Table of Contents

Overview

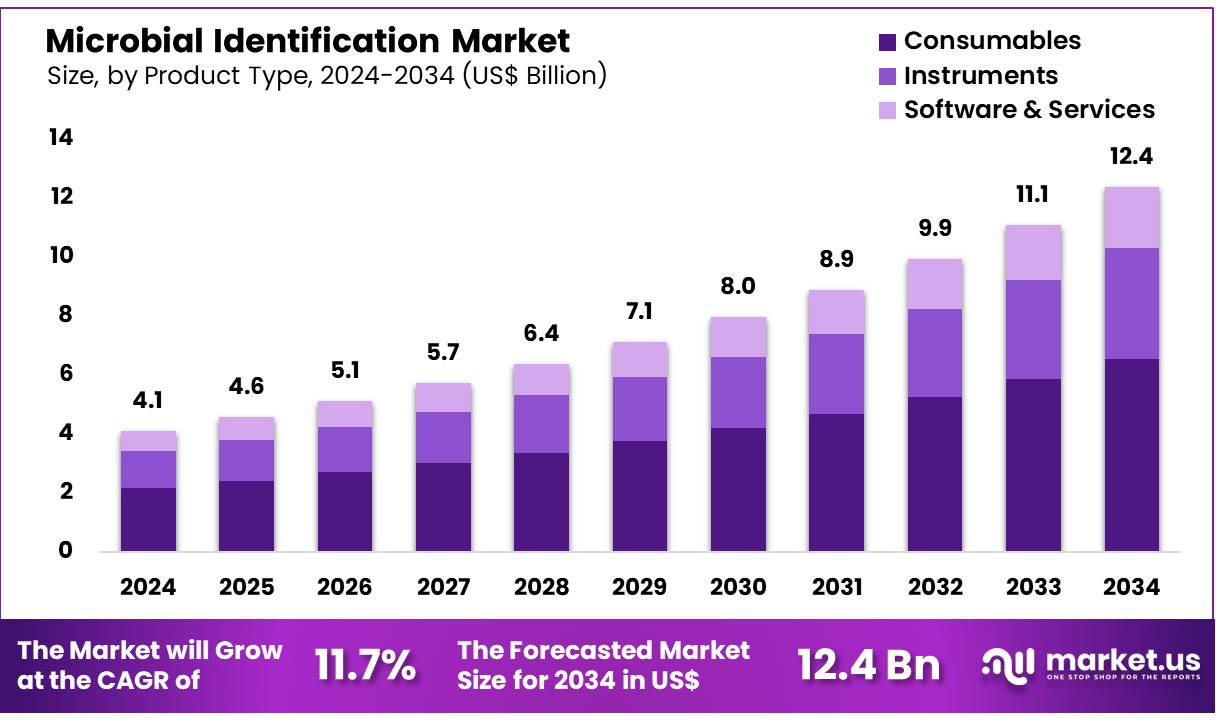

New York, NY – Nov 14, 2025 – Global Microbial Identification Market size is expected to be worth around US$ 12.4 Billion by 2034 from US$ 4.1 Billion in 2024, growing at a CAGR of 11.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.1% share with a revenue of US$ 1.6 Billion.

The microbial identification market has been expanding as demand for rapid and accurate diagnostic solutions has increased across healthcare, pharmaceuticals, food safety, and environmental monitoring. The growth of the market can be attributed to the rising incidence of infectious diseases, the increasing focus on contamination control, and the wider adoption of advanced technologies in laboratory workflows.

The market has been shaped by the integration of molecular diagnostics, mass spectrometry, and automated microbial identification systems, which have enabled higher precision and faster turnaround times. Consistent investments in biotechnology and clinical microbiology have supported the adoption of these systems in hospitals, research institutions, and industrial laboratories.

The expansion of pharmaceutical manufacturing and the enforcement of stringent regulatory standards for quality assurance have further strengthened demand. The use of microbial identification in drug development, sterility testing, and contamination prevention has become a critical component of quality management practices.

