Table of Contents

Overview

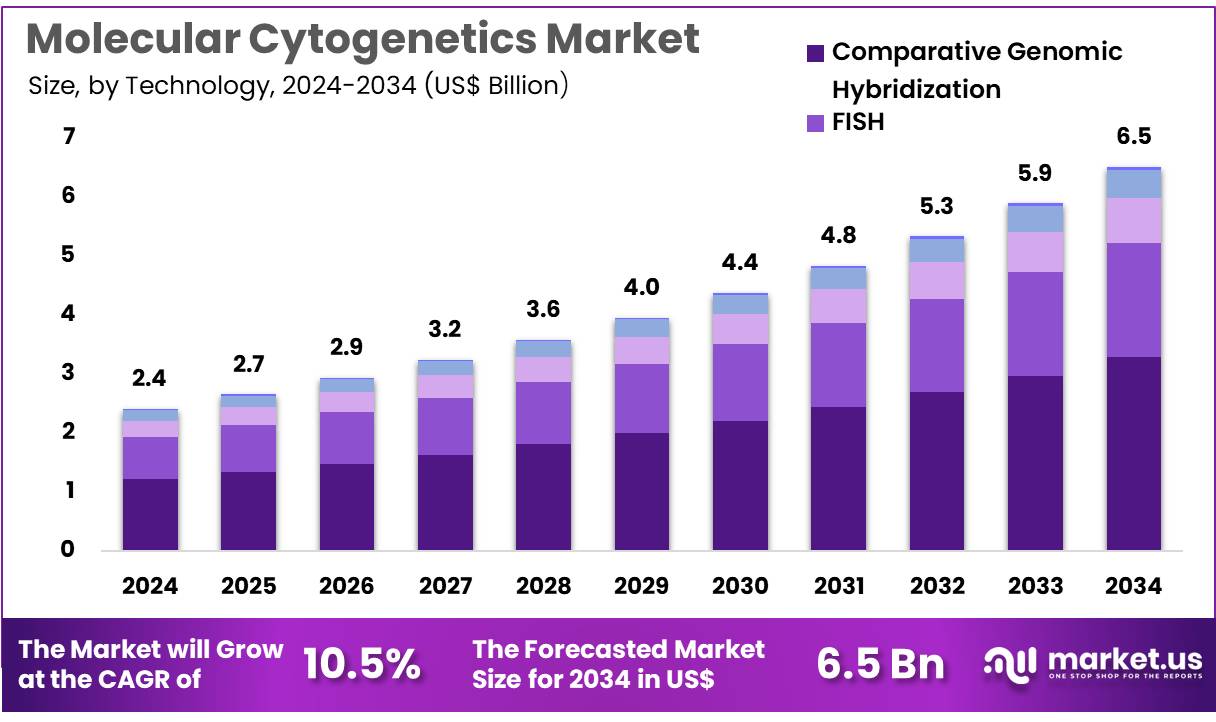

New York, NY – Nov 18, 2025 – Global Molecular Cytogenetics Market size is expected to be worth around US$ 6.5 Billion by 2034 from US$ 2.4 Billion in 2024, growing at a CAGR of 10.5% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 44.9% share with a revenue of US$ 1.1 Billion.

The global molecular cytogenetics market is being shaped by rapid advances in genomic technologies and increasing demand for precision diagnostic solutions. Molecular cytogenetics has been recognized as a critical discipline that integrates cytogenetic techniques with molecular biology tools to detect chromosomal abnormalities with high resolution and accuracy. The growth of the market has been attributed to the rising incidence of genetic disorders, cancer prevalence, and the expanding adoption of personalized medicine.

Technological advancements, including fluorescence in situ hybridization (FISH), comparative genomic hybridization (CGH), and next-generation sequencing (NGS)-based cytogenetic applications, have improved diagnostic efficiency and accelerated clinical decision-making. Increasing investments in research and development by biotechnology companies and academic institutions have further supported the expansion of advanced testing platforms.

The market has also been influenced by the growing use of molecular cytogenetics in prenatal and postnatal diagnostics, oncology testing, and drug development. High demand for early and accurate detection of chromosomal changes has strengthened the uptake of these technologies in clinical laboratories and research facilities. In parallel, the availability of automated imaging systems and AI-enabled analysis tools has enhanced laboratory productivity and reduced interpretation time.

