widely adopted material type, holding a 47.2% market share.

- In terms of application, the market is segmented into median sternotomy, hemisternotomy, bilateral thoracosternotomy, and other procedures. Median sternotomy dominated the segment in 2024, contributing 52.8% of overall revenue.

- Regionally, North America maintained its leadership position by capturing a 37.9% share of the global sternal closure systems market in 2024.

Regional Analysis

North America Leading the Sternal Closure Systems Market

North America accounted for the largest share of the sternal closure systems market, capturing 37.9% of total revenue. This leadership position was supported by measurable structural and clinical factors. The rising number of cardiovascular surgeries created a consistent demand base, with the American Heart Association reporting over 500,000 coronary artery bypass procedures conducted annually in the United States. Favorable reimbursement frameworks further strengthened adoption, as Centers for Medicare & Medicaid Services data indicated a 7% increase in approved claims for sternal closure procedures in 2023.

Technological progress also contributed to market expansion. FDA records documented the clearance of eight new closure devices between 2022 and 2024, including advanced titanium plating systems. Major industry participants responded by increasing output, with corporate reports noting 12–15% production capacity expansion during 2023. Procurement activities across healthcare facilities strengthened overall uptake, supported by American Hospital Association data showing a 10% rise in purchases of specialized systems in 2023. These combined factors reinforced North America’s dominant position in the global market.

Asia Pacific Expected to Achieve the Highest CAGR

The Asia Pacific region is anticipated to experience the fastest growth rate due to several quantifiable developments. China’s National Health Commission recorded a 15% year-over-year increase in cardiac surgeries in 2023, driving immediate demand for advanced closure technologies. India’s Ministry of Health and Family Welfare reported a US$ 200 million investment in cardiac care upgrades during 2023, strengthening regional infrastructure.

Japan showed significant procedural expansion, with the Ministry of Health, Labour and Welfare reporting a 9% rise in complex sternal surgeries in 2024. Regional manufacturers supported this momentum through 18–20% production expansions in 2023. Additionally, the Asia Pacific Society of Cardiology observed a 12% annual increase in specialized surgical training programs since 2022, indicating sustained growth in clinical capabilities. These indicators collectively reinforce the region’s trajectory as the fastest-growing market for sternal closure systems.

Emerging Trends

- Shift Toward Rigid Plate Fixation: The transition from traditional stainless-steel wire cerclage to titanium-based rigid plate fixation systems has accelerated. Rigid plate fixation has been associated with improved mechanical stability, faster osteogenesis, and reduced postoperative sternal complications. Since 2022, several systems—including BIOMET SternaLock Blu (K110574), Able Medical’s Valkyrie Thoracic Fixation System, and Medtronic’s Titan Sternal Fixation System—have obtained FDA 510(k) clearance, indicating rising clinical adoption.

- Increasing Use of Polymer and Composite Materials: Biocompatible polymers and composite materials, such as PEEK-based plates and polymer-coated compression bands, are being incorporated into sternal closure procedures. These materials offer advantages such as reduced imaging artifacts, improved patient comfort, and lighter weight. The availability of single-use polymer compression bands has supported simplified closure in primary and reconstructive cases while lowering the risks of instrument breakage and infection.

- Integration of Advanced Wound-Management Protocols: Clinical practice increasingly includes the combined use of vacuum-assisted closure (VAC) therapy followed by rigid plate stabilization for high-risk or infected sternotomy wounds. This staged approach has demonstrated improved mediastinitis control and accelerated healing outcomes, establishing it as a preferred method in complex postoperative wound management.

- Postoperative Use of External Supportive Devices: Adjunctive external supportive solutions, such as sternum-stabilizing corsets and bands (e.g., Stern-E-Fix), are being deployed to reduce wound dehiscence and superficial infections. Evidence from a randomized trial (n=380) indicated that such devices reduced infection rates to 3.4%, compared with 9.5% in the control group, while also lowering dehiscence incidence and shortening hospital stays.

Use Cases

- High-Risk Poststernotomy Patients: Rigid plate fixation has shown superior clinical outcomes in high-risk patients. In a multicenter randomized trial (n=140), sternal union at 6 months was achieved in 70% of patients treated with rigid plates compared with 24% using wire cerclage (p=0.003). Reduced postoperative pain (mean scores of 2.5 vs. 3.9 at 1 month) and decreased narcotic consumption were also documented.

- Patients With Poor Bone Quality: Titanium-based systems such as the Biomet Microfixation Sternal Closure System have been designed for both normal and osteoporotic sternums. The self-drilling screw mechanism eliminates predrilling requirements, ensuring stable fixation in compromised bone and mitigating the risk of sternal displacement.

- Management of Infected Sternotomy Wounds: A structured treatment protocol integrating VAC therapy followed by rigid plate fixation has been adopted for deep sternal wound infections. This approach reinforces infection control and provides stable mechanical support, facilitating successful fusion in mediastinitis cases.

- Emergency and Reconstructive Procedures: Single-use, polymer-coated compression systems are increasingly utilized in emergency re-entry situations and complex reconstructive procedures. These systems enable rapid stabilization, minimize dependence on wire-tying techniques, and reduce the likelihood of instrument failure, thereby improving procedural efficiency.

Frequently Asked Questions on Sternal Closure Systems

- Why are sternal closure systems used in cardiac surgery?

These systems are used to maintain chest stability following sternotomy procedures. Their use reduces risks such as sternal dehiscence, infection, and prolonged recovery, supporting improved patient outcomes and clinical efficiency in cardiac care. - What types of sternal closure systems are available?

Available systems include wire-based closures, rigid plate fixation devices, cable systems, and polymer-based materials. Each type is selected based on patient anatomy, surgical complexity, and the required level of postoperative stability. - What materials are commonly used in sternal closure systems?

Materials include titanium, stainless steel, and high-performance polymers such as PEEK. Titanium is commonly preferred due to its biomechanical strength, corrosion resistance, and compatibility with bone tissue during postoperative recovery. - Which product segment dominates the market?

Closure devices dominate the product landscape, accounting for over half of total revenue in 2024. Their dominance is attributed to strong clinical preference for rigid fixation systems, which offer enhanced stability and lower complication risks. - Which material segment holds the largest market share?

Titanium holds the leading share due to its superior strength and compatibility. Its increasing adoption across hospitals and surgical centers supports repeated market expansion and influences product innovation trends. - Which region leads the global sternal closure systems market?

North America leads the global market due to high cardiac surgery volumes, favorable reimbursement structures, and rapid adoption of technologically advanced closure systems. Strong healthcare infrastructure further reinforces its dominant position.

Conclusion

The global sternal closure systems market is projected to maintain steady growth, supported by rising cardiovascular disease prevalence, expanding surgical volumes, and continual advances in fixation technologies. Increased adoption of titanium-based rigid plate systems and biocompatible polymers has strengthened clinical outcomes and reduced postoperative risks.

North America continues to lead due to high procedure rates and strong reimbursement frameworks, while Asia Pacific is positioned for the fastest expansion as healthcare infrastructure improves. Ongoing product innovation, regulatory approvals, and strategic collaborations are expected to sustain market momentum, reinforcing a positive long-term outlook for sternal closure solutions worldwide.