Significant growth has also been observed in the food and beverage sector, where microbial identification technologies have been deployed to ensure product safety and compliance with international standards. The rising preference for reliable detection methods has encouraged the development of automated platforms that reduce manual errors and enhance operational efficiency.

Overall, the microbial identification market is positioned for sustained growth, supported by continuous technological innovation, increasing research activities, and the growing need for dependable microbial testing across industries. The market outlook remains positive as organizations prioritize safety, quality, and early detection capabilities.

Key Takeaways

- The microbial identification market generated US$ 4.1 billion in 2024, and with a CAGR of 11.7%, it is projected to reach US$ 12.4 billion by 2033.

- By product type, the market is categorized into instruments, consumables, and software & services, with consumables accounting for 52.7% of the market share in 2024.

- Based on technology, the segmentation includes PCR, next-generation sequencing, microarrays, mass spectrometry, and others, with PCR holding a 42.2% share.

- In terms of application, the market is divided into pharmaceuticals, food & beverage testing, environmental applications, clinical diagnostics, and others, with clinical diagnostics dominating at 55.3%.

- By method, the market is split into proteotypic, phenotypic, and genotypic methods, and genotypic methods lead with a 49.5% revenue share.

- Considering end users, the market includes pharmaceutical and biotechnology companies, hospitals & diagnostic laboratories, food testing laboratories, and others, with hospitals & diagnostic laboratories representing 53.8% of the market.

- North America remained the leading regional market, holding 38.1% of the share in 2024.

Segmentation Analysis

- By Product Type Analysis: The consumables segment accounted for a dominant 52.7% share of the microbial identification market in 2023. The segment’s growth was driven by continuous demand for reagents, media, and essential laboratory supplies required for routine microbial testing. Increased incidence of infectious diseases and rising focus on environmental and industrial hygiene further supported consumption levels. The expanding use of automated identification systems, which depend heavily on recurring consumable inputs in diagnostic and pharmaceutical workflows, is expected to reinforce this segment’s continued expansion.

- Technology Analysis: PCR technology represented 48.2% of the market, supported by its precision, sensitivity, and rapid pathogen detection capabilities. Its broad use in clinical and research laboratories enabled early disease detection and supported outbreak monitoring efforts. The ability of PCR to identify extremely low quantities of microbial DNA positioned it as a core diagnostic tool. Ongoing advancements, including real-time and multiplex PCR, have further enhanced efficiency, ensuring its sustained preference across healthcare and biotechnology applications.

- Application Analysis: The clinical diagnostics segment captured a leading 55.3% market share, reflecting the growing global burden of infectious diseases and the rising need for rapid and reliable diagnostic solutions. Microbial identification technologies play an essential role in guiding clinical decision-making and managing antimicrobial resistance threats. The segment is also supported by the increasing adoption of personalized medicine and the prioritization of early disease detection. Continued investment by healthcare institutions in advanced diagnostic capabilities is expected to sustain future growth.

- Method Analysis: Genotypic methods held a 49.5% share, indicating a clear shift toward molecular approaches that provide high precision in microbial identification. Techniques such as PCR and DNA sequencing deliver highly accurate results through detailed analysis of microbial genetic material. Their use is particularly important for identifying multi-drug-resistant organisms and characterizing complex microbial communities. With the broader availability of high-throughput sequencing platforms, genotypic identification methods are projected to maintain significant momentum in both clinical and research environments.

- End-user Analysis: Hospitals and diagnostic laboratories accounted for 53.8% of the total market, reflecting their central role in infectious disease detection and management. The need for accurate and timely diagnostic information during outbreaks has accelerated the adoption of advanced microbial identification tools in these settings. The increasing reliance on molecular technologies such as PCR and next-generation sequencing further supports market penetration. Continued investment in modern diagnostic infrastructure is expected to sustain this segment’s leading position.