North America and Europe have maintained strong market positions due to established healthcare infrastructures and high testing adoption rates. Emerging economies in Asia-Pacific are witnessing increasing penetration as healthcare expenditure rises and awareness regarding genetic testing improves. Overall, the molecular cytogenetics market is expected to demonstrate steady growth, supported by continuous innovation and expanding clinical applications.

Key Takeaways

- In 2024, the Molecular Cytogenetics market generated revenue amounting to US$ 2.4 Billion. The market has been expanding at a compound annual growth rate of 10.5% and is projected to reach US$ 6.5 Billion by 2033.

- The product type segment comprises instruments, consumables, and software & services. Consumables accounted for the leading share in 2024, representing 61.5% of the total market.

- Based on technology, the market is categorized into comparative genomic hybridization, FISH, immunohistochemistry, karyotyping, and other methods. Comparative genomic hybridization dominated this segment with a share of 50.4%.

- In terms of application, the market is segmented into genetic disorders, oncology, personalized medicine, and others. The oncology segment held the dominant position, contributing 54.2% of total revenue.

- Regarding end users, the market is divided into clinical & research laboratories, hospitals & path labs, academic research institutes, pharmaceutical & biotech companies, and others. Clinical & research laboratories remained the primary contributors, accounting for 47.9% of market revenue.

- Regionally, North America led the global market in 2024 by capturing a share of 44.9%.

Regional Analysis

North America is leading the Molecular Cytogenetics Market

North America dominated the market with the highest revenue share of 44.9% owing to several key factors. A significant contributor was the rising incidence of genetic disorders and cancers in the region. The Centers for Disease Control and Prevention (CDC) reported that approximately 1,519,907 people in the US were living with or in remission from leukemia, lymphoma, or myeloma in 2022. This surge in cancer cases heightened the demand for advanced diagnostic techniques, including molecular cytogenetics, to facilitate early detection and personalized treatment strategies.

Additionally, the robust research and development infrastructure in North America played a pivotal role. The National Institutes of Health (NIH) allocated substantial funding towards genomic research, with the National Human Genome Research Institute (NHGRI) receiving a budget of approximately US$616 million in 2022. Such investments have fostered technological advancements in chromosome analysis tools, thereby expanding the applications of molecular cytogenetics in clinical diagnostics and research.

Furthermore, the region’s well-established healthcare infrastructure and the presence of key industry players have facilitated the rapid adoption of innovative cytogenetic techniques, contributing to market growth.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing prevalence of genetic disorders and cancers. For example, China reported approximately 4.8 million new cancer cases in 2022, underscoring a substantial need for advanced diagnostic solutions.

Additionally, the region’s improving healthcare infrastructure and rising healthcare expenditures are expected to facilitate the adoption of molecular cytogenetic technologies. Government initiatives aimed at enhancing early disease detection and personalized medicine are also likely to drive market growth.

Moreover, collaborations between local healthcare providers and international industry leaders are anticipated to introduce cutting-edge cytogenetic techniques to the Asia-Pacific market, further propelling its expansion. The increased focus on precision medicine and genomic research in countries such as India and Japan is also expected to contribute to the rising demand for molecular cytogenetics in the region.

Emerging Trends

- Integration of High-Throughput Sequencing: The adoption of high-throughput sequencing has been integrated into molecular cytogenetics workflows, supporting the detection of novel chromosomal rearrangements, fusion genes, and somatic mutations. This approach has expanded analytical resolution beyond classical banding techniques and has been widely applied in cancer research to identify therapeutic targets and resistance mechanisms.

- Whole-Genome Sequencing for Disease Surveillance: Whole-genome multilocus sequence typing (wgMLST) has been implemented by public health agencies to enhance pathogen monitoring and disease tracking. In 2022, the CDC reported that surveillance coverage for culture-positive tuberculosis cases reached 96.0% after shifting from conventional genotyping to wgMLST, demonstrating increasing reliance on genomic epidemiology in public health systems.

