Table of Contents

Overview

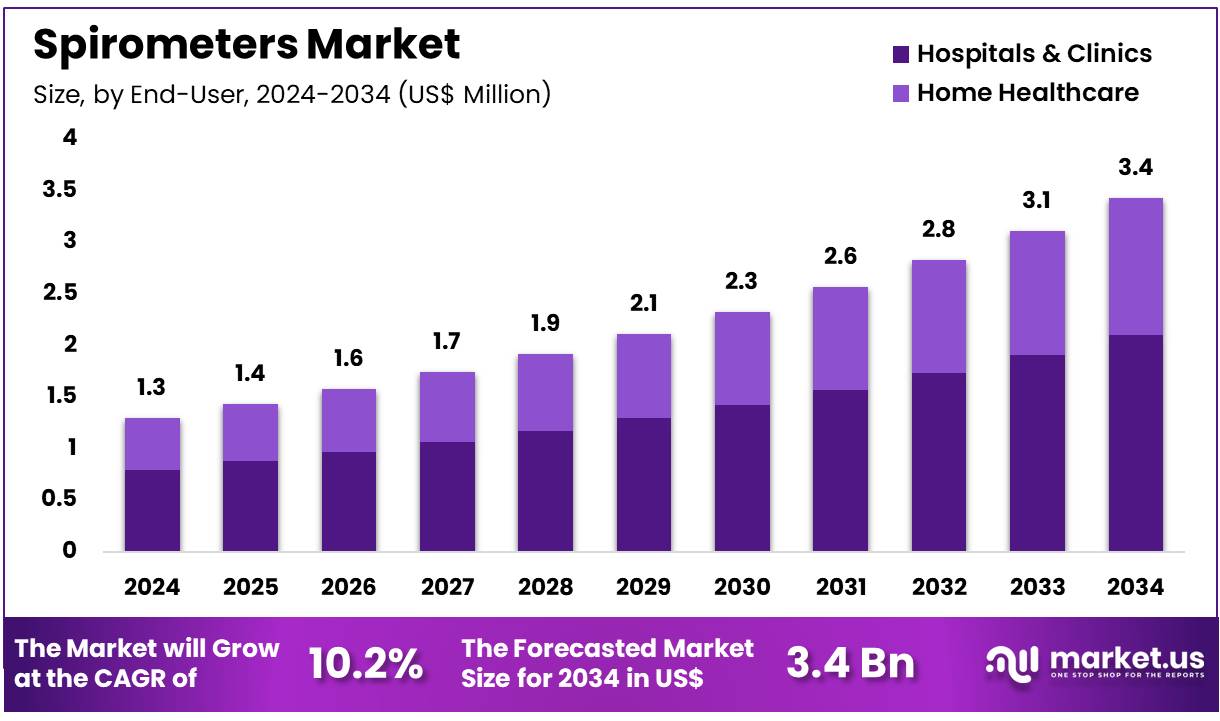

New York, NY – Nov 17, 2025 – Global Spirometers Market size is expected to be worth around US$ 3.4 Billion by 2034 from US$ 1.3 Billion in 2024, growing at a CAGR of 10.2% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 41.7% share with a revenue of US$ 0.5 Billion.

The global demand for spirometers has been observed to increase steadily as respiratory diagnostics continue to gain prominence across healthcare systems worldwide. The market has been supported by a rising prevalence of chronic respiratory diseases, including asthma, COPD, and post-infectious pulmonary complications. In response, the development of advanced spirometry devices has been accelerated, with emphasis placed on improved accuracy, portability, and integration with digital health platforms.

The adoption of spirometers has been further encouraged by an increase in clinical screening programs and strengthened public awareness of lung health. Hospitals, diagnostic centers, and primary care facilities have expanded the use of spirometry to support early detection and continuous monitoring of respiratory conditions. Technological enhancements, including real-time data capture and wireless connectivity, have been incorporated to enhance patient assessment and to enable streamlined clinical workflows.

Significant attention has also been directed toward home-care spirometers, as remote monitoring solutions continue to be preferred by patients and providers. Demand for compact and user-friendly devices has been reinforced by the growth of telemedicine, allowing respiratory function to be evaluated without physical clinical visits.

Market growth has been supported by ongoing innovation, regulatory approvals, and strategic investments by key manufacturers. The expansion of distribution networks across emerging regions has strengthened product accessibility and created new opportunities for industry participants.

This press release highlights the continued evolution of spirometer technologies and the steady progression of the respiratory diagnostics market. The increasing focus on preventive healthcare and digital respiratory monitoring is expected to contribute positively to future market development.

Key Takeaways

- In 2024, the spirometers market generated revenue of US$ 1.3 Billion, recorded a CAGR of 10.2%, and is projected to reach US$ 3.4 Billion by 2033.

- By product type, the market is categorized into devices, software, and consumables & accessories, with devices accounting for 55.8% of the market share in 2023.

- Based on technology, the market is segmented into volume measurement, peak flow measurement, and flow measurement, with flow measurement representing 52.4% of the share.

- In terms of application, the categories include asthma, pulmonary fibrosis, cystic fibrosis, COPD, and others, where COPD emerged as the dominant segment with a 41.5% revenue share.

- The end-user segmentation comprises hospitals & clinics and home healthcare, and hospitals & clinics led with 61.2% of the total revenue.

- North America held the leading position in 2023, capturing 41.7% of the global market share.

Market Segmentation Analysis

- Product Type Analysis: In 2023, the devices segment held a dominant 55.8% share, supported by the rising demand for accurate, portable, and easy-to-use spirometry solutions across clinical and home environments. Increasing cases of asthma and COPD continue to elevate device utilization. Advancements in digital connectivity, data accuracy, and diagnostic performance are strengthening product adoption. As healthcare providers prioritize early detection and cost-efficient monitoring, sustained growth of the devices segment is expected in the coming years.

