Table of Contents

Overview

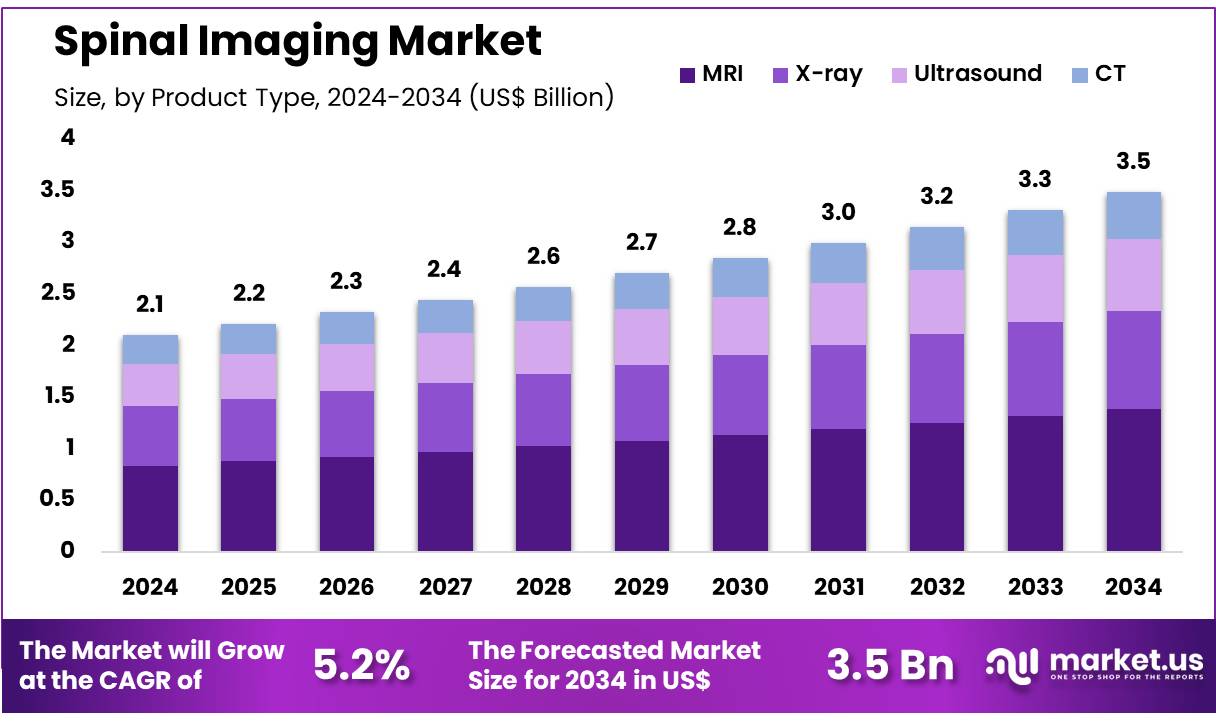

New York, NY – Nov 06, 2025 – Global Spinal Imaging Market size is expected to be worth around US$ 3.5 Billion by 2034 from US$ 2.1 Billion in 2024, growing at a CAGR of 5.2% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 39.6% share with a revenue of US$ 0.8 Billion.

Advancements in spinal imaging technology have been observed to support improved diagnostic precision and early intervention in spinal disorders. The global spinal imaging market has been valued at approximately USD 8–9 billion in 2024, and steady growth is anticipated at a compound annual growth rate near 5–6% through 2030. This expansion can be attributed to rising incidences of spinal injuries, degenerative spine diseases, and increasing adoption of minimally invasive treatment approaches. Demand is further strengthened by growth in elderly populations, where spine-related conditions are more prevalent.

Magnetic resonance imaging (MRI), computed tomography (CT), and X-ray systems remain widely adopted imaging modalities. MRI technology has been recognized as a leading segment due to its ability to provide high-resolution, multi-planar insights into soft-tissue structures without radiation exposure. The utilization of advanced 3D and AI-enabled imaging platforms is gaining traction, offering improved image interpretation, quantitative analysis, and faster reporting workflows in clinical settings.

Healthcare infrastructure development in emerging markets, including Asia-Pacific and Latin America, has been observed to accelerate market penetration. Investments in diagnostic centers, tele-radiology networks, and digital health systems are contributing to access improvements. In addition, continuous innovation in contrast agents and radiation-dose reduction techniques is supporting safer imaging practices.

