Table of Contents

Overview

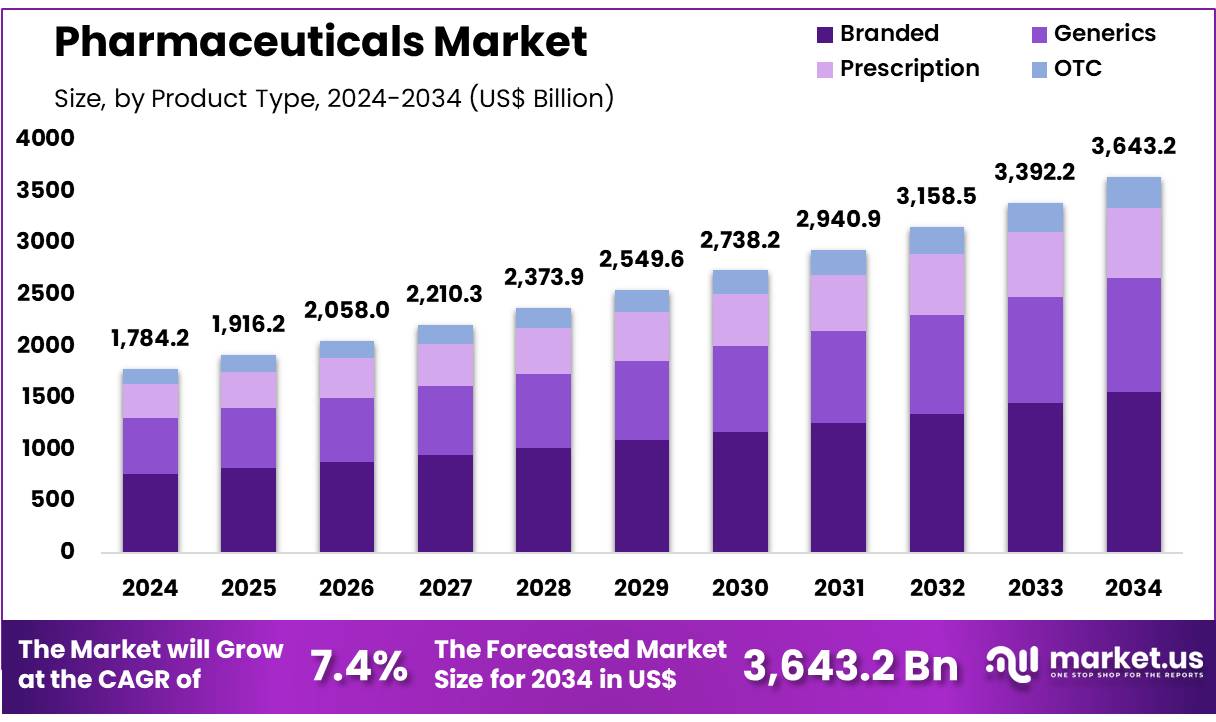

New York, NY – Nov 07, 2025 – Global Pharmaceuticals Market size is expected to be worth around US$ 3643.2 billion by 2034 from US$ 1784.2 billion in 2024, growing at a CAGR of 7.4% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 39.6% share with a revenue of US$ 706.5 Billion.

The global pharmaceuticals market has been characterized by steady expansion, supported by rising healthcare expenditure, sustained innovation, and increasing demand for advanced therapeutic solutions. The growth of the market has been attributed to the rising prevalence of chronic and infectious diseases, which has encouraged wider adoption of prescription and specialty drugs. Strong investments in research and development have continued to strengthen the introduction of novel molecules, biosimilars, and targeted therapies.

The market has been further shaped by the expansion of manufacturing capabilities, the integration of digital technologies, and the adoption of data-driven drug development processes. Regulatory support for accelerated approvals and emphasis on patient safety have reinforced the pace of innovation across key therapeutic categories including oncology, cardiovascular disorders, neurological conditions, and metabolic diseases.

A significant increase in generic drug consumption has been observed, driven by cost-efficiency requirements in both developed and emerging economies. Growth in biologics and personalized medicine has also been recorded, supported by advances in genomics and precision diagnostics. North America has maintained a leading position due to its established healthcare infrastructure and high R&D intensity, while Asia Pacific has demonstrated strong potential with rapid improvements in healthcare access and domestic manufacturing.

