Table of Contents

Overview

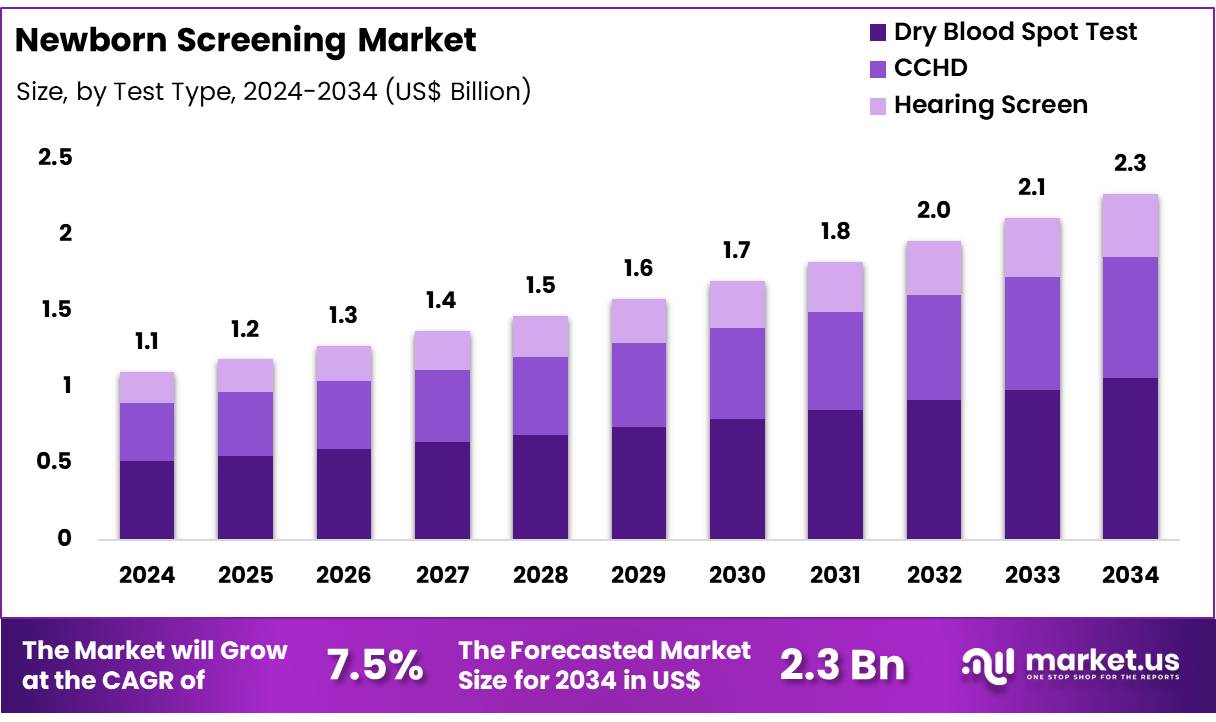

New York, NY – Nov 26, 2025 – Global Newborn Screening Market size is expected to be worth around US$ 2.3 Billion by 2034 from US$ 1.1 Billion in 2024, growing at a CAGR of 7.5% during the forecast period from 2025 to 2034. In 2024, Asia Pacific led the market, achieving over 37.2% share with a revenue of US$ 0.4 Billion.

Newborn screening is recognized as a critical public health program designed to identify serious, rare, and treatable conditions in infants shortly after birth. Early detection enables timely interventions, and the overall survival and long-term health outcomes of affected newborns are significantly improved. The program has been implemented widely across global healthcare systems, and its expansion has been supported by advances in diagnostic technologies.

The screening process typically includes a heel-prick blood test, hearing assessment, and evaluation for critical congenital heart disease. The blood test facilitates the detection of metabolic, endocrine, and genetic disorders, while hearing and cardiac screenings support the identification of sensory and structural abnormalities. The method is safe, minimally invasive, and completed within the first 24 to 48 hours of life.

The growth of newborn screening programs has been driven by rising awareness among healthcare professionals and parents, the increasing incidence of genetic and metabolic disorders, and supportive government policies. According to public health authorities, more than 4 million infants are screened annually in many developed regions, and early diagnosis has prevented severe disability and mortality in a significant proportion of cases.

Ongoing advancements in molecular diagnostics, tandem mass spectrometry, and genomic sequencing have strengthened the scope of screening panels. Broader adoption of these technologies is expected to enhance diagnostic accuracy and expand the number of detectable conditions. Continued collaboration between policymakers, clinicians, and research organizations is expected to support program sustainability and ensure equitable access to newborn screening worldwide.

Key Takeaways

- Market Size: The global newborn screening market is projected to reach approximately US$ 2.3 billion by 2034, increasing from US$ 1.1 billion in 2024.

- Market Growth: The overall market is expected to expand at a CAGR of 7.5% throughout 2025–2034.

- Product Analysis: The instruments segment accounted for 65.3% of total revenue, indicating strong reliance on advanced analytical systems.

- Application Analysis: The tandem mass spectrometry segment remained dominant with a 29.4% share.

- End-Use Analysis: In 2024, segmentation by test type showed the dry blood spot (DBS) test leading the market with a 46.7% share.

- Regional Analysis: In 2024, Asia Pacific emerged as the leading regional market, capturing over 37.2% share and generating US$ 0.4 billion in revenue.

Regional Analysis

In 2024, Asia Pacific held a leading position in the newborn screening market, accounting for over 37.2% of the total share and reaching a market value of US$ 0.4 billion. Growth in this region has been supported by increasing birth rates and the expansion of national healthcare programs. Government-led screening initiatives in countries such as India and China have strengthened early detection of metabolic and genetic disorders. In addition, rising awareness and continuous improvements in healthcare infrastructure are contributing to steady market development across Southeast Asia.