- Long-Read Sequencing for Structural Variant Resolution: Advancements in long-read sequencing have been incorporated into cytogenetic analysis to improve structural variant detection. These platforms can span challenging genomic regions, including repetitive and GC-rich sequences, enabling more accurate identification of complex rearrangements. Supported by the NHGRI Genome Technology Program, recent developments have demonstrated the feasibility of analyzing molecules exceeding 1,000 nucleotides, advancing the creation of comprehensive cytogenomic maps.

Use Cases

- Tuberculosis Outbreak Detection: Molecular cytogenetic methodologies have been applied to monitor tuberculosis transmission patterns. In 2022, whole-genome sequencing was used to genotype 96.0% of culture-positive TB cases in the United States, enabling rapid linkage of cases with identical genomic signatures and supporting targeted outbreak containment efforts.

- Cancer Screening Follow-Up: The CDC reported that approximately 4 million individuals, representing 21.6% of the U.S. population, underwent cancer screening in 2020. A subset required follow-up genetic testing when cytogenetic abnormalities were suspected. Assays such as fluorescence in situ hybridization (FISH) have been used to confirm chromosomal alterations in tumor samples, supporting precise diagnosis and treatment planning.

- Clinical Genomic Profiling in Hematologic Malignancies: In conditions such as acute myeloid leukemia (AML) and myelodysplastic syndromes (MDS), whole-genome sequencing has been examined as an alternative to traditional cytogenetic techniques. Studies have shown that genomic profiling can be completed within clinically actionable timelines, improving the detection of cryptic rearrangements and informing the selection of targeted therapeutic strategies.

Frequently Asked Questions on Molecular Cytogenetics

- What is molecular cytogenetics?

Molecular cytogenetics is a discipline that combines molecular biology and cytogenetics to analyze chromosomal structure and function. It is widely applied for identifying chromosomal abnormalities, gene rearrangements, and genetic markers using techniques such as FISH and comparative genomic hybridization. - What are the key applications of molecular cytogenetics?

Major applications include cancer diagnostics, genetic disorder detection, prenatal and postnatal screening, and pharmacogenomic studies. The technology enables accurate detection of chromosomal aberrations, supporting targeted therapeutic decisions and improving the overall understanding of complex genetic mechanisms. - How does molecular cytogenetics support cancer research?

Cancer research utilizes molecular cytogenetics to identify chromosomal translocations, gene amplifications, and deletions. These insights assist in determining tumor behavior, predicting therapeutic responses, and shaping personalized treatment strategies based on precise genomic alterations observed within malignant cells. - What advantages does molecular cytogenetics offer over traditional cytogenetics?

Molecular cytogenetics provides higher resolution, faster analysis, and more accurate detection of subtle chromosomal changes. These capabilities strengthen diagnostic reliability, facilitate early disease detection, and support comprehensive genomic profiling compared to conventional microscopy-based cytogenetic assessments. - Which products are commonly offered in the molecular cytogenetics market?

The market includes FISH probes, aCGH arrays, reagents, consumables, imaging systems, and software. These products enable advanced chromosomal analysis and are increasingly incorporated into clinical diagnostics, research laboratories, and pharmaceutical development programs globally. - Which regions dominate the molecular cytogenetics market?

North America leads due to strong healthcare infrastructure, advanced research capabilities, and higher adoption of genomic technologies. Significant growth is also observed in Asia-Pacific, driven by expanding diagnostic capacity, increasing investments, and rising awareness of genetic testing. - Which end-users contribute most to market demand?

Hospitals, diagnostic laboratories, academic institutes, and pharmaceutical companies represent primary end-users. Their demand is supported by growing integration of genetic testing, rising oncology workloads, and increased utilization of chromosomal analysis in both clinical and translational research settings.

Conclusion

The molecular cytogenetics market has been advancing steadily, supported by rising genetic disease prevalence, growing oncology diagnostics, and expanding adoption of precision medicine. Continuous technological progress in FISH, CGH, and sequencing-based cytogenetic tools has strengthened diagnostic accuracy and broadened clinical utility.

Increased R&D investments and the emergence of automated and AI-enabled platforms have enhanced workflow efficiency across laboratories. Strong demand from clinical and research institutions, combined with robust healthcare systems in North America and rapid adoption in Asia-Pacific, is expected to sustain market expansion. Overall, the market is positioned for continued growth driven by innovation and widening applications.