The outlook for the pharmaceuticals market remains positive, with continued advancements in treatment technologies and supportive policy frameworks expected to reinforce global demand. Rising focus on sustainable production, improved supply chain resilience, and expansion of digital health ecosystems are anticipated to shape market development over the forecast period.

Key Takeaways

- The pharmaceuticals market is projected to reach approximately USD 3,643.2 billion by 2034, increasing from USD 1,784.2 billion recorded in 2024. The expansion of the market is being supported by continuous advancements in drug development, rising disease prevalence, and sustained healthcare investments.

- In terms of product type, the market has been segmented into branded, generics, prescription, and OTC medications. Branded pharmaceuticals accounted for the largest share in 2023, representing 42.7% of total revenue. This dominance has been attributed to strong adoption of innovative therapies and higher R&D intensity.

- Based on route of administration, the market includes oral, topical, parenteral, inhalation, and other formulations. Oral drugs held a significant share of 48.5%, supported by ease of administration and broad patient acceptance.

- With respect to application, the market has been categorized into cardiovascular diseases, cancer, diabetes, and other therapeutic areas. Cardiovascular treatments emerged as the leading segment, capturing 37.8% of revenue due to the rising incidence of heart-related conditions and growing demand for long-term therapies.

- The end-user landscape consists of hospitals, clinics, and other healthcare facilities. Hospitals remained the primary end-user group, accounting for 54.3% of revenue, driven by higher patient inflow and advanced treatment capabilities.

- Regionally, North America maintained its leadership position with a 39.6% share in 2024, supported by robust healthcare infrastructure and significant pharmaceutical spending.

Regional Analysis

North America accounted for the largest share of the pharmaceuticals market, representing 39.6% of total revenue. This dominance has been driven by rising demand for chronic disease treatments and continuous advancements in drug development. According to a 2021 study published by the US Bone and Joint Initiative, arthritis affects approximately 7 out of every 100 individuals aged 18 to 44, while nearly half of those aged 65 and above experience some form of the condition.

The increasing prevalence of age-related and lifestyle-related diseases has supported the expansion of treatments for arthritis, diabetes, and cardiovascular disorders. Significant investments in research and development have encouraged the introduction of biologics and personalized therapies, contributing to improved clinical outcomes. Government efforts aimed at enhancing drug accessibility and affordability, including expanded insurance coverage, further supported regional market growth.

Adoption of digital health technologies such as AI-enabled drug discovery tools and telepharmacy services has strengthened distribution efficiency. In addition, the strong presence of biotechnology firms and pharmaceutical manufacturers has improved supply chain capabilities and accelerated the development of next-generation treatments, reinforcing North America’s leadership position.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is anticipated to register the fastest CAGR over the forecast period, supported by increasing healthcare investment and rising demand for advanced pharmaceuticals. A 2023 publication by the Indian Ministry of Finance reported that national healthcare spending increased from 1.4% of GDP in 2018 to 1.9% in 2023, indicating improved investment in medical infrastructure and drug access.

Expanding healthcare coverage across China, India, and Japan is expected to enhance access to essential medications. Policy measures promoting domestic pharmaceutical manufacturing are projected to lower production costs and reduce reliance on imports. The growing incidence of chronic diseases, combined with an aging population, is expected to increase demand for innovative and long-term therapies.

Rising investments in biotechnology, precision medicine, and targeted treatment development are anticipated to advance therapeutic innovation. Strategic collaborations between global pharmaceutical companies and regional players are likely to strengthen research capacity and distribution networks. Increasing adoption of digital healthcare platforms, including e-pharmacies and AI-based diagnostic tools, is expected to further support the strong growth outlook for Asia Pacific.

Emerging Trend

The adoption of artificial intelligence in drug development has increased steadily. Regulatory authorities reported receiving more than 500 drug-related submissions containing AI components between 2016 and 2023. Draft guidance released in early 2025 outlines how AI should be applied to support decisions on safety, effectiveness, and quality, ensuring that data produced through these systems meet established regulatory expectations and maintain patient protection.

Antimicrobial resistance continues to influence research priorities within the pharmaceutical sector. Between 2021 and 2023, the pipeline of antibacterial agents expanded from 80 to 97 candidates, reflecting renewed focus on difficult-to-treat infections caused by resistant organisms. Despite this growth, experts have indicated that additional innovative compounds are required to counter pathogens that no longer respond to current therapies, emphasizing the need for sustained investment in antibacterial R&D.