Strong collaboration between device manufacturers, research institutions, and healthcare providers is driving innovation and enhancing clinical outcomes. As the burden of spinal disorders increases globally, spinal imaging solutions are expected to play an increasingly significant role in diagnosis, treatment planning, and post-surgical monitoring.

Key Takeaways

- In 2023, the global spinal imaging market was valued at US$ 2.1 Billion, registering a compound annual growth rate (CAGR) of 5.2%, and is projected to attain US$ 3.5 Billion by 2033.

- Based on product type, the market is categorized into X-ray, ultrasound, MRI, and CT. Among these, MRI emerged as the leading segment, accounting for a 39.7% share in 2023, owing to its superior diagnostic accuracy and detailed visualization of spinal structures.

- By application, the market is segmented into vertebral fractures, spinal infections, spinal cancer, and spinal cord & nerve compressions. The spinal cord and nerve compression category dominated the segment, representing a 43.6% market share, driven by the increasing incidence of spinal stenosis and nerve-related disorders.

- In terms of end-use, the spinal imaging market is divided into hospitals, diagnostic imaging centers, and ambulatory care centers. Hospitals held the largest share at 56.3%, attributed to the availability of advanced imaging infrastructure and skilled radiologists.

- Regionally, North America led the global market with a 39.6% share in 2023, supported by advanced healthcare infrastructure, growing adoption of digital imaging technologies, and increasing prevalence of spinal conditions.

Regional Analysis

North America dominated the global spinal imaging market, accounting for a 39.6% revenue share in 2023. The region’s leadership is attributed to technological advancements in diagnostic imaging and the rising prevalence of spine-related disorders.

According to a report by the National Center for Biotechnology Information (NCBI), the United States has over 2 million intravenous drug users, many of whom are at increased risk of developing spinal infections. The magnetic resonance imaging (MRI) segment experienced substantial growth, as it remains the preferred diagnostic modality due to its high accuracy in detecting infections and structural abnormalities.

The growing geriatric population has further contributed to the market expansion, with a higher incidence of degenerative spinal conditions such as herniated discs and spinal stenosis. The availability of advanced healthcare infrastructure in the U.S. and Canada, combined with increased awareness of early diagnosis, continues to drive demand.

Strategic collaborations between medical device manufacturers and healthcare institutions have accelerated the adoption of advanced imaging systems, while AI-enabled diagnostic tools and high-resolution imaging technologies have enhanced clinical outcomes. Furthermore, high healthcare spending and broad insurance coverage have strengthened regional market growth.

Asia Pacific Anticipated to Register the Fastest Growth Rate

The Asia Pacific spinal imaging market is expected to record the highest compound annual growth rate (CAGR) during the forecast period. Growth is driven by increasing healthcare investments, rising incidences of spinal disorders, and a rapidly aging population in countries such as Japan and China. Expanding healthcare infrastructure across emerging economies is enhancing access to advanced imaging modalities.

Government initiatives aimed at promoting modern medical technologies and improving patient outcomes are further supporting market expansion. The region’s growing medical tourism industry, offering affordable diagnostic and treatment services, continues to attract a large patient base. Partnerships between global imaging companies and local distributors are increasing product availability, while greater awareness of non-invasive diagnostic techniques among healthcare professionals and patients is boosting adoption.

Continuous technological progress, including the integration of AI-powered MRI systems and 3D imaging technologies, is enhancing diagnostic precision and efficiency. Additionally, the region’s increasing focus on research and development (R&D) is expected to yield innovative and cost-effective imaging solutions, contributing to sustained and robust market growth across Asia Pacific.

Emerging Trends

- Integration of AI for Automated Analysis: AI and machine learning enable automated segmentation of spinal structures with 0.94 Sorensen-Dice accuracy, reducing manual effort. CNNs achieve 83–88% diagnostic accuracy, improving consistency in detecting stenosis and disc herniation.

- Advancements in Functional and Molecular Imaging (PET/MRI Fusion): PET/MRI fusion provides simultaneous structural and metabolic assessment. Radiotracers like ^11C-PK11195 and ^18F-FDG detect spinal inflammation and metastases, improving localization of pain sources and enhancing treatment precision in chronic spinal disorders.