- Technology Analysis: Flow measurement technology accounted for 52.4% of the market, driven by its capability to provide real-time and highly accurate lung function assessments essential for managing chronic respiratory diseases. Expanded spirometry use in asthma, COPD, and pulmonary fibrosis care has increased the need for precise airflow metrics. Innovations that improve device sensitivity, ease of use, and integration with digital platforms are enhancing market penetration. With growing demand for advanced respiratory monitoring, the flow measurement segment is anticipated to retain its leading position.

- Application Analysis: The COPD segment led with a 41.5% share, reflecting the rising global incidence of chronic obstructive pulmonary disease. COPD remains a major contributor to mortality, particularly among older adults and long-term smokers. Greater focus on early diagnosis and routine lung function testing is strengthening the role of spirometry in treatment pathways. As governments expand chronic disease management initiatives, demand for spirometers in COPD care is expected to grow steadily through broader diagnostic implementation.

- End-user Analysis: Hospitals and clinics accounted for 61.2% of the market, demonstrating strong dependence on clinical respiratory diagnostics. Increasing cases of asthma, COPD, and other lung disorders have positioned spirometry as a standard assessment tool in institutional care. This segment benefits from skilled personnel, integrated care systems, and structured diagnostic workflows. Growth in telemedicine and preventive screening programs is further supporting spirometry adoption, reinforcing continued expansion across global healthcare facilities.

Regional Analysis

North America Leading the Spirometers Market

North America dominated the spirometers market by capturing 41.7% of total revenue, supported by multiple structural and demographic factors. The increasing prevalence of respiratory conditions, including asthma and chronic obstructive pulmonary disease (COPD), has significantly raised the demand for spirometry testing. As reported by the Asthma and Allergy Foundation of America, nearly 25 million individuals in the United States were living with asthma in 2022, demonstrating a strong need for reliable diagnostic solutions.

Technological progress has resulted in the availability of advanced and user-friendly spirometers, strengthening adoption across clinical environments and home-based care. The rising inclination toward remote healthcare and convenient monitoring tools has further accelerated device utilization.

Moreover, a well-established healthcare ecosystem, coupled with substantial healthcare expenditure, has enabled broad access to respiratory diagnostic equipment. These combined factors supported strong market performance across North America in 2024.

Asia Pacific Expected to Record the Fastest CAGR

The Asia Pacific region is projected to register the highest CAGR over the forecast period, driven by significant demographic, environmental, and policy-related developments. The region’s aging population is expected to increase the demand for respiratory assessment solutions. According to United Nations estimates, the number of older individuals in Asia Pacific is poised to reach 1.3 billion by 2050, rising from 600 million in 2020.

Escalating air pollution in countries such as China and India is anticipated to heighten respiratory disease burden, thereby strengthening demand for spirometry devices. Government-led healthcare initiatives and growing awareness of early respiratory diagnosis are expected to further support market expansion. Collectively, these drivers are projected to contribute to strong and sustained growth in the Asia Pacific spirometers market during the forecast period.

Frequently Asked Questions on Spirometers

- What conditions are diagnosed using spirometers?

Spirometers are primarily used to diagnose asthma, chronic obstructive pulmonary disease, pulmonary fibrosis, and other respiratory disorders. They assist healthcare providers in identifying airflow limitations and assessing disease severity for accurate treatment planning. - Why is spirometry important in healthcare?

Spirometry is essential because it supports early detection of respiratory diseases, enables continuous monitoring of lung function, and helps physicians adjust treatment strategies. Its routine use improves patient outcomes and reduces complications associated with chronic lung conditions. - What factors are driving growth in the spirometers market?

Market growth is driven by increasing respiratory disease prevalence, rising pollution levels, technological advancements, and expanding home healthcare adoption. Improved awareness of early diagnosis further supports demand for advanced spirometry solutions worldwide. - Which regions dominate the spirometers market?

North America leads the market due to strong healthcare infrastructure, high disease burden, and rapid adoption of advanced diagnostic technologies. The region’s significant healthcare spending further enhances access to spirometry equipment across clinical settings. - Why is Asia Pacific expected to grow fastest in this market?

Asia Pacific is projected to grow rapidly because of its aging population, increasing air pollution, expanding healthcare access, and government initiatives focused on respiratory disease management. Rising awareness of diagnostic benefits strengthens regional demand for spirometers. - What types of spirometers are available?

Spirometers are available as desktop models, handheld devices, and portable systems designed for home use. These devices vary in functionality, accuracy, and connectivity features, supporting different clinical needs and patient monitoring requirements. - Who are the primary end users of spirometers?

Spirometers are widely used in hospitals, clinics, diagnostic centers, and home healthcare environments. Healthcare professionals rely on spirometry for diagnostic assessments, while patients use portable devices for ongoing respiratory monitoring at home. - How is technology influencing the spirometers market?

Technological advancements have introduced digital spirometers with wireless connectivity, real-time analytics, and integration with mobile applications. These innovations enhance accuracy, improve patient engagement, and support remote respiratory monitoring across various care settings.

Conclusion

The spirometers market continues to advance steadily, supported by rising respiratory disease prevalence, strong clinical adoption, and rapid technological innovation. Enhanced diagnostic accuracy, digital integration, and growing demand for home-based monitoring are strengthening global uptake. Dominance of devices, flow measurement technology, and COPD applications reflects the market’s clinical priorities, while hospitals and clinics remain essential end users.

North America leads due to established healthcare systems, whereas Asia Pacific is poised for the fastest growth driven by aging populations and pollution-related respiratory issues. Overall, expanding awareness and preventive healthcare initiatives are expected to sustain long-term market progression.