Strengthening pharmaceutical supply chains has become a key area of action to prevent the circulation of substandard or falsified products. A WHO working group established in 2024 has been developing measures to improve excipient quality and detect contaminated raw materials before manufacturing. Complementary training programs are also being prepared to assist countries in identifying falsified medicines distributed online. These efforts aim to protect public health by maintaining the safety and integrity of global medicine supply systems.

Digital health technologies are reshaping the way drug safety and performance are monitored. The global digital health strategy for 2020–2025 promotes the use of real-time data platforms capable of tracking patient outcomes, identifying adverse events quickly, and supporting remote clinical trials. By integrating tools such as telemedicine systems and mobile health applications, regulators and manufacturers seek to expand access to essential medicines and generate richer real-world evidence on treatment effectiveness.

Use Cases

Antiretroviral therapy remains central to HIV management in low- and middle-income countries. By the end of 2020, more than 25 million people were receiving treatment worldwide. Forecasts indicate that, based on current trends and country-specific targets, between 30.6 million and 35.6 million individuals may be on antiretroviral therapy by 2025, highlighting expanding access to essential HIV medicines.

Antimalarial drugs continue to play an essential role in international health programs. In 2025, U.S. foreign aid is expected to support roughly 14 million treatment courses each year, while also supplying about one-quarter of antiretroviral medicines in select regions. This level of funding supports consistent drug availability, although experts caution that a disruption of only two to three months could result in stock-outs before seasonal demand peaks, demonstrating the sensitivity of disease control efforts to supply chain stability.

AI in regulatory submissions has reshaped components of pharmaceutical development. From 2016 to 2023, more than 500 drug applications utilized AI-generated analyses, including predictive modeling for clinical trial performance and AI-based quality assessment during manufacturing. These applications demonstrate how digital tools are being used to accelerate development, improve analytical accuracy, and enhance regulatory submissions under continued oversight to ensure patient safety.

Generic drug manufacturers have benefited from new regulatory resources aimed at improving product quality and reducing review times. In early 2025, the FDA provided webinars and guidance focused on strengthening abbreviated new drug applications. These materials address recurring issues such as weaknesses in analytical methods and outline best practices for demonstrating bioequivalence. Adoption of these resources allows companies to shorten approval timelines and expand access to lower-cost medicines.

Frequently Asked Questions on Pharmaceuticals

- How are pharmaceuticals developed?

Pharmaceutical development follows a structured process that includes discovery, preclinical studies, clinical trials, and regulatory review. This multistage pathway is designed to confirm product effectiveness and minimize safety risks before authorization for commercial manufacturing and distribution. - What are generic drugs?

Generic drugs are equivalent versions of branded medicines that become available after patent expiry. Their quality, dosage, safety, and clinical performance are required to match the original product, enabling cost-efficient treatment access without compromising therapeutic outcomes. - What factors affect pharmaceutical pricing?

Pharmaceutical pricing is influenced by research investments, regulatory compliance costs, manufacturing complexity, and competitive dynamics. Market exclusivity, patent protection, and reimbursement policies further shape final price structures across regions and healthcare systems. - What drives growth in the pharmaceuticals market?

Market growth is attributed to advancements in biotechnology, increasing diagnostic capabilities, higher patient awareness, and aging populations. Expansion is further supported by favorable regulatory reforms and rising investments in personalized medicine, biologics, and targeted therapeutic approaches. - How is technology impacting the pharmaceuticals market?

Technology adoption has accelerated drug discovery, improved manufacturing efficiency, and enhanced patient monitoring. Artificial intelligence, automation, and advanced analytics are being integrated to optimize trial design, reduce development timelines, and support data-driven decision frameworks. - What are biologics and how do they differ from traditional drugs?

Biologics are complex medicines derived from living organisms and are used to treat chronic and immune-related conditions. Their structural complexity and production methods differ from traditional chemical drugs, resulting in higher development costs and stricter manufacturing standards.

Conclusion

The global pharmaceuticals market is expected to demonstrate sustained expansion, supported by rising disease prevalence, growing healthcare investment, and continued innovation in drug development. Strong uptake of branded therapies, increasing generic utilization, and advancements in biologics and personalized medicine are reinforcing market performance across major regions.

Digital health integration, regulatory support, and strengthened supply chain systems are further enhancing industry resilience. North America is projected to remain dominant, while Asia Pacific is anticipated to record the fastest growth. Overall, market prospects remain positive as technological progress, policy initiatives, and expanding treatment access continue to shape long-term development.