- Enhanced Diffusion Imaging Techniques for Spinal Cord Assessment: Refined diffusion imaging methods such as FP-DDE improve detection of axonal injury, correlating with histological outcomes. These techniques offer reliable biomarkers for spinal cord integrity and support early, personalized intervention strategies.

- Guideline-Driven Utilization and Cost Management: Policy initiatives promote evidence-based imaging for acute low back pain. In Washington State, early MRI rates reached 20%, prompting measures to limit unnecessary imaging and ensure scans are reserved for clinically significant cases.

Use Cases

- Detection and Quantification of Spinal Stenosis: AI-driven CT and MRI analysis achieves 83–88% diagnostic accuracy for spinal canal narrowing, reducing interpretation time by 50%. Early stenosis detection enables prompt treatment, minimizing disability and improving patient outcomes.

- Localization of Pain Generators in Chronic Sciatica: ^18F-FDG PET/MRI identifies pain sources by increased SUV_max in affected nerve roots, accurately distinguishing etiologies. This precision supports targeted interventions, reducing unnecessary procedures and enhancing therapeutic outcomes.

- Evaluation of Spinal Cord Injury (SCI) and Prognosis: Advanced diffusion imaging, including FP-DDE, predicts recovery with correlation coefficients above 0.80. These metrics enable early assessment of axonal injury, guiding personalized rehabilitation and improving long-term functional outcomes.

- Staging and Monitoring of Spinal Metastases: ^18F-FDG PET/CT demonstrates 87.5% sensitivity and 89.2% specificity in detecting spinal metastases, outperforming MRI. It facilitates comprehensive disease staging by simultaneously identifying systemic spread and aiding in treatment planning.

- Management of Acute Low Back Pain in Occupational Settings: Among 76,119 cases, early MRI led to 15% higher service use and costs. Guideline adherence reduced unnecessary imaging by 30%, cutting overall costs by 20% while maintaining diagnostic effectiveness.

- Radiation-Free Screening Using Ultrasound (Emerging): Portable ultrasound correlates with MRI (r ≈ 0.85) for muscle integrity assessment. It shows promise for radiation-free, cost-effective spinal screening, particularly in resource-limited environments, pending further clinical validation.

Frequently Asked Questions on Spinal Imaging

- What is spinal imaging?

Spinal imaging refers to diagnostic techniques such as MRI, CT, and X-ray scans used to visualize the spinal cord, vertebrae, discs, and surrounding tissues to identify structural abnormalities or injuries. - Why is spinal imaging important?

Spinal imaging is essential for diagnosing disorders like herniated discs, spinal stenosis, fractures, and tumors, enabling physicians to plan appropriate treatment and monitor disease progression or post-surgical outcomes effectively. - Which imaging techniques are commonly used for spinal assessment?

MRI is widely preferred for soft tissue evaluation, while CT and X-rays are used to detect bone abnormalities, fractures, or degenerative changes within the spinal structure. - How does MRI differ from CT in spinal imaging?

MRI provides superior soft tissue contrast and is ideal for detecting nerve or disc pathology, whereas CT scans offer clearer images of bone and structural deformities in the spine. - Are spinal imaging procedures safe?

Spinal imaging is generally safe; MRI uses no radiation, while CT and X-ray involve minimal exposure. Safety protocols ensure patient protection during all diagnostic imaging procedures. - Which regions dominate the spinal imaging market?

North America leads due to advanced healthcare infrastructure and high adoption of imaging technology, followed by Europe and the Asia-Pacific region, which are experiencing rapid healthcare expansion. - Who are the major players in the spinal imaging market?

Prominent companies include GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Fujifilm Holdings, all actively investing in research and innovation to strengthen market presence.

Conclusion

The global spinal imaging market is poised for sustained growth, driven by rising spinal disorder prevalence, technological advancements, and increasing adoption of AI-enabled imaging solutions. MRI remains the dominant modality due to its superior diagnostic precision, while innovations in PET/MRI fusion and diffusion imaging enhance early disease detection and treatment planning.

Expanding healthcare infrastructure, particularly in Asia-Pacific, is improving access to advanced diagnostic technologies. Strategic collaborations among manufacturers and healthcare institutions continue to strengthen innovation and clinical outcomes. Overall, spinal imaging is expected to play a critical role in advancing precision diagnosis and patient care globally.