Conversely, North America continues to represent a mature and technologically advanced market for newborn screening. The region maintained a substantial share in 2024, supported by mandatory screening policies, particularly within the United States. Data from the Centers for Disease Control and Prevention (CDC) indicate that all U.S. states conduct screening for more than 30 core conditions.

Strong involvement of public health agencies, coupled with high levels of awareness among parents and healthcare professionals, has sustained market demand. Furthermore, the availability of advanced laboratory systems and skilled personnel continues to reinforce North America’s position in delivering early diagnostic interventions for newborns.

Emerging Trends

- Expansion of Screening Panels: The Recommended Uniform Screening Panel (RUSP) in the United States has expanded from 28 core conditions in 2006 to 36 by August 2022. This expansion has supported earlier detection of a broader spectrum of treatable disorders, including severe combined immunodeficiency and critical congenital heart disease.

- Adoption of Point-of-Care Testing: Screening for two major conditions hearing loss and critical congenital heart disease—has shifted to point-of-care settings. This development has reduced diagnostic delays and enabled immediate follow-up interventions before the newborn is discharged.

- Global Implementation Guidance: In March 2024, the World Health Organization introduced regional guidance to advance universal newborn screening across South-East Asia. The guidance emphasizes early screening for hearing impairment, eye abnormalities, and neonatal jaundice to reduce preventable disabilities through standardized testing protocols.

- Data-Driven Quality Improvement: The CDC’s ED3N pilot program is implementing a new data platform designed to enhance disease detection using dried blood spot samples. Advanced analytics are being applied to improve screening accuracy and strengthen the ability of state programs to introduce additional conditions.

Use Cases

- Detection of Metabolic and Genetic Disorders: Approximately 4 million infants are screened annually in the United States, with nearly 12,500 diagnosed with a core disorder equivalent to about one in every 300 births. Early diagnosis and treatment of conditions such as phenylketonuria and medium-chain acyl-CoA dehydrogenase deficiency can prevent severe long-term disabilities.

- Identification of Hearing Loss: Early Hearing Detection and Intervention (EHDI) programs now provide almost universal coverage across the United States. More than 98% of newborns have access to standardized hearing screening, enabling timely device fitting and early speech-language therapy.

- Global Screening Coverage in Low-Resource Regions: Globally, only about 28% of the 140 million annual births approximately 40 million infants undergo newborn screening. In Latin America, screening coverage is estimated at 50% of the region’s 11 million annual births. In the Asia-Pacific region, around 5 million infants are screened annually, while programs in the Middle East test approximately 7 million newborns per year.

- Immediate Clinical Decision Support: Point-of-care screening for critical congenital heart disease enables real-time pulse oximetry testing before discharge. This approach has reduced late diagnoses by up to 50%, thereby improving early-life survival outcomes.

Frequently Asked Questions on Newborn Screening

- Why is newborn screening important?

Newborn screening is important because most screened conditions show no immediate symptoms at birth. Early detection ensures infants receive critical interventions that prevent life-threatening complications, supporting improved survival rates and long-term developmental outcomes. - What tests are included in newborn screening?

Typical newborn screening includes a heel-prick blood test, hearing assessment, and screening for critical congenital heart disease. These tests identify metabolic disorders, genetic abnormalities, and sensory deficits before symptoms develop, enabling earlier intervention and effective disease management. - When is newborn screening performed?

Newborn screening is usually conducted within 24 to 48 hours after birth. This timeframe ensures the timely collection of samples while allowing adequate physiological changes necessary for accurate metabolic and genetic disorder detection. - Are newborn screening tests safe for infants?

Newborn screening tests are considered safe, minimally invasive, and quick. The heel-prick causes mild, brief discomfort, but the benefits of early detection significantly outweigh any temporary distress experienced by the infant. - What is driving growth in the newborn screening market?

Market growth is being driven by rising birth rates, expanded screening programs, technological advancements, and government support. Increased awareness and the adoption of advanced diagnostic tools also contribute to strong and steady market expansion globally. - Which products dominate the newborn screening market?

Instruments dominate the market due to their essential role in delivering accurate and high-throughput testing. Advanced analytical platforms, such as mass spectrometers, are widely utilized to support expanding screening panels and improved diagnostic reliability. - Which region leads the newborn screening market?

Asia Pacific leads the market, supported by rising births, government-backed programs, and expanding healthcare infrastructure. Substantial investments in national screening initiatives and improved diagnostic capabilities have positioned the region at the forefront of global adoption. - What technological advancements influence market growth?

Advancements in tandem mass spectrometry, molecular diagnostics, and genomic sequencing influence market progress. These technologies enhance sensitivity, enable multi-condition detection, and expand testing panels, improving the accuracy and efficiency of newborn diagnostic programs worldwide.

Conclusion

The global newborn screening market is experiencing steady and sustained expansion, supported by rising birth rates, strengthened public health policies, and continued technological progress. Growth has been reinforced by broader adoption of tandem mass spectrometry, molecular diagnostics, and point-of-care testing, which has improved early detection of metabolic, genetic, and sensory disorders.

Regional programs, particularly in Asia Pacific and North America, have ensured high screening coverage and improved clinical outcomes. As healthcare systems prioritize early diagnosis and equitable access, the market is expected to maintain robust momentum, driven by expanding screening panels and increased investment in advanced diagnostic infrastructure.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)