Regional Analysis

North America emerged as the leading region in the microbial identification market, accounting for the highest revenue share of 38.1%. The increased prevalence of infectious diseases, including respiratory infections, gastrointestinal illnesses, and sexually transmitted infections, supported the rising demand for accurate and rapid microbial identification systems. Data from the US Centers for Disease Control and Prevention (CDC) indicated a continued rise in antimicrobial resistance (AMR) cases, underscoring the necessity for advanced diagnostic tools.

Technological advancements in polymerase chain reaction (PCR) and mass spectrometry accelerated detection capabilities, improving both accuracy and speed. Regulatory approvals from the US Food and Drug Administration (FDA) further strengthened market growth by ensuring the safety and reliability of newly developed diagnostic devices. Healthcare providers increasingly adopted integrated platforms combining diagnostic instruments with software solutions, contributing to broader utilization of microbial identification technologies across clinical settings.

The Asia Pacific region is expected to record the fastest CAGR over the forecast period. The World Health Organization (WHO) has reported a high burden of infectious diseases such as tuberculosis and malaria, particularly in India and China. Rapid population growth and urbanization in these countries are anticipated to raise the need for improved healthcare services, including diagnostic testing.

Government initiatives aimed at upgrading healthcare infrastructure, including increased healthcare budgets and enhanced disease surveillance programs, have further supported market expansion. WHO recommendations to strengthen antimicrobial resistance monitoring are also expected to stimulate the adoption of microbial identification technologies. With rising investments and strategic focus on combating infectious diseases, the Asia Pacific market is projected to witness substantial growth in the coming years.

Frequently Asked Questions on Microbial Identification

- What is microbial identification?

Microbial identification refers to the systematic determination of microorganisms at the genus or species level. The process is based on phenotypic, biochemical, or molecular characteristics, enabling accurate differentiation of bacteria, fungi, and other microbes for research, diagnostics, and quality control applications. - Why is microbial identification important?

The importance of microbial identification is linked to its role in contamination control, disease diagnosis, product safety, and regulatory compliance. Accurate identification enables risk mitigation, supports infection management, and ensures that pharmaceutical, food, and environmental processes meet global quality standards. - Which techniques are commonly used for microbial identification?

Common microbial identification techniques include biochemical assays, culture-based methods, MALDI-TOF mass spectrometry, polymerase chain reaction, and genomic sequencing. These methods are selected based on sensitivity, turnaround time, and required accuracy levels across industrial, clinical, and environmental settings. - How is molecular identification different from traditional culture methods?

Molecular identification relies on nucleic acid analysis, offering higher accuracy and speed than culture-based techniques, which depend on microbial growth. Molecular tools detect slow-growing or non-culturable organisms, supporting rapid decision-making in diagnostics, food safety, and pharmaceutical manufacturing. - Which industries are major users of microbial identification technologies?

Major users include pharmaceuticals, biotechnology, clinical diagnostics, food and beverage processing, environmental testing, and water quality assessment. These sectors apply microbial identification to ensure safety, comply with standards, and maintain product integrity across production and quality assurance workflows. - What technology trends are shaping the market?

Key trends include the adoption of MALDI-TOF instruments, genomic sequencing platforms, automated microbial analyzers, and AI-driven interpretation software. These technologies support faster identification, improved accuracy, and lower operational costs, strengthening their use in regulated and high-throughput environments. - Which regions hold the largest share of the microbial identification market?

North America and Europe hold the largest market shares due to advanced healthcare infrastructure, strong regulatory frameworks, and early adoption of modern technologies. Rapid industrialization and rising healthcare investments are driving significant incremental growth in Asia-Pacific markets.

Conclusion

The microbial identification market is expected to maintain strong momentum as demand for rapid, precise, and automated diagnostic solutions continues to rise across healthcare, pharmaceuticals, food safety, and environmental monitoring.

Advancements in molecular diagnostics, PCR, sequencing, and automated platforms have strengthened accuracy and efficiency, supporting broader adoption in clinical and industrial settings. Regulatory requirements, increasing infectious disease burdens, and enhanced focus on contamination control further contribute to sustained expansion. With growing investments in research, diagnostics infrastructure, and technological innovation, the market is well-position